Heat Transfer Fluids Market Overview

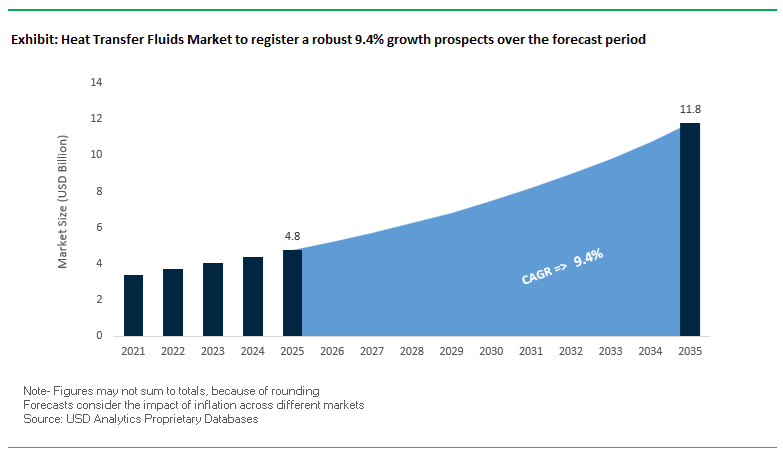

The global heat transfer fluids market is projected to grow from USD 4.8 billion in 2025 to around USD 11.8 billion by 2035, registering a strong CAGR of 9.4% between 2025 and 2035. This growth trajectory is underpinned by rapid adoption of synthetic heat transfer oils, glycol-based thermal fluids, and dielectric EV thermal management fluids across concentrated solar power (CSP), data centers, electric vehicles, chemical processing, and HVAC. For manufacturers and vendors, the market is increasingly defined by temperature stability, viscosity control, corrosion protection, and compatibility with low-carbon and electrification trends, making performance specifications and regulatory compliance central to product differentiation.

Advanced CSP heat transfer fluids are now engineered for continuous operation at temperatures up to 400°C, enabling higher solar-to-electric efficiency and longer plant lifetimes. At the same time, next-generation PAG and silicone-based low-temperature heat transfer fluids are being optimized for pumpability below −40°C to support cold chain logistics and cryogenic systems. In the e-mobility space, dielectric EV thermal fluids and immersion cooling fluids for AI data centers are becoming strategic high-value niches, where vendors differentiate on rapid heat removal, safety, and compatibility with high-voltage electronics. Glycol-based fluids are also increasingly engineered to meet stringent corrosion protection standards and sustainability requirements, driving demand for advanced additive packages and long-life formulations.

Key insights for heat transfer fluid manufacturers and vendors:

- Concentrated Solar Power operating range: Advanced synthetic thermic fluids used in CSP tower systems are designed to maintain thermal stability and low-pressure operation at continuous bulk temperatures up to 400°C (≈750°F), enabling higher efficiency in large-scale solar power plants.

- Low-temperature viscosity optimization: Modified Polyalkylene Glycol (PAG) and silicone-based low-temperature heat transfer fluids are achieving viscosities of <100 cP at −40°C, ensuring reliable circulation and heat transfer efficiency in cold chain logistics and cryogenic applications.

- EV battery charging and thermal management: Emerging dielectric thermal fluids based on Gas-to-Liquid (GTL) technology can support up to a 70% reduction in EV battery charging time (for example, 10% to 80% state-of-charge in under 10 minutes), by maintaining safe cell temperatures during ultra-fast charging.

- Data center immersion cooling performance: Specialized immersion cooling fluids used in HPC and AI data centers can deliver a heat dissipation capacity up to 1,200 times higher than air, enabling higher rack densities and power loads while reducing cooling energy consumption.

- Corrosion protection standards in industrial systems: High-performance glycol-based heat transfer fluids for HVAC and process heating are typically formulated to achieve a metal loss rate of <0.1 mm/year on critical metals such as copper and aluminum, aligning with ASME code requirements and extending system life.

