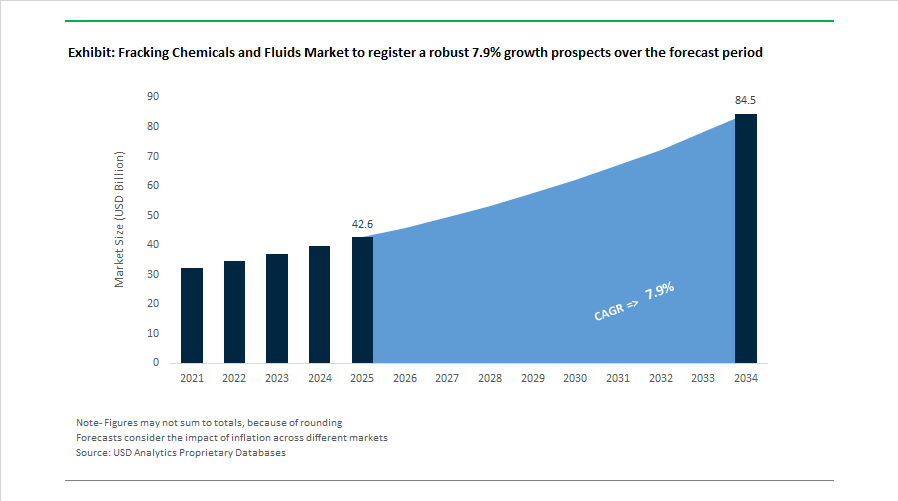

Fracking Chemicals and Fluids Market Size 2025–2034: $42.6 Billion to $84.5 Billion at 7.9% CAGR Fueled by Electrification, Polymer Expansion and HPHT Innovation

The Fracking Chemicals and Fluids Market is projected to expand from $42.6 billion in 2025 to $84.5 billion by 2034, registering a strong CAGR of 7.9%. Growth is supported by rising shale development budgets, increased horizontal well intensity, and rapid electrification of hydraulic fracturing fleets. Slickwater polymers, friction reducers, crosslinkers, biocides, scale inhibitors, surfactants, and high-pressure high-temperature chemical additives remain core revenue streams. Market transformation is increasingly defined by electric frac systems, autonomous pumping platforms, and carbon-intensity reduction strategies integrated directly into fluid chemistry and wellsite logistics.

In February 2026, SLB introduced its fully electric Cameron frac fluid delivery system, replacing traditional hydraulic actuation with electric automation and eliminating hydraulic fluids at the wellsite. The electrification of fluid delivery reduces diesel consumption and aligns with operator sustainability mandates. In February 2026, SLB also secured integrated well services contracts for Mubadala Energy’s Tangkulo deepwater gas development in Indonesia, covering drilling fluids, cementing chemistry, and stimulation fluids under a full well lifecycle model. During the same month, Baker Hughes signed a multi-year preferred provider agreement with Marathon Petroleum, incorporating BIOQUEST™ renewable chemical additives into broader hydrocarbon treatment programs, reinforcing the shift toward bio-based formulations in petroleum operations. In December 2025, Chevron allocated nearly $6 billion for U.S. shale and tight assets across the Permian, DJ, and Bakken basins, with capital earmarked for efficiency improvements and lower-carbon fluid systems.

In 2025, Halliburton projected that its Zeus™ electric fracturing fleets would represent 50% of its total active fleet by year-end, reflecting record demand for electric pumping systems powered by grid electricity or field gas. In January 2025, Halliburton and Coterra Energy launched the Octiv™ Auto Frac Service, introducing fully autonomous hydraulic fracturing technology that uses real-time data to adjust fluid chemistry, viscosity, and pumping pressure without manual intervention. In August 2025, Chemours and SRF Limited formalized a strategic partnership to expand production of high-performance fluorochemical intermediates in India, stabilizing supply of specialized additives required in HPHT fracking environments. Liberty Energy’s year-end 2025 disclosures outlined diversification into geothermal and modular power infrastructure, leveraging its fluid management expertise to support emerging energy and AI-driven gas demand.

Earlier structural capacity shifts began in 2024. In September 2024, SNF Flopam India inaugurated a new regional technical center and announced a $120 million expansion, increasing water-soluble polymer production capacity from 258,000 MT to 458,000 MT annually to serve slickwater and chemical enhanced oil recovery markets. In early 2024, Kemira finalized the divestment of its Oil & Gas portfolio, including friction reducers and fluid loss additives, to Sterling Specialty Chemicals, consolidating supplier dynamics within the global fracking chemicals ecosystem.

