Heterogeneous Catalyst Market to Reach $45.7 Billion by 2034 at 6.1% CAGR Fueled by Hydrogen, e-Methanol, and Advanced Refining Technologies

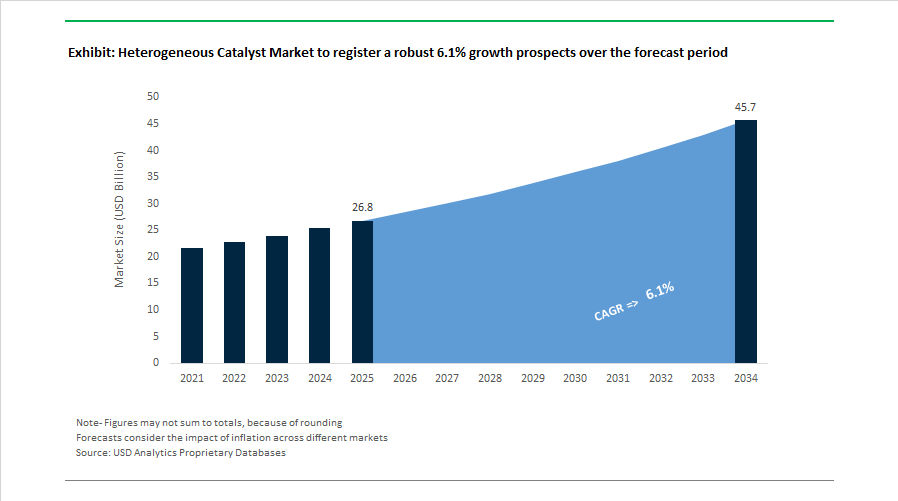

The Heterogeneous Catalyst Market is projected to grow from $26.8 billion in 2025 to $45.7 billion by 2034, registering a CAGR of 6.1%. Expansion is driven by accelerating investments in green hydrogen production, blue ammonia and methanol synthesis, refinery hydroprocessing upgrades, and electrified petrochemical routes. Demand for fixed-bed, fluid catalytic cracking, hydrogenation, oxidation, and reforming catalysts is intensifying as industrial operators pursue carbon intensity reduction, process efficiency gains, and compliance with tightening REACH and global environmental standards.

In January 2024, BASF Process Catalysts partnered with Envision Energy to accelerate green hydrogen and CO2 conversion into e-methanol, targeting decarbonization of shipping fuels and chemical feedstocks. In August 2024, W. R. Grace & Co. introduced its Grace-IDP™ iron deactivation protocol for fluid catalytic cracking, enabling refiners to process heavier crudes without rapid catalyst poisoning. In November 2024, BASF announced investment in an industrial-scale X3D® additive manufacturing plant for 3D-printed catalysts, scheduled for 2026 operations. The technology delivers open-structure catalyst geometries that reduce reactor pressure drop and increase throughput in green transformation projects. In December 2024, BASF inaugurated its Catalyst Development and Solids Processing Center in Ludwigshafen, a high double-digit million-euro hub bridging laboratory discovery and industrial-scale heterogeneous catalyst synthesis.

Strategic consolidation reshaped the competitive landscape in 2025. In May 2025, Honeywell announced a £1.8 billion agreement to acquire Johnson Matthey Catalyst Technologies, integrating blue hydrogen, methanol, and ammonia catalyst capabilities into Honeywell UOP. The transaction, expected to close in early 2026, creates a vertically integrated platform for net-zero process technologies. In 2025, Grace completed acquisition of the remaining stake in Advanced Refining Technologies, strengthening hydroprocessing catalyst capabilities for heavier feedstocks. In October 2025, Evonik Industries launched the Noblyst® F precious metal catalyst line for continuous-flow pharmaceutical manufacturing, reflecting the shift from batch to modular production systems. In November 2025, Clariant received a major industry award for its chromium-free HySat™ platform, eliminating hexavalent chromium in hydrogenation processes to meet strict European chemical safety regulations.

