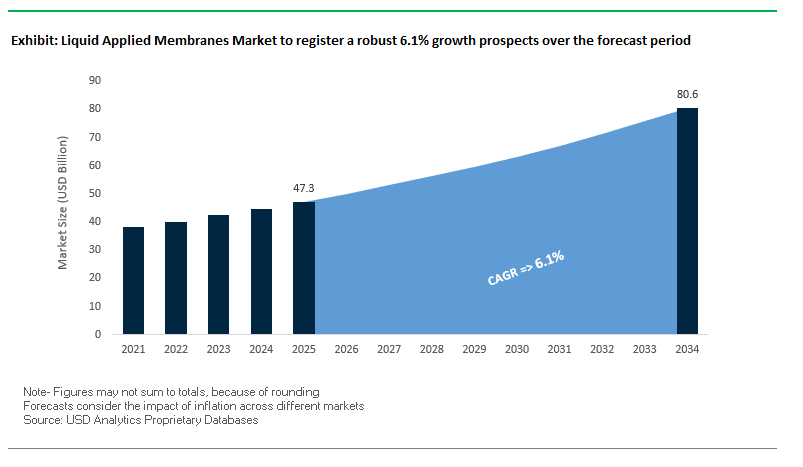

Liquid Applied Membranes Market Overview: Seamless Waterproofing Solutions Gaining Ground (MV: USD 47.3 Bn in 2025 → USD 80.6 Bn by 2034, CAGR 6.1%)

The global liquid applied membranes (LAMs) market is experiencing strong growth, driven by its adaptability, sustainability credentials, and efficiency benefits over traditional sheet-based solutions. Unlike pre-formed membranes, LAMs create a seamless, monolithic waterproof barrier, making them particularly effective for complex geometries, penetrations, and irregular surfaces where seams often become points of failure. This performance advantage is a major reason for their widespread adoption in both new construction and retrofit projects.

Refurbishment and renovation are critical growth drivers. A significant share of demand stems from retrofit applications, where LAMs can be applied directly over aged substrates like old bitumen or concrete. This eliminates the need for complete tear-offs, reducing cost and downtime while extending structural lifespan. In addition, sustainability is at the forefront of industry growth, with water-based and solvent-free formulations gaining market share as green building standards and regulations tighten. The push for low-VOC solutions aligns LAMs with LEED and other certification systems, making them the preferred choice in urban and regulated markets.

Rapid curing is another performance trend reshaping adoption. Advanced polyurethane, hybrid polyurea, and one-component systems are designed for faster installation and rain resistance within hours, ensuring minimal disruption on time-sensitive projects. This feature makes LAMs particularly attractive for commercial roofs, balconies, and infrastructure where downtime costs are high.

Key Insights for Industry Professionals

- Seamless Waterproofing Advantage: Monolithic layers eliminate seams, reducing water ingress risks.

- Retrofit-Driven Demand: Widely used for overlays on old surfaces, cutting project costs and time.

- Sustainability Factor: Water-based, solvent-free, and low-VOC membranes align with green building codes.

- Efficiency Gains: Rapid curing systems enable rain resistance and walkability within hours of application.

Market Analysis: Recent Industry Developments Shaping the Future of LAMs

The liquid applied membranes market has been marked by a wave of product launches and investments in 2025, highlighting the focus on performance, sustainability, and capacity expansion. In August 2025, Sika AG introduced new polyurethane-based waterproofing membranes with enhanced water ponding resistance for flat roofs, addressing one of the key failure points in traditional coatings. Also in August, BASF SE launched its Acronal® binder technology for cementitious waterproofing, designed to deliver flexibility, crack-bridging, and mechanical strength. Around the same time, Dow debuted an ultra-low VOC acrylic polymer for waterproofing, expanding sustainable solutions for wet rooms and balconies, while RPM International’s Tremco Roofing rolled out a fluid-applied roofing system engineered to extend the life of low-slope roofs without full replacement.

