Market Overview: High-Purity Base Metals Underpinning Semiconductor, EV Battery & Aerospace Manufacturing

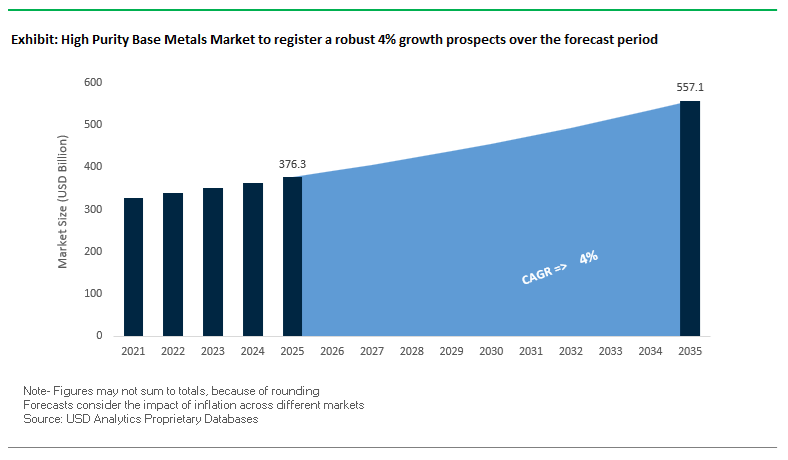

The High Purity Base Metals Market is projected to rise from USD 376.3 billion in 2025 to USD 557 billion by 2035, expanding at a stable CAGR of 4%. This growth is driven by the accelerating demand for Ultra-High Purity Copper (UHP-Cu), 4N–6N aluminum, 4N nickel, and high-purity silicon across semiconductor fabrication, EV batteries, aerospace coatings, and high-performance superalloys. Manufacturers and refiners are rapidly scaling purification technologies—electro-refining, vacuum distillation and zone refining—to meet ultra-tight purity tolerances demanded by advanced electronics, corrosion-resistant aerospace structures and next-gen propulsion systems.

In semiconductor processing alone, UHP Copper (6N purity) is a non-negotiable requirement due to its pivotal role in preventing atomic-scale defects that can trigger yield losses exceeding 75% at advanced manufacturing nodes. Meanwhile, the shift toward lightweight, cadmium-free corrosion protection in aerospace is accelerating the adoption of 4N aluminum coatings that operate reliably up to 400°C without composition drift during thermal cycling. The EV battery sector continues to push copper foil thickness down to 6–8 μm, a threshold only achievable using ultra-pure copper to maintain mechanical stability while supporting higher battery energy density. In high-temperature superalloy manufacturing, 4N-purity nickel remains indispensable for ensuring structural stability above 1,000°C, especially in turbine blades and industrial gas generators.

Key Insights for Manufacturers & Refiners

- 6N UHP Copper purity has become mandatory for chip fabrication to eliminate contamination-driven yield losses.

- EV battery producers demand 6–8 μm copper foils, requiring refineries to tighten purity control and grain-size uniformity.

- 4N Aluminum coatings replacing cadmium/zinc-nickel systems support high-temperature aerospace corrosion protection up to 400°C.

- High-purity nickel (>99.99%) remains essential for superalloys used in turbine engines operating beyond 1,000°C.

- Global base metal purity standards are becoming stricter, driven by electronics, electrification and renewable energy infrastructure.

Market Analysis: Production Expansions, Recycling Infrastructure & Purity Mandates Redefining Supply Chains

The High Purity Base Metals Market is undergoing significant transformation, shaped by expanding mining output, new purity regulations, and rising downstream electrification requirements. In December 2025, Glencore announced plans to ramp up its global copper production to 1.6 million tonnes by 2035, supported by long-term mine expansions meant to meet surging demand from EV charging infrastructure, grid modernization and semiconductor manufacturing. Similarly, February 2025 saw BHP report a record 2 million tonnes of copper output, positioning the company as a primary supplier of high-purity copper feedstocks during a decade of unprecedented electrification-led consumption.