Technology diversification accelerated into 2026. In October 2025 at K 2025, Clariant introduced AddWorks™ titanium-based polyester catalysts, providing a heavy-metal-free alternative to antimony systems amid supply uncertainty following China’s 2024 export restrictions. In 2025, Clariant and Linde validated EDHOX™ Technology, using the OxyMax™ E heterogeneous catalyst to convert ethane directly into polymer-grade ethylene with 60% lower CO2 emissions compared to conventional steam cracking. On January 1, 2026, Evonik operationalized SYNEQT to streamline chemical park infrastructure supporting specialty catalyst production.

The Heterogeneous Catalyst Market is increasingly defined by hydrogen economy integration, additive-manufactured catalyst geometries, refinery feedstock flexibility, electrified ethane conversion, and precious metal catalyst optimization for continuous processing. Competitive differentiation hinges on emission-reduction performance, heavy-metal elimination, digitalized pilot-scale development, and large-scale consolidation aimed at building integrated net-zero catalyst portfolios for refining, petrochemical, pharmaceutical, and renewable fuel value chains.

Heterogeneous Catalyst Market Trends and Opportunities

Industrial-Scale Catalyst Regeneration and PGM Reclamation Becomes a Cost-Critical Strategy

Volatility in platinum, palladium, and rhodium pricing during 2024 and 2025 has fundamentally changed procurement strategies across petrochemicals, refining, and specialty chemicals. End users are moving away from linear catalyst replacement models toward circular catalyst lifecycle management, where regeneration and Precious Group Metal recovery are treated as strategic levers for margin protection and supply security. Industrial regeneration services are now capable of restoring up to 85–90% of baseline catalytic activity at 30–50% of the cost of new catalyst procurement, making regeneration economically indispensable for hydroprocessing and reforming units.

A defining inflection point occurred in May 2025 when Honeywell International announced a USD 2.4 billion acquisition of Johnson Matthey Catalyst Technologies. This transaction created a vertically integrated platform spanning catalyst process licensing, formulation, deployment, and closed-loop PGM reclamation. The combined entity has publicly aligned around a target of achieving 75% recycled PGM content in new catalyst systems by 2030, directly insulating customers from raw material shocks.

Parallel investments are reinforcing this circular shift. BASF established BASF Automotive Catalysts and Recycling as a standalone entity in late 2024, allocating capital from its €4.5 billion battery materials and recycling program to optimize heterogeneous catalyst refining. Using ISO 17025-accredited assaying, BASF is improving metal recovery yields while shortening settlement cycles for refinery and automotive customers. On the technology front, 2025 industrial pilots confirmed that ozone-based oxidation at approximately 125°C can remove carbon fouling that previously required 500°C thermal treatments. This reduces energy consumption by nearly 60% and shortens turnaround times by about 30%, translating directly into lower operating expenditure for refineries.

Accelerated R&D Cycles for Polymer Upcycling and Circular Chemistry

Heterogeneous catalysts are now central to the chemical industry’s response to plastic waste mandates, as polymer upcycling transitions from experimental research to first-of-a-kind commercial deployment. Unlike mechanical recycling, catalytic routes can tolerate mixed, contaminated plastic streams, making them viable for real-world municipal and industrial waste. R&D priorities have shifted decisively toward base-metal and earth-abundant catalysts that deliver high selectivity without relying on costly noble metals.

In August 2024, researchers at University of California Berkeley demonstrated a catalytic vaporization system using tungsten oxide on silica combined with sodium on alumina. This heterogeneous catalyst pair achieved close to 90% monomer recovery from mixed polyethylene and polypropylene, offering a solid-state alternative to homogeneous catalytic systems with significantly lower separation costs. Commercial momentum accelerated further in December 2025 when the BOTTLE Consortium announced that its oxidative recycling platform had reached commercial readiness. Using air and low-cost heterogeneous catalysts, the system converts multi-layer packaging waste into high-value chemical intermediates and was recognized as a 2025 R&D100 Award finalist.

To compress development timelines, catalyst producers are increasingly deploying artificial intelligence and machine learning. By 2025, digital screening platforms were capable of evaluating over one million virtual catalyst structures, enabling rapid optimization of activity, selectivity, and lifetime. These AI-driven workflows have been credited with improving the internal rate of return of hybrid recycling plants by 25–30% by optimizing catalyst replacement and regeneration cycles.

