Liquid Thickeners Market 2025–2034: Texture Science Consolidation, Bio-Based Rheology Modifiers, and Pharma-Grade Carbomers Driving $9.2 Billion Outlook at 5.9% CAGR

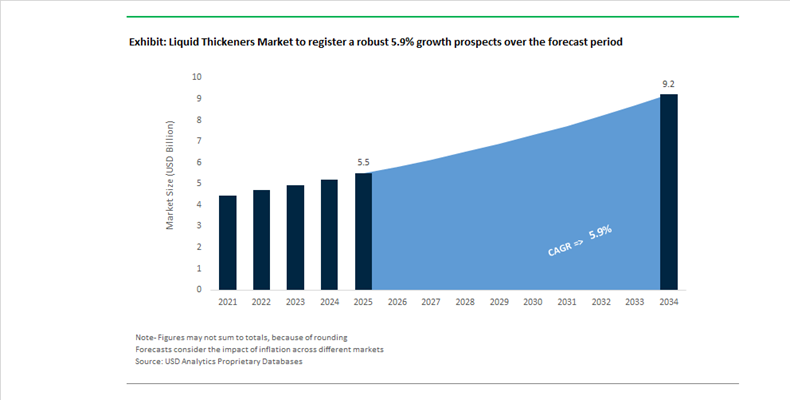

The Liquid Thickeners Market is projected to expand from $5.5 billion in 2025 to $9.2 billion by 2034, registering a CAGR of 5.9%. Growth is supported by increasing demand for rheology modifiers, viscosity control agents, hydrocolloids, associative thickeners, and pharmaceutical-grade carbomers across food and beverage, liquid detergents, architectural coatings, personal care, lubricants, and clinical nutrition applications. Rising consumer preference for clean-label ingredients, low-VOC waterborne formulations, and bio-based polymers is reshaping product development strategies, while aging populations and medical nutrition protocols are strengthening demand for high-performance liquid thickening systems for dysphagia management and therapeutic formulations.

In August 2024, Roquette introduced four tapioca-based cook-up starches under the CLEARAM TR series, engineered to deliver superior clarity, texture stability, and non-GMO compliance in sauces, fruit preparations, and ready-to-drink liquid foods. In November 2024, Tate & Lyle finalized its $1.8 billion acquisition of CP Kelco, integrating starch, pectin, xanthan gum, and gellan gum technologies into a unified global texture solutions platform. By April 1, 2025, Tate & Lyle transitioned to a new operating structure, and in late 2025 reported exceeding $50 million in targeted merger synergies through combined application science programs and reformulation support for high-protein beverages and dairy alternatives. Ashland expanded capacity for its Aquaflow non-ionic synthetic associative thickeners during 2024 and 2025 to support low-VOC architectural paints requiring precise flow and leveling control. These developments highlight consolidation-driven scale advantages in hydrocolloids and synthetic rheology modifiers.

Innovation momentum accelerated through 2025 and early 2026. Throughout 2025, Lubrizol and Evonik intensified production of high-purity pharmaceutical carbomers such as Carbomer 940 and 980, aligning with updated USP and NF excipient quality standards for sterile gels and topical liquids. In late 2025, Lubrizol launched HybriCal, a lithium-free grease thickener system addressing supply volatility in lithium-based lubricants while enabling high-performance semi-solid and liquid formulations. In February 2026, BASF added a new liquid dispersion production line at its Mangalore site to serve South Asian demand for construction chemicals and waterborne coatings. In early 2026, Nouryon introduced FinnFix PB MAX, a 100% bio-based and biodegradable carboxymethylcellulose grade designed for liquid laundry detergents with full renewable carbon indexing. In its February 2026 year-end report, Ingredion emphasized expansion of its Texture and Healthful Solutions segment, particularly modified starches used as primary liquid thickeners in clinical nutrition applications for elderly care.