Recycling and secondary sourcing gained prominence in August 2025, when Argus Media launched its Black Mass Payable Assessment for China, signaling a formal financial structure for high-purity nickel and copper recovery from end-of-life lithium-ion batteries. This was reinforced in October 2025, when Metalor Technologies acquired Gannon & Scott, strengthening its footprint in sustainable e-waste refining and boosting global capability to supply high-purity metals via circular processing routes. The solar energy expansion also influenced market dynamics in September 2025, when Argus introduced new Polysilicon price assessments, reflecting strong growth in photovoltaics—one of the largest consumers of high-purity metallurgical silicon.

Regulatory changes continue elevating minimum purity requirements across industries. The GCC Standardization Organization, in June 2025, mandated a minimum purity of 99.99% (4N) for high-purity base metals used in electronics and critical industrial systems, driving refiners worldwide to enhance processing precision. Meanwhile, research advances accelerated purity coating technologies: In March 2025, new findings highlighted the adoption of aluminum electroplating to produce >99.99% purity aluminum layers for lightweight, corrosion-resistant barriers, particularly valuable in aerospace and defense. Earlier, in April 2024, industry reports introduced increased supply of OFHC Copper, vital for high-frequency, low-loss electronics used in advanced communication and radar systems.

Breakthrough Trends and Emerging Opportunities in Ultra-High-Purity Metals for Next-Generation Electronics and Energy Systems

Market Trend 1: Rapid Expansion of 6N+ Copper Production to Support Sub-5 nm Semiconductor Interconnect Scaling

The high purity base metals market is experiencing a critical technological shift driven by semiconductor manufacturers mandating 6N+ (99.9999%) copper cathodes for next-generation logic devices. As interconnect dimensions shrink to 3 nm and below, impurities—including Fe, Ni, Ag—must be kept below 100 ppb, while radioactive contaminants such as U and Th must be controlled at <10 ppt to eliminate soft error risks in advanced logic and memory devices.

Electromigration reliability becomes exponentially more sensitive at these nodes. High-purity copper consistently demonstrates 2–5× longer Time-to-Failure (TTF) than 5N copper due to significantly reduced impurity segregation at grain boundaries. Achieving the benchmark electrical resistivity of 1.678×10⁻⁸ Ω·m at 20°C is only possible when impurity concentrations approach theoretical limits, making 6N copper the preferred interconnect material for extreme scaling.

To deliver this purity cost-effectively, refiners are deploying next-generation electrorefining systems capable of achieving ≥99.999% impurity removal efficiency for aggressive contaminants like Fe and Ni in a single pass. As chipmakers transition to backside power delivery, ruthlessly low-resistivity copper becomes mission-critical, securing long-term demand for ultra-pure cathode feedstock.

Market Trend 2: Mandatory Use of 5N Aluminum for High-Voltage EV Busbars and Ultra-Thin Battery Collector Foils

Automotive electrification is accelerating the adoption of 5N (99.999%) aluminum, particularly for 800V+ architectures that require ultra-low resistivity conductors. The shift is driven by the sensitivity of electrical resistivity to Fe and Si impurities. At 5N purity, aluminum achieves a 1.2–2.0% reduction in resistivity compared to conventional 3N5 grades—an improvement that significantly reduces heat generation in high-current busbars and extends thermal stability across the entire pack.

Battery manufacturers are now specifying impurity limits of <10 ppm total Fe+Si, especially for 10–15 μm anode current collector foils, where hard inclusions can cause rolling-induced defects. High-purity aluminum slashes pinhole density to <100 defects per m², improving yield and greatly reducing internal short circuit risk in high-energy-density cells.

Additionally, the reduced resistivity of 5N Al helps mitigate localized temperature rise (hotspots) in fast-charging EVs, directly influencing cycle life and SEI stability. This aligns with OEM safety priorities and regulatory tightening around battery thermal propagation prevention.

