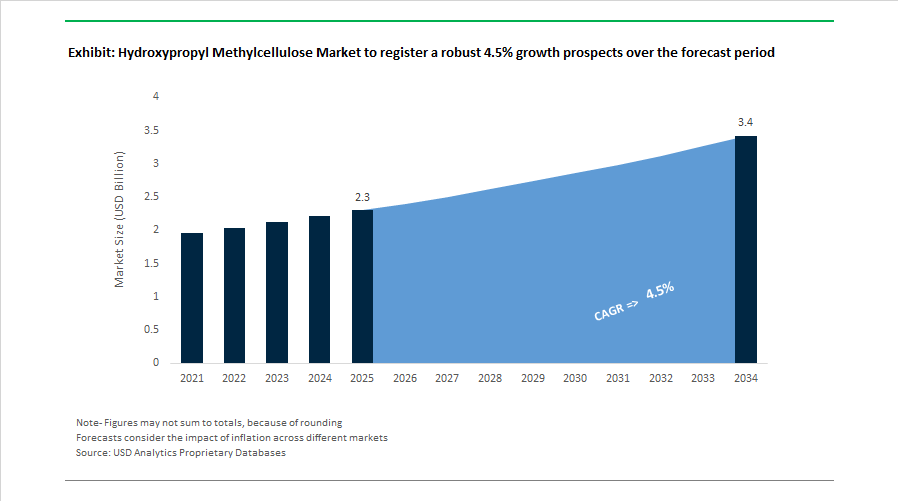

Hydroxypropyl Methylcellulose Market to Reach $3.4 Billion by 2034 at 4.5% CAGR Driven by Pharma-Grade HPMC, Plant-Based Foods, and Dual-Supply Manufacturing Expansion

The Hydroxypropyl Methylcellulose (HPMC) Market is projected to grow from $2.3 billion in 2025 to $3.4 billion by 2034, registering a CAGR of 4.5%. Market expansion is anchored in pharmaceutical excipients, controlled-release drug delivery systems, plant-based capsule technologies, and functional food formulations. Increasing regulatory scrutiny around nitrosamines, rising demand for vegetarian alternatives to gelatin, and strategic capacity expansions across Japan and Europe are redefining the global HPMC competitive environment.

In March 2024, Shin-Etsu Chemical announced a 10 billion yen investment to double production capacity of its pharmaceutical excipient Shin-Etsu AQOAT at the Naoetsu plant in Japan, with completion scheduled for Q2 2026. This expansion directly targets growing global demand for hypromellose acetate succinate polymers that enhance solubility of poorly water-soluble active pharmaceutical ingredients. In May 2024, Vivion, Inc. was recognized in the ICIS Top Chemical Distributors list, reinforcing its strategic role in the nutraceutical and healthy aging supply chain where HPMC capsules are increasingly preferred. In October 2024, at AAPS PharmSci 360, IFF Pharma Solutions presented new research demonstrating the use of HPMC excipients in plant-based pharmaceutical gummies and softgels, reflecting the structural shift away from animal-derived gelatin.

Pharmaceutical-grade innovation accelerated in 2025. In April 2025, IFF launched its Low Nitrite METHOCEL™ HPMC range, engineered to mitigate nitrosamine formation risks. Each batch is tested using ion chromatography to maintain nitrite levels at or below 200 ppb, enabling safer modified-release drug formulations. In April 2025, Shin-Etsu Chemical announced construction of a new pharmaceutical excipient facility at SE Tylose GmbH in Wiesbaden, Germany, establishing a dual-base production system between Japan and Europe, with completion targeted for the second half of 2026. During 2025, Shin-Etsu also doubled warehouse capacity at its Naoetsu plant to strengthen supply chain resilience. In October 2025, Ashland appointed Tilley Distribution as its exclusive U.S. food ingredient distributor for Benecel™ HPMC, intensifying its focus on nutraceuticals and plant-based protein markets in North America. Throughout 2024–2025, Evonik continued expanding adoption of its EUDRACAP HPMC capsules designed for enteric and fast-track drug delivery systems.

