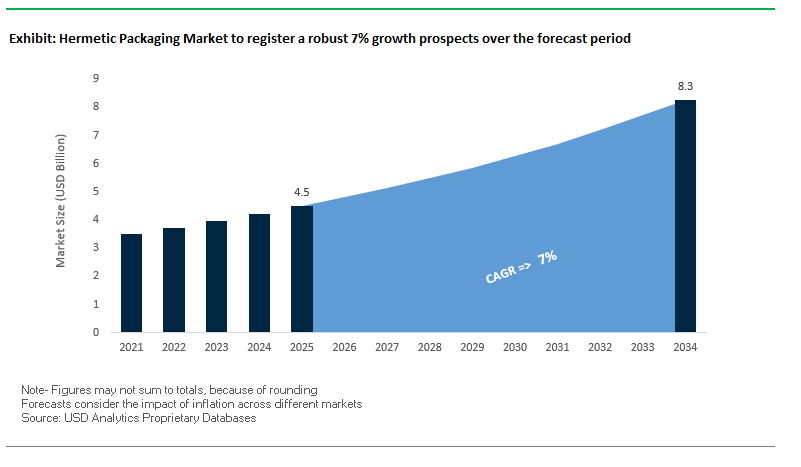

Hermetic Packaging Market Overview: $4.5B in 2025 to $8.3B by 2034 (7.0% CAGR) on High-Reliability Electronics, MEMS & Implantables

The Global Hermetic Packaging Market is valued at USD 4.5 billion (2025) and is projected to reach USD 8.3 billion by 2034, registering a CAGR of 7.0%. Hermetic packaging creating an airtight, gas-tight seal is mission-critical for aerospace, defense, and medical devices, where moisture, ionic contaminants, and corrosive environments can degrade performance. As electronic components shrink and integrate more I/O, demand accelerates for glass-to-metal seals (GTMS), ceramic-to-metal seals, hermetic connectors, high-temperature feedthroughs, and wafer-level hermetic packaging (WLHP) that preserve signal integrity and extend lifecycle reliability.

For buyers and engineering leaders, the commercial case hinges on field reliability and lifetime cost: hermetic enclosures protect MEMS, sensors, RF/optical devices, and implantables, enabling >10-year operation in the human body and survivability in pressure vessels, vacuum, radiation, and extreme temperature profiles.

Key Insights for industry professionals

- Miniaturization & complexity: Higher pin counts and tighter footprints drive ceramic and GTMS adoption for MEMS/sensor packaging.

- Implantables surge: Biocompatible hermetic seals underpin pacemakers, neurostimulators, biosensors, often targeting >10-year device life.

- Aerospace/defense uplift: Rising need for hermetic connectors & feedthroughs to pass signals/power through pressure vessels/harsh media.

- Wafer-level hermeticity: WLHP reduces size, thickness, and weight while improving electrical performance and yield.

- Design-to-reliability economics: Higher upfront package cost offsets RMA, downtime, and mission failure risk in critical applications.

Market Analysis: 2025 Momentum in Ceramics, GTMS Breakthroughs, High-Temp Feedthroughs & 5G/Space

Innovation cadence remains high across materials, processes, and capacity. In August 2025, industry coverage highlighted advanced ceramics in hermetic sensors, enabling more robust, miniaturized packages for IoT and automotive use cases. In July 2025, a leading U.S. hermetic connector maker expanded production to meet military/defense upgrades deploying next-gen electronics.

Two June 2025 milestones underscored reliability gains: a materials science white paper detailed a glass-to-metal sealing advance for vacuum-tight optical components in fiber-optic communications; and a medical technology firm unveiled an implantable biosensor with an innovative long-duration hermetic system, meaningfully reducing replacement frequency.

Supply-side productization continued through May–April 2025. In May 2025, a European specialist launched high-temperature feedthroughs for downhole drilling and industrial automation, engineered for extreme duty cycles. In April 2025, a global advanced-packaging provider injected major R&D into high-frequency hermetic packages for 5G and satellite communications, aligning with the RF front-end’s tighter loss budgets.