Recent Heat Transfer Fluid Developments Across EV, Data Center, and CSP Applications

From June 2024 to late 2025, the global heat transfer fluids market has been defined by a wave of product innovation and application-specific launches targeting EVs, AI data centers, pharmaceuticals, and process industries. In December 2024, Castrol introduced ON Direct Liquid Cooling PG 25, a propylene glycol-based heat transfer fluid engineered for direct-to-chip liquid cooling in AI and high-performance computing (HPC) systems, signalling the growing strategic importance of immersion and direct liquid cooling for next-generation servers. This was complemented by HF Sinclair’s INNOVATE series, launched in October 2024, featuring immersion cooling fluids based on Highly Refined Alkanes (HRA) designed for excellent oxidative stability and high heat transfer performance in immersed computing environments. In January 2025, Global Heat Transfer strengthened its presence in process industries with Globaltherm® Q, a synthetic organic fluid covering an operating range from −35°C to 330°C, targeted at pharmaceutical, oil & gas, and plastics processing plants requiring broad temperature windows and predictable thermal performance.

The EV thermal management segment continues to drive a major share of innovation. In October 2024, Prestone expanded its EV thermal management fluids portfolio with three new products, including an ultra-low-conductivity fuel cell coolant designed to align with the GB29743.2 standard, which OEMs must fully adhere to by mid-2026. Around the same period in 2024, Dow Chemical introduced an enhanced glycol-based heat transfer fluid that delivers a reported 15% improvement in thermal stability, directly addressing industrial customers’ need for higher efficiency and longer fluid life in cooling loops. In September 2025, Shell Lubricants announced a major breakthrough with its Shell EV-Plus Thermal Fluid, demonstrating the ability to charge EV battery packs from 10% to 80% in under 10 minutes by dramatically reducing thermal stress and enabling ultra-fast charging profiles. Building on this, in November 2025, Shell validated that Shell EV-Plus could function as a single-circuit fluid managing the thermal requirements of the battery, motor, and power electronics in a battery electric vehicle, simplifying system design and reducing component count and weight.

On the distribution and ecosystem side, Eastman Chemical Company deepened its market reach in October 2025 by appointing RelaDyne as an authorized distributor for its Therminol® heat transfer fluids across the United States, thereby widening customer access to Therminol products and to the Fluid Genius™ digital monitoring platform, which enables predictive maintenance and fluid life optimization. Collectively, these developments signal a clear shift of the heat transfer fluids industry toward highly engineered, application-specific formulations aligned with electrification, digitization, and low-carbon energy systems, supported by stronger downstream technical services and digital monitoring tools.

Technology-Driven Trends Accelerating Low-GWP Cooling, Electrification, and High-Temperature Renewable Systems

Market Trend 1: Commercial-Scale Shift Toward Ultra-Low GWP Synthetic Fluids for Electrification and Immersion Cooling

The Heat Transfer Fluids Market is undergoing a structural transformation driven by the rapid global shift toward low-GWP synthetic fluids that address both climate regulations and next-generation cooling requirements for EVs, grid electrification, and hyperscale data centers. New hydrofluoroolefin (HFO) formulations—particularly R1234ze—deliver GWP values below 10, replacing legacy refrigerants such as R134a with GWP as high as 1,430. This reduction directly supports global decarbonization mandates, enabling OEMs and data center operators to comply with F-Gas reductions and EPA AIM Act guidelines.

Beyond environmental compliance, advanced synthetic dielectric fluids engineered for immersion cooling demonstrate exceptional AC breakdown voltages of 35–45 kV, ensuring complete electrical insulation for EV battery packs, power electronics, and high-voltage data center systems. This dielectric strength is critical as both EV platforms and AI compute clusters scale to higher voltages and power densities.

A parallel breakthrough is occurring in two-phase immersion cooling for data centers, where low-GWP fluids enable Power Usage Effectiveness (PUE) levels as low as 1.02–1.03, compared to ≈1.70 for conventional air-cooled facilities. These fluids deliver near-isothermal heat removal, effectively eliminating hotspots while enabling compute racks to run beyond 120 kW per rack—an essential capability for AI supercomputing.

Notably, despite drastic reductions in climate impact, modern HFOs match or outperform high-GWP predecessors in thermal performance, including reduced discharge temperatures in EV battery thermal management systems. This combination of regulatory compliance, electrification performance, and data-center cooling efficiency cements low-GWP synthetic fluids as a core growth engine within the heat transfer fluids industry.