Strategic realignment intensified entering 2026. Effective January 1, 2026, Ashland and Univar Solutions established an exclusive EMEA distribution agreement under Foodology by Univar Solutions, targeting the expanding vegan, gluten-free, and plant-based food sectors across Europe, the Middle East, and Africa. In February 2026, Ashland reported fiscal Q1 results confirming that portfolio optimization toward high-margin HPMC and specialty additives sustained solid margins despite temporary startup delays at its Calvert City facility. In the same month, Lotte Chemical, parent of Lotte Fine Chemical, announced a 2026 strategic pivot to reduce commodity petrochemical exposure and accelerate expansion in green materials, including HPMC for food and pharmaceutical applications. In December 2025, Nouryon broke ground on its Home and Personal Care Innovation Center in Brazil, scheduled to become operational in late 2026, focusing on sustainable cellulose ether solutions tailored to South American demand. These developments collectively reinforce the structural shift toward high-purity, plant-based, and regionally diversified HPMC manufacturing ecosystems.

Hydroxypropyl Methylcellulose (HPMC) Market Trends and Opportunities Driving Multi-Industry Applications

Rapid Growth of Dry-Mix Mortars in Construction Increasing Demand for High-Performance HPMC Additives

The hydroxypropyl methylcellulose (HPMC) market is experiencing strong growth driven by rising demand for high-performance dry-mix mortars in modern construction applications. HPMC acts as a critical rheology modifier, water-retention agent, and workability enhancer in cement-based formulations, making it essential for tile adhesives, wall putty, self-leveling compounds, and thermal insulation mortars. As the construction sector increasingly adopts prefabricated building systems, automated construction processes, and green building standards, demand for specialized HPMC grades that improve cement hydration and reduce water evaporation is expanding significantly.

Industry developments highlight the scaling demand for these additives. By early 2026, the global dry-mix mortar additives market has expanded rapidly due to accelerated urban construction and smart city infrastructure development. Leading manufacturers such as Shin-Etsu Chemical have expanded their high-performance HPMC portfolios to support next-generation cementitious materials used in high-strength structural systems. At the formulation level, manufacturers including Chongqing Borida and Jinzhou Ashland are increasing production of customized HPMC grades with specific viscosity profiles to optimize curing performance in large-format tile adhesives and insulation mortars. Regional infrastructure development is also supporting demand growth. In the Asia-Pacific region, which remains the largest consumer of HPMC for construction applications, rising housing construction is a major catalyst. For example, Australia reported more than 240,800 dwellings under construction in early 2026, significantly increasing demand for factory-produced dry-mix mortar systems that reduce on-site labor requirements.

Clean-Label Food and Plant-Based Product Innovation Expanding HPMC Functional Ingredient Applications

The global shift toward plant-based foods and clean-label ingredients is significantly expanding the use of HPMC across food and nutraceutical formulations. As consumers increasingly prefer non-animal alternatives and preservative-free food products, HPMC is being widely adopted as a gelatin substitute, stabilizer, binder, and thermal-gelling agent in plant-based meat products, baked goods, and dairy alternatives. Its ability to create desirable texture, maintain moisture, and stabilize emulsions makes it a valuable ingredient in next-generation vegan and gluten-free food formulations.

Food industry innovation is reinforcing this trend. In December 2025, Kerry Group’s “2026 Taste Trends” report highlighted clean-label formulation and format innovation as key drivers of food product development, with HPMC increasingly used to replicate the mouthfeel and fat-like texture of animal-derived ingredients in plant-based meat analogs. The nutraceutical sector is also witnessing a rapid transition toward vegetarian capsule technologies. In 2025, companies such as Lonza and ACG expanded manufacturing of HPMC-based hollow capsules designed for vegan dietary supplements and allergen-free formulations. These capsules are gaining popularity due to their low moisture content and high stability, making them ideal for encapsulating moisture-sensitive ingredients such as probiotics and functional nutrients. As regulatory focus on natural ingredient claims intensifies, the vegetable capsule segment is projected to grow at approximately 10% CAGR between 2025 and 2034, further strengthening the demand for pharmaceutical- and food-grade HPMC.

