Functional Apparel Market Overview: Performance Materials, Circular Fibers, and Data-Driven Design Reshape A USD 428.6 Billion Industry

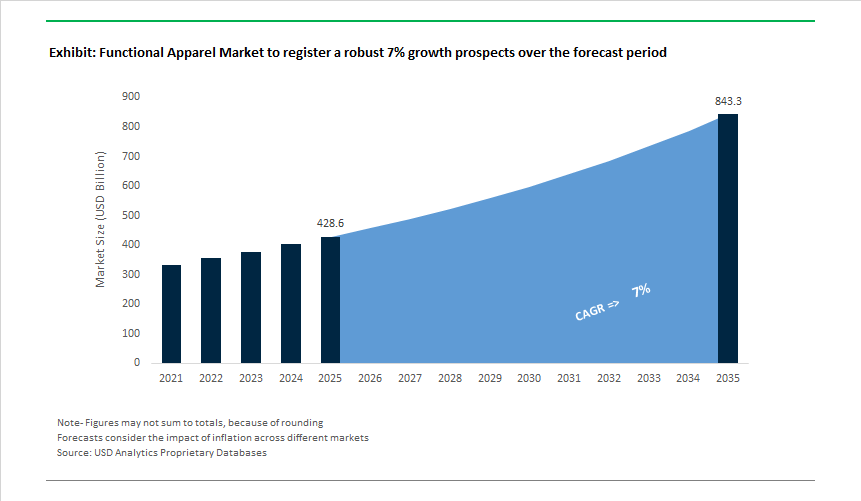

The global Functional Apparel market, valued at USD 428.6 billion in 2025 and projected to reach USD 843.1 billion by 2035 at a 7.0% CAGR, matters now because apparel has shifted from fashion-led differentiation to materials-led performance systems. Growth is structurally anchored in activewear, outdoor apparel, workwear, and athleisure, where garments are engineered as wearable systems delivering moisture transport, thermal regulation, abrasion resistance, UV shielding, and odor control under real-use stress. For manufacturers and brand owners, functional apparel is no longer discretionary-it is a margin-defining category where fabric physics, finishing chemistry, and supply-chain architecture directly determine product acceptance, retail contracts, and lifecycle profitability.

Demand is being reshaped by a clear structural shift: performance specifications and sustainability metrics are converging into a single procurement requirement. Leading manufacturers are designing around measurable fabric parameters such as evaporative resistance (ISO 11092 Ret), air permeability, and wash-durable functional finishes, while simultaneously committing to recycled and circular feedstocks. High recycled polyester penetration-approaching ≥99% where technically feasible-has moved from marketing claim to baseline expectation in many global retail and brand sourcing programs. This has forced producers to re-engineer yarn spinning, knitting, and finishing processes to preserve wicking efficiency, breathability, and tensile durability despite higher recycled content variability. At the same time, PFAS-free, low-impact anti-odor and antimicrobial finishes are replacing legacy chemistries, driven by regulatory pressure and consumer scrutiny around skin contact safety and microplastic release.

Legacy “one-fabric” constructions are increasingly being displaced by body-mapped and zone-engineered designs that deploy differentiated knit structures, yarn deniers, and ventilation zones within a single garment. This substitution logic reduces material usage while improving thermophysiological comfort, with high-exertion product lines targeting air-permeability increases of 50-150 L/m²/s over leisure apparel to manage heat and humidity. From a business outcome standpoint, fabrics engineered to deliver ~30% lower Ret values than standard athletic textiles translate into measurable wearer comfort, longer usage duration, and higher repurchase rates, while anti-odor systems retaining >90% bacterial suppression after 50 washes reduce replacement cycles and warranty risk. Looking forward, market leadership will hinge on manufacturers’ ability to vertically secure recycled feedstocks, industrialize low-impact finishing technologies, and integrate digital fit analytics, athlete lab testing, and field-use telemetry into product development-linking material science, data, and ESG compliance into a single scalable operating model.