Market Trend 2: Retrofitting CSP Infrastructure with Next-Generation Chloride-Based Molten Salts for Higher Efficiency

The second major trend driving Heat Transfer Fluids Market innovation is the large-scale modernization of Concentrated Solar Power (CSP) plants through advanced molten salt chemistry. New chloride-based formulations such as MgCl₂–KCl–NaCl unlock a much broader liquidus range, with melting points of <400°C (≈380°C) and thermal stability up to ≈800°C. This significantly expands CSP operating windows beyond traditional nitrate-based Solar Salt, which melts at ≈220°C but is constrained to ≈565°C maximum operating temperature.

By operating CSP receivers at 700–800°C, chloride salts enable 15–20% higher thermal-to-electric conversion efficiency, transforming CSP into a more competitive gigawatt-scale renewable generation technology. However, high-temperature chloride chemistry introduces corrosion challenges—now being addressed via active metal additives (e.g., Mg) and electrochemical purification, which reduce corrosion rates of high-nickel alloys such as Hastelloy by up to 35× at 850°C. This greatly extends component lifespan and supports long-duration thermal storage for renewable baseload generation.

Because CSP plants globally are aging yet structurally sound, the demand for strategic retrofits using chloride molten salts is accelerating, positioning next-generation HTFs as catalysts for unlocking higher efficiency and improved plant economics across solar-rich regions.

Strategic Growth Opportunities in Battery Energy Storage and High-Temperature Green Hydrogen Systems

Market Opportunity 1: Expansion of Liquid-Based Thermal Management Systems for Grid-Scale BESS Installations

Grid operators, utilities, and battery integrators are increasingly shifting to liquid-cooled thermal management solutions for large Battery Energy Storage Systems (BESS), creating a high-value opportunity for heat transfer fluid suppliers. Liquid cooling offers up to 25× higher heat dissipation than air cooling—an essential capability for stabilizing utility-scale BESS installations above 100 MWh, where thermal runaway propagation risk increases with pack size.

Liquid-cooled systems deliver superior temperature uniformity, minimizing ΔT across thousands of interconnected cells, which extends battery cycle life by 10% or more while ensuring consistent electrochemical behavior. Moreover, only liquid cooling can keep high-density battery systems within the optimal 15–35°C temperature window during rapid charge/discharge events required for grid smoothing, frequency regulation, and renewable energy firming.

As the global grid transitions toward multi-GW battery deployment, the demand for stable, safe, non-conductive dielectric heat transfer fluids and water-glycol blends will accelerate, creating one of the fastest-growing opportunity segments in the heat transfer fluids market.

Market Opportunity 2: Development of High-Temperature, Non-Fouling Heat Transfer Fluids for Green Hydrogen & Ammonia Production

Industrial decarbonization is creating a new opportunity for ultra-high-temperature heat transfer fluids capable of supporting green hydrogen electrolysis, ammonia cracking, and high-temperature catalytic processes. These systems increasingly require operating temperatures of 600–900°C, far beyond the capabilities of traditional synthetic aromatic HTFs, which degrade above ≈357°C (675°F)—leaving a 250°C+ technology gap.

Emerging candidates include molten salts, liquid metals, and ceramic particle slurries engineered for long-duration thermal stability and minimal fouling, outperforming mineral oils by offering 10× greater resistance to oxidation and sludge formation. This extended lifetime directly reduces downtime and maintenance costs in high-capital chemical plants, improving economic feasibility for hydrogen and ammonia pathways.

As global hydrogen strategies accelerate and high-temperature reactors become central to ammonia-to-hydrogen conversion, advanced non-fouling HTFs represent a critical enabling technology for reliable, industrial-scale green molecule production.