Advanced Drug Delivery Systems Creating Opportunities for HPMC in Controlled-Release Pharmaceutical Formulations

The pharmaceutical applications of HPMC represent one of the most technologically advanced segments of the market, particularly in controlled-release drug delivery systems. HPMC functions as a hydrophilic matrix polymer in solid dosage forms, enabling the gradual release of active pharmaceutical ingredients (APIs) over extended periods. This capability is crucial for improving therapeutic effectiveness, reducing dosing frequency, and enhancing patient adherence, particularly in treatments for chronic diseases such as diabetes, cardiovascular disorders, and hypertension.

Recent pharmaceutical innovations highlight the growing importance of HPMC excipients. In November 2025, Roquette received the New Ingredient Award for its Low Nitrite METHOCEL™ HPMC, developed to mitigate nitrosamine contamination risks in drug formulations. The ingredient maintains nitrite levels below 200 parts per billion, supporting compliance with evolving FDA and EMA safety guidelines. Meanwhile, Colorcon highlighted in May 2025 the role of HPMC in improving drug bioavailability, particularly through the conversion of poorly soluble crystalline drugs into amorphous forms using Lotte Fine Chemical’s AnyCoat® HPMC technology. This approach can improve drug absorption by nearly 40% for BCS Class II and IV compounds. Academic research published in June 2025 further demonstrated the effectiveness of multi-layer tablet systems using different HPMC viscosity grades, enabling both immediate-release and extended-release drug delivery within a single tablet.

High-Purity HPMC Unlocking New Opportunities in Ophthalmic Surgery and Medical Device Applications

Beyond pharmaceuticals and food products, high-purity HPMC (Hypromellose) is emerging as a critical material in ophthalmic surgery, medical devices, and advanced healthcare applications. Due to its biocompatibility, lubricating properties, and optical clarity, HPMC is widely used in ophthalmic viscosurgical devices (OVDs) during cataract surgery and other delicate eye procedures. These solutions help maintain eye structure during surgery while protecting sensitive tissues such as the corneal endothelium.

Recent clinical developments highlight the expanding medical applications of HPMC. In January 2026, researchers from University College London and Moorfields Eye Hospital published findings demonstrating that HPMC injections can successfully treat ocular hypotony, a condition characterized by dangerously low intraocular pressure. The study reported that seven out of eight patients regained vision after treatment, demonstrating the potential of HPMC as a safe alternative to silicone oil in ocular therapies. The global rise in cataract surgeries associated with aging populations is also increasing demand for HPMC-based ophthalmic lubricants and surgical aids. Additionally, sustainability considerations are emerging in the medical sector. Industry reports in 2025 indicated that while HPMC is biodegradable, only around 25% of HPMC-based medical products are currently recycled, creating new opportunities for closed-loop packaging systems and biodegradable HPMC-based containers for liquid pharmaceutical formulations.

Hydroxypropyl Methylcellulose Market Share and Segmentation Insights

Industrial Grade Hydroxypropyl Methylcellulose Leads the Market Through Expanding Construction Chemical Applications

Industrial grade hydroxypropyl methylcellulose (HPMC) accounted for 48.60% of the Hydroxypropyl Methylcellulose Market share in 2025, making it the largest grade segment within global cellulose ether demand. Industrial grade HPMC is widely used as a thickener, binder, water-retention agent, and rheology modifier in high-volume industrial applications, particularly within the construction chemicals industry. Its primary role is in cement-based and gypsum-based dry-mix materials, including tile adhesives, plasters, renders, skim coats, and self-leveling compounds, where it improves workability, adhesion, and curing consistency. Because these applications do not require pharmaceutical or food-grade purity levels, industrial grade HPMC offers the most cost-efficient option for manufacturers of construction materials and industrial formulations. In 2025, the segment is benefiting from the global upgrade in construction quality standards, particularly in emerging markets where builders increasingly adopt premium dry-mix mortars and standardized construction materials. This shift has created stronger demand not only for higher volumes of HPMC but also for more specialized viscosity grades optimized for advanced construction systems, reinforcing industrial grade HPMC as a foundational additive in modern construction chemistry.