Market Opportunity 1: Commercialization of 7N Zone-Refined Tin for Quantum Computing, Cryogenic Electronics, and Ultra-Pure Solder Alloys

The emergence of quantum computing and cryogenic electronics is driving a premium opportunity for 7N (99.99999%) tin, produced exclusively through zone refining. Achieving 7N grade demands 30–40 refining passes to push total metallic impurities below 100 ppb, with critical contaminants regulated at 10 ppt to maintain superconducting consistency.

High-purity tin exhibits a sharp superconducting transition at Tc = 3.722 K, with a transition width <1 mK, a performance requirement for qubit stability and cryogenic circuitry where even trace impurities can destabilize Josephson junction behavior.

In high-performance computing and semiconductor packaging, 7N tin also demonstrates superior metallurgical behavior. Ultra-pure solder alloys exhibit up to 50% reduction in BGA void formation compared to 4N solders due to minimized intermetallic compound (IMC) formation, improving joint integrity under thermal cycling. As chiplet architectures become mainstream, demand for void-free, electromigration-resistant solder materials is rising sharply, positioning 7N tin as a strategic materials frontier.

Market Opportunity 2: Establishment of Closed-Loop 4N+ Nickel Recycling Streams for Lithium-Ion Battery Cathode Precursor Manufacturing

The global transition to EV battery gigafactories has created a critical opportunity to produce 4N (99.99%) high-purity nickel from spent NMC cathodes via closed-loop recycling. Modern hydrometallurgical processes recover nickel with ≥98.5% efficiency, while solvent extraction systems achieve separation factors of ≥1000 for Ni/Mn, enabling downstream purification of trace metals (Co, Mn, Fe, Cu, Zn) to <10 ppm total.

These impurity thresholds are essential because Fe and Cu contamination—even >10 ppm—can destabilize the layered crystal structure of regenerated cathode active material, impairing lithium diffusion and causing irreversible capacity fade.

Producing battery-grade nickel sulfate directly from recycled feedstock closes the loop on raw material supply and significantly reduces carbon intensity compared to mining and refining. As OEMs shift toward sustainable cathode chemistries, the ability to deliver 4N+ recycled nickel becomes a competitive differentiator for precursor manufacturers and battery recyclers alike.

High Purity Base Metals Market Share Analysis

Market Share by Metal Type: High Purity Copper Leads Due to Its Dominance in High-Conductivity and Electrification Applications

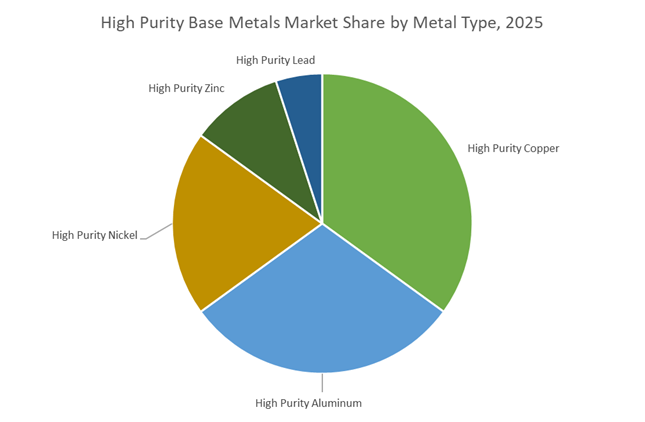

High Purity Copper holds the largest share of the global high purity base metals market—approximately 35% in 2025—because it is the foundational material for high-accuracy electrical and thermal systems that power the modern electronics and electrification ecosystem. With purity levels reaching 4N–6N (99.99%–99.9999%), even trace impurities significantly alter performance, making ultra-high-purity copper indispensable for semiconductor fabrication, high-frequency electronics, precision wiring, and advanced power systems. Its unmatched electrical conductivity—regularly surpassing 100% IACS in oxygen-free grades—positions it as the default choice for microchip interconnects, RF components, 5G infrastructure hardware, and next-generation power delivery architectures. Additionally, its exceptional thermal conductivity (~400 W/m°C) enables advanced heat dissipation in power modules, EV traction motors, and high-density server systems. The metal’s market share is reinforced by surging demand from megatrends such as EV adoption, renewable electrification, grid modernization, and semiconductor scaling—all of which rely disproportionately on high-purity copper compared to other advanced metals. Because EVs require 3–4× more copper than ICE vehicles, and data centers demand increasingly conductive materials to minimize energy loss, high-purity copper serves as the backbone of the global transition toward electrification and high-frequency digital technologies, securing its position as the dominant material in this market.

