Market Overview: Structural Undervaluation of Kraft Lignin and Specialty-Grade Demand Are Recasting the Lignin Products Market

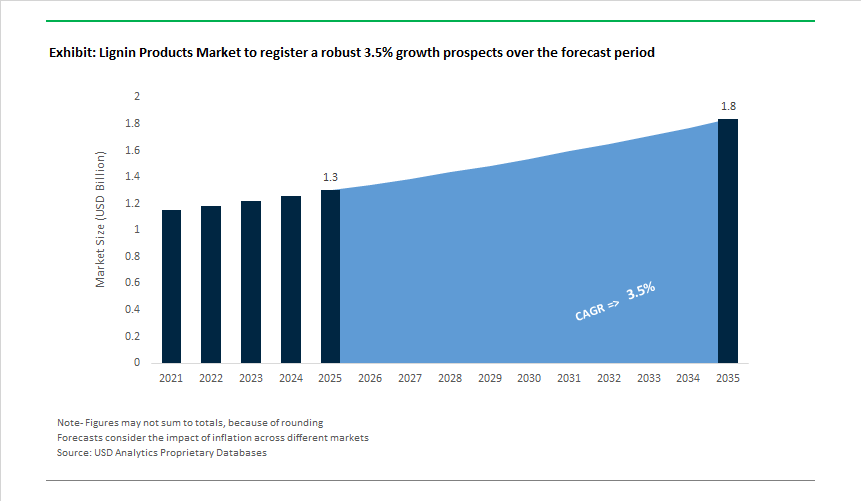

The Global Lignin Products Market is standing at USD 1.3 billion in 2025 and is projected to reach USD 1.8 billion by 2035, expanding at a 3.5% CAGR as lignin transitions from an under-monetized pulping byproduct into a strategically relevant bio-based materials platform. Today, lignin is not constrained by availability; it is constrained by purity, consistency, and application readiness, which is where the market’s real upside is forming.

The fundamental market asymmetry is clear. More than 50 million tonnes of kraft lignin are generated annually, yet less than 5% is valorized into products, with the remainder burned for low-efficiency process energy. This creates one of the largest untapped bio-material feedstock pools in the global chemicals ecosystem. As carbon intensity, petrochemical exposure, and Scope 3 emissions become procurement constraints, lignin is increasingly being evaluated not as waste, but as a low-cost, low-carbon aromatic polymer substitute.

Demand growth is being driven by performance-linked substitution, not sustainability signaling alone. In construction, lignosulfonates are structurally embedded as concrete plasticizers, reducing water demand by 5-15% and enabling lower cement usage per cubic meter-an outcome that directly lowers embodied CO₂ and material cost. In wood adhesives and engineered panels, modified lignin-based phenolic resins are now replacing 30-50% of phenol without compromising bond strength or durability, addressing both cost volatility and regulatory pressure on formaldehyde and fossil-derived inputs.

A higher-value inflection point is forming around materials and advanced manufacturing. Kraft lignin is increasingly evaluated as a carbon fiber precursor, where its aromatic backbone offers a pathway to 25-40% cost reduction versus PAN-based carbon fiber. While still emerging, this application is strategically significant because it expands carbon fiber from aerospace-limited volumes into automotive, wind energy, and infrastructure-scale composites, where cost has historically been prohibitive.

Parallel to bulk applications, high-purity lignin streams are reshaping the specialty end of the market. Organosolv and advanced-fractionated lignins, with purity levels exceeding 90% and minimal sulfur content, are being specified for high-performance resins, polymer blends, dispersants, and pharmaceutical excipients. These segments are growing at >20% year-on-year, albeit from a smaller base, and command materially higher margins due to tighter specifications and qualification barriers. Here, lignin competes not on price alone, but on functional performance and lifecycle carbon advantage versus petrochemical analogues.

From a strategic standpoint, value creation in the lignin products market is increasingly governed by process integration and downstream customization. Producers that control feedstock consistency, sulfur reduction, molecular weight distribution, and formulation capability are moving up the value chain. Investments in fractionation, organosolv processing, and application-specific modification are proving far more decisive than sheer lignin volume access.

