Cheese Packaging Market Overview: Barrier Films, Shelf-Life Innovation, and Circular Materials Driving USD 6.8B by 2034

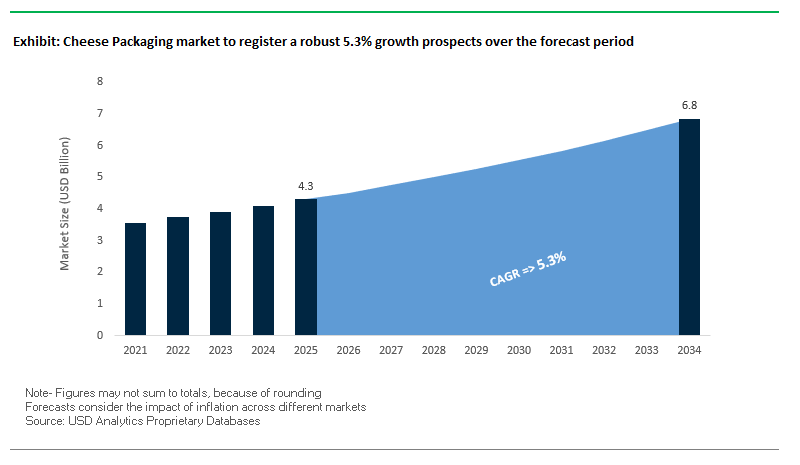

Market value & growth. The cheese packaging market is projected to rise from USD 4.3 billion in 2025 to USD 6.8 billion by 2034, at a CAGR of 5.3%. Demand is underpinned by the need to preserve freshness, extend shelf life, and ensure food safety while meeting aggressive sustainability and recyclability targets across retail and foodservice.

What professionals need to know. Natural cheese accounts for the largest share and over 61% requires specialized barrier packaging to control oxygen and moisture transmission critical for texture, flavor, and microbial stability in products such as cheddar and mozzarella. Semi-rigid formats (trays, cups) capture a significant revenue share by balancing protection, cost, and shelf presentation. Technology roadmaps prioritize advanced barrier films, vacuum skin packaging (VSP), and mono-material (mono-PE/mono-PP) structures to minimize waste and support closed-loop recycling. With >70% of consumers prioritizing sustainable packaging, procurement decisions increasingly weigh PCR content, compostability, and recyclability by design alongside machinability and total cost of ownership.

Key Insights for buyers and ops leaders

- Barrier-first specs: For natural cheese, optimize OTR/WVTR via multilayer films, lidding webs, and VSP to cut spoilage and returns.

- Semi-rigid advantage: Trays/cups offer impact resistance, merchandising appeal, and line efficiency at lower weight than rigid alternatives.

- Shelf-life extension: High-barrier films and VSP reduce food waste and enable longer distribution windows and DTC/e-grocery models.

- Sustainability as a KPI: Scale recycle-ready mono-PE/mono-PP, raise PCR content, and pilot bio-based/compostable options where infrastructure exists.

Market Analysis: From Smart Traceability to Mono-Material Wins (2024–2025)

Cheese pack users are accelerating the shift to smart, transparent, and recyclable formats. In August 2025, adoption of QR/RFID-enabled smart packaging grew across dairy aisles to enhance traceability, consumer education, and authentication a response to retailer data needs and origin-verification demands. June 2025 saw ALPMA debut SAN Fresh for cheese counters, targeting on-counter freshness and shelf-life gains for artisanal SKUs without compromising sensory attributes.

Consolidation and material science breakthroughs are reshaping supply options. The Amcor–Berry merger (May 2025) is set to concentrate film innovation, PCR access, and global converting capacity, potentially improving service breadth for cheese processors. On the line-integration front, Harpak-ULMA and Cabinplant (March 2025) announced pre-integrated systems that combine dosing, handling, and primary/secondary packaging to raise OEE and cut changeover time for sliced, shredded, and cubed cheese. Regulatory winds also favor renewables: the EU’s January 2025 initiative to promote renewable materials boosts investment in paper-based, recyclable, and compostable structures.

