Lithium-Ion Battery Electrolyte Solvent Market 2025–2034: Domestic Capacity Expansion, IRA-Driven Localization, and CO₂-Based Carbonate Synthesis Driving $2,693.9 Million Outlook at 17.2% CAGR

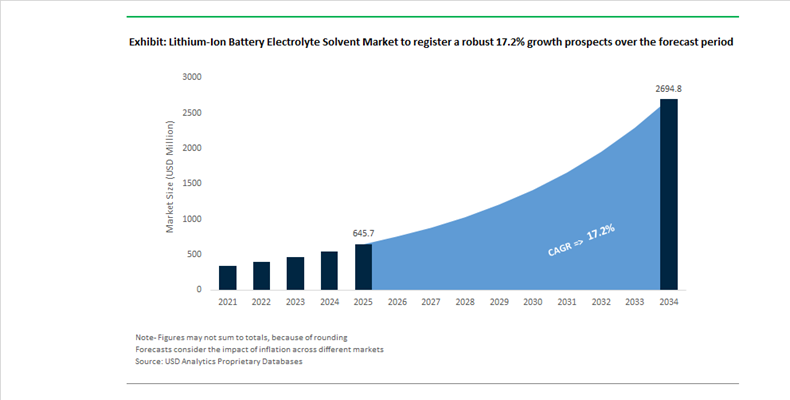

The Lithium-Ion Battery Electrolyte Solvent Market is projected to surge from $645.7 Million in 2025 to $2,693.9 Million by 2034, registering an exceptional CAGR of 17.2%. Growth is fueled by exponential expansion of EV battery gigafactories, localization mandates under the U.S. Inflation Reduction Act and European battery regulations, and rising demand for high-purity carbonate solvents such as ethylene carbonate (EC), dimethyl carbonate (DMC), and ethyl methyl carbonate (EMC). Electrolyte solvent systems remain central to lithium-ion battery performance, influencing ionic conductivity, electrochemical stability window, SEI formation, and high-voltage cathode compatibility. Accelerating adoption of high-nickel cathodes, silicon-rich anodes, and semi-solid-state chemistries is intensifying the need for advanced solvent blends with enhanced oxidative stability and low impurity profiles.

In May 2024, Capchem USA announced a $350 million integrated carbonate solvent and electrolyte plant in Louisiana with annual capacity of 200,000 tons, utilizing proprietary ECOSIP technology to convert ethylene oxide and captured CO₂ into battery-grade carbonates. In late 2024, Tamilnadu Petroproducts initiated modernization of its petrochemical infrastructure and authorized feasibility studies to diversify into specialty battery solvents to support India’s emerging lithium-ion manufacturing base. In March 2025, UBE Corporation broke ground on its $500 million facility in Jefferson Parish, Louisiana, the first large-scale U.S. manufacturing site dedicated to electrolyte solvents, targeting 100,000 metric tons of DMC and 40,000 metric tons of EMC annually, with commercial operations expected in late 2026. In mid-2025, the U.S. government introduced targeted tariffs on imported EC, DMC, and EMC from key Asian hubs, accelerating domestic solvent localization and reshaping global trade flows.

Technological shifts and contract-backed scaling intensified through 2025 and early 2026. In March 2025, TCI Chemicals launched a dedicated sodium-ion electrolyte solvent series to address alternative battery chemistries for grid storage and cost-sensitive applications. In August 2025, BASF Shanshan Battery Materials transitioned to mass production of cathode materials and compatible semi-solid-state electrolyte systems in collaboration with Welion, focusing on solvent formulations that suppress interfacial side reactions in high-capacity cathodes. In November 2025, Enchem announced a $1.03 billion supply agreement covering 350,000 tons of electrolyte deliveries to CATL between 2026 and 2030, while scaling production to 200,000 tons each in Georgia and Poland by 2026 to meet local content requirements. On February 4, 2026, Lotte Chemical confirmed strategic restructuring to prioritize high-performance battery materials, integrating solvent production with cathode foil expansion for the North American EV market. Throughout 2025 and into 2026, producers including Lotte Chemical and Capchem advanced CO₂-capture-based synthesis routes for dimethyl carbonate, positioning low-carbon solvent systems as key differentiators in next-generation EV battery supply chains.

