Glycidyl Methacrylate Market to Reach $532.1 Million by 2034 at 7.2% CAGR Driven by Specialty Monomer Upgrades, 6G Resin Demand, and Bio-Based Coatings Innovation

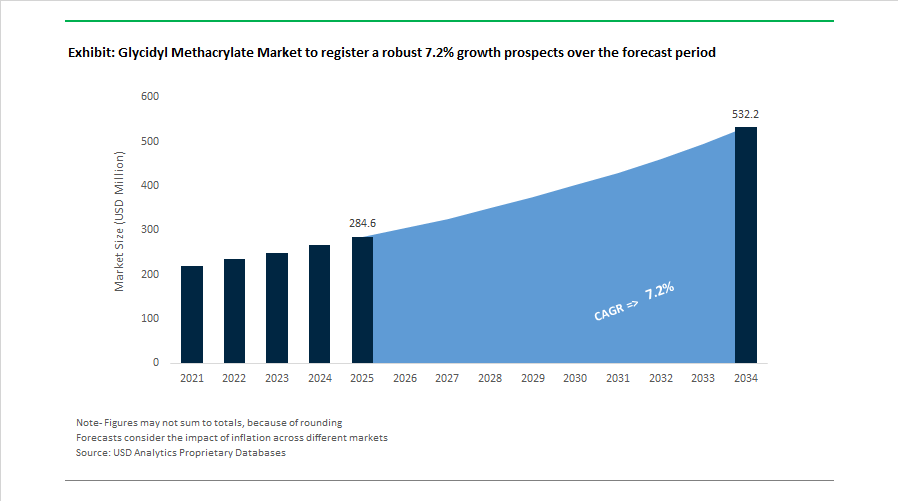

The Glycidyl Methacrylate (GMA) Market is projected to expand from $284.6 Million in 2025 to $532.1 Million by 2034, registering a CAGR of 7.2%. Growth is being fueled by rising demand for high-performance acrylic monomers in automotive coatings, industrial adhesives, 5G/6G electronics resins, biomedical scaffolds, and specialty packaging. Increasing focus on high-purity specialty methacrylates, bio-based GMA development, and regulatory-aligned production standards is strengthening the competitive position of established global producers across North America, Japan, and Europe.

In early 2024, Dow Inc. completed a major production upgrade at its Freeport, Texas facility to address tightening supply of specialty monomers required for high-performance adhesives and coatings in North America. During 2024, Mitsubishi Gas Chemical Company, Inc. finalized a strategic capacity expansion at its Niigata plant to reinforce global supply of high-purity GMA for automotive and industrial coatings. In the same year, Röhm GmbH acquired SABIC’s Functional Forms business, integrating advanced film technologies with methacrylate chemistry and increasing internal consumption of GMA-based surface modifiers. In July 2024, India implemented mandatory BIS standards for petrochemical imports, tightening quality compliance requirements and favoring global manufacturers with ISO-aligned glycidyl methacrylate production systems. Also in 2024, Lummus Technology and Air Liquide entered a licensing agreement for ester-grade acrylic acid technologies, streamlining upstream acrylate feedstock efficiency for GMA producers.

Portfolio optimization and specialty resin investments accelerated during 2024–2025. In October 2024, Evonik Industries AG reorganized its Coating & Adhesive Resins unit to focus on specialty acrylic systems for medical technology and advanced packaging, emphasizing GMA-based high-performance bonding solutions. In January 2025, green-chemistry startups introduced pilot-scale bio-based glycidyl methacrylate formulations using renewable feedstocks, targeting eco-friendly architectural coatings and sustainable packaging applications. In 2025, biomedical research groups, including collaborators of Merck KGaA, validated GMA-modified hydrogels for 3D-printed tissue scaffolds, leveraging the monomer’s dual epoxy and methacrylate functionality for enhanced cross-linking and mechanical strength. Mid-2025 also saw electronics material suppliers in Japan and South Korea launch high-thermal-stability GMA-based resins engineered for 6G communication hardware, addressing dielectric performance requirements for high-frequency circuit boards.