Sustainability moved from pilots to scale. Mondi + Skånemejerier (November 2024) repackaged ICA’s Hushållsost into mono-PP designed for recycling, validating store-ready, circular cheese films. Active packaging R&D is accelerating with October 2024 research showing whey-derived bio-active films that can add 5–10 days of shelf life. Brands are embedding PCR: Cabot Creamery (July 2024) shifted its 8-oz bars to 30% PCR content, demonstrating drop-in compatibility with existing lines and retailer recyclability messaging.

Emerging Trends and Opportunities Defining the Future of the Cheese Packaging Market

Accelerated Adoption of High-Barrier, Lightweight Recyclable Monomaterials

The global cheese packaging market is undergoing a decisive transformation as brands and suppliers pivot from multi-material laminates to recyclable mono-material packaging formats. This shift is strongly driven by regulatory mandates such as the European Union’s Packaging and Packaging Waste Regulation (PPWR), which requires all packaging to be designed for recyclability by 2030. Under the new framework, recyclability grades will directly impact Extended Producer Responsibility (EPR) fees, making complex laminates less economically viable for cheese brands. This has created a surge in demand for polyolefin- and polyethylene-based recyclable films.

Corporate sustainability commitments are reinforcing this transition. Danone, for example, has pledged that 100% of its packaging will be reusable, recyclable, or compostable by 2030, with a particular focus on eliminating virgin fossil-based plastics. To meet these mandates, suppliers are advancing solutions such as ProAmpac’s “ProActive Recycle-Ready” films, introduced in August 2025. These polyolefin-based high-barrier films offer puncture resistance and shelf-life protection for chunk cheeses while being compatible with existing polyethylene recycling streams. By aligning with both regulatory pressures and consumer expectations for sustainable packaging, recyclable monomaterials are becoming the cornerstone of innovation in cheese packaging.

Advanced Modified Atmosphere Packaging (MAP) and Smart Spoilage Indicators for Premium Products

Alongside sustainability, food safety and shelf-life extension remain critical innovation areas in cheese packaging. The latest research in modified atmosphere packaging (MAP) emphasizes dynamic gas blends and gas-scavenging components tailored to specific cheese varieties. For fresh mozzarella, which is highly perishable, optimized CO₂ and N₂ ratios preserve freshness, texture, and microbiological safety, reducing spoilage rates in retail and distribution.

In parallel, the industry is adopting smart freshness indicators that provide real-time insights into product quality. These chemical sensors or colorimetric labels shift color based on pH changes, temperature abuse, or the presence of spoilage compounds. This innovation replaces static “best before” dates with dynamic freshness cues, empowering consumers to make informed consumption decisions and reducing household food waste. Premium cheese brands view this technology as a way to differentiate their offerings while reinforcing consumer trust. Together, MAP optimization and smart packaging create a dual value proposition prolonging shelf life while enhancing transparency in food safety.

Development of Effective Compostable Formats for Fresh Mozzarella and Specialty Cheeses

The next frontier in cheese packaging lies in compostable solutions that can safely contain high-moisture products like mozzarella and ricotta while preserving quality. Traditional biodegradable films have struggled with durability and barrier properties, but new research is addressing this challenge. Cellulose-based films with advanced coatings are showing promise in managing “purge” while maintaining optimal moisture retention. These bio-based formats could redefine packaging for fresh cheeses by aligning performance with compostability.

Competitive Landscape: High-Barrier Performance, Automation, and Recycle-Ready Portfolios

The competitive field blends materials science leaders, automation specialists, and fiber-based transit experts. Vendors differentiate on barrier performance, food safety credentials, sustainability by design, and global service networks.

Amcor PLC advances recycle-ready films for branded cheese

• Flexible films, shrink bags, and rigid containers with a strategic tilt to AmPrima® mono-PE/mono-PP for recycle-ready cheese applications.

• Recognized for recycle-ready grated cheese packaging (Cathedral City) an award-winning proof point for circular retail film.

• Deep materials science and ASSET LCA services help spec lower-impact solutions without sacrificing machinability or seal integrity.