Sector priorities are broadening. March 2025 conference reporting emphasized sustainability in hermetic packaging eco-friendlier materials and cleaner processes without trading off reliability. Earlier, in January 2025, the merger of a thermal-management leader with a hermetic packaging firm created a deeper portfolio for aerospace/defense, integrating heat dissipation and airtight protection under one roof shortening design cycles and qualification timelines.

Emerging Innovations and Strategic Opportunities Driving the Hermetic Packaging Market

Transition to Glass-Based Hermetic Sealing for High-Frequency and Photonic Devices

The hermetic packaging market is experiencing a strategic pivot from traditional ceramic and metal packages to glass-based sealing technologies, including glass frit and laser glass sealing. This shift is driven by the need for superior signal integrity at millimeter-wave (mmWave) frequencies, particularly for 5G/6G infrastructure, and enhanced optical transmission for photonic devices such as lidar and telecom modules. Glass-based seals offer controlled dielectric constants, minimizing signal loss and interference, while laser sealing provides low-thermal-stress bonds that protect temperature-sensitive components. These advancements enable high-precision alignment and hermetic protection of photonic integrated circuits (PICs), ensuring optimal performance in cutting-edge telecom and data communication systems.

Adoption of Miniaturized and Wafer-Level Hermetic Packaging for Medical Implants

The drive for minimally invasive medical devices is propelling hermetic packaging towards wafer-level and ultra-miniaturized formats. This enables direct sealing of MEMS sensors and ASICs for implantable devices like neurostimulators and continuous glucose monitors, reducing size, enhancing reliability, and lowering production costs through batch processing. Wafer-level hermetic packaging allows thousands of chips to be sealed simultaneously, improving efficiency, while maintaining biocompatibility and long-term protection against bodily fluids. This miniaturization trend addresses the growing demand for discreet, reliable medical implants and fosters innovation in patient-centric device design.

Development of Thin-Film Getter Solutions for Ultra-Long-Life Implants and Space Electronics

A significant opportunity exists in integrating advanced thin-film non-evaporable getters (NEGs) within hermetic packages to maintain pristine internal environments for decades. Thin-film getters actively absorb residual gases like water vapor and oxygen, preserving ultra-high vacuum or inert atmospheres essential for long-life medical implants and space-grade electronics. These solutions enable devices to operate reliably for 10-15 years or more in the body, or survive decades in harsh space environments, addressing critical performance and longevity requirements in high-value markets.

Hermetic Packaging for Scalable Quantum Computing Systems

The commercialization of quantum computing creates a rapidly growing demand for hermetic packages that protect delicate qubits superconducting, spin, or trapped-ion from decoherence while supporting high-density, low-loss electrical interconnects. Advanced hermetic solutions must operate at cryogenic temperatures, maintain superfluid helium-tight environments, and allow reliable multichip integration. Innovations in cryogenic interconnects and high-density feedthroughs are critical for scaling quantum processors, ensuring signal integrity, and enabling robust quantum computing platforms. Companies are leveraging expertise from space and semiconductor sectors to meet these highly specialized packaging needs.

Competitive Landscape: Specialists in GTMS, Advanced Ceramics & Wafer-Level Hermeticity

The market is dominated by highly specialized players with deep materials science, clean manufacturing, and application-specific engineering. Differentiation centers on glass-to-metal sealing, ceramic multilayer packages, wafer-level hermeticity, high-temperature feedthroughs, and defense/medical quality systems.

SCHOTT AG GTMS leadership for extreme environments

SCHOTT leverages global expertise in specialty glass and glass-ceramics to deliver custom hermetic solutions spanning medical implants, deep-sea connectors, and safety-critical automotive systems. Its portfolio includes hermetic sensor packages, microelectronic housings, feedthroughs, and optical windows/lens caps. A notable innovation is HEATAN® high-temperature sensor feedthroughs rated to ~1000 °C+, supporting ultra-harsh duty cycles. Strategically, SCHOTT focuses on long-life reliability where component failure is unacceptable, anchoring programs in glass-to-metal sealing and rigorous qualification.