Capacity expansion continued into 2026. In February 2026, Evonik announced further expansion of its hydroxyl-terminated polybutadiene infrastructure, including prior expansions in Marl in 2024 and Shanghai in 2025, and the engineering of a new Asian facility. GMA serves as a critical functionalizing agent in these resin systems to enhance adhesion and thermal stability. In November 2025, Dow presented polymer modifiers incorporating GMA chemistry at in-cosmetics Asia, highlighting applications in durable film-forming personal care products. In January 2026, Dow launched its Transform to Outperform initiative to enhance productivity and margins across Performance Materials & Coatings, reinforcing its strategic emphasis on specialty monomers such as glycidyl methacrylate.

The Glycidyl Methacrylate Market outlook reflects increasing specialty acrylic monomer demand, compliance-driven quality upgrades, 6G electronics resin innovation, biomedical material integration, renewable feedstock pilots, and upstream acrylic acid technology optimization. Competitive differentiation is increasingly defined by high-purity production capacity, epoxy-functional monomer performance, thermal stability metrics, regulatory compliance in emerging markets, and integration into high-margin coatings, adhesives, electronics, and advanced polymer applications.

Glycidyl Methacrylate (GMA) Market Trends and Strategic Growth Opportunities

Regulatory-Led Scaling of GMA-Functionalized Resins for Low-VOC Automotive Coatings

The Glycidyl Methacrylate market is being structurally reshaped by tightening environmental regulations that are accelerating the shift toward low-VOC, high-solid, and waterborne coating technologies. The January 2025 implementation of updated U.S. national VOC emission standards has pushed automotive OEMs and tier-one coating suppliers to redesign resin architectures that deliver durability at substantially reduced solvent levels. GMA plays a central role in this transition as the preferred monomer for introducing glycidyl functionality into acrylic systems, enabling room-temperature crosslinking that improves stone-chip resistance, corrosion protection, and long-term UV stability.

The regulatory catalyst is the revised EPA rule on VOC reactivity factors, which incentivizes the use of lower-ozone-forming monomers such as GMA to support Clean Air Act compliance. This policy shift has triggered widespread portfolio rationalization among resin manufacturers. Mitsubishi Gas Chemical continues to prioritize high-purity GMA production at its Niigata facility, supplying grades above 99% purity for premium automotive clearcoats. At the same time, Dow is expanding deployment of its MAINCOTE and PARALOID acrylic-epoxy hybrid platforms, which leverage GMA chemistry to achieve VOC levels below 25 grams per liter in industrial metal coatings.

Adoption is further supported by automotive lightweighting trends. As electric vehicle platforms increasingly rely on aluminum, composites, and mixed-material assemblies, adhesion performance across dissimilar substrates has become mission critical. By late 2024, industry sourcing data indicated that close to one-fifth of global GMA consumption was tied to specialty coating formulators in the U.S. Midwest, where multi-substrate adhesion promoters based on GMA are being qualified for next-generation EV platforms.

R&D Acceleration in High-Adhesion Dental and Bio-Functional GMA Monomers

Beyond coatings, the dental materials segment is emerging as a high-value growth driver for Glycidyl Methacrylate. Dental manufacturers are moving toward bio-functional restorative systems that improve the long-term stability of the dentin-composite hybrid layer. GMA derivatives, particularly Bis-GMA, are being reformulated to enhance chemical bonding between resin matrices and inorganic fillers, reducing microleakage and clinical failure rates.

Clinical validation is reinforcing this trend. A September 2025 study reported that next-generation GMA-based composite restoratives achieved average shear bond strength levels of approximately 341 newtons, exceeding traditional microhybrid materials by more than 25%. These gains are attributed to optimized monomer-filler interactions enabled by GMA’s reactive epoxy functionality. Parallel innovation is occurring in antimicrobial dentistry. Research supported by the National Institutes of Health has demonstrated that saccharide-derived methacrylate monomers synthesized using GMA can suppress bacterial metabolism of Streptococcus mutans while preserving or enhancing bond durability over extended aging periods.