Electrocatalysts for Gigawatt-Scale Green Hydrogen Production

The rapid scale-up of green hydrogen infrastructure is creating one of the largest new demand pools for heterogeneous catalysts. Proton Exchange Membrane and Solid Oxide Electrolyzer technologies require ultra-low loading PGM catalysts or advanced non-PGM alternatives that balance activity, durability, and cost. As electrolyzer capacity moves from megawatt pilots to gigawatt-scale deployment, catalyst availability and performance are becoming strategic bottlenecks.

In February 2025, Johnson Matthey and Bosch formalized a long-term collaboration to mass-produce catalyst-coated membranes. By combining PGM chemistry expertise with automotive-scale manufacturing discipline, the partnership aims to materially reduce electrolyzer stack costs and accelerate hydrogen adoption. Government-backed localization efforts are reinforcing this trend. Chile committed USD 25.6 million through Corfo in June 2025 to establish domestic electrolyzer manufacturing, while India’s National Green Hydrogen Mission with an outlay of ₹19,744 crore is incentivizing indigenous catalyst production to reduce import dependence.

Performance benchmarks continue to improve. Solid Oxide Electrolyzer systems entering the market in late 2025 are achieving efficiencies above 80% by leveraging high-temperature heterogeneous catalysts that enable effective waste heat recovery. These efficiency gains are narrowing the cost gap between green hydrogen and grey or blue hydrogen, which currently ranges from USD 1.9 to USD 2.4 per kilogram, positioning catalysts as a decisive factor in hydrogen cost parity.

Modular and Decentralized Power-to-X Systems for Energy Security

Energy security concerns and renewable intermittency are driving demand for modular, decentralized Power-to-X systems that convert electricity, biogas, or captured carbon dioxide into synthetic fuels at the source. These systems rely on compact, highly selective heterogeneous catalysts that can operate reliably under fluctuating loads.

A landmark demonstration occurred in July 2025 when the H2Mare initiative launched the world’s first floating offshore e-fuel platform in Germany. The system integrates modular Fischer-Tropsch reactors and Direct Air Capture to convert offshore wind energy and seawater into synthetic fuels without grid dependency. In parallel, INERATEC secured €70 million in financing during 2025 to scale its modular reactor technology. Its Frankfurt facility is designed to produce 2,500 tons of e-fuels annually, using highly selective heterogeneous catalysts to synthesize sustainable aviation fuel from biogenic carbon dioxide and green hydrogen.

As aviation, maritime, and defense sectors accelerate decarbonization timelines, modular catalytic systems are emerging as a critical enabler. Their ability to deliver drop-in fuels with existing infrastructure compatibility positions heterogeneous catalysts at the core of the global Power-to-X economy through 2035.

Heterogeneous Catalyst Market Share and Segmentation Insights

Metal-Based Catalysts Lead the Heterogeneous Catalyst Market in Industrial Catalytic Processes