Earlier in June 2025, 3M Company launched an upgraded Air and Vapor Barrier 3015NP, featuring primer-free installation that reduces labor costs by up to 40%. Mallard Creek Polymers, in April 2025, unveiled three new emulsion polymers under its BarrierPro® line, enhancing adhesion, cold-weather flexibility, and crack-bridging performance. In February 2025, Sika further strengthened its footprint in Latin America with a new manufacturing facility in Mexico, increasing production capacity for LAMs and construction chemicals.

Emerging Trends and Strategic Opportunities in the Liquid Applied Membranes Market

Accelerated Adoption of Silicone-Based LAM for Reflective, Durable Roofing

The liquid applied membranes (LAM) market is witnessing strong adoption of silicone-based coatings driven by demand for energy-efficient and durable building envelopes. Silicone membranes provide superior UV resistance and long-term elasticity, enabling service lives of 10–20 years with minimal maintenance, as noted in technical studies. Their high solar reflectivity, reflecting 80–90% of UV rays, contributes to reduced urban heat island effects and lowers cooling costs by 7–15% in commercial buildings. Unlike other materials, silicone resists ponding water, preventing moisture-related degradation and leaks on flat roofs. The energy-saving and reflective properties of silicone membranes also support compliance with green building standards, such as LEED credits, helping construction projects align with corporate sustainability goals. These performance attributes make silicone-based LAM a preferred solution for modern commercial roofing applications.

Integration of Digital Monitoring and IoT Sensors within Waterproofing Systems

Liquid applied membranes are evolving into intelligent waterproofing solutions with the integration of digital monitoring and IoT sensor technologies. Systems such as SikaRoof® Monitoring employ sensor grids to detect and locate water ingress in real-time, enabling targeted maintenance and reducing labor costs associated with manual leak detection. This proactive monitoring is crucial for high-value assets like data centers and historical buildings, preventing water damage that could result in millions of dollars in losses. Insurance providers are increasingly offering premium discounts for properties equipped with leak detection, recognizing reduced risk exposure. Real-time monitoring not only safeguards critical assets but also enhances the longevity of building envelopes by addressing potential issues before they escalate, positioning IoT-enabled LAM as a transformative solution for asset protection and cost-efficient building maintenance.

Development of Spray-Applied LAM for Rapid Bridge Deck Rehabilitation

The need for rapid rehabilitation of aging transportation infrastructure presents a significant growth opportunity for spray-applied LAM. Polyurea-based systems, such as PPG’s Bridge Deck Membrane, offer rapid curing times—accepting asphalt overlays within an hour and functioning even in temperatures as low as −29°C—allowing bridges to return to service quickly and minimizing traffic disruption. Spray-applied membranes provide seamless, monolithic coverage over complex geometries, bolt heads, and penetrations, preventing water and deicing salts from reaching structural elements. These systems exhibit superior adhesion, crack-bridging capability, and proven performance in extreme conditions, extending the lifespan of bridge decks while reducing long-term maintenance costs. Such advantages position spray-applied LAM as a high-value solution for infrastructure resilience and operational efficiency.

Formulation of Bio-Based and Circular Raw Materials for Sustainable LAM

Sustainability is becoming a key driver in LAM innovation, with opportunities to develop membranes using bio-based polymers and recycled materials. Companies like Derbigum are producing roofing membranes with up to 20% recycled content, contributing to reduced virgin material use and lower CO2 emissions. Research into bio-based polymers from renewable feedstocks such as vegetable oils and tall oil supports the circular economy while maintaining critical waterproofing and elasticity properties. Closed-loop recycling initiatives enable old roofing materials to be reprocessed into new membranes, creating sustainable material cycles. Additionally, green chemistry approaches are applied to minimize hazardous constituents and environmental impact throughout the product lifecycle, making sustainable LAM a compelling option for eco-conscious construction projects.

Competitive Landscape: Leading Companies in the Global Liquid Applied Membranes Industry

The competitive environment is shaped by chemical giants and construction specialists leveraging innovation, global networks, and sustainability to maintain leadership in the LAMs market.