Handling and processing improvements are also expanding adoption. Studies from 2024 and 2025 show that incorporating low-loadings of pre-polymerized Bis-GMA particles can reduce resin viscosity by more than 50%, significantly improving flowability and degree of conversion in light-cured systems. These performance enhancements are positioning high-purity GMA as a cornerstone monomer in advanced restorative and adhesive dentistry.

High-Elasticity Binders for Silicon-Anode Lithium-Ion Batteries

Electrification of transport represents a frontier opportunity for the Glycidyl Methacrylate market, particularly in the development of next-generation binders for silicon-based lithium-ion battery anodes. Silicon offers energy density improvements of 30 to 50% over conventional graphite, but its volumetric expansion during charging creates severe mechanical stress. GMA-functionalized polymer binders offer a unique solution by introducing reactive epoxy groups that enable crosslinking, adhesion to silicon surfaces, and self-healing behavior.

Materials research published in late 2025 demonstrated that GMA-based self-healing polymer binders can restore chemical connectivity within electrode matrices, delivering capacity retention above 94%after 400 cycles. As companies such as Group14 and NanoGraf scale silicon anode production from 2025 onward, demand for functional binders is expected to accelerate rapidly. Polymer suppliers including Trinseo are actively investing in scalable manufacturing routes for GMA-functionalized binders, identifying this segment as a critical enabler for long-duration, high-energy EV batteries.

High-Clarity GMA Copolymers for Flexible and Printed Electronics

The rapid proliferation of wearable electronics, flexible displays, and printed circuitry is opening a lucrative niche for GMA-based copolymers and adhesives. These applications require materials that combine optical clarity, moisture resistance, and mechanical flexibility while adhering reliably to low-energy substrates such as PET and polyimide. GMA’s epoxy functionality enables strong interfacial bonding without compromising transparency, making it highly attractive for next-generation electronics assembly.

Capacity investments signal growing confidence in this opportunity. Henkel completed a major expansion of its Brandon, South Dakota facility in 2025, positioning the site as a flagship hub for advanced electronic and thermal management adhesives supporting mobility and wearable device platforms. At Electronica 2025, multiple suppliers showcased GMA-enhanced encapsulation and gasketing materials designed for ultra-thin, lightweight electronics used in automotive interiors and smart packaging.

Process innovation is supporting commercialization. To manage the high reactivity of GMA-functionalized two-component systems, equipment providers such as Sonderhoff have introduced precision dosing technologies that ensure consistent mixing and clean application at high production speeds. These developments collectively position Glycidyl Methacrylate as a high-value monomer at the intersection of sustainability, advanced materials, and next-generation electronics manufacturing.

Glycidyl Methacrylate Market Share and Segmentation Insights

Industrial Grade Glycidyl Methacrylate Leads the Market Through High-Volume Polymer and Coating Applications

Industrial Grade accounted for 52.80% of the Glycidyl Methacrylate Market share in 2025, making it the most widely used purity category in global GMA production and consumption. Industrial grade glycidyl methacrylate is primarily utilized in polymer modification, coatings formulations, adhesives, and specialty resin synthesis, where standard purity levels provide sufficient performance while maintaining cost efficiency for large-scale industrial applications. GMA is a highly reactive monomer containing both epoxy and methacrylate functional groups, enabling it to participate in polymerization and grafting reactions that enhance adhesion, chemical resistance, and crosslinking performance in polymer systems. These characteristics make industrial grade GMA particularly valuable in acrylic resins, epoxy-modified polymers, and specialty coatings materials used across construction, automotive, and industrial manufacturing sectors. In 2025, manufacturers have focused on optimizing polymerization inhibitor systems, typically based on compounds such as hydroquinone or MEHQ, to improve storage stability without compromising reactivity. Carefully balanced inhibitor packages allow producers to extend shelf life during storage and transportation, reducing product degradation while preserving the polymerization performance required for downstream resin and coating formulations.