Market Analysis: Pilot Plants, Strategic Partnerships and Cost Breakthroughs Accelerate Lignin Valorization

Lignin valorization moved from laboratory promise to demonstrable commercial pilots and strategic investments. In December 2024, Metsä Group launched Metsä LigO from its Äänekoski demo plant - a high-performance lignin product targeted at replacing fossil chemicals in concrete admixtures - signalling early commercial readiness for construction-grade applications. November 2024 saw multiple North American and European moves: Ingevity announced a capital investment to expand chemically modified Kraft lignin production for oil-well dispersants and industrial dispersants, while Mercer inaugurated Europe’s first Kraft lignin pilot plant in Rosenthal, underscoring cross-regional capital flows into lignin separation and scale-up efforts. In September 2024, UPM and Södra formed a partnership to advance next-generation lignin-based resins, with UPM as a key offtaker for Södra’s planned large-scale Kraft lignin facility (expected start-up 2027) - a clear example of supply-chain alignment between producers and end-users.

Commercialization momentum continued into 2025 with technology and market diversification. In July 2025, an EU consortium reported a cost breakthrough in lignin-to-vanillin bioconversion, reducing unit costs by ~40% versus petroleum routes and expanding the addressable chemical space for lignin-derived aromatics. June 2025 marked Rayonier Advanced Materials’ pilot plant inauguration focused on extracting high-purity lignin for carbon-fiber precursors and high-end polymers, while April 2025 saw a major pulp producer launch lignin-based microparticles for UV protection in coatings and sunscreens - an early signal that lignin chemistry can enter higher-margin specialty markets. Regulatory and policy moves also matter: March 2025 China published standards encouraging lignosulfonate use in large infrastructure projects, creating an institutional demand channel that can rapidly scale uptake in concrete admixtures.

Lignin Products Market Trends and Opportunities

Trend 1: Commercialization of Lignin as a Formaldehyde-Free Binder in Wood Panels

The construction and engineered wood products industry is undergoing a structural shift toward lignin-based binders as regulatory pressure, indoor air quality standards, and ESG reporting requirements converge. Traditional phenol-formaldehyde (PF) and urea-formaldehyde resins are increasingly misaligned with upcoming legislation in Europe and North America, particularly as 2026 formaldehyde emission thresholds tighten for residential and public buildings. Against this backdrop, lignin—abundantly available as a by-product of the pulp and paper industry—is emerging as a commercially viable, drop-in replacement rather than an experimental bio-alternative. This transition has moved decisively into industrial reality. In July 2025, Stora Enso confirmed the full-scale deployment of its NeoLigno® binder across mineral wool insulation and particleboard production, demonstrating that lignin-based systems can be cost-neutral while delivering meaningful process advantages. One of the most significant operational benefits is lower curing temperatures—typically 20–30°C below PF resins—which directly reduces energy consumption and improves throughput at panel manufacturing lines. Regulatory compliance is another critical driver. Lignin-based adhesives such as UPM’s WISA-BioBond are consistently achieving EN 717-1 (E1) and CARB Phase 2 compliance well ahead of enforcement deadlines, providing manufacturers with long-term market access and de-risking export strategies. Importantly, 2025 performance data confirms that modern lignin binders now match or exceed PF resins in moisture resistance and biological durability, enabling their use in exterior-grade OSB and plywood. This eliminates the need for dual-resin systems and simplifies supply chains, positioning lignin binders as a structural solution rather than a niche green material.

