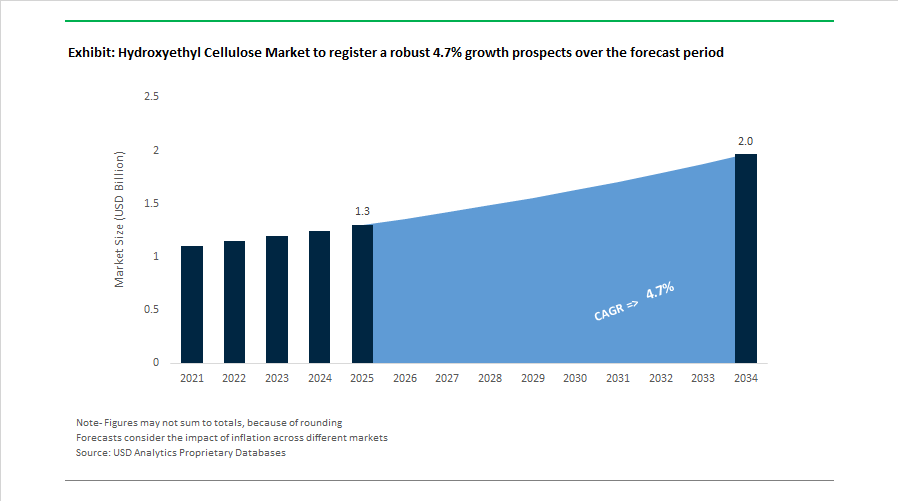

Hydroxyethyl Cellulose Market to Reach $2 Billion by 2034 at 4.7% CAGR Driven by Specialty Additives, Pharma-Grade Cellulose Ethers, and Portfolio Realignment

The Hydroxyethyl Cellulose (HEC) Market is projected to expand from $1.3 billion in 2025 to $2 billion by 2034, registering a CAGR of 4.7%. Market growth is being shaped by rising demand for cellulose ether thickeners in water-based paints, construction materials, personal care formulations, oilfield fluids, and pharmaceutical excipients. Increasing focus on sustainable specialty polymers, portfolio optimization among global producers, and investment in high-purity grades for life sciences are redefining the competitive landscape for hydroxyethyl cellulose manufacturers worldwide.

In July 2024, Shin-Etsu Chemical implemented a global silicone price revision of 10% or more, reflecting broader inflationary pressures in energy, logistics, and feedstock markets that also influenced pricing strategies across cellulose ether producers. In August 2024, Lotte Fine Chemical, in partnership with Japan’s JERA, concluded a joint collaboration agreement to advance low-carbon fuel value chains, strengthening its broader green chemical strategy that supports decarbonized energy inputs for cellulose ether production. In October 2024, Nippon Paper Industries launched its SPOPS liquid packaging system in South Korea, signaling its strategic pivot toward biomass-derived daily-life products and reinforcing its expertise in wood-based cellulose technologies. Throughout 2024 and extending into 2026, Nippon Paper Group implemented a major production reorganization under its Medium-Term Business Plan 2025, reallocating resources from graphic paper toward its Daily-Life Products Business, including cellulose ether manufacturing, targeting a more profitable portfolio by fiscal 2026.

Strategic transformation accelerated in 2025. In May 2025, Nouryon released its sustainability report, highlighting that nearly 35% of 2024 revenue originated from its Eco-Premium Solutions portfolio and confirming that 74% of its R&D pipeline is focused on sustainable innovations, including next-generation cellulose ethers. In 2025, Nouryon also recognized key supply partners such as Asahi Kasei Corp. and Olin Corporation to reinforce global supply stability for specialty cellulose polymers. In October 2025, Ashland expanded its pharmaceutical excipient portfolio by adding high-purity sucrose and parenteral applications for injectables, complementing its high-purity HEC grades used as stabilizers in liquid and solid dosage forms. During the same month, Ashland received a $103 million tax refund related to its Nutraceuticals divestiture, strengthening its balance sheet to support its transition into a focused specialty additives company. By late 2025, Ashland confirmed completion of portfolio optimization initiatives, including divestitures of CMC and methylcellulose businesses, sharpening its strategic focus on high-margin hydroxyethyl cellulose for life sciences and specialty coatings.

