Metal Chelates Market 2025–2034: Biodegradable GLDA Innovation, AI-Driven Micronutrient Precision, and Coatings Consolidation Driving $1,577.2 Million Outlook at 8.6% CAGR

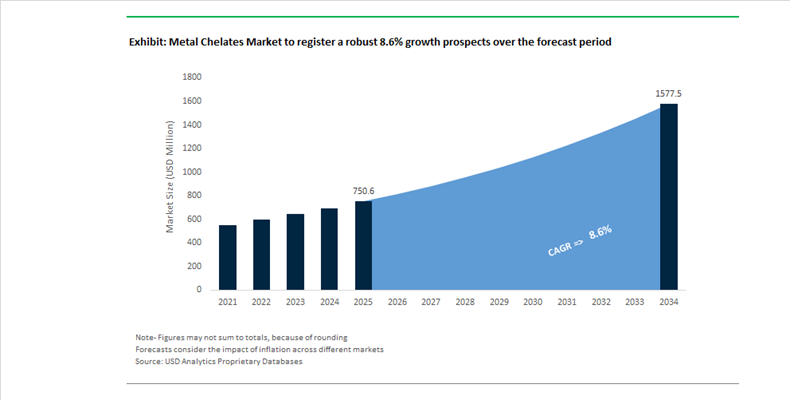

The Metal Chelates Market is projected to expand from $750.6 Million in 2025 to $1,577.2 Million by 2034, registering a strong CAGR of 8.6%. Market growth is being propelled by rising demand for chelated micronutrients in precision agriculture, biodegradable chelating agents in home and industrial care, and high-performance chelates in coatings and specialty chemical formulations. Key products such as EDTA, DTPA, EDDHA, MGDA, and GLDA play critical roles in nutrient stabilization, heavy metal sequestration, scale inhibition, and pigment dispersion. Increasing environmental scrutiny of persistent aminopolycarboxylates is accelerating the shift toward readily biodegradable “green chelates,” while digital agronomy platforms are improving nutrient use efficiency in fertigation and foliar applications.

In late 2024, Valagro completed expansion of its U.S. manufacturing facility under Syngenta ownership, strengthening supply of high-stability EDDHA and DTPA chelates for specialty crops in North America. In April 2025, BASF launched Trilon G, a GLDA-based chelating agent containing approximately 56% renewable carbon and designed to replace persistent EDTA in cleaning and industrial applications. Throughout 2025, EU and North American wastewater treatment operators accelerated adoption of biodegradable MGDA and GLDA chelates to comply with stricter aquatic persistence regulations. In August 2025, Haifa Group inaugurated its Indian headquarters in Hyderabad following a strategic partnership with Deepak Fertilisers, positioning advanced chelated micronutrient solutions closer to high-growth fertigation markets. In November 2025, Haifa introduced an AI-driven agronomist chatbot providing site-specific micronutrient application guidance to smallholder farmers, reinforcing digital integration within the chelate distribution ecosystem.

Strategic realignment intensified in late 2025 and early 2026. In late 2025, AkzoNobel divested its Indian subsidiary for approximately €922 million to focus capital on high-growth industrial segments, while maintaining leadership in specialty chelating agents. In November 2025, Nutrien initiated a strategic review of its phosphate business, potentially reshaping bundled distribution of chelated fertilizers and phosphate-based nutrients. In early 2026, AkzoNobel and Axalta announced a proposed all-stock merger, combining significant R&D resources to accelerate innovation in high-performance chelates for automotive and industrial coatings. In February 2026, Yara confirmed delivery of over $200 million in fixed cost reductions since 2024, enabling reinvestment in decarbonized ammonia platforms that underpin its global micronutrient and chelate portfolio. Concurrently, Yara expanded AI-driven nutrient recommendation systems throughout 2025, leveraging real-time soil analytics to optimize chelated micronutrient dosing and minimize runoff, strengthening the role of data-enabled precision agriculture in driving future chelate demand.