Heat Transfer Fluids Market Share Analysis

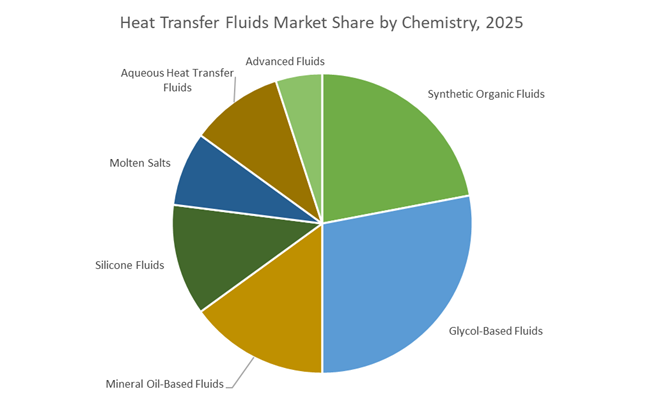

Market Share by Chemistry: Synthetic Organic Fluids Lead High-Temperature Performance Applications

Synthetic organic fluids hold the largest share of the heat transfer fluids market—approximately 22% in 2025—driven by their ability to meet the increasingly stringent thermal and operational requirements of modern industrial systems. Their engineered molecular structures provide superior thermal stability, enabling safe and efficient operation at temperatures exceeding 300–400°C, which is far beyond the capability of mineral-oil-based or glycol-based alternatives. This performance advantage is critical in high-intensity environments such as polymerization, fine chemical synthesis, petrochemical processing, and particularly concentrated solar power (CSP) plants, where consistent thermal output directly influences energy conversion efficiency. Their low viscosity across the operating range enhances pumpability and heat transfer coefficients, ensuring lower energy consumption and improved overall system efficiency—factors that industrial operators prioritize as global energy costs rise. Additionally, the longer service life of synthetic fluids reduces downtime, maintenance expenditure, and fluid replacement cycles, making them a compelling option for continuous-run facilities. The combined value proposition of high-temperature reliability, oxidation resistance, and operational efficiency solidifies synthetic organic fluids as the dominant chemistry segment in the heat transfer fluids market.

Market Share by End-User Industry: Chemical & Petrochemical Processing Drives Largest Consumption

The Chemical & Petrochemical Processing sector accounts for the largest share—approximately 25% of global demand—anchored by the industry’s reliance on uninterrupted, precisely controlled thermal systems across large-scale and high-throughput operations. Processes such as reactor heating and cooling, fractional distillation, re-boiling, and heat exchange in polymer, resin, and specialty chemical manufacturing require heat transfer fluids capable of delivering stable performance under extreme temperature and pressure conditions. As many of these operations run continuously, often 24/7, the sector consumes substantial volumes of high-end HTFs, particularly synthetic organic fluids known for their thermal resilience and long operational lifespan. The rising need for energy-efficient production and compliance with tightening global environmental and energy standards further accelerates the shift toward advanced heat transfer fluids that minimize heat loss, enhance system efficiency, and reduce carbon footprint. Petrochemical complexes, refineries, and specialty chemical manufacturers are also modernizing thermal systems to support digitalized process control and higher operating temperatures, reinforcing the segment’s dominant share in the global HTF demand landscape.

Country Analysis: Global Drivers in the Heat Transfer Fluids Ecosystem

United States: High-Temperature HTF Innovation Driven by ARPA-E, CSP Advancements, and Industrial Electrification

The United States remains a global epicenter for high-performance Heat Transfer Fluids (HTFs), driven by a combination of federal research funding, advanced chemical engineering expertise, and large-scale industrial modernization. The DOE’s ARPA-E HITEMMP program has significantly accelerated innovation by allocating 2024–2025 funding toward next-generation thermal exchange solutions capable of withstanding temperatures approaching 800°C, indirectly stimulating demand for ultra-stable synthetic and engineered HTFs. This research agenda supports breakthrough materials and high-temperature process loops that require fluids with exceptional oxidative stability, vapor pressure control, and heat flux performance. America’s leadership further extends into specialty silicone-based HTFs, as Dow Inc. continues to expand its SYLTHERM™ product line engineered for liquid-phase operations from –40°C to 400°C, enabling reliable thermal regulation across pharmaceuticals, advanced chemical synthesis, and precision manufacturing.