Trends and Opportunities in the Fracking Chemicals and Fluids Market

Strategic Consolidation of ESG-Compliant and Low-Toxicity Chemical Platforms

Environmental transparency has become a baseline operating requirement rather than a differentiator. By November 2025, FracFocus disclosures show that nearly 92% of active U.S. wells now provide full chemical disclosure, up sharply from around 80% in 2020. This structural shift has accelerated the retirement of high-toxicity surfactants, biocides, and scale inhibitors, replacing them with biodegradable and lower aquatic toxicity alternatives that reduce long-term environmental liability from flowback and produced water.

Tier-1 service providers are standardizing “clean chemistry” platforms to align with investor ESG expectations and operator sustainability targets. Halliburton has embedded sustainability metrics into its well construction portfolio, driving a 15 to 20% increase in adoption of its eco-friendly surfactant systems that maintain friction reduction performance while lowering overall chemical load per stage. Similarly, SLB has integrated chemical disclosure, toxicity screening, and lifecycle assessment into its completion fluid offerings to meet operator reporting requirements under global ESG frameworks.

R&D investment is following this shift. In June 2025, Nouryon inaugurated a dedicated innovation center in the United States focused on biodegradable drilling and completion fluids. The center is specifically targeting the replacement of legacy cross-linkers and biocides with chemistries compatible with tighter Clean Water Act discharge standards, signaling that regulatory alignment is now a core product design criterion.

AI-Driven Real-Time Fluid Optimization and Automated Dosing

Digitalization is fundamentally changing how fracking chemicals are consumed. Static, pre-engineered fluid recipes are being replaced by adaptive systems that respond to real-time downhole conditions. In November 2024, Halliburton launched its LOGIX Unit Vitality platform, which applies machine learning to pressure, rate, and rheology data during cementing and fracturing. Field deployments indicate chemical usage reductions of 5 to 10% by dynamically adjusting friction reducer and crosslinker concentrations rather than relying on conservative overdesign.

Predictive analytics are also improving asset uptime. Operational data released by Baker Hughes in 2025 show that AI-driven platforms reduced unplanned downtime by roughly 20% by linking fluid performance to equipment health and wellbore conditions. This capability is especially valuable in long-lateral horizontals where friction reducer costs scale rapidly with lateral length.

Industry consolidation is amplifying these capabilities. Following SLB’s approximately USD 8 billion acquisition of ChampionX in July 2025, digitally enabled production chemicals have expanded across the Permian and Delaware basins. The integration of ChampionX’s chemical formulations with SLB’s digital twins allows automated, well-specific dosing strategies that improve consistency and reduce chemical overspend across large asset portfolios.

High-Performance Chemistry Compatible with Produced Water Reuse

Water management economics are reshaping fracking fluid design. In 2024, Select Water Solutions reported recycling approximately 282 million barrels of produced water, and operators in the Permian Basin now routinely source more than 75% of their fracturing fluid base from treated produced water. Several operators have publicly stated targets exceeding 90% reuse by 2026, sharply reducing freshwater dependence.

This shift creates strong demand for chemicals that remain effective in ultra-high-salinity environments. Conventional polyacrylamide friction reducers lose performance in the presence of divalent ions such as calcium and magnesium. As a result, chemical suppliers are accelerating development of salt-tolerant anionic and cationic PAM variants capable of operating at Total Dissolved Solids levels above 200,000 ppm. These formulations are increasingly specified as standard for Permian and Eagle Ford completions.

Regulatory modernization is reinforcing this opportunity. In March 2025, the U.S. Environmental Protection Agency announced updates to the Oil and Gas Extraction Effluent Guidelines under 40 CFR 435, expanding pathways for beneficial reuse of treated produced water. This policy shift is stimulating additional demand for advanced scale inhibitors, corrosion inhibitors, and biocides that enable reuse beyond hydraulic fracturing, including industrial cooling and limited agricultural applications.

Conformance and Diverting Agents for Re-Fracturing and Well Re-Stimulation

As shale basins mature, re-fracturing has emerged as a capital-efficient alternative to new drilling. Data from the Federal Reserve Bank of Dallas and industry disclosures in the first half of 2025 indicate that re-frac programs can deliver triple-digit percentage returns compared to greenfield wells, particularly in infrastructure-rich plays such as the Eagle Ford and Bakken.