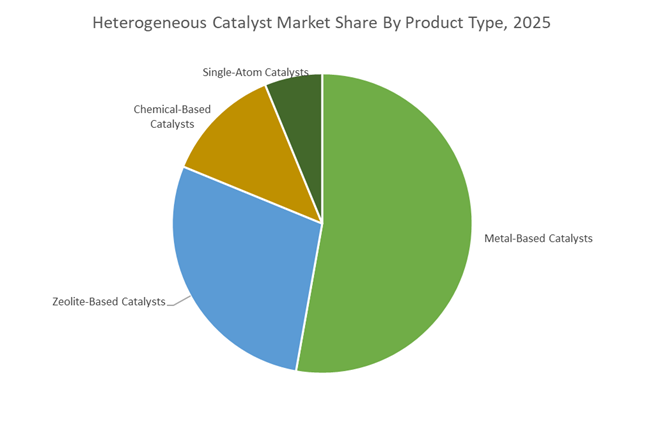

Metal-Based Catalysts accounted for 52.80% of the Heterogeneous Catalyst Market share in 2025, making them the dominant product category across global catalytic technologies. These catalysts typically contain precious metals such as platinum, palladium, and rhodium, along with base metals including nickel, cobalt, and copper, which provide high catalytic activity and selectivity across a wide range of chemical reactions. Metal-based heterogeneous catalysts play a critical role in petroleum refining processes such as hydrocracking, hydrotreating, and catalytic reforming, as well as in major chemical synthesis operations including ammonia production, methanol synthesis, and hydrogenation reactions. Their robust performance and recyclability make them essential for large-scale industrial catalytic systems. In 2025, catalyst manufacturers are increasingly focusing on precious metal optimization strategies to address volatility in platinum group metal supply and pricing. Advanced catalyst designs now incorporate improved metal dispersion techniques, alloying of precious metals with base metals, and nanoscale catalyst structures, enabling manufacturers to achieve comparable catalytic efficiency with lower metal loadings, reducing overall catalyst cost while maintaining reaction performance.

Oil and Gas Industry Drives the Largest Demand for Heterogeneous Catalysts

Oil and Gas represented 44.80% of the Heterogeneous Catalyst Market share in 2025, establishing it as the largest end-use industry for heterogeneous catalytic materials. The refining sector relies heavily on heterogeneous catalysts for conversion, upgrading, and purification processes involved in producing transportation fuels and petrochemical feedstocks. Catalysts are extensively used in fluid catalytic cracking (FCC), hydrodesulfurization, hydrocracking, reforming, and catalytic hydrogenation, enabling refineries to convert crude oil into high-value products such as gasoline, diesel, jet fuel, and petrochemical intermediates. Global demand for transportation fuels and petrochemical raw materials continues to drive catalyst consumption within refinery operations. In 2025, the refining sector is undergoing structural transformation through increased integration between refineries and petrochemical production facilities. As demand growth shifts from transportation fuels toward petrochemical feedstocks such as ethylene, propylene, and aromatics, refiners are investing in catalytic technologies that allow flexible production between fuels and chemicals. This transition is increasing demand for advanced FCC catalysts capable of maximizing light olefin production while maintaining gasoline yield, supporting refinery adaptation to evolving global energy and chemical markets.

Competitive Landscape in Heterogeneous Catalyst Market

BASF SE Pioneers 3D-Printed Catalysts for Decarbonized Chemical Processing

BASF SE maintains its position as the global volume leader in heterogeneous catalysts, leveraging its integrated Verbund model to drive process efficiency and scale. In Q1 2026, BASF commissioned its first commercial-scale 3D-printed catalyst facility in Ludwigshafen using proprietary X3D technology. The platform enables complex open structures that reduce reactor pressure drop, enhance mass transfer, and increase active surface area. The company is prioritizing next-generation catalysts that reduce energy intensity in ammonia synthesis, methanol production, and CO2-to-methanol conversion. BASF is also scaling custom catalyst manufacturing services, offering additive manufacturing capabilities to third-party producers seeking 2030 net-zero compliance. Its portfolio spans metal-based, zeolite, and specialty catalysts tailored for sustainable aviation fuel and hydrogen-related processes.

Honeywell UOP Expands Through Strategic Catalyst Technologies Acquisition

Honeywell UOP is reinforcing its leadership as a global process technology licensor by finalizing the acquisition of Johnson Matthey’s Catalyst Technologies business for £1.325 billion, expected to close by August 2026. This transaction significantly expands Honeywell’s installed base in syngas, ammonia, hydrogen, and methanol catalysts, complementing its dominant position in fluid catalytic cracking and hydroprocessing. The company is integrating its Performance+ digital services platform with catalyst offerings, utilizing AI-driven digital twins for real-time performance optimization and predictive maintenance. In late 2025, Honeywell introduced next-generation sustainable aviation fuel catalysts designed to maximize yields from fats, oils, and greases. The combined portfolio positions Honeywell as a central player in refinery modernization, low-carbon fuels, and hydrogen value chains.