Strategic Trends and High-Growth Opportunities in the Lithium-Ion Battery Electrolyte Solvent Market

Trend: Circular Economy Integration for Battery-Grade Linear Carbonates

The lithium-ion battery electrolyte solvent market is undergoing structural realignment as OEMs demand lower Scope 3 emissions and verifiable sustainability credentials under emerging battery passport frameworks. Producers of dimethyl carbonate and ethyl methyl carbonate are pivoting toward circular feedstocks, including recycled ethylene glycol, captured carbon dioxide, and bio-methanol, to reduce cradle-to-gate carbon intensity.

In early 2025, UBE Corporation confirmed the deployment of its proprietary gas-phase nitrite process, enabling lower energy consumption and direct production of ultra-high-purity battery-grade DMC. Traceability is becoming a competitive differentiator. By October 2025, Mitsubishi Chemical Group implemented blockchain-based solvent traceability platforms in partnership with Chaintope Inc. and Circularise, allowing customers to verify circular carbon content and align with the EU safe-and-sustainable-by-design framework. Investment trends from 2024 to 2025 indicate that circular feedstocks could reduce solvent carbon footprints by up to 30% by 2027 compared to coal-based routes.

Trend: Expansion of Fluorinated Solvents for High-Voltage Battery Platforms

The push toward higher energy density is accelerating adoption of fluorinated electrolyte solvents capable of supporting cell voltages above 4.3 volts. Fluoroethylene carbonate is transitioning from a minor additive to a core co-solvent as it enables stable cathode electrolyte interphase formation in high-nickel and silicon-anode systems.

A 2025 study indexed by the National Institutes of Health validated that FEC-based electrolytes paired with LiPO2F2 salts can sustain high reversible capacity in NMC cathodes over extended cycling at 4.4 volts. Adoption is broadening beyond high-nickel chemistries. Late-2025 research demonstrated that fluorinated solvent systems improve low-temperature performance and achieve over 90% capacity retention after 1,000 cycles in lithium iron phosphate pouch cells. Industry formulators are now increasing FEC loading to co-solvent levels of up to 25% in next-generation electrolyte blends.

Opportunity: IRA-Driven Onshoring of Battery Solvent Production in the United States

Policy intervention is creating an immediate market opportunity for domestic electrolyte solvent manufacturing. Under the U.S. Inflation Reduction Act, solvents qualify as battery components and must be produced in North America to access clean vehicle tax credits.

In March 2025, UBE Corporation broke ground on a USD 491 million manufacturing complex in Louisiana, set to become the only domestic producer of battery-grade DMC and EMC with operations planned for late 2026. Asian suppliers are also restructuring. In October 2025, Enchem pivoted capital toward expanding facilities in Georgia and Indiana to serve customers such as LG Energy Solution and Samsung SDI within Foreign Entity of Concern guidelines. Consolidation is reinforcing profitability, highlighted by Mitsubishi Chemical’s December 2025 transfer of electrolyte assets in the U.S. and UK under its KAITEKI Vision 35 strategy.

Opportunity: Low-Viscosity Electrolytes for Extreme Fast Charging

Extreme fast charging has emerged as the next performance frontier, requiring electrolytes with ultra-low viscosity and high ionic conductivity. Research presented at ECS Meeting Abstracts in late 2025 highlighted butyronitrile- and ether-based co-solvents that enable 10 to 80% charging in under 15 minutes while suppressing lithium plating.

These solvent systems also improve cold-weather performance, maintaining capacity at minus 20 degrees Celsius. Commercial momentum is accelerating. In December 2025, Enchem secured a five-year contract worth approximately KRW 1.5 trillion to supply specialized fast-charging electrolytes to CATL, covering a total volume of 350,000 tonnes between 2026 and 2030. This contract underscores how low-viscosity solvent innovation is becoming a decisive competitive lever in next-generation battery platforms.