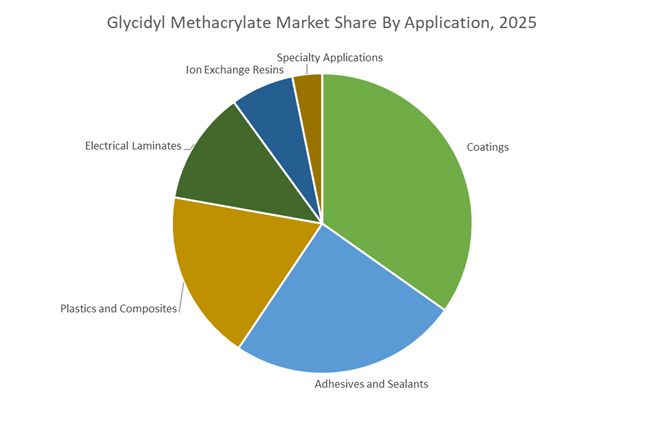

Coatings Industry Drives the Largest Demand for Glycidyl Methacrylate in High-Performance Resin Systems

Coatings represented 34.80% of the Glycidyl Methacrylate Market share in 2025, establishing it as the leading application sector for glycidyl methacrylate-based monomers. In coatings formulations, glycidyl methacrylate functions as a functional monomer incorporated into acrylic, polyester, and epoxy resin systems, where it introduces reactive epoxy groups capable of forming crosslinked polymer networks. These crosslinking reactions significantly enhance adhesion strength, chemical resistance, mechanical durability, and corrosion protection, making GMA-containing resins widely used in automotive coatings, industrial protective coatings, and architectural finishes. In 2025, the coatings segment is experiencing rapid innovation driven by the growing adoption of low-VOC powder coating technologies. Glycidyl methacrylate-based acrylic resins are increasingly used in powder coatings because they enable low-temperature curing, improved weather resistance, and high-gloss surface finishes. These characteristics are particularly valuable in automotive clearcoats and architectural powder coatings, where environmental regulations are placing increasing pressure on traditional curing agents such as TGIC, encouraging manufacturers to adopt GMA-functionalized resin systems.

Competitive Landscape in Glycidyl Methacrylate Market

Mitsubishi Gas Chemical Company Leads Ultra-High-Purity GMA Production

Mitsubishi Gas Chemical Company, Inc. remains the global volume leader in glycidyl methacrylate, positioning the monomer as a core pillar of its Specialty Chemicals growth strategy. In the final year of its MTMP 2026 plan, MGC is adjusting production scales to meet increased demand from AI servers, advanced semiconductor substrates, and optical polymer systems. Its ultra-high-purity GMA grades are engineered for low metal and low impurity profiles, critical for electronic materials and high-frequency circuit boards. In early 2026, MGC revised performance forecasts upward due to strong demand for GMA-modified resins in generative AI server infrastructure. The company continues prioritizing its GMA and MXDA portfolios to reinforce its global presence in specialty monomers with high barrier-to-entry manufacturing standards.

Dow Strengthens Vertically Integrated Performance Monomer Supply

The Dow Chemical Company operates as the leading Western producer of glycidyl methacrylate through its Performance Monomers segment. Dow leverages world-scale manufacturing assets with backward integration into key raw materials, ensuring supply security and cost efficiency across North America and Europe. GMA is positioned as a critical building block in automotive coatings, structural adhesives, and industrial protective systems where enhanced cross-linking improves durability and chemical resistance. During late 2025 and early 2026, Dow secured ISCC PLUS certification for acrylate and monomer production, supporting sustainable and bio-attributed GMA offerings. Its strategic emphasis on e-mobility integrates GMA into battery enclosure coatings and electronic component protection systems for electric vehicles.