• Scale high-barrier, mono-material structures that run on existing equipment, reducing conversion risk and changeover cost.

Sealed Air (CRYOVAC®) extends shelf life with high-barrier shrink systems

• CRYOVAC® barrier shrink bags, forming webs, and lids engineered for oxygen/moisture control and microbial stability.

• Gold standard for case-ready cheese and foodservice packs where sanitary design and consistent seals are non-negotiable.

• Food science + automation expertise via global Packaging Design Application Centers to co-optimize film, tray, and sealing jaws.

• Expand solutions for retail and foodservice while enabling SME processors through e-commerce channels and turnkey support.

Constantia Flexibles secures flavor with high-barrier dairy films

• Flexible wrappers for soft cheese, pouches for hard cheese, and aluminum-based systems (outer shell, lid, tear strip) for processed cheese.

• High-barrier know-how preserves flavor and texture, limiting oxidation and moisture gain across chilled chains.

• End-to-end dairy expertise and formats that bridge premium shelf appeal with line speed and seal reliability.

• Position as a one-stop dairy packaging partner with sustainable, regulation-ready solutions across countries and retail specs.

Mondi Group scales mono-material, designed-for-recycling cheese films

• Plastic and paper-based solutions with a focus on mono-material PP/PE films and paper-where-possible concepts.

• Mondi + Skånemejerier launched mono-PP Hushållsost packs an award-winning reference for circular dairy.

• Integrated model from material R&D to converting to tailor barrier + machinability for shredded, sliced, and block cheeses.

• “Sustainable by design” roadmap: expand recyclable/reusable/compostable offerings that clear retailer recyclability marks.

Smurfit Kappa fortifies cold-chain logistics with fiber-based transit packs

• Corrugated bulk and secondary solutions for industrial and retail cheese logistics.

• PackExpert models precise strength needs by route, stack, and temperature, cutting damage and optimizing board grade.

• ISTA-certified test labs and global footprint safeguard bulk blocks and multi-packs, reducing breakage and CO₂ per shipped unit.

• Engineer recyclable, high-performance corrugated that complements primary films and improves e-grocery/outbound compliance.

Tekni-Plex delivers high-barrier cups and lidding for on-the-go dairy

• High-barrier cups, lids, and flexible films tuned for freshness and safety in snacking and portion control.

• Supports the growth of on-the-go cheese snacks with oxygen/moisture barriers that protect taste and texture.

• Materials science capability and custom engineering for line-fit, seal peels, and retort/ESL where required.

• Invest through a dedicated Consumer Products division to accelerate sustainable, performance-led cheese formats.

Cheese Packaging Market Share Insights

Market Share by Material in the Cheese Packaging Industry

Plastic dominates the global cheese packaging market with a 65% share in 2025, driven by its unmatched ability to extend shelf life while balancing convenience and product visibility. Multi-layer flexible films, vacuum-sealed pouches, and rigid plastic tubs offer superior barrier protection against oxygen, moisture, and light, ensuring preservation across shredded, sliced, and soft cheese categories. The rise of resealable formats such as zip locks and peel-and-reseal lids further strengthens plastic’s position by catering to consumer demand for convenience and portion control. Paper and paperboard account for 25% of the market, gaining traction due to sustainability mandates and consumer preference for eco-friendly solutions. Their role in breathable wraps for hard cheeses like Gouda and Cheddar, along with structural cartons for cream cheese tubs and gourmet wheels, ensures they remain integral despite lower barrier performance compared to plastics. Metal and glass represent niche but vital roles in specialty packaging. Tinplate cans preserve processed cheese powders and shelf-stable products, while glass jars support premium offerings such as feta and mozzarella balls in oil, where product visibility and a premium aesthetic are paramount. Innovative biodegradable films, including PLA-based and compostable polymers, form a small but critical “Other” category, representing the industry’s response to plastic reduction pressures and signaling the future direction of sustainable cheese packaging innovation.