Trend 2: Industrial Scale-Up of Lignin-Derived Polyols for Polyurethane Systems

The chemical industry is rapidly revaluing lignin as a functional aromatic feedstock for polyurethane (PU) foams, particularly in insulation and construction applications where fire performance and thermal stability are critical. Unlike aliphatic bio-based alternatives, lignin’s inherently aromatic structure closely mirrors fossil-derived polyols, allowing it to integrate into existing PU formulations with fewer performance trade-offs. This shift has gained significant momentum with the commissioning of world-scale biorefineries. In December 2025, UPM Biochemicals reached a major milestone at its €1.27 billion Leuna biorefinery in Germany, the first commercial facility globally designed to convert wood into biochemicals at scale. The plant has begun industrial separation of lignin streams for Renewable Functional Fillers and lignin-based polyols, supporting a combined biochemical output of roughly 220,000 tonnes annually. On the formulation side, recent research from the Center for Bioplastics and Biocomposites shows that up to 40 wt% lignin-based polyols can now be incorporated into rigid and semi-flexible PU foams without compromising compressive strength or thermal conductivity. These systems achieve λ-values and mechanical properties comparable to fossil-based benchmarks while reducing the embedded carbon footprint of insulation products by more than 25%. Fire performance further strengthens lignin’s value proposition. Pilot-scale testing in 2025 demonstrated that PU foams synthesized via oxypropylated Kraft lignin exhibit significantly lower peak heat release rates, enabling manufacturers to reduce reliance on costly halogenated flame retardants. This combination of scale, performance parity, and inherent fire resistance is positioning lignin-derived polyols as a core building block for next-generation, low-carbon insulation materials.

Opportunity 1: Lignin-Based Carbon Fiber Precursors for Automotive Lightweighting

The automotive industry’s push toward electrification and vehicle lightweighting is opening a high-impact opportunity for lignin-based carbon fiber (LCF) as a cost-disruptive alternative to polyacrylonitrile (PAN). Carbon fiber demand is accelerating as OEMs seek to offset the mass of battery packs in electric vehicles, yet PAN-based fibers remain constrained by high costs, complex supply chains, and fossil feedstock dependence. Lignin offers a structurally compelling alternative due to its high carbon content and aromatic backbone, aligning well with carbon fiber conversion pathways. This potential is now being actively supported by public funding and industrial partnerships. In August 2024, the U.S. Department of Energy allocated $54.4 million toward carbon management and biomass-to-materials programs, explicitly targeting lignin conversion into structural materials to support net-zero transport goals. Academic and industrial reviews published in mid-2025 indicate that lignin-based precursors could reduce carbon fiber production costs by 30–50%, provided challenges around melt-spinning stability are addressed. Recent breakthroughs in blending lignin with compatible polymers have significantly improved spinnability, bringing the industry closer to the $15/kg cost threshold required for mass-market automotive adoption. On the supply side, major pulp producers such as Suzano and West Fraser are increasingly collaborating with automotive OEMs to supply Kraft lignin for pilot-scale fiber production. These lignin-derived fibers are currently being qualified for non-structural components—including seat frames, interior reinforcements, and battery enclosures—where weight reduction directly translates into extended EV range. As process yields improve, lignin-based carbon fiber is positioned to evolve from an R&D initiative into a strategic materials platform for the automotive sector.

Opportunity 2: Lignin Sulfonates as Bio-Based Dispersants in Lithium-Ion Battery Manufacturing

Lithium-ion battery manufacturing represents a fast-emerging downstream opportunity for lignin sulfonates, particularly as the industry seeks sustainable, low-cost alternatives to synthetic dispersants and binders. The shift toward high-silicon and silicon-carbon composite anodes has amplified the need for dispersants that can tolerate extreme volume expansion—often exceeding 300%—without compromising electrode integrity. Research published in October 2025 confirms that modified lignosulfonates perform exceptionally well in this role, maintaining slurry homogeneity and mechanical cohesion over extended cycling. Unlike conventional PVDF-based systems, lignin-derived dispersants exhibit greater elasticity, allowing electrodes to accommodate silicon expansion without cracking or delamination. From a manufacturing perspective, the economics are equally compelling. Substituting synthetic dispersants with lignin sulfonates can reduce electrode slurry preparation costs by 10–15%, while simultaneously improving sustainability metrics. This is increasingly important as the EU Battery Regulation (2025/2026) mandates detailed carbon footprint disclosures across the battery value chain. Lignin-based inputs offer a direct pathway to lower Scope 3 emissions. Processing advantages further reinforce adoption potential. Lignosulfonates are inherently water-soluble, enabling aqueous electrode processing and significantly reducing dependence on NMP, a toxic solvent under growing regulatory scrutiny from both the EPA and ECHA. As battery manufacturers accelerate dry and water-based electrode technologies, lignin sulfonates are emerging but as an enabling material for next-generation, compliant battery manufacturing lines.