Strategic Trends and High-Impact Opportunities in the Liquid Thickeners Market

Trend: Precision Texture Engineering for Plant-Based Dairy and Meat Analogues

The liquid thickeners market is undergoing a qualitative shift from generic viscosity control toward precision texture engineering as plant-based dairy and meat analogues move into their second generation of product development. Food manufacturers are no longer optimizing solely for thickness; instead, they are targeting structural mimicry that reproduces the melt, stretch, and bite characteristics of animal-derived fats and muscle fibers. This has elevated the strategic importance of advanced blends of citrus fibers, pectins, gums, and cellulose derivatives that can deliver multi-functional performance under shear, heat, and freeze–thaw cycles.

A major inflection point occurred in November 2024 when Tate & Lyle completed its acquisition of CP Kelco for approximately USD 1.8 billion. By April 2025, the combined entity began operating as a unified mouthfeel solutions platform, integrating starch science with high-performance pectins and gellan gums to address syneresis, chalkiness, and phase separation in plant-based beverages. Clean-label innovation is accelerating in parallel. Enzymatic texturization technologies are enabling fiber-based thickeners that also deliver nutritional benefits. Industry data from 2025 indicates that nearly 30% of global food launches now feature clean-label claims, with upcycled citrus fibers emerging as a preferred solution due to their ability to generate high viscosity without synthetic modifiers. Advances in methylcellulose chemistry are further enabling thermal gelation behavior, allowing plant-based burgers to firm during cooking and release moisture upon biting, closely replicating animal fat dynamics.

Trend: High-Efficiency Thickeners Enable Compact and Concentrated Home Care Formats

Sustainability-driven packaging regulations, particularly in Europe, are reshaping formulation priorities in the liquid thickeners market for home and personal care. Manufacturers are increasingly dependent on high-efficiency rheology modifiers that maintain stability, pour control, and performance in ultra-concentrated systems designed for e-commerce and refill-based distribution models. These smart thickeners must function at very low dosage levels while stabilizing high active ingredient loads.

Corporate innovation milestones highlight this trend. In July 2025, Procter & Gamble expanded the rollout of Tide Evo, a compact detergent platform built around fiber-tile architecture. This system relies on advanced thickeners that ensure instant dissolution in cold water while maintaining mechanical stability during shipping. Similarly, in April 2025, Unilever launched Cif Infinite Clean, a probiotic-based concentrated spray requiring rheology modifiers compatible with live microbial cultures. These formulations deliver vertical cling on hard surfaces without compromising bacterial viability. High-performance thickeners are also enabling refill-at-home systems by reducing water content in primary bottles by up to 80%, translating into reported plastic reductions of around 90% and materially lower Scope 3 transportation emissions.

Opportunity: Medically Calibrated Thickeners for Dysphagia Management

Aging demographics and the rising prevalence of neurodegenerative disorders are creating a regulated, clinically driven growth opportunity for liquid thickeners in dysphagia management. Patients with impaired swallowing require precisely calibrated textures to reduce aspiration risk, making consistency and amylase resistance critical performance attributes.

Clinical practice has shifted decisively toward gum-based systems, particularly xanthan gum, which now accounts for approximately 45% of dysphagia thickener usage. Unlike starch-based alternatives, these thickeners maintain viscosity when exposed to saliva, improving safety outcomes for patients recovering from stroke or living with Parkinson’s disease. Commercial scale-up is evident. During 2024 and 2025, Hormel Foods and Nestlé Health Science expanded ready-to-drink portfolios such as ThickenUp and Thick & Easy Hydrolyte. These products are factory-calibrated to International Dysphagia Diet Standardisation Initiative levels and offer extended shelf life, reducing caregiver burden. Digital dosing tools are also emerging to help families achieve accurate texture levels in home-prepared meals, lowering hospitalization risk and enabling decentralized care.