Market Share by Cheese Type in the Cheese Packaging Industry

Processed cheese holds the largest market share at 40%, reflecting its immense global volume and wide array of packaging requirements, from individually wrapped slices to aerosol cheese cans. This segment drives innovation in hermetic sealing, portion-controlled packaging, and flexible single-serve solutions, cementing its role as the most packaging-intensive cheese type. Hard and semi-hard cheeses account for 30% of the market, balancing between vacuum-sealed plastic for long shelf life and breathable wax paper or specialty cheese paper that supports aging. Their dual packaging requirements highlight the blend of preservation and tradition demanded by both retail and artisanal distribution channels. Soft cheeses like Brie and Camembert represent a smaller but high-value segment, requiring packaging that carefully manages gas exchange and moisture retention. Specialized multi-layer plastics and paperboard boxes with selective permeability are critical to maintaining texture and preventing ammonia buildup during storage. Fresh cheeses such as Mozzarella, Ricotta, and Cottage cheese are heavily dependent on refrigerated, high-barrier plastic tubs or cups with sealed lids, reflecting their short shelf life and high moisture content. Although smaller in overall volume compared to processed cheese, these categories emphasize the precision engineering of packaging materials to balance preservation, freshness, and consumer appeal.

Market Share by End-Use in the Cheese Packaging Industry

Retail dominates the cheese packaging industry with a 75% market share, underscoring the role of packaging as both a protective barrier and a powerful marketing tool in competitive dairy aisles. High-clarity films, innovative printing, and resealable features are critical in this segment, where packaging differentiates brands, communicates freshness, and drives impulse purchases. The rise of convenience-driven formats such as single-serve snack packs and family-size resealable bags further accelerates retail’s dominance. Foodservice applications, accounting for 25% of the market, emphasize bulk efficiency over branding. Packaging in this segment is designed for durability, ease of handling, and portion control, featuring 5-pound bags of shredded cheese, industrial tubs of cream cheese, and large blocks designed for in-house shredding. Unlike retail, the foodservice sector prioritizes functionality and cost efficiency, with minimal investment in aesthetics. This balance between high-volume retail competition and cost-driven foodservice needs underscores the dual nature of demand shaping the global cheese packaging market.

United States: Sustainable, Convenient, and Smart Packaging Driving Cheese Market Growth

The United States cheese packaging market is evolving rapidly, with sustainability emerging as a key driver. Manufacturers are investing in mono-material films and post-consumer recycled (PCR) content for rigid trays and containers, aligning with corporate sustainability goals and consumer demand for eco-friendly products. This shift reflects broader U.S. trends toward a circular economy in food packaging, especially in dairy. Additionally, innovations in advanced barrier technology are extending shelf life by protecting cheese from oxygen and moisture, which reduces food waste and ensures premium freshness across both hard and soft cheese segments.

Convenience and consumer engagement are equally reshaping the U.S. cheese packaging landscape. Demand for single-serve cheese packs, resealable closures, and easy-open formats is increasing in response to the rise of on-the-go snacking. Snack packs featuring cheese cubes and sticks highlight this trend, particularly among younger consumers. At the same time, smart packaging innovations such as QR codes for traceability, recipe sharing, and product information are enhancing consumer experience and brand loyalty. Together, these shifts are making the U.S. one of the most dynamic and innovation-led cheese packaging markets globally.

Germany: Circular Economy and Artisan Cheese Needs Redefining Packaging Standards

Germany is leading the European cheese packaging market with a strong focus on circular economy principles. Driven by the EU’s Packaging and Packaging Waste Regulation (PPWR), companies are innovating with recyclable and reusable materials designed to meet strict sustainability targets. The collaboration between MBM Innovations and dsm-firmenich, which developed a new cheese maturation membrane eliminating the need for coatings, exemplifies how technological partnerships are directly reducing food waste and shaping the future of eco-friendly cheese packaging in Europe.

The German market also has a unique demand profile driven by its artisan and traditional cheese culture. Packaging must allow cheeses to breathe while managing humidity and oxygen levels, ensuring proper flavor maturation. This has resulted in specialized packaging designs that balance sustainability with functional performance. With Germany’s dual emphasis on sustainability and artisanal authenticity, the country is setting benchmarks for the global cheese packaging sector.