Metal Chelates Market Trends and Opportunities

Trend: Strategic Capacity Expansion for High-Purity Micronutrient Chelates in Controlled Environment Agriculture

The Metal Chelates Market is undergoing a structural upgrade driven by the rapid expansion of Controlled Environment Agriculture (CEA), vertical farming, and precision hydroponics. These systems require micronutrient chelates with near-zero impurity profiles, as even trace chlorides or heavy metals can clog micro-irrigation emitters or destabilize recirculating nutrient solutions. Standard agricultural chelates are increasingly unfit for purpose in high-tech greenhouses, prompting suppliers to invest in high-purity chelation chemistry. In January 2025, Bayer Crop Science launched its next-generation Wojiarun line in China, upgrading calcium fertilizers from ionic salts to highly stable chelated complexes to improve uptake efficiency and consistency in advanced greenhouse systems.

Performance benchmarks are also shifting. Modern Fe-EDDHSA chelates are now engineered to remain stable at soil pH levels up to 9.0, a critical requirement for vertical farming and alkaline substrates where nutrient precipitation is a persistent challenge. In 2025, field initiatives in France demonstrated drone-compatible foliar chelate formulations applied across more than 800 hectares of vineyards, delivering rapid nutrient absorption that conventional soil-applied salts cannot achieve. Supporting this transition, CHS Inc. introduced Levesol in late 2024, a specialized chelating agent that prevents phosphorus from binding micronutrients, increasing zinc and iron bioavailability by an estimated 15 to 20%. These developments position high-purity chelates as foundational inputs for scalable, water-efficient agriculture.

Trend: Heavy Metal Sequestering Chelates for Lithium-Ion Battery “Black Mass” Recycling

The acceleration of lithium-ion battery recycling has created a second high-growth axis for the Metal Chelates Market. With global recycling capacity reaching an estimated 1.6 million tons annually in 2025, hydrometallurgical processing has become the dominant recovery pathway, relying on selective chelation to separate valuable metals from shredded battery waste, known as black mass. Chelating agents act as precision separation tools, selectively binding nickel, cobalt, and manganese to produce battery-grade salts rather than lower-value mixed alloys. Reports from Green Li-ion in 2025 indicate that advanced hydrometallurgical routes achieve greenhouse gas emission reductions of 58 to 81% compared to virgin mining, underscoring the sustainability advantage of chelate-enabled recovery.

Technical advances continue to raise recovery efficiency. Protocols published in ACS Omega in December 2025 demonstrate recovery of 72.2% of lithium as lithium carbonate and 97% of plastics and graphite from spent LFP batteries using tightly controlled chelation and ion-exchange processes. Beyond efficiency, metal chelates are becoming strategic tools for resource sovereignty. With more than 70% of global cobalt supply concentrated in the Democratic Republic of Congo, Western recyclers such as Redwood Materials are deploying specialized chelating chemistries to enable closed-loop recycling. This approach directly supports compliance with the EU Battery Regulation by supplying recycled, battery-grade metals back into cathode manufacturing.

Opportunity: Ultra-Pure Copper Chelates for Semiconductor Advanced Packaging

One of the highest-value opportunities in the Metal Chelates Market is emerging from advanced semiconductor packaging. The growth of artificial intelligence and high-performance computing is accelerating adoption of 2.5D and 3D packaging architectures, which require nanoscale copper interconnects with extreme planarity. Chemical Mechanical Planarization and copper plating processes depend on ultra-pure copper chelators to prevent galvanic corrosion while ensuring defect-free surfaces. In October 2025, Bloomberg Intelligence projected that the advanced packaging market could expand eightfold to USD 80.5 billion by 2033, driven largely by hybrid bonding technologies that create copper-to-copper connections at unprecedented densities.