Sika AG: Expanding Polyurea and Polyurethane Systems for Superior Performance

Sika remains a market leader with its Sikalastic® portfolio, covering polyurethane, polyurea, and cementitious LAMs. Its recent two-component polyurea hybrid technology for hand-applied systems has broadened access to high-performance membranes in small-scale and renovation projects. By emphasizing cool roof solutions and vapor-permeable membranes, Sika is aligning with energy efficiency and sustainability trends. With a robust manufacturing footprint, including its new Mexico facility (Feb 2025), Sika’s end-to-end solutions ensure compatibility and long-term performance.

BASF SE: Driving Sustainability with Hybrid Binder Technology

BASF plays a key role in enabling high-performance waterproofing via its dispersions and additives portfolio. Its Acronal® Xpress hybrid binders, introduced in August 2025, deliver faster curing, flexibility, and strength while remaining low-VOC and APEO-free. BASF’s strategy is tightly aligned with eco-friendly construction practices, enabling its customers to produce durable, high-performance membranes that comply with global green standards.

Dow Chemical Company: Advancing Acrylic Emulsion Waterproofing Systems

Dow continues to innovate in liquid waterproofing with its PRIMAL™ dispersions and new ultra-low VOC acrylic polymer launched in July 2025. Its formulations are valued for adhesion, elongation, and crack-bridging in wet rooms, balconies, and below-grade structures. Dow’s emphasis on environmentally responsible products positions it as a preferred partner for contractors and developers focused on long-lasting, low-odor solutions.

RPM International Inc.: Strengthening Retrofit and Fluid-Applied Roofing Solutions

Through subsidiaries like Tremco, RPM delivers fluid-applied roofing systems engineered for cost-efficient retrofits. In July 2025, Tremco launched a new low-slope roofing system, highlighting RPM’s role in extending the lifecycle of aging roofs. By combining technical support with sustainable formulations, RPM provides comprehensive retrofit solutions that reduce lifecycle costs and improve resilience.

3M Company: Innovating with Primer-Free Air and Vapor Barriers

3M leverages its expertise in adhesives and polymer science to deliver advanced air and vapor barriers that complement liquid-applied waterproofing systems. Its 3015NP barrier upgrade in June 2025 showcases innovation in installation efficiency, offering primer-free adhesion and saving up to 40% in labor. 3M’s strategic focus on energy-efficient, conformable, and self-sealing membranes ensures that it continues to play a vital role in the building envelope and waterproofing market.

Liquid Applied Membranes Market Share Insights

Elastomeric Membranes Dominate Market Share by Type in the Liquid Applied Membranes Industry

Elastomeric membranes account for the largest 45.3% share of the liquid applied membranes (LAM) industry in 2025, underscoring their dominance in modern waterproofing. Polyurethane- and acrylic-based elastomeric systems are valued for their high elasticity (often >200%), which allows them to bridge cracks and withstand thermal cycling, making them indispensable for rooftops, podiums, and exposed structures where movement is inevitable. This performance edge, combined with the ability to provide seamless, joint-free waterproofing, has made elastomerics the preferred solution for high-spec commercial and residential projects. Bituminous membranes maintain a strong position due to cost-effectiveness and proven reliability, particularly in below-grade applications such as basements and foundations, while cementitious coatings occupy a stable niche in water-retaining structures like tanks and swimming pools. The “others” category, comprising silicone-based and hybrid polymer technologies, represents the innovation frontier, offering VOC-free, high-reflectivity, and extreme-weather-resistant solutions. Collectively, the segmentation illustrates how elastomeric membranes lead on versatility and durability, while bituminous and cementitious products anchor traditional and specialized markets.