Kyocera Corporation Ceramic packages with integrated electrical performance

Kyocera provides multilayer ceramic packages (e.g., CDIP, CQFP) that pair thermal stability with excellent dielectric properties for high-reliability semiconductors. Offerings span sensor, RF, and mixed-signal devices that require hermeticity and thermal management. Integration strengths include wafer-level vacuum sealing and getter utilization for MEMS improving out-gassing control and stability. Strategy centers on robust, moisture-shielding ceramic packages for downhole, space, and medical applications with stringent qualification regimes.

Teledyne Technologies (Teledyne Microelectronics) Wafer-level hermetic packaging for defense & medical

Teledyne Microelectronics delivers hermetic packaging and assembly for aerospace/defense and medical markets, covering diverse materials and sealing methods. It has pioneered wafer-level packaging (WLP) for MEMS, integrating fabrication and hermetic sealing to achieve smaller, more reliable, and cost-effective components. Capabilities include high-vacuum furnace sealing, resistance seam sealing, laser welding, and precision wire bonding, ensuring mission-grade reliability. The focus is tailored, custom hermetic solutions aligned to defense/medical quality and documentation.

Santier, Inc. (An Egide Company) Hermetic housings plus engineered thermal management

Santier designs and manufactures hermetic microelectronic housings/assemblies with an emphasis on thermal management materials. Its portfolio spans metallic and ceramic packages for aerospace, defense, and medical programs, complemented by powder metallurgy, 5-axis machining, and integrated value-add services. Recent quality milestones Nadcap® Chemical Processing and AS9100:D underscore aerospace-grade process control. Strategy: custom, under-one-roof solutions that meet exacting specs for heat, vibration, and environmental stress.

Amkor Technology, Inc. OSAT scale for hermetic MEMS, sensors & SiP integration

Amkor is among the largest outsourced semiconductor assembly and test (OSAT) providers, with a wide portfolio spanning MEMS, optical sensors, SiP, and TSV platforms. It supports hermetic protection where required, integrating multiple dies and functions in compact footprints while preserving moisture/ion ingress resistance. Amkor’s value lies in high-volume, high-yield manufacturing plus DFx collaboration, enabling cost-effective, reliable packaging for miniaturized, high-function electronics across industrial, automotive, medical, and communications end markets.

Hermetic Packaging Market Share Insights

Ceramic-to-Metal Sealing Leads Market Share by Type in the Hermetic Packaging Industry

Ceramic-to-metal sealing accounts for approximately 40% of the hermetic packaging market, establishing itself as the high-performance leader for extreme-condition applications. Its superior thermal stability, mechanical strength, and airtightness make it the preferred choice for aerospace avionics, defense systems, high-power semiconductors, and laser diodes. These applications demand packages that withstand temperature cycling, vibration, and high pressure without performance degradation. Glass-to-metal sealing follows closely with 35% share, serving as the cost-effective workhorse across medical implants, automotive electronics, and volume-driven sensor applications. Transponder glass, reed glass, and passivation glass occupy niche but critical roles protecting RFID tags, relay switches, and semiconductor surfaces respectively. This segmentation highlights the trade-off between cost efficiency and performance reliability, with ceramic-to-metal sealing securing leadership due to its unmatched ability to safeguard mission-critical components under the harshest operating conditions.