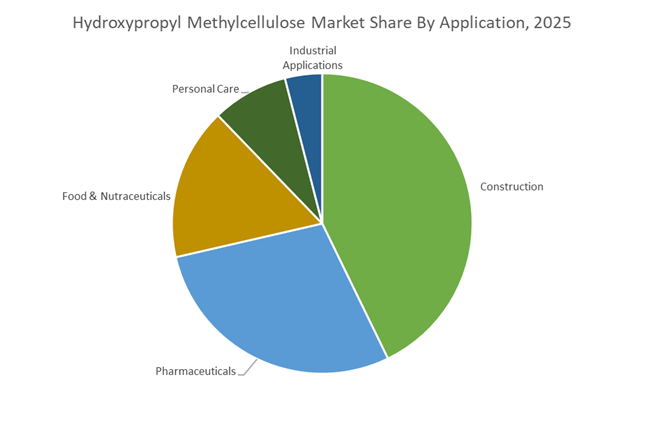

Construction Industry Drives the Largest Hydroxypropyl Methylcellulose Consumption

Construction represented 42.80% of the Hydroxypropyl Methylcellulose Market share in 2025, establishing it as the largest application segment for HPMC-based additives. HPMC plays a critical functional role in cementitious and gypsum-based building materials, where it provides water retention, improved workability, extended open time, and enhanced slip resistance in tile adhesives, mortars, plasters, and self-leveling compounds. Water retention is particularly important because it ensures proper hydration of cement particles, improving bond strength and preventing premature drying during installation. The increasing global adoption of factory-produced dry-mix construction materials has further strengthened HPMC demand, as these products require consistent rheology control and reliable performance during application. In 2025, construction material innovation is also being shaped by sustainability initiatives within the building industry. HPMC enables the formulation of lightweight mortar systems that reduce material consumption and transportation emissions, while also supporting recycled aggregates and alternative cement binders used in green building materials. These characteristics position hydroxypropyl methylcellulose as an enabling additive for the next generation of environmentally optimized construction products.

Competitive Landscape in Hydroxypropyl Methylcellulose Market

Shin-Etsu Reinforces Pharmaceutical Dominance and Thermal Performance

Shin-Etsu Chemical remains the largest global producer of cellulose ethers, leveraging SE Tylose as its core manufacturing platform. In May 2025, the company approved a ¥500 billion share buyback, underscoring strong free cash flow generation from specialty chemicals. A ¥10 billion investment program through 2026 is strengthening pharmaceutical cellulose production, including a new facility in Germany to serve regulated European markets. The company is advancing HEMC and HPMC hybrid grades engineered for enhanced gelation stability in high-temperature construction environments across Asia and the Middle East. Implementation of biomass cogeneration systems in Southeast Asia is reducing annual CO2 emissions by approximately 48,000 tons, reinforcing long-term sustainability positioning.

Ashland Prioritizes High-Purity Pharma and Clean-Label Cosmetics

Ashland Inc. has transitioned into a focused specialty materials company emphasizing pharmaceutical and personal care applications. In February 2026, it refined its Adjusted EBITDA outlook to $400 to $420 million, reflecting disciplined portfolio management. Under the Benecel brand, Ashland introduced a low-nitrite HPMC grade designed to improve stability of sensitive active pharmaceutical ingredients in solid oral dosage forms. A $103 million tax refund in late 2025 strengthened liquidity and R&D investment capacity in cellulose excipients. Through its Globalize Pillar strategy, Ashland targets double-digit expansion in biofunctional actives and microbial protection, leveraging HPMC’s film-forming properties for clean-label cosmetic formulations.