Commercial Construction Leads Market Share by End-Use in the Liquid Applied Membranes Industry

Commercial construction holds the largest 35.6% share of end-use in the LAM industry, reflecting the vast demand from high-rise offices, malls, healthcare facilities, and hotels where durability and lifecycle performance are critical. These projects prioritize elastomeric membranes for their longevity, seamless application, and contribution to energy efficiency via cool roof technologies. Residential construction follows closely at 30%, fueled by global urbanization and multi-unit housing developments, where balconies, basements, and terraces increasingly rely on user-friendly elastomeric and cementitious systems instead of traditional bituminous solutions. Public infrastructure is the most performance-intensive application, with membranes deployed in bridges, tunnels, and reservoirs to protect critical assets over decades, driving demand for both high-spec elastomerics and bituminous systems. Industrial end-use is a smaller but high-value segment, focused on chemical resistance, abrasion resistance, and oil impermeability in manufacturing plants and chemical storage areas. Emerging “other” applications in transportation and agriculture demonstrate the adaptability of LAM technology beyond conventional construction. This end-use distribution highlights how commercial and residential projects dominate by volume, while infrastructure and industrial sectors push the envelope on technical specifications.

United States Liquid Applied Membranes Market Expands With Low-VOC Innovations and Infrastructure Demand

The U.S. liquid applied membranes market is shaped by a fragmented regulatory environment, with EPA guidelines and state-level air quality boards driving the adoption of low-VOC and water-based formulations. Compliance with the International Building Code (IBC) and local building codes ensures that liquid applied membranes meet stringent waterproofing and structural integrity standards for residential, commercial, and infrastructure projects.

Technological advancements, including self-healing membranes and hybrid systems that combine polyurethane and acrylic chemistries, are meeting diverse construction requirements. Corporate investments are notable, such as GCP Applied Technologies’ Integritank system, applied in major tunnel projects in Mexico, highlighting U.S. expertise in large-scale infrastructure. Strong demand is seen in commercial buildings, bridges, and parking structures, driven by public and private retrofitting initiatives. Sustainability remains a key driver, with bio-based, low-VOC, and reflective “cool roof” membranes reducing energy consumption and promoting eco-friendly construction practices.

Germany Leads in High-Performance Liquid Applied Membranes Through Digital Innovation and Circular Economy Practices

Germany’s LAMs market benefits from a stringent regulatory framework that promotes sustainability indirectly through initiatives like the EU Packaging and Packaging Waste Regulation (PPWR). Industry 4.0 initiatives are driving high-performance membrane formulations, including PMMA (polymethyl methacrylate) membranes that provide rapid curing and cold-weather durability.

Germany’s established recycling and sustainable construction incentives boost the adoption of eco-friendly waterproofing solutions. Companies like Ardex are strategically investing in new technologies to expand capabilities, catering to growing demand for durable, sustainable, and high-performance liquid applied membranes in both new construction and infrastructure renovation projects. The focus on green building and energy-efficient waterproofing solutions positions Germany as a global leader in advanced LAM technologies.

China Liquid Applied Membranes Market Grows With Green Initiatives and Infrastructure Mega Projects

China’s LAMs industry is strongly influenced by the dual carbon goal and initiatives like the Action Plan for Large-Scale Equipment Updates, promoting sustainable and recycled materials in construction. Regulatory reforms such as GB/T 31268, addressing excessive packaging, indirectly influence the adoption of environmentally friendly construction materials.

Ongoing mega infrastructure projects, including Belt and Road Initiative bridges, tunnels, and metro systems, create significant demand for durable and reliable liquid applied membranes. Investments in automation, AI, and “5G plus industrial internet” technologies are enhancing production efficiency. Strategic partnerships, like Xiniupi Waterproof Technology Co., Ltd. collaborating with European firms, are developing reinforced membranes with nonwoven fabrics. The focus on domestic manufacturing and high-quality solutions is driving China’s leadership in specialized LAM applications.

India Liquid Applied Membranes Market Expands With Circular Economy and Smart City Projects

India’s LAMs market is accelerating due to the Make in India initiative and the Smart Cities Mission, creating high demand for sustainable liquid applied membranes in construction and infrastructure. Government incentives and circular economy policies are encouraging the adoption of eco-friendly waterproofing solutions.

Technological advancements are led by Pidilite Industries’ Dr. Fixit brand, offering advanced waterproofing solutions for residential, commercial, and industrial applications. Corporate investments are rising to meet demand from India’s expanding real estate, infrastructure, and industrial sectors. Key applications include high-performance waterproofing for residential buildings, commercial complexes, and chemical manufacturing facilities, aligning with global safety and durability standards.