The U.S. is also pushing boundaries in concentrated solar power (CSP) systems, supported by the DOE’s SIPS 2024 initiatives, which allocated $5.4 million toward innovations in solar receiver strain monitoring and advanced turbomachinery. These advancements rely heavily on aromatic synthetic fluids like DOWTHERM™ A, known for stability under cyclic thermal loads. Parallel to renewable energy, U.S. industrial electrification trends are reshaping heat fluid usage in automated plants, where synthetic HTFs support continuous process heating, waste heat recovery, and efficiency-driven thermal optimization. Together, these strategic developments reinforce the U.S. as a global leader in high-temperature, high-stability, research-driven heat transfer fluid technologies.

China: Industrial Heat Transfer Fluid Scale-Up and Solar Thermal System Dominance

China’s role in the global Heat Transfer Fluids Market is defined by its massive manufacturing base, accelerated shift toward industrial sustainability, and unmatched leadership in the solar thermal energy landscape. Chinese producers ramped up production capacities for synthetic HTFs in 2024 to meet rising demand from polymer, polyester, and specialty chemical manufacturing, where processes commonly exceed 350°C and require fluids with high thermal conductivity, oxidative resistance, and long lifecycle stability. The country's dominance in the solar thermal sector remains unparalleled—China accounted for nearly 64% of global solar water collector sales in 2024, driving exceptional volume demand for glycol-based HTFs used in district heating, rooftop systems, and industrial heat networks.

As competition intensifies in traditional solar water heater markets, Chinese solar firms are transitioning toward large-scale Solar Heat for Industrial Processes (SHIP), an area that relies heavily on high-temperature synthetic oils for stable, high-efficiency thermal transfer. Domestic players such as Dalian Richfortune Chemicals are also expanding portfolios to reduce dependency on imported HTFs, offering specialty thermal oils tailored for oil & gas, chemical processing, and high-load heat circulation systems. China’s ability to rapidly scale production while integrating HTFs across renewable energy, petrochemicals, and industrial heating positions it as a global anchor for future thermal fluid market expansion.

Germany: Bio-Based Thermal Fluids, Green Chemistry, and High-Efficiency Industrial Heat Management

Germany stands at the forefront of Europe’s Heat Transfer Fluids innovation, driven by strict environmental regulations, strong sustainability mandates, and its engineering-intensive industrial base. Leading European chemical companies—including BASF SE and LANXESS—are investing in new generations of synthetic organic HTFs engineered for exceptional thermal stability, low fouling, and extended operating life in high-load European chemical plants. The country’s sustainability push is further supported by EU-funded initiatives promoting green chemistry, enabling the adoption of bio-based and renewable substitutes for traditional petroleum-derived fluids.

A major sustainability milestone was the commissioning of ORLEN Południe’s BioPG facility in May 2023, producing renewable propylene glycol from glycerol—a critical ingredient for low-toxicity, environmentally friendly glycol-based HTFs widely used in HVAC systems, heat pumps, and district heating. Germany’s district heating network continued to expand in 2024 with 6.9 MWth of new solar thermal capacity added, increasing the need for efficient, low-viscosity HTFs capable of long-term thermal cycling. Additionally, the German automotive sector is accelerating adoption of advanced e-thermal fluids used in electric vehicle (EV) battery thermal management, where maintaining temperatures between 20°C and 50°C is essential for battery longevity. These developments make Germany a global reference point for sustainable, high-performance, and industrially compliant HTF advancements.

United Kingdom: Nanofluid Breakthroughs and Data Center Cooling with Graphene-Enhanced HTFs

The United Kingdom is rapidly emerging as a leader in advanced nanofluid engineering, particularly in thermal management solutions designed for high-density computing, HPC clusters, and next-generation data center cooling systems. A landmark development occurred in late 2025 when Haydale Graphene Industries PLC launched a graphene-enhanced heat-transfer fluid, introducing a new category of ultra-efficient cooling media. This innovation leverages surface-functionalized graphene particles to dramatically enhance thermal conductivity and improve overall heat dissipation efficiency, setting a transformative precedent for direct-to-chip cooling and liquid immersion technologies in global data centers.