Market Share Analysis: Lignin Products Market

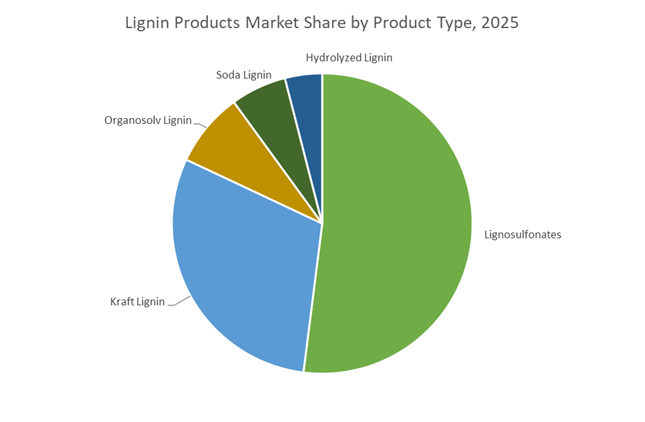

Market Share by Product Type: Lignosulfonates Cement Their Lead as the Default Bio-Based Dispersant

Lignosulfonates command approximately 52% of the global lignin products market because they sit at the intersection of scale, functionality, and immediate substitutability for fossil-based dispersants. Unlike emerging lignin derivatives that require downstream chemical modification, lignosulfonates are inherently water-soluble and deployable “as-is,” which explains their continued dominance despite innovation elsewhere. Global supply leadership from Borregaard, with over 1.1 million metric tons of annual capacity, has structurally anchored this segment by ensuring consistent quality and multi-region availability—two non-negotiables for construction, agriculture, and chemicals buyers. The commercial value proposition has sharpened in 2025 as producers pivot toward high-purity, low-sugar lignosulfonates, unlocking 20–30% price premiums while meeting stricter performance and residue requirements. Performance data from Sappi and Borregaard confirms that modern lignosulfonates can deliver up to 30% water reduction in concrete, directly lowering cement usage—the largest cost and carbon contributor in construction mixes. This ability to couple cost savings with emissions reduction is the core reason lignosulfonates still account for over 90% of revenue within water-soluble lignins, reinforcing their role as the market’s cash-flow engine rather than a legacy product at risk of displacement.

Market Share by Application: Construction & Infrastructure Anchor Demand Through Low-Carbon Concrete Economics

Construction and infrastructure represent around 38% of total lignin product demand, making it the largest application segment by value, driven by the urgency to decarbonize concrete without sacrificing mechanical performance or project timelines. Lignin-based admixtures have become the most economical route for developers to achieve LEED and BREEAM compliance, particularly in high-volume public infrastructure programs across Asia-Pacific. The lignin-concrete admixtures market alone is valued at approximately USD 4.7 billion in 2025, underpinned by smart-city and transport investments in India and China. Performance benchmarks from Stora Enso and peer-reviewed 2025 studies show 15–20% improvements in compressive strength, enabling thinner structural elements and lower overall material intensity—an efficiency gain that resonates strongly with EPC contractors. The commercial inflection point came in 2025 when large industrial developers validated lignin at scale; Meta reported 43% faster strength gain and 35% carbon reduction using lignin-optimized concrete mixes for data center construction, reframing lignin as a speed-to-market enabler. Combined with the rapid adoption of lignin as a bitumen replacement in asphalt—where it can displace up to 50% of fossil inputs—construction has become the demand stabilizer that secures lignin’s long-term market share.