These operations require specialized chemical systems to temporarily seal depleted perforations and redirect stimulation energy into unstimulated rock. Biodegradable particulate diverters based on polylactic acid and advanced viscosified acids are gaining traction because they provide predictable degradation at bottom-hole temperatures, leaving minimal residue that could impair future production.

A high-profile example is Chevron’s deployment of its triple-frac completion strategy across roughly half of its Permian wells in early 2025. The approach reduced completion times by 25% and per-well costs by 12%, relying heavily on precision surfactants, fluid stabilizers, and diverters to ensure uniform proppant placement across multiple stages. This trend highlights a sustained opportunity for chemical suppliers that can deliver performance-critical, application-specific formulations rather than commoditized additives.

Fracking Chemicals and Fluids Market Share and Segmentation Insights

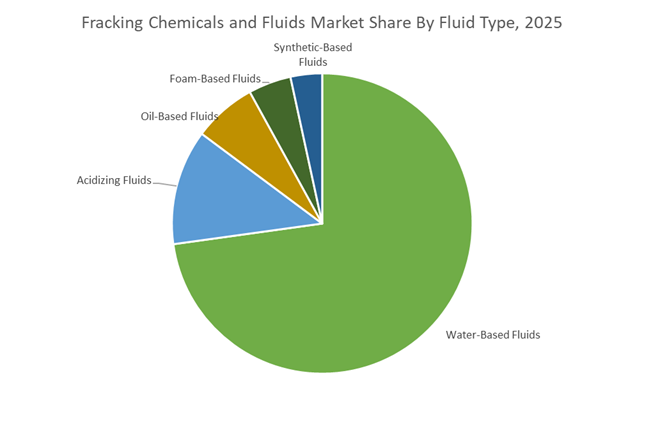

Water-Based Fracturing Fluids Dominate Hydraulic Fracturing Operations Due to Cost Efficiency and Operational Flexibility

Water-Based Fluids accounted for 72.80% of the Fracking Chemicals and Fluids Market share in 2025, making them the most widely used fluid system in hydraulic fracturing operations worldwide. These fluids—commonly formulated as slickwater, linear gels, and crosslinked gel systems—serve as the base medium used to transport proppants and specialized fracturing chemicals into underground shale formations, enabling the creation of fractures that release trapped hydrocarbons. Water-based systems dominate the market primarily because water is widely available, cost-effective, and compatible with modern high-volume fracturing techniques used in unconventional oil and gas production. In 2025, a significant operational trend shaping the market is the rapid expansion of produced water reuse in fracturing fluid systems. Rising costs associated with freshwater sourcing, wastewater disposal, and environmental compliance have pushed operators to invest heavily in produced water treatment and recycling technologies. Reusing high-total-dissolved-solids (TDS) produced water requires specialized chemical formulations, including advanced friction reducers, biocides, corrosion inhibitors, and scale control additives designed to maintain fluid performance under high salinity conditions. This development has created a growing niche for specialty fracturing chemicals engineered specifically for recycled water systems, strengthening innovation within the fracking chemicals and fluids market.

Onshore Hydraulic Fracturing Drives the Vast Majority of Global Fracturing Chemical Consumption

Onshore applications represented 94.80% of the Fracking Chemicals and Fluids Market share in 2025, reflecting the overwhelming concentration of hydraulic fracturing activity within land-based unconventional resource developments. Shale oil and gas extraction—the primary driver of global fracturing demand—occurs predominantly in onshore shale basins such as the Permian Basin and Bakken in the United States, the Montney and Duvernay formations in Canada, the Vaca Muerta shale in Argentina, and emerging unconventional plays in China and the Middle East. These large-scale onshore drilling programs involve high-volume hydraulic fracturing campaigns, often requiring millions of gallons of fluid and large volumes of specialized fracturing chemicals per well. In contrast, offshore hydraulic fracturing remains a relatively small segment of the market, largely due to higher operational complexity, stricter environmental regulations, and logistical constraints associated with offshore drilling platforms. However, in 2025 there is growing interest in fracturing-based reservoir stimulation in deepwater oil fields, particularly in regions such as the Gulf of Mexico, Brazil’s pre-salt basins, and offshore West Africa. These projects use carefully engineered fracturing treatments designed to enhance reservoir productivity while managing strict environmental and operational requirements. Despite this emerging offshore activity, the massive scale of onshore unconventional drilling continues to dominate global demand for fracking chemicals and fluids.