Clariant AG Advances Chromium-Free and Antimony-Free Catalyst Technologies

Clariant AG has repositioned itself as a sustainability-focused specialty catalyst provider with emphasis on decarbonization and electrification. In early 2026, Clariant commercially launched AddWorks titanium-based catalysts for polyester production, providing an antimony-free alternative amid global export restrictions on antimony. The company received Best Catalyst Technology recognition in 2025 for its HySat chromium-free hydrogenation platform, eliminating hexavalent chromium risks in industrial hydrogenation. Through its EDHOX technology, co-developed with Linde, Clariant enables ethane-to-ethylene conversion at reduced temperatures, lowering CO2 emissions by up to 60% compared to conventional steam cracking. Operating through Catalysts and Adsorbents business units with over 10,000 employees globally, Clariant is strengthening its position in sustainable petrochemical transformation.

Evonik Industries Focuses on Continuous Flow and Circular Plastics Catalysis

Evonik Industries AG is targeting high-margin precision catalysis segments, moving away from bulk commodity markets. In 2025 and 2026, Evonik introduced the Noblyst F catalyst series optimized for continuous flow chemistry, addressing the pharmaceutical industry’s shift from batch to continuous manufacturing. The inauguration of a world-scale alkoxides plant on Jurong Island, Singapore, reinforces Evonik’s Asia-Pacific catalyst supply capabilities. The company is scaling its Purocel catalyst series to upgrade pyrolysis oil derived from recycled plastics into feedstock suitable for premium polymer production, supporting circular economy objectives. Evonik’s portfolio includes activated metal catalysts and engineered metal foams that enhance heat transfer efficiency compared to conventional catalyst pellets.

ExxonMobil Product Solutions Integrates Catalysts into Hydrogen and CCS Strategies

ExxonMobil Product Solutions operates as both a major catalyst consumer and technology licensor across refining and petrochemical complexes. In 2026, the company advanced a joint development agreement with BASF focused on methane pyrolysis technology that produces hydrogen and solid carbon without direct CO2 emissions. Its proprietary Galoryl and zeolite-based catalysts are widely deployed in xylene isomerization and toluene disproportionation units globally. ExxonMobil is expanding investments in carbon capture and storage infrastructure where heterogeneous catalysts and adsorbents enable industrial CO2 separation at scale. In late 2025, the company reported record performance from next-generation FCC catalysts that shift refinery output toward high-value petrochemical feedstocks rather than gasoline, reinforcing margin resilience amid energy transition pressures.

China: State-Led Localization, Emissions Compliance, and AI-Accelerated Discovery

China is executing one of the most comprehensive industrial transformations in the heterogeneous catalyst industry, combining state subsidies, emissions regulation, and digital chemistry. Under alignment with the 15th Five-Year Plan, the Ministry of Industry and Information Technology prioritized high-end catalyst localization across refining, chemicals, and energy transition value chains. In late 2025, chemical clusters in Shandong received a USD 4.2 billion subsidy package to replace imported noble-metal catalysts with domestically engineered single-atom heterogeneous catalysts. This initiative directly targets cost reduction, supply security, and performance parity in refining and petrochemical applications.

Refining efficiency remains a central focus. Sinopec Catalyst Company operationalized a new FCC catalyst production line in late 2025, designed to process heavier crude slates with higher conversion efficiency while lowering carbon intensity per barrel by an estimated 9%. Emissions regulation is reinforcing catalyst upgrades. The nationwide enforcement of GB 18352.6-2025 China 6b standards has driven a documented 15% increase in palladium loading in automotive catalytic converters, reflecting tighter tailpipe emission thresholds. Hydrogen and green chemistry are emerging as parallel demand drivers. By early 2026, China deployed more than 2,000 hydrogen refueling stations under the National Hydrogen Energy Development Plan, sharply increasing demand for platinum-group-metal heterogeneous catalysts used in on-site electrolysis systems. Innovation velocity is also accelerating through AI. In 2025, Chinese catalyst producers began deploying DeepSeek lean model architectures to simulate reaction environments, reducing trial-and-error phases in catalyst discovery by 35%. This innovation pipeline extends into fertilizers, with a state-backed green ammonia pilot in Inner Mongolia testing ruthenium-based heterogeneous catalysts for low-pressure synthesis, supporting long-term decarbonization of domestic nitrogen value chains.