Electronics Hold the Largest Market Share by End-Use Industry in the Hermetic Packaging Market

Electronics represent the largest end-use segment with around 35% market share, positioning them as the volume and innovation driver of hermetic packaging. The surge in IoT devices, MEMS sensors, and optoelectronics such as LEDs and laser modules has amplified demand for hermetic protection against moisture and atmospheric contaminants. These components require long-term reliability to function in critical applications ranging from consumer electronics to defense systems. Aerospace and defense, with about 25% share, remain the extreme-environment specialist sector, where hermetic packaging ensures operational integrity of satellites, radar systems, and avionics. Medical devices form another high-value pillar, particularly for life-critical implants like pacemakers and neurostimulators, where glass-to-metal sealing ensures biocompatibility and decades-long stability. Automotive applications are rapidly expanding due to electrification and sensorization, while telecommunications packaging secures the infrastructure backbone for high-speed data transfer. Collectively, the end-use segmentation underscores how hermetic packaging adapts across industries with varying reliability, cost, and regulatory requirements.

United States: Aerospace, Medical, and Defense Sectors Fuel High-Reliability Hermetic Packaging

The U.S. hermetic packaging market is strongly influenced by evolving regulations from the FDA and Department of Defense (DoD), emphasizing safety, durability, and performance for critical applications in healthcare, aerospace, and defense sectors. Technological advancements are driving miniaturization and integration, with innovations such as fan-out wafer-level packaging (FOWLP) and system-in-package (SiP) enabling multiple chips to be housed in a single, hermetic enclosure.

Corporate initiatives are fueling growth, with companies like MacDermid Alpha Electronics Solutions launching hydrogen and moisture getter products for medical, telecom, and aerospace applications. Strategic acquisitions, such as Qnnect’s purchase of Hermetic Solutions Group in 2022, and investments in R&D, including the acquisition of RHP DiaCool IP for advanced thermal management, highlight the industry’s focus on innovation. Key applications span aerospace avionics, sensors, missile components, and medical implantable devices, with increasing demand driven by the need for patient safety, product reliability, and long-term operability.

China: Government Policies and Miniaturization Trends Drive Hermetic Packaging Demand

China’s hermetic packaging market is propelled by governmental initiatives under the “Made in China 2025” plan, which promotes high-tech manufacturing and aims to increase domestic content of core materials to 70% by 2025. Technological advancements, including AI and automation integrated with “5G plus industrial internet,” are enhancing production efficiency and flexible manufacturing capacity.

Regulatory reforms are also shaping the market, with government directives to curb over-packaging and establish a whole-chain administration system by 2025. The rapid industrialization of electronics, telecommunications, and automotive industries is driving the demand for smaller, more efficient hermetic packages. Market consolidation is occurring as stricter environmental policies lead to the closure of less-efficient manufacturers, leaving larger producers with greater market share and stronger capabilities to meet the growing demand for advanced hermetic packaging solutions.

Germany: Sustainable Manufacturing and Smart Packaging Innovations Lead the Market

Germany’s hermetic packaging industry is guided by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which sets stringent requirements for recyclability and recycled content. German companies are leveraging technological innovations such as SCHOTT AG’s advanced glass-to-metal sealing and multilayer ceramic packaging for medical implants and RF devices.

Smart packaging innovations, including embedded sensors for humidity and temperature monitoring, are gaining traction to reduce waste and enhance sustainability. The medical device sector is a significant end-user, demanding high-reliability hermetic solutions for implantable devices. Additionally, the automotive and aerospace sectors contribute to market growth, supported by corporate initiatives like GEA Heating & Refrigeration Technologies’ expansion of semi-hermetic product portfolios and launch of new screw compressor models.

Japan: Precision Manufacturing and Aging Population Drive Hermetic Packaging Advancements

Japan’s hermetic packaging market benefits from advanced precision manufacturing and cutting-edge technologies tailored for aerospace, defense, and telecommunications applications. Regulatory policies, such as the new “positive list” for synthetic materials effective June 2025, ensure that packaging and imported products meet stringent safety standards.

Research and development are central to the market, with companies focusing on improving performance for consumer electronics, including laptops, smartphones, and wearable devices. Key applications include reliable medical devices for Japan’s aging population, along with automotive and defense industries requiring packaging capable of withstanding extreme conditions. Corporate players such as Kyocera Corporation lead the market with ceramic-to-metal sealing solutions, providing durable hermetic packaging across high-tech sectors.