Market Analysis: Recent Strategic Moves & Technology Drivers

The functional apparel landscape tightened its focus on sustainability and vertically integrated material strategies through 2024-2025. Notably, Apr 2024 Patagonia published lifecycle evidence that semi-mechanically recycled polyester cuts CO₂e by ~50% vs virgin polyester, accelerating commercial interest in industrial-scale textile recycling and circular feedstocks. This technical validation underpinned Mar 2025 partnerships such as H&M Group & Circular Systems, which announced textile-to-textile recycling integrations to move beyond bottle-based recycled polyester and improve mechanical and chemical recycling yields - a step-change for large-volume functional wear where textile-to-textile closed loop reduces supply risk and Scope 3 emissions. Concurrently, brands are investing in targeted product innovation: Oct 2024 saw Nike’s FIT ADV launch with body-mapped thermal zones and computational fabric design, while Jan 2025 Lululemon expanded men’s performance ranges leveraging premium fabric engineering and high-margin DTC distribution, signaling continued premiumization in technical apparel.

Commercial consolidation and supply-chain repositioning also reshaped the sector. Jul 2025 Coats’ acquisition of OrthoLite expanded its materials platform into premium footwear insoles, reinforcing the materials+components play for vertically oriented suppliers. VF Corporation (The North Face) pushed circular programs and material commitments in Aug 2024, accelerating reuse/repair initiatives and regenerative sourcing to meet regulatory and retailer ESG thresholds. Brands are responding to consumer durability expectations by tightening wash-life standards and specifying anti-microbial finishes that survive consumer laundering cycles. At the same time, margin optimization and brand repositioning occurred: May 2025 Under Armour reorganized leadership to sharpen product strategy and improve channel economics, while companies like Adidas reported near-complete recycled polyester utilization and measurable Scope 3 emission reductions - demonstrating that scale-enabled sustainability is now a competitive baseline rather than a niche differentiator.

Functional Apparel Market Trends and Opportunities

Trend 1: Textile-Based Biometric Sensing in Performance Wear

Functional apparel is transitioning from passive protection to an active, data-generating interface that continuously monitors the human body, fundamentally reshaping how performance wear is designed and valued. By 2025, smart fabrics have moved beyond experimental prototypes into scaled commercialization, driven by advances in textile-integrated sensors that eliminate the need for external devices. Conductive yarns, silver nanowires, and printed conductive inks are now embedded directly into knitted and woven structures, enabling garments to capture heart rate, muscle activation, respiration patterns, hydration levels, and skin temperature with medical-grade accuracy. Defense and military programs have played a catalytic role in accelerating this transition, validating that textile-based sensing can meet stringent reliability and durability requirements under extreme physical stress. Unlike chest straps or wearables that cause discomfort and inconsistent data capture, sensorized fabrics distribute contact points across the body, improving signal fidelity while preserving comfort and freedom of movement. The next layer of differentiation is being driven by AI-enabled analytics: continuous biometric data streams are increasingly processed in real time using machine learning models that convert raw physiological signals into actionable insights. By late 2025, performance apparel platforms are offering personalized recovery guidance, fatigue prediction, and early warning indicators for overtraining or health anomalies, positioning functional garments as long-term companions in both athletic performance optimization and preventative healthcare ecosystems.

Trend 2: Molecular-Level Recycling for Technical Apparel Circularity

The functional apparel industry is confronting a structural sustainability challenge as high-performance garments—often composed of complex blends, coatings, and elastomers—reach end of life. Mechanical recycling methods have proven inadequate for these materials, as they degrade fiber strength and compromise performance attributes critical for sportswear and protective clothing. In response, the industry is shifting toward molecular-level chemical recycling technologies that depolymerize textiles back into virgin-grade monomers while preserving material integrity. By 2025, fiber-to-fiber recycling pathways have demonstrated the ability to regenerate polyester with performance characteristics equivalent to virgin material, enabling true circularity for high-stress applications such as running apparel, outdoor gear, and compression wear. This shift is reinforced by vertically integrated recycling infrastructure, where feedstock collection, depolymerization, purification, and repolymerization occur within a single industrial ecosystem, reducing contamination risk and improving yield predictability. Europe and Asia are emerging as focal points for capacity expansion, with large-scale plants designed to process hard-to-recycle textile waste and PET fines into high-purity feedstocks. As regulatory pressure intensifies and brands commit to closed-loop targets, molecular recycling is no longer a sustainability add-on but a strategic requirement to secure long-term access to high-quality synthetic fibers without increasing dependence on fossil-based raw materials.