In February 2026, Ashland Inc. reported first-quarter fiscal 2026 sales of $386 million and narrowed its full-year Adjusted EBITDA outlook to $400–$420 million due to temporary startup delays at its Calvert City plant and weather-related disruptions. Despite operational headwinds, the company highlighted strong margins supported by its emphasis on high-value specialty additives such as HEC. In the same month, Lotte Chemical announced its 2026 strategy to reduce dependence on commodity petrochemicals and accelerate expansion in high-performance materials and eco-friendly energy solutions, reinforcing upstream strength for specialty cellulose ether markets. Additionally, Shin-Etsu Chemical progressed toward completion of its new 2.1 billion yen plant in Zhejiang Province, China, scheduled for February 2026, expanding regional infrastructure to support high-functional emulsions and specialty additives that align with growing demand for advanced hydroxyethyl cellulose formulations in Asia-Pacific.

Hydroxyethyl Cellulose (HEC) Market Trends and Opportunities

Regulatory Reformulation Driving Zero-VOC Architectural Coatings Adoption

Regulatory tightening across North America has transformed low-VOC and zero-VOC paints from a sustainability preference into a compliance-driven requirement, placing Hydroxyethyl Cellulose at the center of modern architectural coatings formulations. Following the U.S. EPA final rule effective January 17, 2025, national VOC emission standards for architectural and aerosol coatings have been aligned more closely with California-style reactivity limits. As a result, waterborne acrylic systems accounted for an estimated 45.7% of total U.S. paint sales by late 2025, materially expanding the addressable market for HEC as a primary rheology modifier.

Leading coatings manufacturers such as Sherwin-Williams and PPG Industries have accelerated the integration of advanced HEC-based rheology packages to overcome historic performance trade-offs associated with low-VOC formulations. Industry case studies from 2024 and 2025 show that optimized HEC systems reduce sagging, spatter, and roller marks, lowering consumer complaints related to uneven finishes by as much as 30% and directly reducing product returns.

Indoor air quality considerations are further reinforcing this trend. Insights shared at the AIA Conference on Architecture 2025 indicate that healthier interior environments are driving a 5.9% increase in R&D spending on functional additives. In response, HEC is increasingly combined with self-crosslinking acrylic binders to enhance scrub resistance and block resistance without reliance on traditional coalescing solvents. This positions HEC as a cornerstone ingredient for premium, regulation-compliant interior coatings marketed on durability and occupant wellness.

Supply Chain Volatility Accelerating Vertical Integration in Cellulose Ethers

The global HEC market remains highly exposed to fluctuations in dissolving wood pulp pricing, creating margin pressure and supply uncertainty for downstream formulators. As of December 2025, capacity rationalization in the pulp industry and evolving trade policies have driven notable volatility. In September 2025, the APAC Cellulose Ether Price Index increased by 0.39% quarter over quarter, with average HEC prices reaching approximately USD 4,516 per metric ton FOB Qingdao, reflecting higher refined cotton and energy input costs.

Global dissolving pulp consumption reached roughly 10 million tons in 2024, with viscose fiber absorbing around 83% of supply. The remaining 17% allocated to cellulose ethers is increasingly constrained, particularly for specialty grades required in coatings, construction chemicals, and energy applications. Government data from India, the world’s second-largest pulp consumer, highlights rising dependence on imports to satisfy an annual pulp requirement of approximately 1.2 million tons, intensifying competition for feedstock availability.