Evonik Expands Sustainable VISIOMER® Specialty Methacrylates

Evonik Industries AG markets glycidyl methacrylate under its VISIOMER® portfolio, targeting high-value coatings and adhesive applications requiring controlled reactivity and low odor. Under its Next Generation strategy, Evonik is focusing on label-friendly, low-VOC specialty methacrylates compatible with water-borne and high-solid coating systems. VISIOMER® GMA plays a central role in enabling cross-linking and adhesion promotion under increasingly stringent 2026 VOC regulations. At the American Coatings Show 2026, Evonik is highlighting sustainable VISIOMER® Terra solutions that incorporate bio-based content into methacrylate formulations. The company’s long-term carbon reduction objectives position GMA as a tool for extending material life cycles in infrastructure and industrial maintenance coatings.

Sumitomo Chemical Integrates GMA with Chemical Recycling Technologies

Sumitomo Chemical Co., Ltd. is embedding glycidyl methacrylate into its ICT and Mobility Solutions strategy under the Boost 2028 initiative. In February 2026, the company confirmed commercial availability of PMMA Chemical Recycling technology in partnership with Lummus Technology, enabling conversion of end-of-life acrylics into high-purity monomers. This circular approach is expected to extend to broader methacrylate portfolios including GMA. GMA is used to functionalize advanced display materials, automotive lighting components, and specialty resins for electronics. ISCC PLUS certification for chemically recycled MMA supports the company’s sustainability positioning, while financial restructuring initiatives in early 2026 reinforce capital allocation toward electronic chemicals and advanced polymer segments.

Estron Chemical Focuses on High-GMA Acrylic Resin Systems

Estron Chemical, Inc. is a specialized manufacturer known for high-GMA-content acrylic resins used in powder coatings and thermoset applications. Its Isocryl® resin series is widely adopted in clear-coat automotive finishes due to superior weatherability, clarity, and cross-link density. In 2026, Estron is expanding its South Korean manufacturing operations to better serve Asia-Pacific electronics and laminate markets. The company emphasizes formulation versatility, enabling customers to fine-tune mechanical strength and chemical resistance through tailored GMA-functionalized additives. Its focus on specialty resin systems positions Estron as a key supplier for high-performance refinish and industrial coating segments.

Merck KGaA Supplies High-Purity GMA for Biomedical and Semiconductor Markets

Merck KGaA, through its Life Science and Electronics divisions, supplies high-purity glycidyl methacrylate for pharmaceutical, biomedical, and semiconductor applications. GMA reagents are utilized in hydrogel-based materials for blood-contacting medical devices and catheter coatings requiring controlled cross-linking. In 2026, Merck is integrating digital traceability platforms across its monomer catalog to ensure compliance with stringent GMP and semiconductor-grade quality standards. The company is leveraging strong growth in Indian and Chinese pharmaceutical packaging markets, which are expanding at approximately 9 to 10%CAGR. Its Life Science 2030 sustainability roadmap emphasizes safer handling and reduced environmental impact in the production and distribution of reactive methacrylate monomers such as GMA.

Japan: Semiconductor Purity Leadership and Circular Polymer Integration

Japan continues to define the upper end of the glycidyl methacrylate industry through its emphasis on electronic-grade purity, feedstock security, and circular material flows. In late 2024, Mitsubishi Gas Chemical completed a major expansion at its Niigata facility, explicitly targeting ultra-high-purity GMA for electronics and advanced materials. This strategic move was reinforced in November 2025 through a long-term agreement with Transition Industries, securing access to ultra-low-carbon methanol and positioning GMA production on a defined pathway toward carbon-neutral manufacturing under the company’s Carbopath platform by 2029.