Lithium-Ion Battery Electrolyte Solvent Market Share and Segmentation Insights

Carbonate Solvents Dominate Lithium-Ion Battery Electrolyte Solvent Market with Proven Electrochemical Stability

Carbonate solvents accounted for 68.40% of the Lithium-Ion Battery Electrolyte Solvent Market share in 2025, establishing them as the primary solvent system used in lithium-ion battery electrolyte formulations. Key carbonate solvents including ethylene carbonate (EC), dimethyl carbonate (DMC), ethyl methyl carbonate (EMC), diethyl carbonate (DEC), and propylene carbonate (PC) provide the optimal balance of high dielectric constant, low viscosity, strong lithium salt solubility, and wide electrochemical stability window required for high-performance battery electrolytes. These solvents play a central role in lithium-ion battery ion transport, electrode interface stability, and overall electrochemical efficiency, supporting their extensive use across electric vehicles, consumer electronics, and stationary energy storage systems. Carbonate-based electrolyte systems also benefit from mature manufacturing infrastructure and well-established supply chains, enabling large-scale battery production. In 2025, battery developers focusing on high-energy cathode chemistries such as NMC 811 and NMC 9.5.5 have advanced carbonate solvent formulations using optimized additive packages to enhance oxidative stability at elevated voltages, enabling improved cycle life and stable electrolyte performance in next-generation high-energy lithium-ion batteries.

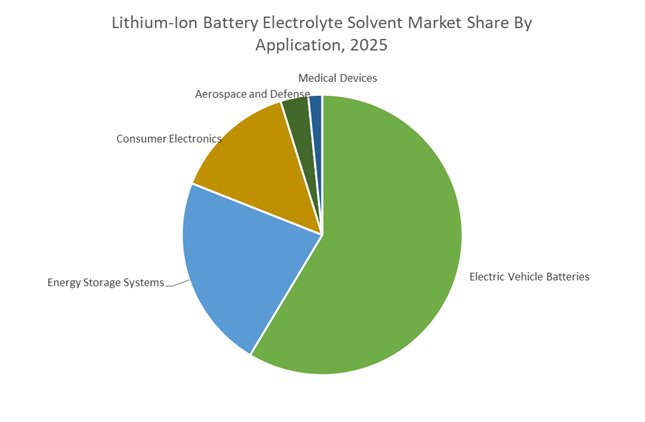

Electric Vehicle Batteries Drive the Largest Share of Electrolyte Solvent Consumption

Electric vehicle batteries accounted for 58.60% of the Lithium-Ion Battery Electrolyte Solvent Market share in 2025, making the automotive electrification sector the dominant consumer of battery electrolyte solvents globally. The rapid expansion of electric vehicle manufacturing and battery gigafactory capacity has created substantial demand for high-purity electrolyte solvents used in lithium-ion battery cell production. Each EV battery pack typically requires 50–100 kWh of battery capacity, translating into significant volumes of electrolyte solutions composed of lithium salts and carbonate solvent blends. Battery electrolytes are critical for lithium-ion transport between anode and cathode, thermal stability, and electrochemical efficiency, directly influencing battery performance, safety, and durability. In 2025, ongoing innovation in EV battery technology has led to the adoption of diverse cell formats including cylindrical, prismatic, and pouch cells, each requiring customized electrolyte solvent formulations. High-power battery cells designed for fast charging often use different carbonate solvent ratios compared with high-energy density cells, creating specialized electrolyte solvent demand across the rapidly evolving electric vehicle battery manufacturing ecosystem.

Lithium-Ion Battery Electrolyte Solvent Market Competitive Landscape

The lithium-ion battery electrolyte solvent market in 2026 is driven by localized carbonate production, ultra-high-purity EC/DMC synthesis, and vertical integration across feedstocks. Competitive intensity is rising around Rules of Origin compliance, CO2-based circular production, and solvent systems tailored for 800V EV batteries and next-generation chemistries.