Market Share by End-Use: Electrical & Electronics Sector Dominates Due to Semiconductor Scaling and High-Purity Conductivity Requirements

The Electrical & Electronics sector accounts for the largest share of the high-purity base metals market—approximately 40% in 2025—because ultra-high-purity materials, especially copper, are indispensable for semiconductor manufacturing, circuit architecture, and advanced electronic device performance. Semiconductor fabrication alone drives massive demand for 5N–6N purity copper, used in sputtering targets, wafer metallization, interconnect layers, redistribution lines, micro-bumping, and heat spreaders. As chip architectures evolve toward smaller nodes, higher transistor density, and higher current density, high impurity tolerance becomes unacceptable, making high-purity copper an irreplaceable input material. The explosive global growth of 5G, IoT, cloud computing, AI servers, and edge devices further amplifies consumption, as these applications require ultra-low-resistance pathways for high-frequency signal transmission and stable power distribution. Beyond semiconductors, high-purity base metals are critical to PCBs, high-frequency connectors, EMI shielding materials, and precision electrical components—each representing high-value, high-purity-intensive applications. The sector’s dominant revenue share is further enabled by strong secular trends in electronics miniaturization, high-performance computing, and EV power electronics, all of which require increasingly pure copper, aluminum, and nickel to improve conductivity, reduce heat, and ensure long-term reliability. As a result, the Electrical & Electronics sector remains the central growth engine of the global high-purity base metals market.

Country Analysis: Strategic High Purity Base Metals Capabilities Reshaping Global Supply Chains

China: Global Refining Dominance and Accelerated High-Purity Aluminum & Battery Metal Capacity

China remains the most influential force in the High Purity Base Metals Market, driven by unmatched refining capacity, aggressive investment in ultra-high-purity metals, and its decisive control of battery-grade value chains. With an estimated 80% control of global battery metal refining, China dictates global access to high-purity nickel, cobalt intermediates, and precursor chemicals essential for next-generation cathode chemistries. The country’s dominance extends to solid-state batteries, where over 80% of global capacity by 2025 is expected to be located in China, requiring ultra-high-purity nickel, copper, and aluminum foil to meet purity thresholds for dendrite-resistant electrolyte interfaces.

China’s expansion is reinforced by significant investments in ultra-high-purity aluminum and zinc, announced throughout 2024–2025, catering to aerospace structural components, consumer electronics, and semiconductor packaging. Parallel to these advances, China is developing a powerful circular HPBM ecosystem, with new recycling facilities capable of producing 98–99% purity copper from complex scrap streams—reducing environmental footprint and reinforcing material security. The country’s immense EV ecosystem and massive renewable energy grid infrastructure create sustained demand for oxygen-free high-conductivity copper busbars, aluminum conductors, and advanced alloy materials, cementing China’s role as the undisputed global refining and high-purity metal processing hub.

United States: National HPBM Reshoring, Critical Mineral Security, and High-Purity Copper/Nickel Infrastructure

The United States is rapidly reshaping its high-purity metals landscape through legislated industrial policy, seeking to eliminate vulnerabilities in critical mineral refining and HPBM supply chains. The CHIPS and Science Act and the Inflation Reduction Act (IRA) provide billions in subsidies, tax credits, and procurement guarantees to stimulate domestic refineries for high-purity copper, nickel, and cobalt—materials crucial for semiconductor fabs, EV batteries, and electricity transmission networks. Despite producing over 1,000 kt/year of mined copper, the U.S. remains heavily dependent on imported refined copper, outlining a strategic bottleneck that new electro-refineries and solvent extraction facilities aim to solve.