France: Protecting Heritage Cheeses with Eco-Design and Safety-First Packaging

France’s cheese packaging market is strongly influenced by its rich heritage and global reputation for regional specialty cheeses such as Camembert and Roquefort. Protecting the integrity of these products is a priority, with innovations in specialized aeration systems that support natural maturation and preserve authenticity. Packaging design in France plays a crucial role in safeguarding geographic indications while maintaining product quality throughout distribution.

Sustainability and compliance with European regulations are also central. French companies, including Knauf Industries, are developing eco-designed trays and lids that use recyclable and environmentally friendly materials. Moreover, strict food safety regulations drive demand for packaging that maintains the organoleptic qualities of cheese while ensuring protection against contamination. France stands out as a market where packaging innovation seamlessly blends sustainability, regulatory compliance, and cultural preservation.

United Kingdom: Recyclability, Trade Efficiency, and Premium Cheese Packaging Trends

The United Kingdom’s cheese packaging sector is adapting to post-Brexit realities and government-led sustainability initiatives. New trade agreements with the EU are set to ease cross-border movement of British cheese by reducing sanitary and phytosanitary (SPS) checks, increasing the importance of packaging designed for faster transit and extended shelf life. At the same time, the U.K. government’s Extended Producer Responsibility (pEPR) program is pushing companies toward recyclable solutions and transparent recyclability assessments, aligning industry practices with sustainability targets.

The market is also witnessing growth in premium and artisan cheese consumption, which demands high-quality, visually appealing packaging that communicates product value. Producers are investing in packaging that combines aesthetic appeal with functional features, such as protective barriers and resealable options. As a result, the U.K. cheese packaging market is positioning itself at the intersection of regulatory compliance, premium branding, and sustainable innovation.

Italy: Protecting PDO Cheeses While Expanding Flexible Packaging Adoption

Italy’s cheese packaging market is deeply shaped by its responsibility to preserve the authenticity of PDO (Protected Designation of Origin) cheeses like Parmigiano Reggiano and Pecorino Romano. Packaging plays a critical role in protecting these products’ unique characteristics while meeting strict EU and national quality standards. Innovations are focusing on specialized materials that preserve flavor integrity, while also enabling international distribution of premium cheeses.

At the same time, the Italian market is showing a growing preference for flexible packaging formats, such as plastic pouches and films, particularly for shredded and processed cheeses. These solutions are cost-effective, extend shelf life, and cater to modern retail and export demands. While sustainability is gaining momentum, affordability remains an equally important factor, pushing manufacturers to balance eco-friendly materials with cost efficiency for producers across different scales.

Canada: Eco-Friendly Innovation and Plant-Based Cheese Packaging Solutions

Canada’s cheese packaging industry is undergoing a strong shift toward sustainable and biodegradable materials, driven by rising consumer awareness and regulatory emphasis on environmental protection. Producers are adopting compostable and reusable wraps, especially for gourmet and artisan cheeses, to meet the demands of eco-conscious consumers. This sustainability-driven transformation is reinforcing Canada’s role as an innovator in North American cheese packaging solutions.

A particularly notable trend in Canada is the adoption of plant-based materials such as PLA (polylactic acid), PHA (polyhydroxyalkanoates), and natural wraps like beeswax-coated cloths, offering biodegradable alternatives to conventional plastics. Meanwhile, advancements in high-barrier flexible films are helping extend shelf life, reduce oxygen and moisture infiltration, and minimize food waste. These innovations make Canada a growing hub for next-generation, eco-friendly cheese packaging technologies.