Capchem expands global carbonate solvent capacity with circular feedstock integration

Shenzhen Capchem Technology is scaling its “one-stop” electrolyte ecosystem through aggressive global capacity expansion and vertical integration. Its $260 million Saudi Arabia plant (200,000 tons/year) and Poland expansion strengthen supply to Europe and Southeast Asia, while its Louisiana project leverages ethylene oxide and captured CO2 to create a circular carbonate production loop. With active development of solid-state electrolyte materials and diversified global manufacturing, Capchem is positioning itself as a resilient supplier of battery-grade EC and DMC aligned with gigafactory localization trends.

UBE builds U.S.-based high-purity carbonate production using proprietary C1 chemistry

UBE Corporation is emerging as a critical non-China supplier by establishing domestic U.S. production of battery-grade solvents. Its Louisiana facility will deliver 100,000 tons of DMC and 40,000 tons of EMC annually, addressing supply chain vulnerabilities and compliance with regional sourcing mandates. Leveraging its proprietary nitrite-based C1 process, UBE produces ultra-high-purity solvents with minimal by-products, meeting stringent requirements for high-performance lithium-ion batteries and semiconductor-grade applications. Strategic integration with downstream elastomer businesses further enhances value chain synergies.

Lotte Chemical integrates CCU into carbonate solvent production for low-carbon supply chains

Lotte Chemical is embedding carbon capture and utilization (CCU) into its electrolyte solvent strategy, constructing a 602 billion won facility that converts 200,000 tons of captured CO2 into EC and DMC. This approach reduces reliance on imported solvents while aligning with green subsidy frameworks and low-carbon mandates. Its integrated battery materials portfolio, including separators and copper foil, strengthens vertical control. Parallel development of sulfide-based solid electrolytes and aqueous ESS systems positions Lotte at the forefront of next-generation electrolyte innovation.

Tinci scales electrolyte and LiPF6 integration to reinforce cost leadership

Tinci Materials is consolidating its position as a volume leader by expanding LiPF6 and carbonate-based electrolyte capacity while increasing upstream self-sufficiency. Its Anhui expansion boosts liquid LiPF6 output to 280,000 tons/year, with dedicated EMC and DMC production lines supporting diversified solvent systems. Rapid revenue growth (16.65 billion yuan in 2025) reflects strong demand from EV battery manufacturers. Simultaneously, pilot-scale solid-state electrolyte production and lithium sulfide capacity signal a strategic pivot toward next-generation battery chemistries while maintaining cost competitiveness.

Mitsubishi Chemical focuses on advanced solvent additives for high-voltage battery performance

Mitsubishi Chemical is restructuring its battery materials portfolio to prioritize high-value solvent additives and next-generation electrolyte systems. Divestment of U.S. and UK electrolyte assets allows greater focus on advanced carbonate blends and additives such as vinylene carbonate, critical for stabilizing SEI layers in nickel-rich cathodes. Its “Interphase First” strategy targets performance optimization in 800V EV architectures, addressing challenges such as transition-metal dissolution and cycle life degradation. Concentration on Asia-Pacific production hubs further supports its specialization in high-purity, performance-driven electrolyte solutions.

United States: Domestic Electrolyte Solvent Sovereignty Under IRA and FEOC Rules

The United States lithium ion battery electrolyte solvent market entered a structural transition phase in 2025, driven by federal industrial policy, supply chain security mandates, and next-generation battery performance requirements. A pivotal development was UBE Corporation breaking ground in March 2025 on a USD 491 million Dimethyl Carbonate and Ethyl Methyl Carbonate facility in Louisiana. Scheduled for completion in July 2026, this project establishes the first fully domestic source of DMC and EMC in the U.S., addressing a long-standing dependency on Asian imports. The facility is engineered to deliver 100,000 tons of DMC and 40,000 tons of EMC annually by late 2026, using a proprietary gas-phase nitrite process that materially reduces energy intensity and trace impurity formation compared with ethylene-based routes. This positions U.S. battery OEMs to meet tightening purity thresholds for fast-charging and high-voltage cell chemistries.