Japan Liquid Applied Membranes Market Strengthens With Seismic-Resistant and High-Performance Solutions

Japan’s LAMs market leverages its precision manufacturing expertise to deliver next-generation waterproofing solutions capable of withstanding the country’s unique seismic and environmental challenges. Advanced technologies focus on superior material durability, barrier properties, and self-sealing membranes.

Regulatory support through sustainable construction initiatives drives demand for high-performance liquid applied membranes. Notable projects, such as Sika’s Sikalastic application on the Hoto Fudo building, demonstrate innovative deployment techniques. Japanese manufacturers are emphasizing value-added and specialty membranes to meet the stringent needs of commercial, residential, and industrial infrastructure, ensuring both functional performance and environmental sustainability.

Brazil Liquid Applied Membranes Market Accelerates With Sustainable Construction Practices and Strategic Investments

Brazil’s LAMs market is shaped by the National Solid Waste Policy, which encourages sustainable building materials and eco-friendly waterproofing solutions. Technological advancements include the development of biodegradable, recyclable, and compostable membrane solutions to reduce environmental impact.

The market is driven by growing demand in commercial, residential, and agricultural sectors, with significant corporate investments such as Henkel’s Inspiration Center for Adhesive Technologies in São Paulo, enhancing local innovation and collaboration. The EU-Mercosur trade agreement is expected to further boost market diversification, attracting domestic and international players and supporting the growth of high-performance, sustainable liquid applied membranes for modern construction projects.

Liquid Applied Membranes Market Report Scope

Liquid Applied Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$47.3 Billion

|

|

Market Size (2034)

|

$80.6 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Type (Cementitious, Elastomeric, Bituminous, Others), By Application (Roofing, Walls, Building Structures, Roadways, Others), By End-Use (Residential Construction, Commercial Construction, Industrial, Public Infrastructure, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, Mapei S.p.A., BASF SE, Carlisle Companies Inc., SOPREMA Group, Fosroc, Inc., H.B. Fuller Company, Tremco Inc., Pidilite Industries Ltd., The Dow Chemical Company, Ardex GmbH, Wacker Chemie AG, Johns Manville, Henry Company (a part of Carlisle Companies), Kemper System America, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Applied Membranes Market Segmentation

By Type

- Cementitious

- Elastomeric

- Bituminous

- Others

By Application

- Roofing

- Walls

- Building Structures

- Roadways

- Others

By End-Use

- Residential Construction

- Commercial Construction

- Industrial

- Public Infrastructure

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Liquid Applied Membranes Market

- Sika AG

- Mapei S.p.A.

- BASF SE

- Carlisle Companies Inc.

- SOPREMA Group

- Fosroc, Inc.

- H.B. Fuller Company

- Tremco Inc.

- Pidilite Industries Ltd.

- The Dow Chemical Company

- Ardex GmbH

- Wacker Chemie AG

- Johns Manville

- Henry Company (a part of Carlisle Companies)

- Kemper System America, Inc.

* List Not Exhaustive

Methodology

The research methodology for the Liquid Applied Membranes (LAMs) Market conducted by USDAnalytics integrates primary and secondary research to provide industry professionals with precise and actionable insights. Primary research involved interviews with waterproofing manufacturers, construction contractors, chemical suppliers, and technology experts to capture first-hand information on market dynamics, material innovations, installation trends, and sustainability practices. Secondary research included analysis of annual reports, government publications, regulatory guidelines, industry white papers, and technical journals to validate market trends and quantify adoption patterns. Both top-down and bottom-up approaches were employed to estimate market size, considering factors such as construction activity, retrofitting demand, regional regulations, and product innovations. Forecasting models incorporated technological advances in elastomeric, polyurethane, and silicone membranes, alongside sustainability-driven shifts toward low-VOC and bio-based materials. This methodology enables USDAnalytics to provide a comprehensive market outlook, supporting strategic decisions for stakeholders in commercial, residential, infrastructure, and industrial applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.