U.S. companies are entering partnerships to produce battery-grade nickel sulfate and cobalt sulfate, creating an integrated domestic ecosystem for EV cathode manufacturers. Major diversification moves include Rio Tinto’s $2.5 billion Rincon lithium project and the acquisition of Arcadium Lithium, which strengthens U.S.-aligned battery precursor security and indirectly reduces pressure on HPBM imports. As semiconductor expansion accelerates under CHIPS mandates, the U.S. is prioritizing ultra-clean, low-oxygen copper and high-purity aluminum needed for chip interconnects, power modules, and advanced packaging—solidifying the country’s transition from raw metal producer to a high-end HPBM manufacturing base.

Canada: High-Purity Nickel Leadership, Hydrometallurgical Innovation, and Low-Carbon HPBM Production

Canada is emerging as a global leader in Class 1 battery-grade nickel (99.8%+), supplying high-energy-density cathode producers seeking stable, ESG-compliant mineral sources. With a global reputation for metallurgical excellence, Canadian producers are transitioning to transformative Hydrogen Plasma Reduction technologies to replace carbon-intensive smelting processes. These hydrogen-based systems produce nickel with far lower carbon emissions, aligning the country with global net-zero mining initiatives and making Canadian high-purity nickel a preferred feedstock for premium EV battery manufacturers.

Canada is also pushing the frontier in AI-driven hydrometallurgical optimization, particularly in Quebec, where digital process modeling has demonstrated 5–8% improvements in nickel and copper recovery rates. These advancements increase the economic viability of HPBM operations and create more consistent purity outputs for downstream partners. Beyond production efficiency, Canada is pioneering tailings carbonation, using mine waste to sequester hundreds of thousands of tonnes of CO₂ annually—positioning the country at the intersection of low-carbon metallurgy and future-ready battery material supply.

India: Strategic Copper Refining Expansion and High-Purity Metal Security Under NCMM

India is rapidly transitioning from an HPBM import-dependent nation to an emerging refining powerhouse. The inclusion of copper in the Critical Minerals List (2023) and its prioritization under the National Critical Minerals Mission (NCMM) underscores the strategic importance of domestic copper availability for power grids, EV charging, and electronics manufacturing. India’s most transformative development is the Adani Group’s massive copper refinery in Mundra, which launched with a 500,000-tonne annual capacity targeting an expansion to 1 million tonnes by 2029, making it one of the largest integrated copper facilities in Asia.

To strengthen mineral exploration, the government introduced a new Exploration Licence (2023) enabling greater private-sector participation in deep-seated copper, nickel, and cobalt deposits. Meanwhile, policy-driven circular economy initiatives—including the proposed recycled copper content mandate rising from 5% (FY28) to 20% (FY31)—are boosting the secondary HPBM industry and driving innovation in high-purity scrap processing. India’s international strategy complements domestic buildout: securing Zambian greenfield exploration rights ensures long-term copper availability for its growing electrification and grid modernization programs.

Japan & South Korea: Ultra-High Purity Zinc, Indium, and Specialty HPBM for Semiconductors and Advanced Electronics

Japan and South Korea anchor the global supply of Ultra-High Purity (UHP) base metals used in semiconductor fabrication, optoelectronics, battery materials, and high-frequency communication systems. Japan leads global production of UHP Zinc, with Nippon Light Metal’s 2025 expansion adding 10,000 tpa of ultrapure zinc for advanced coatings, chip-level components, and high-end galvanic applications. Parallel to this, Sumitomo Metal Mining is doubling nickel and cobalt refining by 2028 to support the explosive growth in NMC and solid-state EV batteries.

South Korea, home to world-leading semiconductor and display manufacturers, excels in ultra-clean HPBM processing through companies like Korea Zinc Co. Ltd., recognized for producing some of the world’s highest purity zinc and lead grades. Both countries supply ultra-high purity indium (5N–7N) and antimony, critical feedstocks for III-V compound semiconductors (InSb, GaSb) used in infrared imaging, quantum sensors, and high-speed logic devices. This positions Japan and South Korea as indispensable nodes in the HPBM supply chain for global semiconductor expansion, AI-driven electronics, and precision optical systems.