Opportunity: Advanced Rheology Modifiers for Lithium-Ion Battery Slurries

Beyond food and healthcare, the liquid thickeners market is expanding into energy storage, where aqueous polymers are being re-engineered as critical slurry stabilizers in lithium-ion battery manufacturing. Materials such as carboxymethyl cellulose now play a dual role as binders and rheology modifiers, ensuring uniform dispersion of high-nickel cathode and silicon-rich anode particles during high-speed electrode coating.

In 2024, research published in Nature Communications, with contributions from Ashland, demonstrated elastic gel polymer electrolytes that support higher silicon loading, a key lever for extending electric vehicle range. Ashland expanded its Bondwell aqueous binder and CMC portfolios through late 2025 to support gigafactory-scale production, improving slurry stability while reducing electrode cracking during cycling. Process control is becoming equally important. In early 2025, the UK Battery Industrialisation Centre and the Faraday Institution emphasized that real-time rheology monitoring can reduce electrode coating defects by up to 15%, positioning advanced thickeners as enablers of cost-efficient battery scale-up.

Liquid Thickeners Market Share and Segmentation Insights

Hydrocolloids Lead Liquid Thickeners Market with Natural Functional Ingredients in Formulation Science

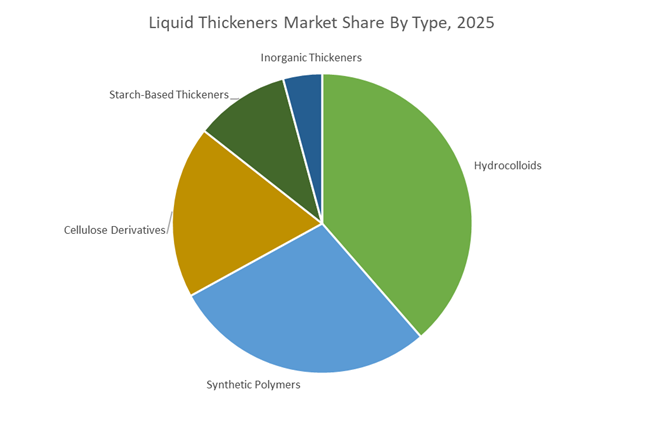

Hydrocolloids held 38.6% of the Liquid Thickeners Market share in 2025, making them the largest category of thickening agents used across food, pharmaceutical, and personal care formulations. Hydrocolloids such as xanthan gum, guar gum, pectin, carrageenan, and alginates are widely used because they provide efficient viscosity control, stabilization, emulsification, and suspension properties in liquid formulations. These naturally derived thickening agents deliver significant functional advantages in food processing, beverage stabilization, cosmetic emulsions, and pharmaceutical suspensions, where precise control of texture and rheology is essential for product performance. Hydrocolloids are particularly valued for their ability to maintain stable viscosity across varying temperature ranges, pH conditions, and shear environments, making them highly versatile for industrial product formulation. In 2025, growing consumer demand for clean label ingredients and plant-based formulation systems has accelerated the adoption of hydrocolloid thickeners sourced from natural raw materials. Manufacturers are therefore investing in minimally processed gums and novel plant-derived hydrocolloid solutions that deliver consistent thickening performance while supporting natural ingredient labeling in food, beverage, and personal care applications.

Food and Beverage Industry Drives the Largest Share of Liquid Thickener Consumption

Food and beverage applications accounted for 42.8% of the Liquid Thickeners Market share in 2025, positioning the sector as the primary consumer of liquid thickening agents globally. Thickeners are essential functional ingredients used to control viscosity, mouthfeel, texture, and stability across a wide range of processed foods including sauces, gravies, soups, dairy products, beverages, dressings, bakery fillings, and confectionery products. Food manufacturers depend on advanced thickening systems to ensure consistent product texture, suspension stability, and shelf-life performance, particularly in high-volume industrial food production. The demand for thickeners has expanded further as global consumers increasingly prefer convenience foods, ready-to-eat meals, and formulated beverages that require precise rheological control. In 2025, the rapid expansion of plant-based food products and alternative proteins has significantly increased the demand for high-performance thickening systems. Food formulators are increasingly using hydrocolloid blends and advanced thickener systems to replicate the creaminess of dairy products, the juiciness of meat analogues, and the structural stability of plant-based beverages, supporting innovation in modern plant-based food manufacturing.