Dow Restructures to Focus on High-Margin Cellulose Derivatives

Dow Inc. is executing structural realignment to prioritize high-value performance materials and coatings. The Transform to Outperform initiative launched in January 2026 aims to generate $2 billion in additional operating EBITDA by 2028 through simplification and asset optimization. Dow is rationalizing upstream capacity, including the planned shutdown of a major UK siloxanes plant, to reallocate capital toward specialty derivatives such as HPMC. Recent innovation includes cellulose-based alternatives to fluoropolymer processing aids, supporting PFAS-free packaging regulations. The company is shifting from merchant sales models toward supplying higher-margin internal derivative demand in construction and packaging applications.

Shandong Head Group Expands Global Capsule Integration

Shandong Head Group has evolved into a vertically integrated competitor controlling HPMC powder production and empty capsule manufacturing. In 2026, the company is finalizing investment in a United States facility capable of producing more than 20 billion capsules annually, strengthening its presence in North American plant-based capsule supply chains. A May 2025 exclusive European distribution agreement with Univar Solutions enhances regulatory and market access for pharmaceutical-grade HPMC. Its production facilities achieved EcoVadis Silver and Bronze ratings in 2025, supporting credibility with Western pharmaceutical customers. The Headcel HPMC powder and Healsee capsule brands position the company as a direct challenger to established multinational excipient suppliers.

Lotte Fine Chemical Accelerates Specialty Transition

Lotte Fine Chemical is repositioning its cellulose ether portfolio toward high-value pharmaceutical and food-grade applications. The Fine Chemical division reported KRW 439.1 billion in 2025 revenue, with profitability expected to improve following inventory normalization. Facility expansions in Ulsan support integration of high-purity cellulose derivatives alongside clean ammonia and electronic materials. Under its 100-Year Vision, the company targets KRW 7 trillion in sales by 2030 by increasing specialty product contribution, including materials for EV and semiconductor sectors. Dividend commitments in early 2026 reflect financial discipline while maintaining investment momentum in high-margin cellulose derivatives.

Nouryon Strengthens Bio-Based and Infrastructure Solutions

Nouryon continues to advance a customer-focused strategy centered on construction and life science additives. The opening of a major Innovation Center in Shanghai in November 2025 significantly expanded regional technical support capabilities. In 2026, the company introduced fully bio-based detergent ingredients aligned with biodegradable polymer trends, leveraging cellulose derivative expertise. Supply chain resilience initiatives and collaboration with logistics and chemical partners reinforce reliability in global HPMC distribution. The Bermocoll line remains a leading solution in European smart-city infrastructure projects and water-based paints, valued for its rheological control and compatibility with sustainable building materials.

United States: Onshoring Momentum and High-Throughput Pharmaceutical Enablement

The United States hydroxypropyl methylcellulose industry is undergoing decisive supply chain consolidation alongside policy-backed onshoring of pharmaceutical excipients. In 2025, Ashland Inc. accelerated its $60 million manufacturing optimization by consolidating specialty cellulose production at Hopewell, Virginia. This move strengthens operational efficiency and scale for the Benecel™ HPMC portfolio, particularly for large-scale, high-speed tableting lines where particle size control and batch uniformity are critical. Deployment of fine-particle Benecel™ XRF grades reached a key milestone in 2025, supporting continuous manufacturing environments that demand predictable flowability and compression behavior.