Competitive Landscape: Integrated Pulp Players and Specialty Chemistries Lead Lignin Commercialization

The competitive field is led by vertically integrated pulp and paper companies and specialty chemistry firms that convert pulping byproducts into specification-grade lignin streams. Leaders combine feedstock control, fractionation expertise, and downstream application development (resins, dispersants, carbon precursors). Companies that can supply consistent, low-sulfur lignin with tailored molecular-weight distributions will dominate early industrial markets.

Borregaard ASA - Specialty Lignosulfonate and Dispersant Leader With Diversified Bio-Chemical Portfolio

Borregaard derives the majority of revenue from wood-based specialty biochemicals and is a leading supplier of advanced lignosulfonates for oil-well drilling, construction admixtures, and battery dispersants. The company invests across wood-derived nanomaterials (e.g., Exilva MFC) and holds patents on modified lignosulfonates for thermal paper and textile dye dispersants - assets that support high-value, specification-driven market penetration. Borregaard’s use of sustainably managed forest feedstock and its focus on product consistency position it to capture demand where regulatory and quality standards are strict.

Stora Enso Oyj - Industrial Kraft Lignin Scale and Phenol-Substitution Capability

Stora Enso operates one of the world’s largest industrial Kraft lignin separation plants (Sunila, Finland) with ~50,000 t/year capacity of Lineo lignin powder. The company has demonstrated the commercial feasibility of replacing up to 50% of phenol in plywood adhesives and is actively developing lignin-derived carbon materials and anode precursors for sodium-ion batteries. Stora Enso’s scale, commercial supply agreements in construction and chemicals, and experience in large-volume lignin handling make it a critical supplier for high-volume lignin valorization pathways.

Ingevity Corporation - Chemically Modified Kraft Lignin Specialist Focused On Dispersants and Oilfield Chemistry

Ingevity is a North American leader in chemically modified lignosulfonates and Kraft lignin derivatives, historically serving oilfield drilling fluid and industrial dispersant markets. Its process optimizations target tight molecular-weight distributions for predictable performance in concrete admixtures and drilling fluids. Ingevity’s expansion investments reflect a strategy to broaden lignin applications into asphalt binders, agricultural encapsulants, and other infrastructure markets where formulation control and supply reliability matter.

Nippon Paper Industries - Asian Pulp Major Advancing High-Purity Lignin Biomaterials

Nippon Paper is leveraging large pulp positions to diversify into lignin-derived phenolics and polymer intermediates, developing bio-based phenol and aromatic monomers to displace petrochemical feedstocks. The company’s focus on organosolv and high-purity lignin streams targets electronics and advanced polymer matrices, while its work on lignin-based polyurethane foams indicates a commercial push into insulation and automotive materials. Collaboration with Japanese universities accelerates R&D for lignin electrolytes and separators for next-gen energy storage.

Rayonier Advanced Materials (RYAM) - High-Purity Lignin Extraction and Tailored Fractionation For Specialty Markets

Rayonier Advanced Materials is known for producing high-purity lignin streams with low ash and sulfur, ideal for demanding applications such as vanillin synthesis, carbon fibre precursors, and specialty bioplastics. RYAM invests in advanced fractionation to supply lignin by tailored molecular-weight range, enabling custom feedstocks for resins and coatings. Its pilot plant (June 2025) underscores a push to commercialize high-value lignin derivatives that command premium pricing versus bulk lignosulfonates.

Germany has emerged as the European epicenter for industrial-scale lignin valorization, moving decisively beyond pilot concepts toward fully commercialized bio-based chemical production. The defining milestone is UPM’s Leuna Biorefinery, which reached stable operations in December 2025. As the world’s first industrial-scale wood-based biorefinery capable of efficiently separating lignin from sugars, Leuna establishes a new benchmark for high-purity kraft lignin extraction, a prerequisite for downstream chemical consistency and pricing power. This capability directly supports the production of Renewable Functional Fillers (RFF) designed to replace fossil-derived carbon black and silica in rubber and plastics—applications with stringent performance requirements.