Competitive Landscape in Fracking Chemicals and Fluids Market

SLB Expands Digital Oilfield Integration and Sustainable Fracturing Systems

SLB remains the largest global oilfield services provider, reporting $36.29 billion in revenue for 2025 and targeting a 10% increase in digital and integration revenue in 2026 through its DELFI ecosystem. The company has shifted toward an integrated sustainability model, combining advanced fracking chemicals with AI-driven reservoir analytics to automate fluid dosing in real time. In late 2025, SLB launched Drilling Mud Virtualization and closed-loop water recycling systems that reduce chemical waste by more than 20%, setting a new industry benchmark for operational efficiency. Its expansion into the Middle East and Asia-Pacific includes a major contract with OGDCL to evaluate tight gas prospects in Pakistan using advanced hydraulic fracturing fluids. By integrating digital performance analytics with low-carbon completion technologies, SLB is redefining the role of a fracking chemicals supplier into that of a performance optimization partner.

Halliburton Leads Intelligent Fracturing and Slick-Water Additive Innovation

Halliburton continues to dominate North American shale through its ZEUS IQ™ intelligent fracturing platform and Illusion® dissolvable frac plugs, which eliminate mechanical drill-out operations and significantly reduce non-productive time. Slick-water friction reducers drive the industry’s shift toward long-lateral horizontal wells, a segment where Halliburton maintains strong leadership. In February 2026, the company signed a memorandum of understanding with Pertamina to deploy unconventional stimulation technologies across mature Indonesian fields. The launch of NEX Lab℠ in January 2026 accelerates research into sustainable fracturing chemistries and advanced completion systems. Halliburton’s execution model integrates high-performance friction reducers with field-level digital monitoring, reinforcing its position at the intersection of operational efficiency and chemical innovation in hydraulic fracturing.

Baker Hughes Integrates Carbon-Smart Fluids with Autonomous Well Construction

Baker Hughes positions itself as an energy technology company combining fracking chemicals with digital analytics and carbon-conscious drilling strategies. In February 2026, the company became the preferred chemical solutions provider for Marathon Petroleum, deploying its XERIC™ and BIOQUEST™ portfolios across 12 U.S. refineries, strengthening downstream integration. The Kantori™ autonomous well construction solution introduced in 2026 uses artificial intelligence to dynamically adjust fluid rheology, reducing aquifer contamination risks and optimizing fracture propagation. Baker Hughes is expanding into carbon capture and storage and geothermal applications, leveraging its expertise in stimulation fluids for CO2 sequestration wells. The Leucipa™ data platform enables automated production optimization and fluid performance analytics across U.S. natural gas basins. This integration of AI, carbon-smart fluid systems, and real-time monitoring enhances Baker Hughes’ competitive position in advanced fracturing solutions.

BASF Strengthens Biomass-Balanced Polymers for High-Pressure Reservoirs

BASF serves as a foundational supplier of polymers and surfactants used in high-performance fracking fluids, particularly AMPS-based polymers engineered for high-temperature and high-pressure environments. For 2026, BASF forecasts EBITDA between €6.2 billion and €7.0 billion, with Chemicals and Nutrition segments driving earnings momentum. Under its Winning Ways strategy, BASF is prioritizing biomass-balanced oilfield chemicals, targeting net-zero carbon variants across its friction reducer portfolio. The startup of the Zhanjiang Verbund site in late 2025 expanded production capacity for specialty polymers serving Asia-Pacific shale and tight gas developments. BASF’s deep integration within the chemical value chain ensures reliable feedstock supply and cost stability amid raw material volatility. Its leadership in advanced polymer chemistry reinforces its role as a critical upstream partner in the hydraulic fracturing additives market.

Solvay Focuses on Green Biocides and Lithium Recovery from Produced Water

Solvay differentiates itself through high-selectivity surfactants and friction reducers tailored for complex reservoir chemistries. Its TOLCIDE® biocides and ALKAMULS® surfactant lines are widely used in hydraulic fracturing fluids to control microbial activity and enhance hydrocarbon flow. The company has pioneered green biocides with rapid biodegradability profiles, addressing increasing environmental compliance requirements in North America and Europe. In early 2026, Solvay completed a significant debt reduction phase, enabling reinvestment into lithium recovery technologies from produced water, a rapidly emerging segment linked to energy transition supply chains. Integration with its Essential Chemicals division allows Solvay to supply soda ash and peroxide for large-scale well stimulation programs. Through its Technical Zero initiative targeting zero liquid discharge of fluorinated substances by late 2026, Solvay strengthens its ESG positioning within the fracking chemicals and fluids market.