Policy alignment is reinforcing domestic capacity. Under Executive Order 14293, the U.S. Food and Drug Administration convened public meetings in late 2025 to streamline onshoring of critical excipients, offering Facility Readiness guidance that directly benefits HPMC producers supplying regulated drug products. Downstream integration also advanced with Ashland’s October 2025 appointment of Tilley Distribution as its exclusive U.S. partner for cellulosics in food, beverage, and nutraceuticals, tightening supply chains for HPMC-based meat alternatives and gluten-free formulations. Beyond pharma, U.S. architectural coatings formulators are adopting HPMC as a primary thickener to meet stricter 2026 VOC limits, leveraging its bio-derived profile to position net-zero residential coatings.

China: Regulatory Realignment and Global Capsule Leadership

China’s HPMC industry is being reshaped by tighter excipient governance and expanding dominance in vegetarian capsule manufacturing. In March 2025, the National Medical Products Administration issued Announcement No. 30, refining the excipient framework and compelling domestic HPMC producers to align Quality Management Systems with global standards when supplying formulations originally developed with imported excipients. This has accelerated investments in compliance documentation, analytical capability, and process control across leading producers.

Food-contact compliance is also intensifying. The National Health Commission released GB 4806.10-2025 in September 2025, mandating stricter migration limits for cellulose-based additives in coatings used for food packaging effective September 2026. On the demand side, China has consolidated its position as a leading global supplier of HPMC-based vegetarian capsules, with firms such as Shandong Head expanding automated dipping lines to meet rising Western nutraceutical demand through 2026. Parallel regulatory tightening under the Ministry of Industry and Information Technology will enforce stricter RoHS thresholds from January 2026, requiring Supplier Declarations of Conformity for HPMC binders used in consumer electronics.

India: Domestic Excipient Emergence and Capsule Capacity Build-Out

India has reached a structural inflection point in HPMC with the emergence of domestic pharmaceutical-grade excipients. In May 2025, Pharcos Specialty Ltd. launched Pharcocel, the country’s first locally manufactured pharma-grade HPMC, directly supporting the Atmanirbhar Bharat objective to reduce reliance on imports from China and Europe. This milestone is reshaping qualification strategies among Indian generic manufacturers that previously depended on overseas sources for film coatings and binders.

Capacity expansion is accelerating downstream. Late 2025 saw Natural Capsules Limited and RHR Medicare commission new HPMC softgel lines to serve the fast-growing vegetarian capsule segment. In parallel, Ashland Inc. confirmed progress on its India tablet coating facility slated for 2026, positioning HPMC-based film coatings at the center of the country’s expanding generic drug output.

South Korea: Global Partnerships and Cross-Sector Material Integration

South Korea’s HPMC market is pivoting toward high-value positioning through global partnerships and cross-sector innovation. In October 2025, Lotte Fine Chemical finalized an exclusive multi-year partnership with Colorcon, appointing Colorcon as the global representative for the AnyCoat® HPMC family. This integration pairs Lotte’s high-purity manufacturing with a global technical services network, expanding reach in regulated pharmaceutical markets.

Financial resilience underpins this strategy. Lotte Fine Chemical reported KRW 443.4 billion in Q3 2025 sales, prioritizing high-value cellulose ethers to offset muted construction demand. Beyond pharma, South Korean electronics leaders are collaborating with HPMC producers to develop specialty binders for AI circuit foils and next-generation energy storage system battery foils, leveraging HPMC’s film-forming properties and thermal stability in advanced electronics manufacturing.

Japan: Solubility Enhancement Leadership and Smart-Release Drug Design

Japan continues to set the benchmark for advanced HPMC derivatives in controlled drug delivery. Shin-Etsu Chemical is on track to complete a 10 billion JPY expansion at its Naoetsu plant by Q2 2026, doubling capacity for Shin-Etsu AQOAT, a hypromellose acetate succinate grade used to enhance solubility of poorly dissolving APIs. This investment aligns with rising demand for bioavailability-enhancing excipients across complex oral formulations.

Japan’s pharmaceutical sector leads in HPMC-AS adoption for enteric and controlled-release drugs, with new patents filed in 2025 for smart-release capsules engineered to dissolve at precise intestinal pH thresholds. These innovations reinforce Japan’s role as a technology originator rather than a volume supplier in the global HPMC value chain.