Russia: Integrated Mining Base and Strategic High-Purity Nickel & Copper Supplier

Russia remains a major supplier of high-purity nickel and copper, leveraging vertically integrated mining, smelting, and refining capabilities. Companies such as Norilsk Nickel maintain some of the world’s largest reserves of sulfide nickel ores, allowing Russia to produce high-purity nickel suitable for aerospace alloys, EV batteries, and specialty stainless steels. Despite geopolitical constraints, Russia continues to supply key HPBM grades to Asian and Middle Eastern markets, maintaining relevance in global specialty metals trade.

Competitive Landscape: Global Leaders Strengthening High-Purity Metal Production, Refining & Circular Supply Chains

The competitive landscape of the High Purity Base Metals Market is defined by vertically integrated miners, advanced refiners, and specialty manufacturers developing ultra-high-purity feedstocks for semiconductors, EV batteries, aerospace and renewable energy systems. Companies differentiate through electro-refining capability, recycling infrastructures, purity control technologies, and carbon-efficient production pathways.

Glencore – Expanding Copper Supply to Meet Global Electrification Demand

Glencore operates one of the world’s most diversified portfolios of copper, nickel, zinc, cobalt and ferroalloys, integrating mining, refining, trading and recycling. Its strategic objective to increase copper production to 1.6 million tonnes by 2035 reflects its commitment to supporting the massive rise in demand from the EV, renewable energy and semiconductor sectors. The company’s vertically integrated model allows tight control over purity grades, feedstock reliability and cost structures, positioning Glencore as a dominant supplier of high-purity metals within global electrification value chains.

Codelco – World Leader in High-Purity Copper Cathodes

Codelco, holding the world’s largest copper reserves, remains the primary global supplier of high-grade electrolytic copper cathodes essential for producing UHP-Cu (6N) used in semiconductor and high-frequency electronics. The company is investing heavily in sustaining mine output despite aging ore grades, with long-term structural projects aimed at preserving global copper purity supply. Its dominance in primary copper production ensures unmatched reliability for manufacturers requiring ultra-clean copper feedstocks.

Hindalco Industries – Integrated Aluminum & Copper Producer Supporting EV and Electronics Growth

Hindalco is a global leader in aluminum sheet, plate and extrusions, as well as a major supplier of high-purity copper products required for India’s expanding electronics manufacturing and EV ecosystems. It has increased high-purity copper production capacity by 15–20%, driven by demand for ultra-thin copper foils and high-conductivity materials. Hindalco’s fully integrated value chain—from bauxite mining to downstream fabrication—enables stringent purity control for aerospace, automotive lightweighting and power electronics applications.

Aurubis AG – Europe’s Leading Copper Recycler and High-Purity Metal Refiner

Aurubis is at the forefront of copper refining and specialty recycling, transforming complex concentrates and scrap into high-purity copper and precious metals. Its strong emphasis on the Circular Economy reduces environmental impact while ensuring stable long-term supply of high-purity materials to European manufacturers. Aurubis' refining capabilities support industries requiring ultra-clean copper for EV batteries, semiconductors and high-efficiency power transmission systems.

Norsk Hydro – Low-Carbon, High-Purity Aluminum for Critical Electrical Applications

Norsk Hydro leverages hydropower-driven production to supply low-carbon aluminum, a key differentiator for OEMs prioritizing Scope 3 emission reduction. The company supplies high-purity aluminum grades tailored for electrical conductors, EV infrastructure and semiconductor applications. With growing demand for sustainable metal sourcing, Hydro’s integrated operations and high-purity portfolio position it as a preferred supplier for lightweight, energy-efficient product design.

Teck Resources – High-Purity Zinc & Expanding Copper Portfolio in North America

Teck Resources is one of the world’s largest producers of refined zinc, essential for high-performance galvanizing and corrosion-resistant alloys requiring high-purity feedstocks. The company is also advancing major copper expansion projects across the Americas, ensuring strong regional supply for renewable energy systems, electronics and EV component manufacturing. Its integrated refining capabilities support stable and scalable production of high-purity base metals across industrial applications.