Opportunity 1: Advanced Thermo-Regulating Materials for Extreme Climates

Rising global temperatures, longer heatwaves, and expanding industrial activity in extreme environments are creating a high-specification opportunity for advanced thermo-regulating materials in functional apparel. Military forces, emergency responders, and industrial workers are increasingly exposed to heat stress, making thermal management a mission-critical requirement rather than a comfort feature. By 2025, layered apparel systems integrating moisture-wicking base layers, adaptive insulation, and breathable outer shells are becoming standard in defense modernization programs and industrial safety upgrades. The commercial maturation of active thermoregulation technologies—particularly Phase-Change Materials (PCMs)—is enabling garments to absorb excess body heat during high exertion and release it during rest phases, maintaining a stable microclimate close to the skin. These materials are now engineered to function across repeated thermal cycles without degradation, addressing historical durability concerns. In industrial contexts, breathable and thermally adaptive fabrics are being deployed to reduce fatigue, improve cognitive alertness, and lower the incidence of heat-related injuries in high-risk occupations such as firefighting, mining, and heavy manufacturing. As climate volatility increases, thermo-regulating apparel is emerging as a productivity and safety investment, not merely a premium feature.

Opportunity 2: Self-Cleaning and Pathogen-Inactivating Functional Fabrics

The convergence of public health awareness and material science innovation is accelerating the commercialization of self-cleaning and pathogen-inactivating textiles across healthcare, public services, and high-traffic environments. Photocatalytic nanocoatings applied to functional fabrics are transforming garments into active antimicrobial surfaces capable of neutralizing pathogens rather than merely resisting contamination. By 2025, nano-engineered coatings based on titanium dioxide and hybrid oxide systems have demonstrated exceptional efficacy, achieving near-total inactivation of virus-laden droplets and sustained antibacterial performance even after repeated laundering. These materials function by generating reactive oxygen species under ambient light, breaking down organic pollutants and microbial membranes without relying on chemical leaching. Beyond healthcare uniforms, this technology is expanding into hospitality apparel, public transit upholstery, and service-sector workwear, where hygiene standards are increasingly scrutinized. Importantly, next-generation formulations balance antimicrobial performance with wearability, ensuring that treated fabrics remain breathable, lightweight, and comfortable for extended use. As infection control, labor safety, and maintenance efficiency converge, self-sterilizing functional fabrics represent a scalable opportunity to redefine hygiene standards across multiple end-use environments.

Market Share Analysis: Functional Apparel Market

Market Share by Application: Sportswear and Activewear Anchor the Functional Apparel Economy

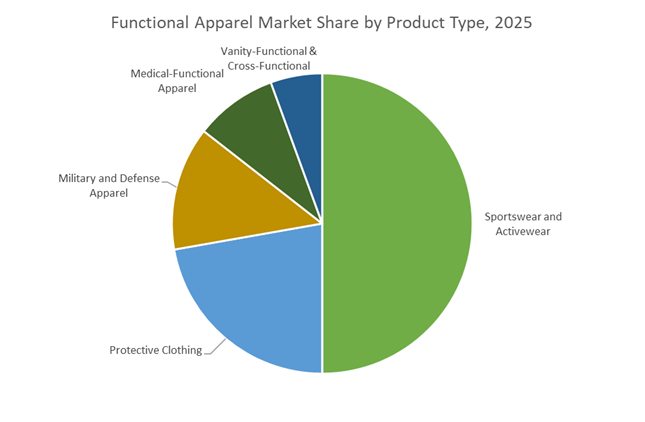

Sportswear and activewear account for approximately 45% of the global Functional Apparel Market, making this segment the single largest demand driver and the primary engine of innovation. Its dominance is structurally linked to the global athleisure transition, where performance apparel has moved beyond sports into everyday wear, dramatically expanding addressable volume. Consumers increasingly expect garments to create personal micro-climates—actively managing moisture, heat, and movement rather than passively covering the body. High-performance moisture management technologies enable fabrics to retain a fraction of the water absorbed by natural fibers, allowing significantly faster drying and sustained comfort during extended wear. Thermal regulation capabilities further reinforce market share, as advanced textiles are engineered to balance evaporative cooling without discomfort, maintaining optimal body temperature across variable activity levels. Waterproof yet breathable membrane systems remain critical for outdoor and endurance segments, where protection from external elements must coexist with internal vapor transmission. Compression apparel adds another layer of value by improving muscle stabilization and perceived endurance, linking apparel performance directly to physical output. Collectively, these functional benefits align with lifestyle shifts toward health, mobility, and multi-purpose wardrobes, positioning sportswear and activewear as the commercial core of the functional apparel market.