Saudi Arabia: Jafurah-Led Scale-Up Redefining High-Temperature Fracturing Chemistry

Saudi Arabia has emerged as one of the most strategically important growth markets for fracking chemicals and stimulation fluids, anchored by the late-2025 peak construction phase of the Jafurah unconventional gas field. Led by Saudi Aramco, the USD 110 billion Jafurah program underpins the Kingdom’s objective to reach 2 billion cubic feet per day of sales gas by 2030. This scale and depth of development is materially increasing demand for high-temperature cross-linked fracturing fluids, particularly systems capable of maintaining viscosity and proppant suspension in deep, high-pressure reservoirs. The strategic pivot toward non-associated gas to reduce liquid fuel burn for power generation is further reinforcing the use of advanced organometallic cross-linkers engineered for extreme downhole conditions.

Service integration and localization are accelerating this transition. In December 2025, SLB secured a five-year integrated stimulation contract that embeds frac automation and digital chemical dosing into Aramco’s unconventional program. These systems are improving fluid efficiency and consistency across multi-stage fracturing operations. Parallel to this, the iktva program has driven the commissioning of localized facilities for friction reducers and biocides by international service providers during 2025. This localization is reducing supply lead times ahead of the 2026 drilling calendar and structurally embedding Saudi Arabia as a long-term, high-specification market for advanced fracking chemicals.

United States: Efficiency, Environmental Scrutiny, and Digitalization Driving Reformulation

The United States remains the largest and most technologically advanced consumer of fracking chemicals and fluids, with 2025 characterized by efficiency gains and regulatory-driven reformulation. Modern completion designs and water management practices have shifted the industry decisively toward recycled water-based fluids, which now dominate domestic usage. Horizontal wells continue to define chemical demand intensity, accounting for the majority of fluid volumes and requiring high-performance slickwater formulations optimized for long laterals and complex fracture networks.

Environmental oversight is reshaping additive selection. In 2025, the U.S. Environmental Protection Agency intensified scrutiny of PFAS-related precursors in oilfield chemicals, prompting rapid substitution toward fluorine-free surfactants and biodegradable friction reducers to safeguard groundwater. At the basin level, operators such as Chevron and ExxonMobil reported measurable reductions in chemical waste through the deployment of IoT-enabled automated blending units. In the Permian Basin, these systems delivered double-digit waste reductions in 2025, reinforcing digital dosing and real-time monitoring as standard features of U.S. completion chemistry.

Argentina: Vaca Muerta Industrialization Unlocking Chemical Demand at Scale

Argentina’s fracking chemicals and fluids market is entering a new industrial phase driven by record operational intensity in the Vaca Muerta shale. In October 2025, the play executed more than 2,000 fracturing stages in a single month, supported by strong improvements in well connection rates. This scale-up is translating directly into sustained demand for high-volume fracturing fluids, proppant transport additives, and friction reducers tailored for pad-based development.

Infrastructure resolution is amplifying this momentum. The 2025 expansion of the Oldelval pipeline system has removed export and evacuation constraints, enabling operators to convert large drilled but uncompleted inventories into active production. This shift is triggering a 2026 surge in chemical procurement. At the service level, Tenaris announced an expansion of its integrated services offering at AOG 2025, including additional hydraulic fracturing capacity scheduled for late 2026. Combined with cost-competitive breakevens maintained by YPF and its partners, Argentina is consolidating its position as the leading unconventional chemicals market outside North America.

China: Green Fracturing and Multi-Resource Integration Shaping Chemical Innovation

China’s fracking chemicals and fluids market is evolving under a dual mandate of resource security and environmental constraint. The Ministry of Industry and Information Technology’s 2025–2026 Work Plan targets sustained growth in chemical value addition, with emphasis on high-end polyolefins and electronic chemicals that share feedstock and synthesis pathways with synthetic fracturing additives. This policy alignment is encouraging domestic chemical producers to move upstream into higher-value fluid systems.

Technology transfer and resource integration are accelerating. The Beijing International Shale Gas Technology and Equipment Exhibition scheduled for March 2026 is positioned as a platform for disseminating green fracking technologies to domestic firms such as Zhonghao Chenguang. At the same time, China’s 2026 helium extraction strategy is driving demand for specialized chemical separation processes integrated with upstream fracturing and production. Field-level innovation is also advancing, with Sinopec and CNPC successfully trialing CO2-based fracturing in Sichuan’s deep shale blocks in late 2025, reducing water intensity in water-stressed regions and reshaping fluid system design.