Policy alignment is amplifying the strategic importance of these investments. The Department of Energy announced a USD 500 million circularity-focused grant program in August 2025 under the Bipartisan Infrastructure Law, explicitly prioritizing domestic electrolyte solvent and salt production. In parallel, finalized Foreign Entity of Concern guidance issued in December 2025 has accelerated the restructuring of solvent procurement strategies, as eligibility for 2026 Inflation Reduction Act tax credits increasingly hinges on non-Chinese supply chains. Portfolio optimization is also underway, with Mitsubishi Chemical Group transferring its U.S.-based electrolyte manufacturing assets in late 2025 to refocus on high-margin specialty solvent licensing and downstream thermal management materials used in AI server and semiconductor cooling applications.

China: Scale Leadership with Carbon Transparency and Self-Sufficiency Mandates

China remains the global scale leader in lithium ion battery electrolyte solvent production, but the market is being reshaped by regulatory tightening and sustainability disclosure requirements. The Ministry of Industry and Information Technology issued its 2025–2026 petrochemical roadmap in October 2025, targeting more than 5% annual growth in chemical added value while explicitly prioritizing battery-grade solvents for EV applications. From 2026 onward, NEV battery manufacturers will be required to report full carbon footprints, including upstream emissions associated with solvents such as propylene carbonate and dimethyl carbonate. This is pushing solvent producers toward cleaner synthesis routes and renewable-powered facilities.

Industrial policy is also reinforcing localization. Beijing’s 2026 strategy seeks to raise domestic self-sufficiency for critical battery intermediates beyond 90%, tightening approval for new low-end refining projects while granting priority capacity boosts to high-purity solvent and advanced blend facilities. Demand visibility remains strong, illustrated by Enchem’s five-year agreement signed in December 2025 to supply 350,000 tons of electrolyte to CATL starting in 2026. These dynamics position China as a high-volume but increasingly compliance-driven market, where carbon intensity and traceability are becoming decisive competitive variables.

South Korea: CCU-Enabled Solvent Manufacturing and Global Alliance Strategy

South Korea is positioning itself as a premium, low-carbon supplier of lithium ion battery electrolyte solvents through capital-intensive investments and coordinated industry alliances. Lotte Chemical is executing a KRW 602 billion investment at its Daesan complex to build high-purity ethylene carbonate and dimethyl carbonate capacity, targeting commercialization across 2025–2026 under its Green Promise 2030 framework. A defining feature of this project is the integration of Carbon Capture and Utilization technology capable of processing 200,000 tons of CO₂ annually, which is then reused as a feedstock for electrolyte solvent synthesis. This materially lowers lifecycle emissions and strengthens positioning with OEMs facing tightening Scope 3 reporting requirements.

Institutionally, the launch of the Korea Battery Alliance in November 2025 signals a coordinated push to secure downstream solvent and electrolyte supply chains in the U.S. and Europe ahead of 2026 regulatory inflection points. R&D intensity is rising in parallel, with UBE and Korean partners lifting research expenditure to roughly 4% of sales in late 2025, focused on C1 chemical chain innovations that improve solvent purity and compatibility with advanced battery sealing and high-voltage cell designs.

Japan: IP-Centric Solvent Strategy and Feedstock Stability

Japan’s lithium ion battery electrolyte solvent sector is evolving toward an intellectual property and licensing-led model rather than volume manufacturing. MU Ionic Solutions, an affiliate of Mitsubishi Chemical, received the Asia IP Elite 2025 award in December 2025, underscoring Japan’s strategic pivot toward exporting solvent process know-how and electrolyte formulations rather than commodity volumes. This approach allows Japanese firms to capture value across global battery supply chains without direct exposure to capacity cycles.

Feedstock security remains a parallel priority. In September 2025, Mitsubishi Chemical, Mitsui Chemicals, and Asahi Kasei formed a limited liability partnership to jointly manage ethylene manufacturing assets. This ensures cost-efficient and stable ethylene supply for downstream DMC production while supporting cross-industry applications, including PFAS-substitute barrier resins introduced in late 2025.