In response, producers such as Ashland and Novonesis are implementing strategic sourcing and backward-integration initiatives. These include securing 20 to 25% of wood pulp needs from certified sustainable forests to stabilize costs, manage 20 to 30% raw material price swings observed over the past two years, and comply with REACH and the EU Deforestation Regulation. Vertical integration is increasingly viewed not only as a cost-control lever but as a prerequisite for long-term supply reliability in the HEC market.

High-Purity HEC for Advanced Shale Gas Hydraulic Fracturing

The resurgence of multi-stage hydraulic fracturing in the Permian and Delaware basins has opened a high-margin opportunity for ultra-clean Hydroxyethyl Cellulose grades. Compared with guar gum, high-purity HEC delivers superior performance in high-salinity environments while minimizing formation damage due to its low residue profile after gel breaking.

Operational data from 2024 and 2025 indicates that shale operators adopting specialized HEC-modified drilling and fracturing fluids achieved measurable wellbore stability improvements. ExxonMobil reported a 52% reduction in wellbore collapse incidents after deploying tailored HEC systems, attributing the gains to HEC’s non-ionic chemistry and reduced sensitivity to brine interference in deep shale formations.

Technological advances in low-viscosity HEC variants further strengthen this opportunity. These grades form effective filter cakes on well walls, reducing fluid loss by up to 40% and stabilizing downhole pressure during high-risk operations, including coalbed methane and tight gas plays. Modern HEC products are also engineered for complete solubility in 15% hydrochloric acid, enabling rapid degradation during post-fracturing cleanup and preserving reservoir permeability. This clean-break performance is increasingly viewed as essential for maximizing hydrocarbon recovery and lowering long-term production risk.

Aqueous Electrode Slurries for Next-Generation EV Battery Manufacturing

A frontier growth avenue for Hydroxyethyl Cellulose is emerging within the electric vehicle battery supply chain as manufacturers transition away from toxic solvents such as NMP toward fully aqueous processing. HEC is gaining traction as a critical binder and rheology modifier for electrode slurries used in lithium-ion battery production.

Peer-reviewed research published in September 2025 confirms that the molecular weight of cellulose binders plays a decisive role in slurry rheology. High-molecular-weight HEC grades enhance storage modulus and yield stress, preventing particle slumping during high-speed coating operations that now reach line speeds of up to 15 meters per minute. This performance is particularly critical for high-nickel cathode chemistries such as NMC811, where coating uniformity directly influences thermal stability and cycle life.

HEC’s strong water-retention capacity also enables crack-free electrode formation by controlling solvent evaporation during drying. Manufacturers leveraging optimized HEC formulations are targeting up to a 15% improvement in formulation accuracy and yield, reducing active material waste at a time when the battery industry is scaling toward terawatt-hour production levels by 2030. As regulatory pressure mounts to eliminate hazardous solvents from gigafactories, HEC is positioned as a strategic enabler of safer, higher-yield, and more sustainable battery manufacturing processes.

Hydroxyethyl Cellulose Market Share and Segmentation Insights

Industrial Grade Hydroxyethyl Cellulose Leads the Market Through Construction and Industrial Applications