Germany: Sustainable Pharma Packaging and Low-Carbon Production Pilots

Germany’s HPMC landscape is increasingly defined by sustainability and decarbonization objectives. The country will host Pharma Sustainability Days in early 2026, focusing on eco-conception of pharmaceutical packaging where HPMC is gaining traction as a biodegradable alternative to petroleum-based polymers in blister packs. This focus is translating into early adoption among European drug makers seeking to reduce packaging footprints.

Upstream, German chemical clusters including Evonik and Shin-Etsu Tylose are piloting green hydrogen in etherification reactors. These pilots target a reduction in the carbon intensity of HPMC production by approximately 15% by end-2026, positioning Germany as a leader in low-emission excipient manufacturing for regulated markets.

Comparative Snapshot: Hydroxypropyl Methylcellulose Industry by Country

Hydroxypropyl Methylcellulose Market County Level Snapshot

|

Country

|

Strategic Focus

|

Primary Driver

|

Competitive Implication

|

|

United States

|

Onshoring and CM readiness

|

FDA policy support and VOC limits

|

Domestic scale and pharma throughput

|

|

China

|

Compliance and capsule exports

|

NMPA realignment and food-contact rules

|

Global capsule supply leadership

|

|

India

|

Import substitution

|

Domestic excipient launches

|

Cost and security advantages

|

|

South Korea

|

Global partnerships

|

Pharma distribution integration

|

High-value market access

|

|

Japan

|

Advanced drug delivery

|

Solubility and smart-release tech

|

Technology leadership

|

|

Germany

|

Sustainability and decarbonization

|

Green packaging and hydrogen pilots

|

Low-carbon excipient positioning

|

Hydroxypropyl Methylcellulose Market Report Scope

Hydroxypropyl Methylcellulose Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2034)

|

$3.4 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Grade (Pharmaceutical Grade, Food Grade, Industrial Grade, Cosmetic Grade), By Function (Binder & Disintegrant, Thickener & Rheology Modifier, Film-Forming Agent, Controlled Release Matrix, Stabilizer & Emulsifier), By Application (Pharmaceuticals, Construction, Food & Nutraceuticals, Personal Care, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ashland Inc., Shin-Etsu Chemical Co., Ltd., Lotte Fine Chemical Co., Ltd., Dow Inc., Nouryon B.V., Shandong Head Co., Ltd., Associated British Foods plc, Colorcon, Inc., JNC Corporation, Kima Chemical Co., Ltd., Tai'an Ruitai Cellulose Co., Ltd., Celotech Chemical Co., Ltd., Zhejiang Haishen New Materials Co., Ltd., Pharcos Specialty Ltd., Huzhou Zhanwang Pharmaceutical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydroxypropyl Methylcellulose Market Segmentation

By Grade

- Pharmaceutical Grade

- Food Grade

- Industrial Grade

- Cosmetic Grade

By Function

- Binder & Disintegrant

- Thickener & Rheology Modifier

- Film-Forming Agent

- Controlled Release Matrix

- Stabilizer & Emulsifier

By Application

- Pharmaceuticals

- Construction

- Food & Nutraceuticals

- Personal Care

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydroxypropyl Methylcellulose Industry

- Ashland Inc.

- Shin-Etsu Chemical Co., Ltd.

- Lotte Fine Chemical Co., Ltd.

- Dow Inc.

- Nouryon B.V.

- Shandong Head Co., Ltd.

- Associated British Foods plc

- Colorcon, Inc.

- JNC Corporation

- Kima Chemical Co., Ltd.

- Tai'an Ruitai Cellulose Co., Ltd.

- Celotech Chemical Co., Ltd.

- Zhejiang Haishen New Materials Co., Ltd.

- Pharcos Specialty Ltd.

- Huzhou Zhanwang Pharmaceutical Co., Ltd.

*- List not Exhaustive