Strategically, Germany’s lignin momentum is tightly aligned with EU Green Deal industrial decarbonization goals, particularly within the automotive, tire, and specialty polymer supply chains. Once fully ramped, the Leuna site is expected to produce 220,000 tonnes of advanced biochemicals annually, positioning Germany not merely as a technology innovator but as a volume supplier of bio-based lignin derivatives. The country’s emphasis on chemical-grade purity and integration with existing petrochemical clusters gives it a structural advantage over regions still focused on energy-grade lignin utilization.

Finland – Battery-Grade Lignin and Hard Carbon Leadership

Finland is defining the highest-value frontier of the lignin products market by commercializing lignin-derived materials for lithium-ion battery anodes. The centerpiece of this strategy is Stora Enso’s Lignode® platform, which converts sustainably sourced lignin into hard carbon, offering a renewable alternative to synthetic graphite. At its November 2025 Capital Markets Day, Stora Enso positioned biomaterials as a core growth engine, signaling that battery-grade lignin is no longer experimental but central to long-term capital allocation.

Finland’s advantage lies in system-level mill optimization, with over 30% of its 2.5 million tonnes of pulp capacity already channeled into value-added applications. Facilities such as Varkaus and Heinola are being fine-tuned to improve lignin yield and extraction economics, lowering barriers to scale. Complementing corporate investment, Business Finland–backed research consortia are targeting selective lignin bond cleavage to unlock aromatic chemicals, reinforcing Finland’s role as the global innovation hub for electrochemical and battery-focused lignin applications.

Norway – Premium Lignosulfonates and ESG-Driven Demand

Norway continues to dominate the specialty lignin segment, where performance consistency and regulatory credentials outweigh sheer volume. Borregaard, one of the world’s most advanced biorefineries, reported NOK 1,799 million in Q3 2025 revenues, underpinned by growing demand for high-purity lignosulfonates in pharmaceuticals, nutraceuticals, construction admixtures, and specialty adhesives. These products command premium pricing due to their narrow molecular weight distributions and stringent impurity control.

Equally critical is Norway’s ESG leadership, which has become a commercial differentiator rather than a branding exercise. Borregaard’s EcoVadis Gold rating and recognition among Time Magazine’s World’s Most Sustainable Companies are increasingly used to secure long-term offtake agreements with European construction and healthcare customers. The NOK 100 million commercial paper issuance in December 2025, earmarked for lignin portfolio optimization, underscores Norway’s strategy of deepening value per ton rather than expanding low-margin output.

Brazil – Volume-Driven Kraft Lignin Potential from Eucalyptus

Brazil represents the volume-growth pillar of the global lignin products market, underpinned by unparalleled hardwood forestry scale. Suzano’s R$490 million Limeira investment, which came online in December 2025, expanded fluff pulp capacity by 400% to 440,000 tonnes per year, dramatically increasing the availability of lignin-rich side streams. While current utilization remains focused on pulp and hygiene products, the scale of Suzano’s operations positions Brazil as a future anchor supplier of kraft lignin for global markets.

Suzano’s Nature Strategy, reinforced at COP30, explicitly targets side-stream valorization, and improved Q3 2025 cash costs have created financial headroom for advanced lignin extraction technologies between 2026 and 2030. Unlike Europe’s purity-driven model, Brazil’s competitive edge lies in low-cost, high-volume lignin recovery from eucalyptus, making it a natural supplier for construction binders, asphalt modifiers, and bulk bio-based materials where price elasticity is critical.

United States – Circular Supply Chains and Energy-Linked Lignin Pathways

The United States is integrating lignin into its circular economy and energy security frameworks, rather than positioning it solely as a specialty chemical. Through multiple U.S. Department of Energy Funding Opportunity Announcements (2025–2026), lignin has been explicitly prioritized as a feedstock for sustainable fuels, renewable propane, and advanced vehicle materials. Programs such as the SPARC initiative signal federal intent to move lignin beyond internal mill combustion toward commercial chemical conversion.