India: Refining Modernization, Standards Enforcement, and Bio-Based Catalysis

India’s heterogeneous catalyst industry is expanding in tandem with refinery upgrades, petrochemical investments, and tightening quality controls. In 2025, the Indian government and state-run enterprises such as Indian Oil Corporation and Bharat Petroleum committed nearly USD 45 billion to new petrochemical and refinery projects. These investments include dedicated polyolefin units utilizing advanced Ziegler-Natta heterogeneous catalysts to improve polymer performance and yield consistency. Anticipating long-term fuel demand growth, the Ministry of Petroleum and Natural Gas fast-tracked modernization of five major refineries in 2025, prioritizing hydrocracking and desulfurization catalyst upgrades.

Regulatory discipline is tightening the market. Effective January 2026, the Bureau of Indian Standards mandated quality certification for all industrial catalysts used in public sector refineries, directly targeting sub-standard imports and accelerating adoption of validated heterogeneous catalyst systems. Strategic foreign investment is reinforcing domestic capability. In January 2025, Mitsubishi Chemical Group announced an expansion in India focused on heterogeneous catalysts for semiconductor materials and electric vehicle supply chains. India’s bioeconomy agenda is also influencing catalyst design. Under the BioE3 policy, three new facilities were funded in 2025 to develop bio-based heterogeneous catalysts supporting castor-derived chemicals such as heptanoic acid and sebacic acid, aligning catalyst innovation with renewable feedstock utilization.

United States: Feedstock Optimization, Sustainable Fuels, and Catalyst Reformulation

The United States heterogeneous catalyst market is being shaped by shale-derived feedstock advantages, sustainable fuel incentives, and evolving environmental guidance. Over the 24 months ending December 2025, U.S. Gulf Coast refiners invested more than USD 1.2 billion in advanced catalytic technologies to optimize ethane-to-ethylene conversion. These investments reflect the strategic importance of silica-alumina and zeolite-based heterogeneous catalysts in maximizing olefin yields from shale-based feedstocks.

Policy support is accelerating energy transition applications. The Inflation Reduction Act introduced expanded tax credits in 2025 for Sustainable Aviation Fuel, triggering construction of four new Midwest biorefineries that rely on heterogeneous deoxygenation catalysts for biomass-to-fuel conversion. Regulatory pressure is also reshaping catalyst materials. Updated 2026 guidance from the U.S. Environmental Protection Agency restricted certain fluorinated catalyst supports due to PFAS concerns, accelerating reformulation toward non-fluorinated zeolitic systems in specialty chemical production. Innovation in refining catalysts remains strong. W.R. Grace & Co. introduced the PARAGON catalyst series in late 2024, engineered to maximize propylene yield in FCC units. The first large-scale North American refinery implementation was completed in Q2 2025, reinforcing the United States’ leadership in performance-driven catalyst deployment.

Germany: Decarbonized Catalyst Manufacturing and Closed-Loop Precious Metals

Germany’s heterogeneous catalyst industry is advancing through decarbonization, emissions control, and precious metal recovery. In late 2025, leading producers including BASF and Evonik converted approximately 30% of their catalyst production energy consumption to green hydrogen, meeting interim targets under the EU Fit for 55 framework. This transition materially lowers the carbon footprint of catalyst manufacturing while strengthening compliance with EU sustainability benchmarks.

Strategic partnerships and recycling infrastructure further differentiate Germany. In January 2024, BASF partnered with Envision Energy to develop heterogeneous catalysts for green e-methanol synthesis, with the first German pilot plant reaching full capacity in late 2025. Supply chain resilience is supported by advanced recycling. Heraeus Holding inaugurated a modernized facility in 2025 capable of recovering 98% of platinum from spent industrial catalysts, stabilizing exposure to volatile PGM pricing. Regulatory enforcement remains a strong catalyst for adoption. Amendments to the EU Industrial Emissions Directive in 2025 mandated Best Available Techniques, compelling German plants to deploy high-selectivity catalysts that reduce NOx and SOx emissions by an additional 20%.