Market Share by Fabric Type: Synthetic Polymers Form the Performance Backbone of Functional Apparel

Synthetic polymers account for approximately 70% of total fabric usage in the Functional Apparel Market, reflecting their unmatched ability to deliver engineered performance at global scale. Polyester, nylon, and elastane dominate because their molecular structures can be precisely modified to achieve durability, stretch, moisture control, and abrasion resistance—attributes that natural fibers cannot consistently deliver. High-tenacity synthetic fibers provide extended garment lifespans under intense mechanical stress, making them indispensable in active, outdoor, and workwear applications. Market share is further reinforced by the rapid shift toward recycled synthetics, particularly recycled polyester, which allows brands to meet sustainability targets without compromising strength, color fastness, or process efficiency. Advanced yarn engineering has also reduced dependence on traditional elastane by delivering stretch and recovery through bi-component polymer structures, improving shape retention and wash durability over time. These innovations enable brands to balance performance, sustainability, and cost control simultaneously. As functional apparel continues to prioritize engineered reliability, circularity, and mass customization, synthetic polymers remain the foundational material platform, securing their dominant share in the global market.

Competitive Landscape: Overview + Company Profiles

The functional apparel competitive set is split between vertically integrated global sports giants that control fabric innovation and premium DTC specialists that monetize brand experience and higher ASPs. Leadership is defined by material IP (sizing, coatings, fabric constructions), scale of recycled feedstock sourcing, athlete lab validation capability, and omnichannel distribution efficiency.

Nike Inc. - Industry Leader in Digital Material Engineering and Body-Mapped Performance Systems

Nike combines massive R&D scale with proprietary systems like Dri-FIT ADV, using data-driven, body-mapped material placement to optimize thermal comfort and sweat management. Its patent portfolio and athlete testing facilities enable rapid prototyping and validation of new finishes, wicking yarns, and engineered knits. Nike’s global supply chain and brand reach make it a primary specification partner for performance fabrics; manufacturers aiming for large OEM contracts should align formulations with Nike’s digital material and testing protocols.

Lululemon Athletica Inc. - Premium DTC Specialist Monetizing Proprietary Fabric Constructions

Lululemon’s strength is premium fabric systems (Luon™, Nulu™) and a high-margin DTC model that funds aggressive product innovation. Its expanded men’s performance lines and tight community-driven product testing produce high consumer loyalty and superior inventory turn. For suppliers, Lululemon’s exacting quality and finish durability standards mean long-term, high-value contracts for proven recycled yarns and engineered stretch knits.

Adidas AG - Scale-Driven Sustainability and Recycled-Polyester Leadership

Adidas leverages global scale to implement ambitious circularity targets (≥70% preferred materials, 99% recycled polyester usage where feasible) and collaborates on high-profile material initiatives (e.g., Parley). Its procurement and supplier frameworks reward certified recycled content and lower GHG footprints, making it a strategic partner for textile innovators that can deliver certified, high-volume recycled yarns and transparent supply chains.

VF Corporation (The North Face) - Outdoor Performance With Strict Material and Circularity Standards

VF’s The North Face emphasizes durable waterproof/breathable constructions and circular programs (Renewed, regenerative sourcing). The brand demands high-performance laminates and PFC-free DWR finishes, plus rigorous mechanical and field testing. Suppliers targeting outdoor technical segments must meet puncture/wear thresholds and provide repair/renewal pathways that align with VF’s lifespan-focused product positioning.

Under Armour, Inc. - Margin Recovery Through Product and Channel Optimization

Under Armour has refocused on product quality and channel discipline to lift gross margins and reposition the brand in key performance niches (golf, outdoor). The company values fabrics that deliver quantifiable performance gains (moisture transport, thermal management) at competitive cost structures and is responsive to finish durability and wash-life claims. For suppliers, Under Armour presents opportunities for targeted category wins by demonstrating cost-effective, durable fabric systems that improve athlete outcomes.