On the industrial side, Smurfit Westrock—following its merger—reported $8.0 billion in Q3 2025 net sales, with a strategic reassessment of lignin use across its North American mills. The gradual shift from energy recovery to commercial lignin extraction reflects a broader U.S. trend: monetizing biomass streams to strengthen domestic supply chains for low-carbon fuels and chemicals, particularly in transport and heavy industry.

Canada – Policy-Led Demand for Lignin-Based Wood Chemistry

Canada’s lignin strategy is being shaped decisively by federal procurement and industrial resilience policy. Under Budget 2025, the government allocated $186 million to implement the “Buy Canadian” policy, explicitly favoring domestically produced wood products and biochemicals. This creates a captive demand base for lignin-based adhesives, binders, and resins used in plywood, engineered wood, and cross-laminated timber (CLT).

The policy direction is reinforced by Prime Minister Mark Carney’s 2025 measures to modernize the softwood lumber industry through side-stream valorization, accelerating the replacement of fossil-based urea-formaldehyde resins with lignin-derived alternatives. Complementary funding via the Canada Fund for Local Initiatives supports decentralized biomass processing, positioning Canada as a policy-driven growth market for construction-grade lignin applications rather than export-led commodity supply.

2025 Strategic Matrix: Lignin Products National Comparison

Lignin Products National Matrix

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

Germany

|

Industrial scaling

|

Leuna biorefinery stable operations

|

Renewable functional fillers (rubber, plastics)

|

|

Finland

|

Battery innovation

|

Lignode® hard carbon optimization

|

Li-ion battery anodes

|

|

Norway

|

Specialty chemicals

|

NOK 1,799M Q3 revenue / NOK 100M financing

|

High-purity lignosulfonates

|

|

Brazil

|

Volume leadership

|

R$490M Limeira fluff pulp expansion

|

Kraft lignin from eucalyptus

|

|

United States

|

Circular supply chains

|

DOE SPARC & circularity grants

|

Bio-based fuels & vehicle materials

|

|

Canada

|

Industrial resilience

|

$186M Buy Canadian policy

|

Lignin resins for wood products

|

Lignin Products Market Report Scope

Lignin Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2035)

|

$1.8 Billion

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Product Type (Lignosulfonates, Kraft Lignin, Organosolv Lignin, Soda Lignin, Hydrolyzed Lignin), By Application (Construction, Energy Storage, Agriculture, Industrial Chemicals, Advanced Materials, Food & Flavors, Pigments), By End-User Industry (Construction & Infrastructure, Automotive & Transportation, Packaging & Consumer Goods, Electronics, Chemicals & Pharmaceuticals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Borregaard ASA, UPM-Kymmene Corporation, Stora Enso Oyj, Metsä Group (Metsä Fibre), Domsjö Fabriker AB (Aditya Birla Group), Nippon Paper Industries Co. Ltd., Changzhou Shanfeng Chemical Industry Co. Ltd., Burgo Group S.p.A., LignoTech Florida, The Dallas Group of America, GreenValue S.A., CH-Bioforce Oy, WestRock Company, Suzano S.A., Ingevity Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lignin Products Market Segmentation

By Product Type

- Lignosulfonates

- Kraft Lignin

- Organosolv Lignin

- Soda Lignin

- Hydrolyzed Lignin

By Application

- Construction

- Energy Storage

- Agriculture

- Industrial Chemicals

- Advanced Materials

- Food & Flavors

- Pigments

By End-User Industry

- Construction & Infrastructure

- Automotive & Transportation

- Packaging & Consumer Goods

- Electronics

- Chemicals & Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Lignin Products Market

- Borregaard ASA

- UPM-Kymmene Corporation

- Stora Enso Oyj

- Metsä Group (Metsä Fibre)

- Domsjö Fabriker AB (Aditya Birla Group)

- Nippon Paper Industries Co., Ltd.

- Changzhou Shanfeng Chemical Industry Co., Ltd.

- Burgo Group S.p.A.

- LignoTech Florida

- The Dallas Group of America

- GreenValue S.A.

- CH-Bioforce Oy

- WestRock Company

- Suzano S.A.

- Ingevity Corporation

*- List not Exhaustive