Haydale has also secured a UKIPO Notice of Intention to Grant for its graphene-based HTF technology, strengthening intellectual property protection and enabling focused commercialization. A strategic partnership with Liquitherm Technologies Group further accelerates deployment across industrial and commercial markets, signaling strong adoption potential in IT cooling, electronics manufacturing, and high-load thermal operations. Complementing the nanofluid boom, the UK heat pump market has seen growing demand for specialized glycol-based fluids, highlighted by Fernox Ltd.’s HP EG Heat Transfer Fluid launched in 2022 for ground and air-source systems. Together, the UK’s innovations in graphene nanofluids, heat pump thermal solutions, and data center cooling technologies establish the region as a pioneering force in next-generation HTF formulation.

India: Renewable Energy Expansion and Industrial Heat Transfer Applications Driving Thermal Fluid Demand

India’s Heat Transfer Fluids Market is expanding rapidly, fueled by the country’s aggressive renewable energy targets and accelerating industrial modernization. India’s national energy transition strategy, which emphasizes solar-driven capacity expansion, has significantly boosted demand for high-performance thermic fluids in concentrated solar power (CSP) plants. CSP remains one of the fastest-growing segments in India’s thermal fluid market due to its dependence on stable, high-temperature HTFs for transferring heat from the solar field to the power block, ensuring consistent electricity generation even during variable sunlight conditions.

Beyond renewable energy, India’s oil & gas sector remains a major HTF consumer, relying on thermal fluids for process heating, glycol regeneration, and facility optimization—an industry strengthened by government policies enabling 100% FDI. Meanwhile, India’s expanding pharmaceutical manufacturing ecosystem uses HTFs extensively for reaction temperature control, crystallization, and bulk drug production, requiring thermally stable, contamination-resistant, and high-purity fluids. As India continues advancing toward industrial automation and renewable energy scalability, demand for precise, reliable, and application-specific HTFs is expected to accelerate across both heavy-duty and emerging sectors.

Competitive Landscape in the Global Heat Transfer Fluids Market

The competitive landscape of the heat transfer fluids market is characterized by a mix of diversified chemical majors and specialized thermal fluid providers, all racing to serve high-growth applications such as concentrated solar power (CSP), EVs, data centers, biofuels, and industrial HVAC systems. Leading players like Dow, Eastman, ExxonMobil, Shell, and BASF are expanding portfolios that span synthetic organic fluids, glycol-based coolants, silicone fluids, and advanced dielectric e-fluids, while differentiating through digital services, lifecycle care, and application-specific technical support. Their strategies converge on high thermal stability, long fluid life, corrosion protection, and sustainability, reflecting end-user requirements across energy, chemical processing, automotive, and electronics sectors.

Dow Inc. drives growth with DOWTHERM, DOWFROST, and SYLTHERM heat transfer fluids

Dow commands a strong position in the global heat transfer fluids market with its DOWTHERM™, DOWFROST™, and SYLTHERM™ product families that cover high-temperature synthetic organic fluids, inhibited glycol formulations, and silicone-based fluids for extreme temperatures. The company’s 2024 launch of an enhanced glycol-based fluid, boasting 15% higher thermal stability and improved corrosion resistance, directly addresses industrial demands for longer service intervals and reduced lifecycle costs. Dow strategically targets fast-growing segments such as data center cooling and pharmaceutical processing, promoting non-toxic, high-efficiency glycol solutions like DOWFROST™ LC for direct-to-chip or food-related applications. Flagship products such as DOWTHERM™ A remain benchmarks for CSP applications, offering reliable operation up to 400°C, reinforcing Dow’s reputation for durability in high-temperature heat transfer systems.

Eastman Chemical expands Therminol heat transfer fluid reach with digital TLC services

Eastman’s competitive strength in the heat transfer fluids industry is anchored in its Therminol® portfolio, covering high-temperature liquid-phase fluids like Therminol 66 and mixed-phase solutions like Therminol VP-1, engineered for long service life and stability in demanding industrial environments. The company differentiates through its Total Lifecycle Care (TLC) program, integrating Fluid Genius™ digital monitoring, in-depth fluid analysis, and system design support to help customers maximize uptime and optimize fluid replacement cycles across more than 15,000 systems worldwide. In October 2025, Eastman appointed RelaDyne as an authorized distributor across the U.S., significantly extending Therminol’s distribution footprint and technical support reach. With products that operate across a broad temperature range from around −115°C to 400°C, Eastman is strongly positioned in biofuels, chemical manufacturing, and CSP, where reliability and predictive analytics-driven maintenance are crucial buying factors.