High Purity Base Metals Market Report Scope

High Purity Base Metals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$376.3 Billion

|

|

Market Size (2035)

|

$557 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Metal Type (High Purity Copper, High Purity Nickel, High Purity Aluminum, High Purity Zinc, High Purity Lead), By Purity Grade (4N Grade, 5N Grade, 6N Grade, Ultra-High Purity), By End-Use Application (Electrical & Electronics, Transportation, Power Generation & Energy Storage, Industrial Machinery & Additive Manufacturing, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BHP, Rio Tinto, Codelco, Glencore, Nornickel, Hindalco, Korea Zinc, Dowa Holdings, Sumitomo Metal Mining, Hindustan Zinc, Norsk Hydro, CHALCO, Boliden, KGHM Polska Miedź, Umicore

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Purity Base Metals Market Segmentation

By Metal Type

- High Purity Copper

- High Purity Nickel

- High Purity Aluminum

- High Purity Zinc

- High Purity Lead

By Purity Grade

- 4N Grade (≥99.99%)

- 5N Grade (≥99.999%)

- 6N Grade (≥99.9999%)

- Ultra-High Purity (≥7N)

By End-Use Industry

- Electrical & Electronics

- Transportation

- Power Generation & Energy Storage

- Industrial Machinery & Additive Manufacturing

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High Purity Base Metals Market

- BHP

- Rio Tinto

- Codelco

- Glencore

- Nornickel

- Hindalco

- Korea Zinc

- Dowa Holdings

- Sumitomo Metal Mining

- Hindustan Zinc

- Norsk Hydro

- CHALCO

- Boliden

- KGHM Polska Miedź

- Umicore.

*- List not Exhaustive

Research Coverage: High Purity Base Metals Market

This USDAnalytics report investigates how ultra-high-purity copper, nickel, aluminum, zinc and related base metals are becoming strategic enablers for semiconductor scaling, EV battery platforms, aerospace propulsion and advanced power electronics. It delivers rigorous analysis reviews of mining, refining and recycling value chains, tracks breakthroughs in electro-refining, vacuum and zone-refining routes, and highlights how tightening 4N–7N purity specifications are reshaping procurement strategies across electrical & electronics, transportation, power generation and industrial machinery users. The study examines the impact of solid-state batteries, sub-5 nm interconnects, ultra-thin collector foils and low-carbon metallurgy on high-purity base metal demand, maps emerging circular flows from black mass and e-waste recovery, and evaluates regional policy pushes around critical mineral security. With detailed benchmarking of purity grades, application-critical contamination thresholds and end-use adoption patterns, this report is an essential resource for strategy teams, procurement leaders, refinery operators and technology managers seeking to de-risk supply, optimize material choice and capture growth in the High Purity Base Metals Market worldwide.

Scope Highlights

- Segmentation:

- By Metal Type: High Purity Copper, High Purity Nickel, High Purity Aluminum, High Purity Zinc, High Purity Lead

- By Purity Grade: 4N Grade (≥99.99%), 5N Grade (≥99.999%), 6N Grade (≥99.9999%), Ultra-High Purity (≥7N)

- By End-Use Industry: Electrical & Electronics, Transportation, Power Generation & Energy Storage, Industrial Machinery & Additive Manufacturing, Aerospace & Defense

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, capturing policy, investment and technology shifts in each core region.

- Timeframe: Includes historic data from 2021–2025 and robust forecasts from 2026–2034, enabling long-term planning across semiconductor, EV, grid and industrial use cases.

- Companies: In-depth analysis/profiles of 15+ companies, covering strategies and capabilities of major miners, refiners and recyclers such as BHP, Rio Tinto, Codelco, Glencore, Nornickel, Hindalco, Korea Zinc, Sumitomo Metal Mining, Norsk Hydro, CHALCO, Boliden, KGHM Polska Miedź, Umicore and others.