Cheese Packaging Market Report Scope

Cheese Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.3 Billion

|

|

Market Size (2034)

|

$6.8 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Metal, Glass, Others), By Packaging Format (Flexible Packaging, Rigid Packaging, Other Formats), By Cheese Type (Hard & Semi-Hard Cheese, Soft Cheese, Fresh Cheese, Processed Cheese), By End-Use (Foodservice, Retail)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi plc, Sealed Air Corporation, Huhtamaki Oyj, DS Smith plc, Syntegon Technology GmbH, Krones AG, Crown Holdings, Inc., Sonoco Products Company, Sidel S.A., Berry Global Inc., AR Packaging, Constantia Flexibles Group GmbH, Tetra Pak

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cheese Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Others

By Packaging Format

- Flexible Packaging

- Rigid Packaging

- Other Formats

By Cheese Type

- Hard & Semi-Hard Cheese

- Soft Cheese

- Fresh Cheese

- Processed Cheese

By End-Use

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cheese Packaging Market

- Amcor plc

- Mondi plc

- Sealed Air Corporation

- Huhtamaki Oyj

- DS Smith plc

- Syntegon Technology GmbH

- Krones AG

- Crown Holdings, Inc.

- Sonoco Products Company

- Sidel S.A.

- Berry Global Inc.

- AR Packaging

- Constantia Flexibles Group GmbH

- Tetra Pak

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global cheese packaging market, providing a comprehensive analysis of current dynamics, breakthroughs in materials and formats, and emerging opportunities shaping the sector. The analysis reviews the latest technological developments such as high-barrier mono-material films, vacuum skin packaging (VSP), modified atmosphere packaging (MAP), smart spoilage indicators, and compostable formats, highlighting their role in extending shelf life, ensuring food safety, and meeting sustainability mandates. This report is an essential resource for packaging engineers, procurement leaders, R&D teams, and executives seeking actionable insights into the evolution of cheese packaging across retail, foodservice, and industrial applications. By evaluating competitive strategies, market penetration, and regulatory influences, this report captures both historical trends from 2021 to 2024 and forecasts from 2025 to 2034, helping stakeholders identify high-value opportunities in recyclable, bio-based, and automation-enabled solutions. Additionally, the research highlights industry best practices for balancing cost efficiency, operational scalability, and circular economy principles in cheese packaging design. USDAnalytics further provides analysis of 15+ leading companies, including Amcor plc, Mondi Group, Sealed Air, and Constantia Flexibles, offering detailed insights into their material innovation, global footprint, and sustainability initiatives that are redefining packaging norms.

Scope Highlights

- Segmentation: By Material (Plastic, Paper & Paperboard, Metal, Glass, Others), Packaging Format (Flexible, Rigid, Other Formats), Cheese Type (Hard & Semi-Hard, Soft, Fresh, Processed), End-Use (Foodservice, Retail)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic Data: 2021–2024

- Forecast Period: 2025–2034

- Companies: Analysis/profiles of 15+ companies including Amcor plc, Mondi plc, Sealed Air Corporation, Huhtamaki Oyj, DS Smith plc, Syntegon Technology GmbH, Krones AG, Crown Holdings, Sonoco Products Company, Sidel S.A., Berry Global Inc., AR Packaging, Constantia Flexibles Group GmbH, and Tetra Pak

Methodology

The research methodology employed by USDAnalytics combines both primary and secondary research to deliver a granular understanding of the cheese packaging market. Primary research includes interviews with industry executives, procurement managers, packaging engineers, and sustainability officers, while secondary research draws from company reports, trade publications, regulatory frameworks, and market databases. Quantitative analysis leverages historical shipment data, production statistics, and consumption trends from 2021 to 2024, with projections modeled through CAGR-based forecasting to 2034. Advanced market sizing techniques, cross-validation, and triangulation ensure the accuracy of segment-wise, material-wise, and regional insights. Competitive benchmarking is conducted by evaluating product portfolios, technology adoption, R&D investments, and sustainability commitments of key players. The methodology also incorporates trend mapping and scenario analysis to evaluate the impact of regulatory changes, circular economy initiatives, and evolving consumer preferences on market growth. By integrating qualitative insights with quantitative modeling, the study provides actionable, decision-ready intelligence for market participants, policy-makers, and strategic investors aiming to optimize operational efficiency and innovation pipelines in cheese packaging.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.