The United States functional apparel market in 2025 is structurally anchored in defense procurement, healthcare monitoring, and climate-resilient performance wear. Federal demand is moving beyond conventional PPE toward integrated wearable systems, where garments function as data platforms. The Department of Defense’s expansion of “Soldier Systems” programs has elevated smart uniforms-embedded with biometric sensors, thermal regulation layers, and environmental hazard detection-from pilot concepts to scaled procurement items. This has created downstream demand for conductive yarns, flexible microelectronics, and textile-compatible power storage, aligning closely with broader CHIPS and Science Act objectives to onshore advanced electronics manufacturing.

On the commercial side, U.S. brands are aggressively investing in proprietary moisture-wicking, UV-protective, and heat-adaptive fabrics to address extreme weather exposure across outdoor labor, defense training, and recreational markets. Innovation hubs such as AFFOA are acting as industrial accelerators, translating lab-scale fiber-based batteries and communication systems into manufacturable textile platforms. As a result, the U.S. market is defining the high-margin frontier of functional apparel-where defense-grade reliability, medical-grade monitoring, and consumer performance converge.

China: Domestic Brand Science and Smart Factory Scale-Up

China’s functional apparel market is concluding the 14th Five-Year Plan with a decisive pivot toward value-added technical textiles and domestic brand dominance. National policy emphasis on industrial modernization and “Dual Circulation” has shifted investment away from export-driven volume toward high-performance functional polymers, antimicrobial coatings, and graphene-enhanced fabrics. State incentives are supporting vertically integrated smart factories, particularly in Guangdong, where automated knitting, seamless garment construction, and in-line coating systems are reducing lead times and improving consistency at scale.

Domestic champions are reinforcing this transition through heavy investment in performance science centers, focusing on biomechanics, aerodynamics, and thermal regulation. These facilities are supporting advanced cycling apparel, footwear rebound systems, and climate-adaptive sportswear aligned with China’s long-term objective of building a globally competitive sports and wellness economy. China’s strategic advantage lies in its ability to industrialize functional apparel innovations rapidly, compressing the time between material discovery and mass-market deployment.

India: PLI-Backed Manufacturing Scale and Technical Textile Localization

India’s functional apparel market in 2025 is being structurally reshaped by Production Linked Incentive (PLI) schemes and the National Technical Textiles Mission. The reduction in investment thresholds under PLI has widened participation, enabling mid-sized manufacturers to enter high-value segments such as medical functional apparel (Meditech) and industrial protective clothing (Protech). This policy-driven expansion is positioning India as a global alternative manufacturing hub for man-made fiber–based functional garments, particularly for export-oriented PPE, workwear, and climate-adaptive uniforms.

Performance metrics from 2025 indicate strong early traction, with rising turnover and export realization under the PLI framework. Parallel funding under NTTM is accelerating domestic capability in antimicrobial textiles, flame-resistant fabrics, and barrier garments for high-risk industrial and healthcare environments. India’s competitive strength is emerging at the intersection of cost-efficient scale, regulatory support, and growing domestic demand for safety-compliant functional apparel.

South Korea: Sensorized Textiles and Shape-Memory Fiber Innovation

South Korea is carving out a specialized position in the functional apparel market by focusing on the intelligence layer-where materials science, electronics, and apparel converge. Government-backed R&D programs are channeling capital into on-device AI, flexible sensors, and phase-change materials that enable garments to actively respond to body heat and external conditions. This strategy aligns closely with South Korea’s broader leadership in semiconductors and advanced materials.

Corporate innovation is reinforcing this direction, with recycled spandex, cooling yarns, and shape-memory fibers being engineered for global athleisure, medical, and industrial applications. The planned establishment of mini-fabs for electronic textiles reflects a strategic intent to localize critical components of smart apparel supply chains. South Korea’s role in the market is less about volume and more about defining next-generation functional architectures for wearable intelligence.

France: Chemical Regulation and Sustainable Functional Redesign

France is exerting disproportionate influence on the global functional apparel market through regulatory leadership. The 2025 prohibition of PFAS in consumer clothing and footwear has forced a fundamental redesign of waterproofing, stain resistance, and durability systems across the industry. This has accelerated the adoption of fluorine-free durable water repellents and bio-based surface treatments, reshaping supplier qualification standards well beyond French borders.

Complementing chemical restrictions, France’s mandatory environmental cost labeling framework is pushing brands toward lifecycle transparency and eco-design principles. Functional apparel producers operating in or exporting to France are now redesigning materials, coatings, and supply chains to meet these benchmarks. As a result, France has become the reference market for sustainability-compliant functional apparel, influencing global sourcing and material innovation priorities.