India: Policy Expansion and Fiscal Pressure Driving Precision Chemical Use

India’s fracking chemicals and fluids market is at an early but accelerating stage, shaped by policy expansion and cost discipline. The extension of the OALP-X bidding round to February 2026 has opened a record acreage base, including ultra-deepwater and unconventional blocks that require international-grade chemical expertise. This is broadening the technical requirements for fracturing fluids, particularly for high-pressure and offshore environments.

Fiscal dynamics are sharpening efficiency focus. The increase in GST on oil and gas exploration services to 18% in September 2025 has forced domestic operators and service companies to optimize chemical dosing and logistics. Concurrently, the government’s push to unlock shale potential in the Krishna-Godavari Basin is driving demand for salt-tolerant gelling agents suitable for coastal and offshore conditions. With a national mandate to reduce oil import dependency to below 70% by 2030, India is channeling multi-billion-dollar infrastructure investment into upstream development, indirectly strengthening the long-term outlook for advanced fracking chemical systems.

Canada: Gas-Weighted Plays and Sustainability-Centered Fluid Design

Canada’s fracking chemicals and fluids market is entering a gas-led rebound phase, with pressure pumping activity expected to rise in 2026 across the Montney and Duvernay plays. As LNG Canada advances toward full operations, producers are accelerating completion programs that rely on long-lateral horizontal wells and sophisticated proppant transport chemistries to optimize gas recovery.

Sustainability is a defining differentiator. Canadian operators are at the forefront of adopting biodegradable and bio-based oilfield chemicals, aligning fracturing fluid design with federal carbon reduction targets. Investments in environmentally compatible formulations are reaching a milestone by mid-2026, positioning Canada as a reference market for low-impact fracking fluids that balance performance with regulatory alignment.

Country-Level Strategic Drivers in the Fracking Chemicals and Fluids Market

Fracking Chemicals and Fluids Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for Fracking Chemicals and Fluids

|

|

Saudi Arabia

|

Jafurah unconventional gas and localization

|

High-temperature cross-linked fluids and localized supply chains

|

|

United States

|

Efficiency gains and PFAS scrutiny

|

Shift toward biodegradable, digitally dosed fluid systems

|

|

Argentina

|

Vaca Muerta scale-up and pipeline expansion

|

Sustained high-volume demand for fracturing fluids

|

|

China

|

Green fracking and resource integration

|

CO2-based fluids and advanced chemical synthesis

|

|

India

|

OALP expansion and fiscal optimization

|

Precision dosing and salt-tolerant additives

|

|

Canada

|

LNG-driven gas development and sustainability

|

Bio-based, low-impact fracturing chemistries

|

Fracking Chemicals and Fluids Market Report Scope

Fracking Chemicals and Fluids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$42.6 Billion

|

|

Market Size (2034)

|

$84.5 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Fluid Type (Water-Based Fluids, Oil-Based Fluids, Foam-Based Fluids, Synthetic-Based Fluids, Acidizing Fluids), By Chemical Function (Friction Reducers, Gelling Agents, Cross-Linkers, Biocides, Surfactants, Corrosion and Scale Inhibitors, pH Buffering Agents, Clay Stabilizers), By Well Type (Horizontal Wells, Vertical Wells), By Application (Onshore, Offshore)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Halliburton Company, SLB, Baker Hughes Company, Weatherford International plc, Liberty Energy Inc., BASF SE, Dow Inc., Gujarat Fluorochemicals Limited, Chevron Phillips Chemical Company, Calfrac Well Services Ltd., Tenaris S.A., Solvay S.A., Clariant AG, Kemira Oyj, Innospec Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fracking Chemicals and Fluids Market Segmentation

By Fluid Type

- Water-Based Fluids

- Oil-Based Fluids

- Foam-Based Fluids

- Synthetic-Based Fluids

- Acidizing Fluids

By Chemical Function

- Friction Reducers

- Gelling Agents

- Cross-Linkers

- Biocides

- Surfactants

- Corrosion and Scale Inhibitors

- pH Buffering Agents

- Clay Stabilizers

By Well Type

- Horizontal Wells

- Vertical Wells

By Application

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fracking Chemicals and Fluids Industry

- Halliburton Company

- SLB

- Baker Hughes Company

- Weatherford International plc

- Liberty Energy Inc.

- BASF SE

- Dow Inc.

- Gujarat Fluorochemicals Limited

- Chevron Phillips Chemical Company

- Calfrac Well Services Ltd.

- Tenaris S.A.

- Solvay S.A.

- Clariant AG

- Kemira Oyj

- Innospec Inc.

*- List not Exhaustive