From an application standpoint, Japanese producers are setting global benchmarks by scaling 99.9% plus assay grades. These electronic-grade GMA monomers are being increasingly specified in 2026 for next-generation photoresists and 5G base-station laminates, where dielectric stability and impurity control directly affect signal reliability. Circularity is also gaining commercial traction. In September 2025, Mitsubishi Chemical Group demonstrated recycled acrylic resins containing GMA-based modifiers for exterior components on the Honda N-ONE e: electric vehicle, signaling the integration of glycidyl methacrylate into closed-loop automotive polymer systems. Parallel investments in Mechanical Vapor Recompression distillation are helping domestic producers offset high imported energy costs while cutting thermal energy demand by roughly 15% heading into 2026.

United States: Composite Materials Scale-Up and Regulatory Traceability

In the United States, glycidyl methacrylate demand is being driven by structural materials innovation and tightening regulatory oversight. Following the completion of its Freeport, Texas expansion, Dow Chemical has scaled production of its DERAKANE-GMA and PRIMACOR-GMA lines. For the 2026 cycle, these materials are being prioritized as lightweight, high-strength binders for electric vehicle battery housings and aerospace composite structures, where chemical resistance and fatigue performance are critical.

Regulation is simultaneously reshaping operational practices. Updated reporting requirements under the Toxic Substances Control Act, issued by the Environmental Protection Agency, will take effect in May 2026 and mandate enhanced lot-level traceability for epoxide-based functional monomers, including GMA. This is driving investments in digital compliance systems across the value chain. On the innovation front, Dow’s MobilityScience portfolio launched in the 2025–2026 window features GMA-modified polyolefin elastomers designed for automotive seating foams and cable jacketing that align with forthcoming end-of-life vehicle directives. Additional Gulf Coast investments in 2025 have brought specialized GMA-based adhesive lines online for commercial aviation maintenance, reinforcing the role of glycidyl methacrylate in high-value, regulation-sensitive applications.

Germany: Bio-Circular Methacrylates and Low-Odor Coating Systems

Germany’s glycidyl methacrylate industry is evolving in close alignment with European sustainability mandates and performance-driven coatings demand. In May 2025, Evonik launched its VISIOMER eCO line, incorporating GMA derivatives produced from circular and bio-circular feedstocks certified under ISCC PLUS. These materials are positioned to support compliance with European Green Deal objectives, particularly in industrial coatings and structural adhesives scheduled for wider adoption in 2026.

Innovation visibility accelerated at the European Coatings Show 2025 in Nuremberg, where German formulators introduced label-friendly specialty methacrylates using GMA to enable low-odor, ambient-temperature curing for flooring and protective coatings. At the production level, Evonik’s ongoing portfolio optimization at the Marl Chemical Park through 2027 is concentrating capital on Next Generation Solutions, with glycidyl methacrylate serving as a critical reactive diluent in sustainable resin architectures. This strategic focus underscores Germany’s role as a technology and formulation hub rather than a volume-driven supplier.

China: Scale Manufacturing, Export Momentum, and PFAS Substitution

China’s glycidyl methacrylate industry remains structurally centered on scale efficiency, export competitiveness, and rapid process automation. In 2025, the Ministry of Industry and Information Technology intensified smart manufacturing mandates across Shandong chemical clusters, pushing producers to integrate AI-driven catalytic control systems to optimize allyl alcohol epoxidation and improve yield stability in GMA synthesis.

On the supply side, Lier Chemical completed a significant capacity expansion in August 2025, consolidating its position as a major exporter of technical-grade GMA to Southeast Asian plastics and rubber additive markets. Beyond volume growth, functional innovation is emerging. In December 2025, Mitsubishi Chemical’s China operations advanced GMA-modified SoarnoL gas-barrier coatings for paper packaging, offering oil-resistant performance as a substitute for PFAS-based treatments. This development aligns with global regulatory bans on per- and polyfluoroalkyl substances expected to tighten in 2026, opening a new compliance-driven demand channel for GMA-modified polymers.