South Korea: Military Investments and Semiconductor Leadership Boost Hermetic Packaging Growth

South Korea’s hermetic packaging market is driven by substantial government investments in defense, with a projected $268.8 billion expenditure over five years. Domestic players like Hanwha and LIG Nex1 are expected to benefit, creating strong demand for hermetic solutions in military and defense applications.

The country’s semiconductor industry, particularly in memory chips where it holds a 57% global share, is a key consumer of hermetic packaging for chip protection. Technological innovation focuses on highly efficient and reliable ceramic-to-metal sealing solutions. Beyond defense and semiconductors, the aerospace, automotive, and telecommunications sectors, including the development of 5G infrastructure, are significant drivers, increasing the need for hermetic packaging to safeguard sensitive electronic components and maintain high operational reliability.

Hermetic Packaging Market Report Scope

Hermetic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.5 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Configuration (Multilayer Ceramic Packages, Pressed Ceramic Packages, Metal Can Packages), By Type (Ceramic to Metal Sealing, Glass to Metal Sealing, Transponder Glass, Reed Glass, Passivation Glass), By Application (Aeronautics & Space, Military & Defense, Automotive, Healthcare, Telecom, Industrial, Others), By End-Use Industry (Electronics, Medical Devices, Telecommunications, Aerospace & Defense, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SCHOTT AG, Amkor Technology Inc., Kyocera Corporation, Materion Corporation, AMETEK Inc., Teledyne Technologies Inc., Egide S.A., Micross Components Inc., Niterra Co., Ltd., Texas Instruments Incorporated, Hermetic Solutions Group, TDK Corporation, Corfin Industries, Suron, SGA Technology

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hermetic Packaging Market Segmentation

By Configuration

- Multilayer Ceramic Packages

- Pressed Ceramic Packages

- Metal Can Packages

By Type

- Ceramic to Metal Sealing

- Glass to Metal Sealing

- Transponder Glass

- Reed Glass

- Passivation Glass

By Application

- Aeronautics & Space

- Military & Defense

- Automotive

- Healthcare

- Telecom

- Industrial

- Others

By End-Use Industry

- Electronics

- Medical Devices

- Telecommunications

- Aerospace & Defense

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Hermetic Packaging Market

- SCHOTT AG

- Amkor Technology Inc.

- Kyocera Corporation

- Materion Corporation

- AMETEK Inc.

- Teledyne Technologies Inc.

- Egide S.A.

- Micross Components Inc.

- Niterra Co., Ltd.

- Texas Instruments Incorporated

- Hermetic Solutions Group

- TDK Corporation

- Corfin Industries

- Suron

- SGA Technology

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-layered methodology to deliver comprehensive insights into the global Hermetic Packaging Market. Our approach integrates primary research, including interviews with industry executives, engineers, and key stakeholders, alongside secondary research from company reports, trade journals, government publications, and scientific papers to ensure accuracy and depth. Market sizing and forecast calculations are derived using a combination of bottom-up and top-down approaches, with careful adjustments for emerging trends, regulatory frameworks, and technological innovations such as wafer-level hermetic packaging, glass-to-metal seals, and thin-film getter integration. USDAnalytics further analyzes product segmentation, end-use adoption, and regional dynamics, including high-growth markets in the U.S., China, Germany, Japan, and South Korea, ensuring actionable insights for industry professionals. Competitive benchmarking evaluates capabilities, portfolios, and strategic initiatives of leading players such as SCHOTT AG, Kyocera Corporation, Teledyne Technologies, and Amkor Technology, providing a holistic view of market evolution, growth drivers, and opportunities in aerospace, defense, medical, and electronics sectors. The methodology emphasizes reliability, scalability, and long-term performance trends, delivering a robust foundation for strategic decision-making and investment planning in the hermetic packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.