Liquid Thickeners Market Competitive Landscape

The liquid thickeners market in 2026 is driven by clean-label hydrocolloids, bio-based rheology modifiers, and cold-process formulation technologies. Competitive dynamics are centered on multifunctional texture systems, pharmaceutical-grade excipients, and fermentation-integrated production, enabling advanced viscosity control, mouthfeel engineering, and regulatory-compliant formulations across food, personal care, and life sciences.

Ashland advances pharmaceutical-grade cellulosic thickeners for high-purity applications

Ashland Inc. is strengthening its leadership in cellulosic rheology through a focused specialty additives strategy following portfolio divestitures. Its expansion into high-purity injectable excipients, including low-nitrite cellulosics and sucrose systems, targets biotech-led drug delivery and stabilization markets. A strategic distribution partnership with IMCD enhances U.S. market penetration for personal care and home care thickeners. With Life Sciences growth driven by demand for oral and parenteral formulations, Ashland is positioning its liquid thickeners as precision excipients for complex pharmaceutical and high-performance formulation environments.

Tate & Lyle builds global hydrocolloid leadership through CP Kelco integration

Tate & Lyle, incorporating CP Kelco, has emerged as a dominant force in liquid thickener systems by integrating pectin, gellan gum, and advanced hydrocolloid technologies. Synergies exceeding $50 million and a $420 million innovation pipeline highlight strong demand for solution-based texture systems. Its GENU® pectin and KELCOGEL® gellan gum portfolios enable optimized viscosity and mouthfeel in plant-based dairy and functional beverages. The Texture University™ platform enhances customer formulation capabilities, positioning the company as a technical partner in clean-label, multisensory product development.

BASF accelerates biodegradable rheology modifiers for sustainable formulations

BASF SE is transitioning toward bio-based and biodegradable liquid thickeners, replacing synthetic acrylates with renewable alternatives such as Verdessence® Maize. Its expansion in Mangalore supports regional demand for rheology modifiers in coatings and construction chemicals, while Lamesoft® OP Plus addresses cold-process, energy-efficient personal care formulations. Strategic pricing adjustments reflect increased R&D investment in green chemistry. BASF’s focus on low-PCF, biodegradable thickeners aligns with regulatory and consumer-driven shifts toward sustainable formulation technologies.

Ingredion drives clean-label texture innovation with biotech-derived starch systems

Ingredion Incorporated is leveraging its global Idea Labs® network to develop clean-label liquid thickeners that deliver enhanced mouthfeel and health-oriented functionality. Investments in biotech-derived starches and fibers enable creamy textures in low-fat and reduced-sugar formulations, supporting evolving consumer preferences. Its focus on aeration and multisensory hydrocolloid systems targets premium food trends, including layered snacks and functional beverages. With operations in over 120 countries, Ingredion excels in localized texture optimization, particularly in Asia-Pacific dairy and beverage markets.

Lubrizol expands specialty polymer thickeners with regional innovation hubs

The Lubrizol Corporation is advancing high-performance liquid thickeners through polymer innovation and localized R&D infrastructure. Its HybriCal™ grease thickener system introduces lithium-free, environmentally improved rheology solutions for industrial applications. Expansion of innovation centers in Singapore and Shanghai supports rapid development of specialty coatings and liquid systems tailored to APAC demand. Strategic distribution partnerships in Europe enhance market access, while expertise in complex rheological transitions enables Lubrizol to deliver multifunctional thickener solutions across personal care, industrial, and mobility sectors.