Germany and the European Union: Circular Functional Apparel and Protech Leadership

Germany remains the engineering nucleus of Europe’s functional apparel ecosystem, supported by Horizon Europe funding and EU-wide circularity mandates. The “Textiles of the Future” partnership is accelerating the commercialization of recycled functional fibers, moving projects from pilot scale toward industrial readiness. This funding focus is reinforcing Germany’s leadership in high-TRL deployment rather than early-stage experimentation.

At the regulatory level, the introduction of Extended Producer Responsibility for textiles is accelerating investment in monomaterial functional garments designed for full recyclability. Germany also continues to dominate the Protech segment, with advanced testing and certification infrastructure supporting arc-flash, chemical-resistant, and high-visibility workwear. The EU’s coordinated policy framework is positioning Europe as the global benchmark for circular, safety-certified functional apparel.

Strategic Driver Summary: Functional Apparel Market (2025)

Functional Apparel Market Matrix

|

Country / Region

|

Primary Strategic Driver

|

Key Policy / Development (2025)

|

Priority Functional Apparel Focus

|

|

United States

|

Defense & healthcare integration

|

DoD “Soldier Systems” expansion, AFFOA scaling

|

Biometric wearables, smart uniforms

|

|

China

|

Domestic brand science

|

14th Five-Year Plan completion

|

Performance activewear, smart factories

|

|

India

|

Manufacturing localization

|

PLI for technical textiles

|

MMF-based Protech & Meditech

|

|

South Korea

|

Materials intelligence

|

KRW-backed sensor and fiber R&D

|

Shape-memory & cooling textiles

|

|

France

|

Sustainability regulation

|

PFAS ban, environmental cost labeling

|

Fluorine-free functional coatings

|

|

Germany / EU

|

Circular economy

|

Horizon Europe & EPR rules

|

Recyclable Protech functional apparel

|

Functional Apparel Market Report Scope

Functional Apparel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$428.6 Billion

|

|

Market Size (2035)

|

$843.1 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Product Type (Sportswear & Activewear, Protective Clothing, Medical-Functional Apparel, Military & Defense Apparel, Vanity-Functional Apparel, Cross-Functional Assemblies), By Functionality (Environmental Hazard Protection, Moisture Management, Antimicrobial & Odor Control, Smart & Integrated Technology, Mechanical Protection), By Fabric Type (Synthetic Polymers, Natural Fibers, Specialty Fibers, Smart & Electronic Textiles), By Consumer Group (Men, Women, Children, Special Needs), By Distribution Channel (Online & E-Commerce, Specialty Stores, Supermarkets & Hypermarkets, Institutional & Government Sales)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nike Inc., Adidas AG, Lululemon Athletica Inc., Under Armour Inc., VF Corporation, Puma SE, ASICS Corporation, Columbia Sportswear Company, Fast Retailing Co., Ltd., Hanesbrands Inc., Cintas Corporation, Anta Sports Products Limited, Industria de Diseño Textil S.A., Amer Sports Corporation, Gap Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Functional Apparel Market Segmentation

By Product Type

- Sportswear and Activewear

- Protective Clothing

- Medical-Functional Apparel

- Military and Defense Apparel

- Vanity-Functional Apparel

- Cross-Functional Assemblies

By Functionality

- Environmental Hazard Protection

- Moisture Management

- Antimicrobial and Odor Control

- Smart and Integrated Technology

- Mechanical Protection

By Fabric Type

- Synthetic Polymers

- Natural Fibers

- Specialty Fibers

- Smart and Electronic Textiles

By Consumer Group

- Men

- Women

- Children

- Special Needs

By Distribution Channel

- Online and E-Commerce

- Specialty Stores

- Supermarkets and Hypermarkets

- Institutional and Government Sales

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Functional Apparel Market

- Nike, Inc.

- Adidas AG

- Lululemon Athletica Inc.

- Under Armour, Inc.

- VF Corporation

- Puma SE

- ASICS Corporation

- Columbia Sportswear Company

- Fast Retailing Co., Ltd.

- Hanesbrands Inc.

- Cintas Corporation

- Anta Sports Products Limited

- Industria de Diseño Textil, S.A.

- Amer Sports Corporation

- Gap Inc.

*- List not Exhaustive