European Union: Lifecycle Accountability and Carbon-Priced Solvent Trade

The European Union is shaping demand for lithium ion battery electrolyte solvents primarily through regulation rather than capacity expansion. Battery Regulation (EU) 2023/1542 introduces mandatory producer responsibility organization membership from January 2026, requiring solvent manufacturers to provide granular lifecycle documentation covering sourcing, processing, and emissions. This is reinforced by the Carbon Border Adjustment Mechanism, which by early 2026 will impose carbon pricing on imported solvent precursors, structurally favoring suppliers with renewable-powered or carbon-neutral production.

Mandatory battery labeling requirements taking effect by mid-2026 further elevate solvent purity and transparency expectations, as chemical composition disclosures become compulsory. These measures are accelerating procurement shifts among EU battery makers toward solvent suppliers that can demonstrate low-carbon production pathways and auditable supply chains, reshaping competitive dynamics across the region.

Lithium Ion Battery Electrolyte Solvent Market: Country-Level Strategic Snapshot

Lithium-Ion Battery Electrolyte Solvent Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Industrial Lever

|

Supply Chain Implication

|

|

United States

|

Domestic sovereignty and IRA compliance

|

First domestic DMC/EMC capacity, FEOC rules

|

Rapid reshoring of solvent supply

|

|

China

|

Scale with carbon disclosure

|

Self-sufficiency targets, footprint reporting

|

Cleaner, policy-aligned volume leadership

|

|

South Korea

|

Low-carbon premium positioning

|

CCU-integrated solvent plants, alliances

|

Preferred supplier for regulated markets

|

|

Japan

|

IP and licensing leadership

|

Solvent process know-how, feedstock JV

|

Asset-light global value capture

|

|

European Union

|

Regulatory-driven demand shaping

|

Lifecycle reporting, CBAM

|

Shift toward renewable-based solvents

|

Lithium-Ion Battery Electrolyte Solvent Market Report Scope

Lithium-Ion Battery Electrolyte Solvent Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$645.7 Million

|

|

Market Size (2034)

|

$2693.9 Million

|

|

Market Growth Rate

|

17.2%

|

|

Segments

|

By Solvent Type (Carbonates, Esters, Ethers, Sulfones and Nitriles, Ionic Liquids), By Purity Level (Battery Grade, Industrial Grade), By Application (Electric Vehicle Batteries, Consumer Electronics, Energy Storage Systems, Aerospace and Defense, Medical Devices), By Battery Chemistry (Lithium Iron Phosphate, Nickel-Based Lithium Chemistries, Solid-State Battery Systems)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mitsubishi Chemical Group, UBE Corporation, Enchem, Lotte Chemical, BASF SE, Capchem Technology, Guangdong Guotai-Huarong New Chemical Materials, Tinci Materials Technology, Shanshan Technology, Mitsui Chemicals, Kanto Chemical, Soulbrain, Huntsman Corporation, Central Glass, Panax Etec

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lithium-Ion Battery Electrolyte Solvent Market Segmentation

By Solvent Type

By Purity Level

- Battery Grade

- Industrial Grade

By Application

- Electric Vehicle Batteries

- Consumer Electronics

- Energy Storage Systems

- Aerospace and Defense

- Medical Devices

By Battery Chemistry

- Lithium Iron Phosphate

- Nickel-Based Lithium Chemistries

- Solid-State Battery Systems

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Lithium-Ion Battery Electrolyte Solvent Market

- Mitsubishi Chemical Group

- UBE Corporation

- Enchem

- Lotte Chemical

- BASF SE

- Capchem Technology

- Guangdong Guotai-Huarong New Chemical Materials

- Tinci Materials Technology

- Shanshan Technology

- Mitsui Chemicals

- Kanto Chemical

- Soulbrain

- Huntsman Corporation

- Central Glass

- Panax Etec

*- List not Exhaustive