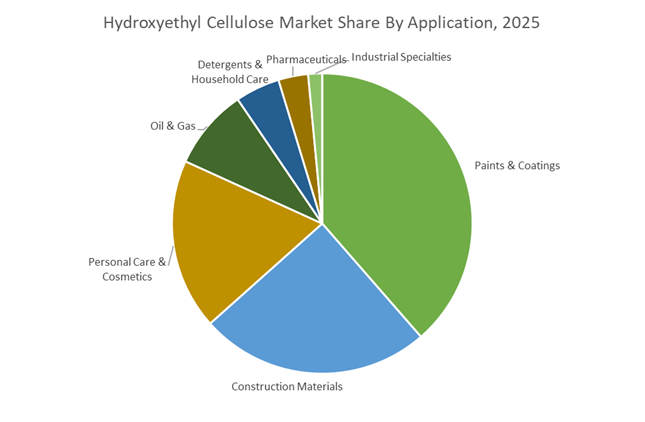

Industrial grade hydroxyethyl cellulose (HEC) accounted for 48.60% of the Hydroxyethyl Cellulose Market share in 2025, making it the dominant grade across global industrial formulations. Industrial grade HEC is extensively used as a water-soluble thickener, rheology modifier, and water-retention agent in high-volume sectors such as construction materials, paints and coatings, oilfield chemicals, and industrial formulations, where ultra-high purity specifications are not required. The material offers excellent viscosity control, film-forming capability, and compatibility with water-based systems, making it a versatile additive for large-scale manufacturing processes. In 2025, demand growth in this segment is strongly linked to the global construction expansion, particularly in emerging economies across Asia-Pacific, the Middle East, and Latin America where urbanization and infrastructure investment are accelerating. Hydroxyethyl cellulose is widely incorporated into cement-based mortars, tile adhesives, gypsum plasters, and joint compounds, where it improves water retention, workability, and application performance. These functional benefits enhance curing consistency and mechanical strength in cementitious materials, reinforcing industrial grade HEC’s position as a critical additive in modern construction chemistry.

Paints and Coatings Segment Drives the Largest Hydroxyethyl Cellulose Consumption

Paints and Coatings represented 38.60% of the Hydroxyethyl Cellulose Market share in 2025, establishing the sector as the largest application for hydroxyethyl cellulose-based rheology modifiers. HEC is widely used in water-based architectural paints, industrial coatings, and decorative coatings because it delivers essential rheological properties such as pigment suspension, viscosity control, flow and leveling performance, and spatter resistance during roller or spray application. These characteristics enable paint manufacturers to maintain uniform dispersion of pigments and fillers while ensuring smooth coating films on surfaces. In 2025, demand in this segment is being significantly influenced by the global transition toward low-VOC and waterborne coating technologies, driven by stricter environmental regulations and sustainability initiatives in the coatings industry. As solvent-based coatings decline, water-based latex systems increasingly rely on cellulose-based rheology modifiers such as HEC to achieve the required application performance without organic solvents. This transition has strengthened the role of hydroxyethyl cellulose as a core functional additive in zero-VOC and low-VOC coating formulations, particularly in architectural paints used in residential and commercial construction.

Competitive Landscape in Hydroxyethyl Cellulose Market

Ashland Strengthens Pharmaceutical-Grade HEC Leadership

Ashland Inc. remains a benchmark supplier of high-performance hydroxyethyl cellulose for pharmaceutical and personal care applications. The April 2025 expansion of its Nanjing cellulose ether facility directly targets rising demand for pharmaceutical-grade HEC in Asia-Pacific. Its Natrosol brand continues to dominate architectural coatings and cosmetics due to strong biostability and efficient thickening performance. In 2025, Ashland introduced low-impurity HEC grades tailored for ophthalmic solutions and advanced drug delivery systems, reinforcing its presence in regulated healthcare markets. Under its Responsible Solvers framework, the company is emphasizing pulp traceability, emissions reduction, and lower environmental impact manufacturing to align with 2030 sustainability targets.

Dow Integrates HEC into Consumer Care and Energy Applications

Dow Inc. leverages its global materials science platform to position hydroxyethyl cellulose within both consumer care and infrastructure segments. The CELLOSIZE HEC portfolio supports sulfate-free shampoo formulations and clean-label personal care products, responding to global ingredient transparency trends. In oil and gas, CELLOSIZE HEC grades function as high-efficiency viscosifiers for workover and completion fluids, ensuring stable rheology under high salinity conditions. Dow is prioritizing bio-based and circular feedstocks for cellulose derivatives to comply with evolving EU chemical safety regulations. With strong penetration in North America, Dow maintains a leading share in the United States hydroxyethyl cellulose market, supported by integrated supply capabilities.