ExxonMobil leverages Mobiltherm heat transfer oils and base oil integration

ExxonMobil participates in the heat transfer oils market through its Mobiltherm™ series, covering mineral oil-based and synthetic fluids optimized for closed-loop, non-pressurized indirect heating systems. A key competitive advantage is its upstream integration and base oil refining expertise, which ensures a secure supply of high-purity base stocks that resist thermal cracking and oxidation, thereby extending fluid life in industrial systems. The company’s strategy aligns heat transfer fluid development with broader chemical processing and energy-efficiency trends outlined in its global outlook, positioning Mobiltherm products as reliable solutions for expanding chemical and process industries. Mobiltherm 600 series fluids are widely used in asphalt processing, rubber manufacturing, and textile mills, where stable moderate-to-high operating temperatures are required without the complexity and cost of fully synthetic formulations.

Shell accelerates EV and immersion cooling with Thermia and EV-Plus e-fluids

Shell has emerged as a key innovator in e-fluids and dielectric heat transfer solutions, complementing its traditional Shell Thermia thermal oils used in industrial heating and process applications. Leveraging its Gas-to-Liquid (GTL) PurePlus technology, Shell formulates high-purity, sulfur-free base oils that underpin its new Shell EV-Plus Thermal Fluid and immersion cooling fluids for data centers and EV powertrains. In September 2025, Shell demonstrated that EV-Plus can support sub-10-minute battery charging from 10% to 80% by effectively managing heat and reducing thermal stress within EV battery packs. By November 2025, it successfully showcased a single-circuit thermal management architecture where EV-Plus cools the battery, motor, and power electronics simultaneously, offering OEMs system simplification and weight reduction. Recent acquisitions of companies such as Panolin and MIDEL/MIVOLT have further broadened Shell’s portfolio into ester-based fluids for transformers, EVs, and data centers, reinforcing its multi-segment leadership in the advanced heat transfer fluids market.

BASF focuses on Hytherm and Antifrogen fluids with advanced corrosion protection

BASF competes in the heat transfer and functional fluids market through products such as Hytherm 500 and its Antifrogen® glycol-based series, targeting industrial process heating, HVAC, refrigeration, and renewable energy systems. Its major differentiator lies in its additive chemistry expertise, enabling proprietary inhibitor packages that deliver superior corrosion and scale protection, thereby prolonging equipment life and maintaining heat transfer efficiency in closed-loop systems. BASF’s heat transfer fluids are extensively integrated into complex chemical and petrochemical processing units, where the company provides technical advisory services and regulatory compliance support across global installations. Antifrogen fluids play a critical role in geothermal heat pumps, solar thermal systems, and industrial refrigeration, where non-toxicity, freeze protection, and long-term stability are crucial decision factors for engineering consultants and plant operators.

Heat Transfer Fluids Market Report Scope

Heat Transfer Fluids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2035)

|

$11.8 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Chemistry (Synthetic Organic Fluids, Glycol-Based Fluids, Mineral Oil-Based Fluids, Silicone Fluids, Molten Salts, Aqueous Heat Transfer Fluids, Advanced Fluids), By Operating Temperature (Low Temperature, Medium Temperature, High Temperature, Ultra-High Temperature), By Application (Industrial Process Heating & Cooling, Concentrated Solar Power, EV Battery Cooling & E-Thermal Management, Heat Recovery Systems, Refrigeration & Freezing), By End-User Industry (Chemical & Petrochemical Processing, Oil & Gas, Renewable Energy, Automotive & Transportation, Food & Beverage Processing, Pharmaceuticals & API Manufacturing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Eastman Chemical, ExxonMobil, Chevron, BASF SE, Shell plc, Huntsman Corporation, LANXESS, Clariant AG, Wacker Chemie, Indian Oil Corporation, Phillips 66, Schultz Canada, Arkema, Dalian Richfortune Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Heat Transfer Fluids Market Segmentation