France: Sustainable Fuels and Low-Impact Synthesis Breakthroughs

France’s heterogeneous catalyst industry is increasingly defined by sustainable fuel technologies and public-sector research leadership. In 2025, Axens reported a record order backlog for its Vegan technology catalysts used in hydrotreated vegetable oil production. These catalysts are being supplied to three major European Sustainable Aviation Fuel projects scheduled for commissioning in 2026, positioning France as a key technology exporter in renewable fuels.

Public research institutions are driving next-generation catalyst innovation. IFP Energies Nouvelles announced a cobalt-free heterogeneous catalyst for Fischer-Tropsch synthesis in late 2025. This breakthrough significantly reduces the environmental footprint and supply risk associated with synthetic fuel production, while maintaining high selectivity and operational stability. France’s combined industrial and research momentum underscores its strategic role in lowering the carbon intensity of heterogeneous catalysis across energy and chemical applications.

Summary Table: Country-Level Strategic Signals in the Heterogeneous Catalyst Industry

Heterogeneous Catalyst Market County Level Snapshot

|

Geography

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Impact

|

|

China

|

State subsidies, emissions enforcement

|

FCC, hydrogen, green ammonia

|

Localization and AI-driven acceleration

|

|

India

|

Refinery upgrades, BIS certification

|

Petrochemicals, bio-based chemicals

|

Quality control and capacity expansion

|

|

United States

|

Shale feedstocks, SAF incentives

|

Olefins, renewable fuels

|

Feedstock optimization and reformulation

|

|

Germany

|

EU decarbonization, recycling

|

Green methanol, emissions control

|

Low-carbon and closed-loop systems

|

|

France

|

SAF demand, public R&D

|

HVO, synthetic fuels

|

Sustainable fuel catalyst leadership

|

Heterogeneous Catalyst Market Report Scope

Heterogeneous Catalyst Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$26.8 Billion

|

|

Market Size (2034)

|

$45.7 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Product Type (Metal-Based Catalysts, Zeolite-Based Catalysts, Chemical-Based Catalysts, Single-Atom Catalysts), By Support Material (Alumina, Silica, Activated Carbon, Titania and Zirconia), By Application (Petroleum Refining, Chemical Synthesis, Environmental Catalysis, Polymerization, Hydrogenation), By End-Use Industry (Oil and Gas, Chemicals and Petrochemicals, Automotive and Transportation, Environmental and Water Treatment, Pharmaceuticals and Food Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Johnson Matthey Plc, Clariant AG, W. R. Grace & Co., Evonik Industries AG, Albemarle Corporation, Honeywell UOP, Topsoe, Sinopec Catalyst Company, Axens, ExxonMobil Chemical, LyondellBasell Industries N.V., Umicore, Shell plc, Heraeus Holding GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Heterogeneous Catalyst Market Segmentation

By Product Type

- Metal-Based Catalysts

- Precious Metal Catalysts

- Transition Metal Catalysts

- Zeolite-Based Catalysts

- Chemical-Based Catalysts

- Single-Atom Catalysts

By Support Material

- Alumina

- Silica

- Activated Carbon

- Titania and Zirconia

By Application

- Petroleum Refining

- Chemical Synthesis

- Environmental Catalysis

- Polymerization

- Hydrogenation

By End-Use Industry

- Oil and Gas

- Chemicals and Petrochemicals

- Automotive and Transportation

- Environmental and Water Treatment

- Pharmaceuticals and Food Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Heterogeneous Catalyst Industry

- BASF SE

- Johnson Matthey Plc

- Clariant AG

- W. R. Grace & Co.

- Evonik Industries AG

- Albemarle Corporation

- Honeywell UOP

- Topsoe

- Sinopec Catalyst Company

- Axens

- ExxonMobil Chemical

- LyondellBasell Industries N.V.

- Umicore

- Shell plc

- Heraeus Holding GmbH

*- List not Exhaustive