Shin-Etsu Expands Pharmaceutical Cellulose Capacity Globally

Shin-Etsu Chemical is executing a differentiation strategy to elevate specialty cellulose ethers above commodity cycles. A 10 billion yen investment announced in 2025 and 2026 includes a new cellulose derivatives facility in Germany and expanded storage infrastructure in Japan. The company reported a 17.7% increase in operating income for its Functional Materials segment in the fiscal year ending March 2025, driven by strong demand for high-functionality cellulose products. Shin-Etsu emphasizes supply chain resilience through diversified production footprints across Europe and Asia. A 500 billion yen share buyback initiated in May 2025 reflects financial strength and long-term confidence in specialty materials growth.

Nouryon Advances Hydrophobically Modified EHEC Technologies

Nouryon is a leading supplier of ethyl hydroxyethyl cellulose for premium architectural coatings. In March 2025, the company introduced Bermocoll EHM MAX, a hydrophobically modified EHEC grade reported to deliver approximately 10% higher efficiency than conventional rheology modifiers. The company is evaluating Southeast Asian sites for a new 15,000 to 20,000 ton per year production facility to support regional construction expansion. Nouryon’s integrated manufacturing model emphasizes co-location with key customers to reduce logistics emissions and enhance supply reliability. Its EHEC variants offer superior salt tolerance and solubility control, supporting high-performance interior and exterior paint formulations.

Lotte Fine Chemical Targets Infrastructure and Green Feedstocks

Lotte Fine Chemical has established itself as a key Asian exporter of cellulose ethers, particularly in self-leveling construction materials and cement-based formulations. Its Mecellose brand competes directly in building materials and industrial coatings applications across Southeast Asia and the Middle East. The company is optimizing high-viscosity HEC grades to improve water retention in arid-climate infrastructure projects, a critical performance parameter for large-scale construction. In 2025, Lotte expanded its Green Cellulose research initiatives to explore agricultural waste as an alternative feedstock for next-generation cellulose ethers. This pivot aligns with sustainability-driven procurement policies in public infrastructure projects.

SE Tylose Drives European Regulatory and Process Excellence

SE Tylose, part of the Shin-Etsu Group, operates one of the most advanced hydroxyethyl cellulose plants globally, centered in Wiesbaden. The facility is a major supply hub for European natural and vegan cosmetic markets. In 2025 and 2026, implementation of advanced process analytics and real-time viscosity monitoring reduced downtime by an estimated 15% and improved molecular weight consistency. The Tylose brand offers a broad viscosity spectrum for tile adhesives, exterior insulation systems, and high-performance coatings. SE Tylose is positioning itself as a regulatory leader by proactively aligning with upcoming EU environmental and labeling standards ahead of 2027 compliance deadlines.

United States: Capacity Consolidation and Regulatory-Driven Demand Upgrade

The United States hydroxyethyl cellulose industry is undergoing structural consolidation combined with quality-driven demand expansion. In July 2025, Ashland Inc. rationalized its domestic manufacturing footprint by closing the Parlin, New Jersey facility and transferring all HEC output to Hopewell, Virginia. This move is anchored in a $60 million investment strategy aimed at achieving larger batch economics, improved asset utilization, and tighter control over pharmaceutical- and personal-care-grade specifications. The consolidation reflects broader U.S. trends toward near-shoring and scale optimization as import volatility and tariff exposure disrupted legacy cellulose ether supply chains in early 2025.

Regulatory forces are reinforcing this shift. Stricter low-VOC mandates enforced by the Environmental Protection Agency during 2025–2026 have accelerated the substitution of solvent-borne thickeners with high-purity, bio-based HEC in architectural and industrial waterborne coatings. Parallel to coatings, pharmaceutical excipient demand has strengthened materially. U.S. producers reported a roughly 20% rise in high-purity pharmaceutical-grade HEC output across 2024–2025, driven by controlled-release oral solids and ophthalmic formulations where viscosity stability and inertness are critical. Trade tariffs introduced in early 2025 further reinforced domestic expansion, as formulators in personal care and home care sought pricing stability through local sourcing.