By Chemistry

- Synthetic Organic Fluids

- Glycol-Based Fluids

- Mineral Oil-Based Fluids

- Silicone Fluids

- Molten Salts

- Aqueous Heat Transfer Fluids

- Advanced Fluids

By Operating Temperature

- Low Temperature (to −50°C)

- Medium Temperature (−10°C to 200°C)

- High Temperature (200°C to 400°C)

- Ultra-High Temperature (400°C+)

By Application

- Industrial Process Heating & Cooling

- Concentrated Solar Power (CSP)

- EV Battery Cooling / E-Thermal Management

- Heat Recovery Systems

- Refrigeration & Freezing

By End-User Industry

- Chemical & Petrochemical Processing

- Oil & Gas

- Renewable Energy

- Automotive & Transportation (EV)

- Food & Beverage Processing

- Pharmaceuticals & API Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Heat Transfer Fluids Market

- Dow Inc.

- Eastman Chemical

- ExxonMobil

- Chevron

- BASF SE

- Shell plc

- Huntsman Corporation

- LANXESS

- Clariant AG

- Wacker Chemie

- Indian Oil Corporation

- Phillips 66

- Schultz Canada

- Arkema

- Dalian Richfortune Chemicals

*- List not Exhaustive

Research Coverage

The High-Performance Heat Transfer Fluids Market research by USDAnalytics delivers a comprehensive, decision-grade assessment of how synthetic organic fluids, glycol-based coolants, silicone oils, molten salts, and advanced dielectric e-fluids are reshaping thermal management in CSP, data centers, EVs, chemical & petrochemical processing, and industrial HVAC. Drawing on multi-year datasets and industry case examples, this report investigates the latest technology breakthroughs in low-GWP formulations, ultra-high temperature molten salt systems, immersion cooling media for AI workloads, and EV battery fast-charging fluids, while examining their impact on capex, opex, and system reliability. It provides rigorous analysis reviews of operating temperature windows, chemistry choices, lifecycle performance, and failure modes, alongside benchmarking of leading product families deployed in process heating, heat recovery systems, and e-thermal management. The study highlights how regulatory shifts, electrification, and renewable integration are steering buyers toward higher stability, longer-life, and more sustainable heat transfer fluids, as well as how vendors are responding through digital fluid monitoring, service models, and application-specific formulations. Designed for strategy, R&D, procurement, and engineering teams, this report is an essential resource for stakeholders seeking to de-risk technology selection, optimize total cost of ownership, and capture growth opportunities in the evolving high-performance heat transfer fluids market.

Scope Highlights

- Segmentation:

By Chemistry – Synthetic Organic Fluids, Glycol-Based Fluids, Mineral Oil-Based Fluids, Silicone Fluids, Molten Salts, Aqueous Heat Transfer Fluids, Advanced Fluids

By Operating Temperature – Low Temperature (to −50°C), Medium Temperature (−10°C to 200°C), High Temperature (200°C to 400°C), Ultra-High Temperature (400°C+)

By Application – Industrial Process Heating & Cooling, Concentrated Solar Power (CSP), EV Battery Cooling / E-Thermal Management, Heat Recovery Systems, Refrigeration & Freezing

By End-User Industry – Chemical & Petrochemical Processing, Oil & Gas, Renewable Energy, Automotive & Transportation (EV), Food & Beverage Processing, Pharmaceuticals & API Manufacturing

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, assessing regional policy frameworks, industrial structures, and adoption patterns for high-performance heat transfer fluids.

- Historic & Forecast Coverage: Quantitative market data and qualitative insights from 2021–2025 as the historical base, with detailed forecasts, scenario analysis, and growth outlooks for the period 2026–2034.

- Companies Covered: Competitive analysis and strategic profiling of 15+ key players, including Dow Inc., Eastman Chemical, ExxonMobil, Chevron, BASF SE, Shell plc, Huntsman Corporation, LANXESS, Clariant AG, Wacker Chemie, Indian Oil Corporation, Phillips 66, Schultz Canada, Arkema, and Dalian Richfortune Chemicals.