India: Bio-Based Policy Push and Fast-Curing Coatings Innovation

India’s glycidyl methacrylate landscape is in an early but strategically important transition phase, shaped by policy alignment and start-up-led innovation. Under the BioE3 policy framework, the Indian government has identified bio-based GMA intermediates as priority molecules to reduce reliance on imported Chinese technical-grade materials. This policy signal is encouraging domestic investment in upstream epoxide chemistry and downstream resin formulation capabilities.

At the application level, innovation is being driven by emerging technology firms. In late 2025, NanoEpoxy Labs piloted nano-reinforced GMA dispersions capable of reducing curing times in industrial paints by up to 40%. These systems are being positioned for infrastructure and urban development projects, where faster turnaround and improved surface durability offer clear economic advantages. While current volumes remain modest, the combination of policy support and performance-driven use cases is laying the groundwork for broader adoption through 2026.

Comparative Overview: Glycidyl Methacrylate Industry by Country

Glycidyl Methacrylate Market County Level Snapshot

|

Country / Region

|

Strategic Focus Area

|

Structural Impact on GMA Industry

|

|

Japan

|

Semiconductor purity and circular polymers

|

Leadership in ultra-high-purity and recycled GMA

|

|

United States

|

EV and aerospace composites, TSCA compliance

|

High-value demand with strong regulatory oversight

|

|

Germany

|

Bio-circular feedstocks and sustainable coatings

|

Technology-led growth in specialty formulations

|

|

China

|

Smart manufacturing and export scale

|

Cost-efficient supply and PFAS replacement solutions

|

|

India

|

BioE3 policy and fast-curing coatings

|

Emerging demand driven by infrastructure and innovation

|

Glycidyl Methacrylate Market Report Scope

Glycidyl Methacrylate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$284.6 Million

|

|

Market Size (2034)

|

$532.1 Million

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Purity Type (High-Purity Grade, Industrial Grade, Standard Grade), By Application (Coatings, Adhesives and Sealants, Plastics and Composites, Electrical Laminates, Ion Exchange Resins, Specialty Applications), By End-Use Industry (Automotive and Transportation, Electrical and Electronics, Building and Construction, Packaging and Printing, Aerospace and Defense, Healthcare and Biomedical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Mitsubishi Gas Chemical Company, Inc., Mitsubishi Chemical Group Corporation, Evonik Industries AG, Sumitomo Chemical Co., Ltd., Estron Chemical, Inc., NOF Corporation, Osaka Organic Chemical Industry Ltd., Lier Chemical Co., Ltd., Jiangsu Sanmu Group, Hubei Xian Shen Biotechnology Co., Ltd., Jin Dun Chemical, Lianyungang Ningkang Chemical Co., Ltd., Hexion Inc., Kowa American Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glycidyl Methacrylate Market Segmentation

By Purity Type

- High-Purity Grade

- Industrial Grade

- Standard Grade

By Application

- Coatings

- Adhesives and Sealants

- Plastics and Composites

- Electrical Laminates

- Ion Exchange Resins

- Specialty Applications

By End-Use Industry

- Automotive and Transportation

- Electrical and Electronics

- Building and Construction

- Packaging and Printing

- Aerospace and Defense

- Healthcare and Biomedical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Glycidyl Methacrylate Industry

- Dow Inc.

- Mitsubishi Gas Chemical Company, Inc.

- Mitsubishi Chemical Group Corporation

- Evonik Industries AG

- Sumitomo Chemical Co., Ltd.

- Estron Chemical, Inc.

- NOF Corporation

- Osaka Organic Chemical Industry Ltd.

- Lier Chemical Co., Ltd.

- Jiangsu Sanmu Group

- Hubei Xian Shen Biotechnology Co., Ltd.

- Jin Dun Chemical

- Lianyungang Ningkang Chemical Co., Ltd.

- Hexion Inc.

- Kowa American Corporation

*- List not Exhaustive