China: Volume Leadership with Green Manufacturing Discipline

China continues to anchor global hydroxyethyl cellulose volume supply, while simultaneously tightening environmental and quality controls. Under the Ministry of Industry and Information Technology priority framework for high-end specialty chemicals, a leading producer in Nanjing commissioned a new production line in 2025, adding 25,000 tons of annual HEC capacity primarily aimed at infrastructure-linked applications such as dry-mix mortars and construction additives. This expansion reinforces China’s role as the primary volume supplier for Asia-Pacific construction markets.

At the same time, policy incentives are reshaping production practices. Government green manufacturing blueprints for 2025–2026 offer tax rebates for plants adopting automated etherification and digital quality-control systems, with reported improvements of around 16% in batch consistency. Supply stability also benefited indirectly from the Ministry of Commerce decision in November 2025 to suspend certain export controls on lithium-battery-related raw materials, easing pressure on upstream cellulose ether feedstocks used in battery binders. Looking ahead, new 2026 provincial regulations in Jiangsu mandating closed-loop solvent recovery during HEC synthesis are raising compliance thresholds, favoring larger, technologically advanced producers over smaller regional operators.

India: Construction-Led Growth and Clean Beauty Substitution

India’s hydroxyethyl cellulose demand profile is being shaped by infrastructure acceleration and formulation shifts in personal care. Under the National Infrastructure Pipeline, large-scale residential and commercial construction activity during 2025–2026 has materially increased the use of HEC in cementitious mortars, tile adhesives, and renders, where water retention and workability directly affect application efficiency. This construction-driven pull is structurally different from cyclical coatings demand and provides steady baseline consumption for domestic suppliers.

Simultaneously, India has emerged as a fast-growing personal care innovation hub. In 2025, domestic cosmetic brands launched a record number of clean-label products, replacing synthetic carbomers with HEC as a biodegradable rheology modifier in sulfate-free shampoos and skin gels. On the supply side, Gujarat Alkalies and Chemicals Ltd. optimized its specialty chemical lines in late 2025 to expand local availability of HEC derivatives for oil and gas drilling fluids, supporting import substitution in a segment historically dependent on overseas suppliers.

South Korea: High-Value Differentiation Beyond Construction

South Korea’s hydroxyethyl cellulose industry is pivoting away from volume-driven construction markets toward higher-margin specialty applications. Lotte Fine Chemical reported improved profitability in its green materials division in Q3 2025, supported by rising sales of MECELLOSE® HEC grades despite subdued downstream construction activity. This shift reflects a deliberate focus on premium performance attributes rather than tonnage growth.

Innovation is reinforcing this repositioning. In March 2025, South Korean researchers demonstrated the viability of hydroxyethyl cellulose as a water-soluble co-binder for high-voltage lithium-ion battery cathodes, achieving 82% capacity retention after 200 cycles. This research has elevated HEC’s profile in energy storage materials. In parallel, Lotte’s broader digitalization roadmap includes Robotic Process Automation and AI-driven efficiency models, with plans to extend these systems to cellulose ether production lines by late 2026 to enhance yield predictability and cost control.

Germany: Compliance-Driven Innovation and Smart Coatings

Germany’s hydroxyethyl cellulose landscape is being reshaped by regulatory enforcement and sustainability-led material innovation. European producers operating in Germany, including Nouryon and Shin-Etsu Chemical, are upgrading reactors and energy systems to comply with updated Industrial Emissions Directive standards for 2025–2026. These upgrades are targeting emission reductions of up to 14%, increasing capital intensity but improving long-term regulatory resilience.

Compliance scrutiny has also intensified. In June 2025, the European Chemicals Agency launched its REF-15 enforcement project to verify safe-use information in safety data sheets, directly affecting high-viscosity HEC grades used in industrial workplaces. Beyond compliance, Germany is leveraging HEC in advanced material development. Climate-neutral construction initiatives have spurred R&D into nano-structured HEC for smart coatings, where enhanced corrosion resistance and durability are critical for heavy industrial environments.