United States: Bio-Based APG Scale-Up and AI-Engineered Rheology Systems

The United States liquid thickeners market is moving decisively toward bio-based surfactants, precision rheology control, and energy-efficient processing. In late 2025, BASF confirmed the construction of a new Alkyl Polyglucosides production line at its Cincinnati, Ohio site, scheduled for completion in 2026. This facility is positioned as a strategic hub for biodegradable liquid thickeners serving clean-label home care, personal care, and institutional cleaning formulations, where formulators are prioritizing plant-derived viscosity modifiers with low aquatic toxicity. Parallel to this capacity build, Ashland Global introduced Collapeptyl™ in 2025, a hybrid rheology modifier designed using AI-driven molecular modeling. The technology enables near-instant viscosity build in rinse-off systems, allowing manufacturers to cut batch mixing times and lower energy intensity across 2026 production cycles.

Healthcare and industrial applications are reinforcing this shift toward functional performance. Updated FDA guidance in 2025 on medical-grade liquid thickeners for dysphagia management has accelerated substitution away from starch systems toward xanthan and gum-based clear thickeners with high amylase resistance. At the same time, U.S. data center expansion is creating niche demand for high-performance fluorinated liquid thickeners that stabilize viscosity in dielectric immersion cooling fluids. Sustainability policy alignment is further shaping product design, with cold-processable ingredients such as Texturpure™ SA-2 gaining traction by eliminating heat-intensive neutralization steps and supporting Department of Energy 2026 efficiency objectives.

China: High-End Specialty Thickener Localization and Water-Efficiency Mandates

China’s liquid thickeners market is being reshaped by industrial policy that emphasizes self-sufficiency, sustainability, and high-end chemical supply. The Ministry of Industry and Information Technology released its 2025–2026 growth roadmap targeting over 5% annual expansion in chemical added value, with explicit prioritization of specialty surfactants and high-purity thickening agents for electronics, EV electrolytes, and advanced manufacturing. This has translated into accelerated investments in domestic HPMC and CMC production, as authorities push to lift self-sufficiency for critical intermediates beyond 90% by late 2026.

Environmental policy is acting as a parallel demand catalyst. China’s 2025 Catalog of Nationally Encouraged Industrial Water-Saving Processes now includes high-efficiency thickening and liquid separation technologies for mining and textiles, driving adoption of advanced rheology modifiers that improve water reuse. On the supply side, BASF completed the transition of its Jinshan operations to 100% renewable electricity in late 2025, materially lowering the product carbon footprint of liquid thickeners exported to Europe under CBAM rules. This positions Chinese-made specialty thickeners as both cost-competitive and compliance-ready for global markets.

India: Guar-Based Rheology Security and Regulatory Quality Tightening

India occupies a structurally important position in the global liquid thickeners market through its guar gum ecosystem and expanding pharmaceutical manufacturing base. In 2025, government-led sustainable farming initiatives in Rajasthan, implemented with industry partners such as Ashland Global, modernized guar supply chains to ensure traceability and nature-derived credentials aligned with 2026 European transparency requirements. This move strengthens India’s role as a reliable source of natural rheology modifiers for food, personal care, and oilfield applications.

Industrial policy is reinforcing downstream demand. Under the Production Linked Incentive scheme, realized investments reached ₹1.76 lakh crore in 2025, accelerating the commissioning of new API plants that rely on liquid thickeners to maintain suspension stability and dose uniformity. Regulatory tightening is also reshaping import dynamics. Quality Control Orders implemented in February 2025 require all imported liquid thickeners used in consumer goods to meet Bureau of Indian Standards purity norms, effectively curbing sub-standard inflows and supporting domestic formulators focused on compliant, high-performance rheology systems.

Germany: Circular Formulation Design and Biodegradable Thickener Substitution

Germany’s liquid thickeners market is increasingly defined by circular economy compliance and ingredient substitution driven by EU regulation. With the European Union’s Packaging and Packaging Waste Regulation becoming applicable from August 2026, German manufacturers are reformulating liquid thickeners to ensure compatibility with recycling streams for plastic and glass packaging. This is pushing demand toward rheology modifiers that do not interfere with recyclability or create residue during reprocessing.