Brazil: Localization and Energy-Linked Demand

Brazil is emerging as a strategic development market for hydroxyethyl cellulose, driven by localized innovation and offshore energy activity. In December 2025, Nouryon broke ground on a Home and Personal Care Innovation Center in Itupeva, designed to co-create biopolymer-based HEC solutions adapted to South American climatic and consumer conditions. The facility is expected to support regional formulation development rather than bulk export production.

Energy exploration is providing an additional demand pillar. Rising offshore drilling activity in Brazil’s pre-salt fields has increased the use of salt-tolerant HEC grades as fluid-loss additives in complex drilling fluids. This application favors technically robust formulations and positions Brazil as a niche but strategically important market for high-performance HEC rather than commodity grades.

Comparative Snapshot: Hydroxyethyl Cellulose Industry by Country

Hydroxyethyl Cellulose Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Strategic Shift

|

Industry Implication

|

|

United States

|

VOC regulation and pharma demand

|

Capacity consolidation and near-shoring

|

Higher purity, domestic supply focus

|

|

China

|

Infrastructure and volume leadership

|

Green manufacturing and compliance

|

Scale advantage with rising entry barriers

|

|

India

|

Infrastructure and clean beauty

|

Import substitution and formulation shift

|

Broad-based domestic consumption growth

|

|

South Korea

|

Specialty materials and batteries

|

Premium differentiation

|

Margin expansion beyond construction

|

|

Germany

|

Regulatory enforcement and sustainability

|

Smart coatings and compliance upgrades

|

Innovation-led, high-cost positioning

|

|

Brazil

|

Localization and offshore energy

|

Regional innovation hubs

|

Niche, performance-driven demand

|

Hydroxyethyl Cellulose Market Report Scope

Hydroxyethyl Cellulose Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$2 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Grade (Industrial Grade, Cosmetic Grade, Pharmaceutical Grade, Food Grade), By Viscosity Type (Low Viscosity, Medium Viscosity, High Viscosity), By Physical Form (Powder, Liquid / Solution), By Application (Paints & Coatings, Construction Materials, Personal Care & Cosmetics, Oil & Gas, Pharmaceuticals, Detergents & Household Care, Industrial Specialties)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ashland Inc., Dow Inc., Shin-Etsu Chemical Co., Ltd., Nouryon B.V., Lotte Fine Chemical Co., Ltd., Cargill, Incorporated, Daicel Corporation, Lamberti S.p.A., JNC Corporation, Zhejiang Haishen New Materials Co., Ltd., Shandong Head Pharmaceutical Co., Ltd., Wuxi Sanyou New Material Technology Co., Ltd., Celotech Chemical Co., Ltd., Yil-Long Chemical Group, Shandong Bide Pharmaceutical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydroxyethyl Cellulose Market Segmentation

By Grade

- Industrial Grade

- Cosmetic Grade

- Pharmaceutical Grade

- Food Grade

By Viscosity Type

- Low Viscosity

- Medium Viscosity

- High Viscosity

By Physical Form

By Application

- Paints & Coatings

- Construction Materials

- Personal Care & Cosmetics

- Oil & Gas

- Pharmaceuticals

- Detergents & Household Care

- Industrial Specialties

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydroxyethyl Cellulose Industry

- Ashland Inc.

- Dow Inc.

- Shin-Etsu Chemical Co., Ltd.

- Nouryon B.V.

- Lotte Fine Chemical Co., Ltd.

- Cargill, Incorporated

- Daicel Corporation

- Lamberti S.p.A.

- JNC Corporation

- Zhejiang Haishen New Materials Co., Ltd.

- Shandong Head Pharmaceutical Co., Ltd.

- Wuxi Sanyou New Material Technology Co., Ltd.

- Celotech Chemical Co., Ltd.

- Yil-Long Chemical Group

- Shandong Bide Pharmaceutical Co., Ltd.

*- List not Exhaustive