Innovation is centered on biodegradability and regulatory foresight. At In-cosmetics Global 2025, German suppliers showcased lignin-derived liquid thickeners developed from forestry side streams, offering measurable CO2 footprint reductions of around 5% compared with synthetic carbomers. In parallel, the May 2025 EU ban on certain camphor-derived substances has accelerated the replacement of legacy stabilizers with next-generation liquid-to-powder rheology modifiers. These developments position Germany as a lead market for compliant, bio-based thickening technologies entering 2026 consumer product cycles.

Thailand: APG Regional Hub and Bio-Circular-Green Export Strategy

Thailand is consolidating its role as a Southeast Asian production and export hub for bio-based liquid thickeners. In November 2025, BASF inaugurated a major expansion of its Alkyl Polyglucosides capacity in Bangpakong, establishing the site as the primary regional supply base for APG-based liquid thickeners serving personal care, crop protection, and agricultural adjuvant markets. This expansion improves regional supply resilience while aligning with rising demand for low-VOC, plant-derived surfactant systems.

Policy support under Thailand’s Bio-Circular-Green economy framework is reinforcing this trajectory. The 2025–2026 BCG incentives offer tax holidays for investments in enzymatic extraction of natural gums and bio-based rheology modifiers, explicitly targeting export-oriented production. As a result, Thailand is positioning itself as a competitive supplier of sustainable liquid thickeners to Asia-Pacific and European buyers seeking alternatives to petroleum-derived viscosity modifiers.

Liquid Thickeners Market: Country-Level Strategic Snapshot

Liquid Thickeners Market County Level Snapshot

|

Country

|

Strategic Driver

|

Focus Area

|

Industrial Implication

|

|

United States

|

Clean-label demand and AI optimization

|

APGs, AI-designed rheology, medical-grade thickeners

|

Faster processing, lower energy intensity, diversified end-use

|

|

China

|

Policy-led localization and water efficiency

|

HPMC, CMC, renewable-powered production

|

High-end domestic supply with export compliance

|

|

India

|

Guar security and pharma expansion

|

Natural gums, API suspension systems

|

Stable global supply and quality-led import substitution

|

|

Germany

|

EU circular economy regulation

|

Biodegradable, recyclable-compatible thickeners

|

Leadership in compliant formulation design

|

|

Thailand

|

Bio-based export positioning

|

APG capacity, enzymatic extraction

|

Regional hub for low-VOC, plant-derived thickeners

|

Liquid Thickeners Market Report Scope

Liquid Thickeners Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.5 Billion

|

|

Market Size (2034)

|

$9.2 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Type (Hydrocolloids, Cellulose Derivatives, Synthetic Polymers, Starch-Based Thickeners, Inorganic Thickeners), By Source (Plant-Derived, Microbial or Fermentation-Based, Synthetic, Marine-Derived), By Application (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Paints and Coatings, Industrial Applications, Home Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ashland Global Holdings, BASF SE, Ingredion, CP Kelco, Cargill, Dow, Kerry Group, Archer Daniels Midland, Tate and Lyle, Clariant AG, Lubrizol Corporation, Akzo Nobel, Solvay, Mitsubishi Chemical Group, Nouryon

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Thickeners Market Segmentation

By Type

- Hydrocolloids

- Cellulose Derivatives

- Synthetic Polymers

- Starch-Based Thickeners

- Inorganic Thickeners

By Source

- Plant-Derived

- Microbial or Fermentation-Based

- Synthetic

- Marine-Derived

By Application

- Food and Beverage

- Pharmaceuticals

- Personal Care and Cosmetics

- Paints and Coatings

- Industrial Applications

- Home Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Liquid Thickeners Market

- Ashland Global Holdings

- BASF SE

- Ingredion

- CP Kelco

- Cargill

- Dow

- Kerry Group

- Archer Daniels Midland

- Tate and Lyle

- Clariant AG

- Lubrizol Corporation

- Akzo Nobel

- Solvay

- Mitsubishi Chemical Group

- Nouryon

*- List not Exhaustive