Demand visibility is strengthening across the supply chain. In November 2025, TECHCET estimated the global plating chemicals market, including copper chelators, at USD 1.38 billion, with nearly equal demand split between device interconnects and advanced packaging applications. To capture this growth, Moses Lake Industries opened a USD 100 million R&D facility in Arizona in late 2025 focused on high-purity electrolytes and copper plating chemistries. In parallel, MacDermid Alpha launched MICROFAB SC-40 PLUS, a system designed for high-density copper pillar plating. These investments signal sustained demand for precision chelation chemistry tailored to AI-driven semiconductor manufacturing.

Opportunity: Biodegradable Chelates for Sustainable Industrial Cleaning and Water Management

Regulatory pressure on persistent chelating agents such as EDTA is reshaping demand in industrial and institutional cleaning markets. The EU’s provisional agreement on updated Detergents and Surfactants regulations in June 2025 introduced momentum toward product passport systems that favor readily biodegradable ingredients. This shift creates a substantial opportunity for biodegradable chelates such as GLDA and EDDS, which deliver strong scale inhibition while minimizing environmental persistence. In early 2025, BASF launched Trilon G, a chelating agent with 56% renewable carbon content and over 60% biodegradation within 28 days, enabling compliance with EU Ecolabel and Nordic Swan standards at industrial scale.

Sector-specific adoption is accelerating. The pulp and paper industry, which accounts for approximately 26% of chelate consumption, is rapidly shifting toward DTPA and GLDA to stabilize hydrogen peroxide bleaching and improve fiber brightness while reducing chemical waste. Water treatment regulations are also driving demand. Under the Vessel Incidental Discharge Act and related wastewater mandates, chelates must demonstrate natural remediation in aquatic environments. In response, Nouryon and BASF are expanding capacity for Dissolvine GL to serve industrial cleaning and water treatment customers, positioning biodegradable metal chelates as essential enablers of compliance-driven, sustainable operations.

Metal Chelates Market Share and Segmentation Insights

Aminopolycarboxylic Acid Chelates Lead Metal Chelates Market with Strong Metal Complexation Performance

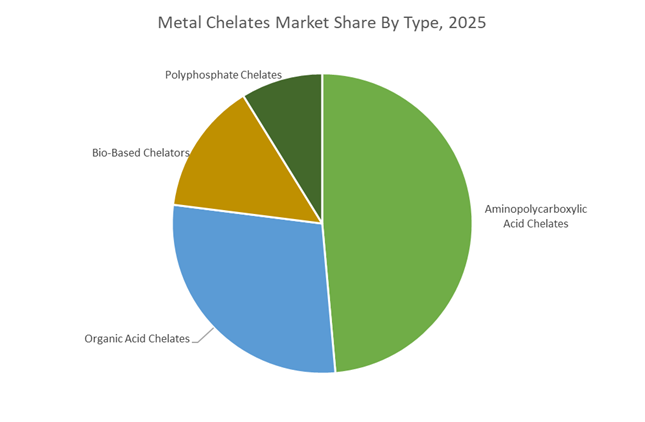

Aminopolycarboxylic acid chelates accounted for 48.60% of the Metal Chelates Market share in 2025, making them the most widely used chelating agents across agriculture and industrial processing sectors. This category includes widely used compounds such as EDTA (ethylenediaminetetraacetic acid), DTPA (diethylenetriaminepentaacetic acid), EDDHA (ethylenediamine-N,N'-bis(2-hydroxyphenylacetic acid)), and IDHA, which are valued for their strong ability to bind metal ions and maintain stability across a wide pH range. These chelates are extensively applied in micronutrient fertilizers, water treatment systems, detergents, and industrial metal processing, where controlling metal ion availability is essential for process efficiency and product performance. Their strong complexation properties ensure that metals such as iron, zinc, copper, and manganese remain soluble and bioavailable, particularly in challenging soil or industrial environments. In 2025, EDDHA chelates have emerged as a high-value segment due to their superior stability in calcareous and alkaline soils, where conventional chelates such as EDTA may degrade or precipitate, enabling improved iron delivery in high-pH agricultural soils.

Agriculture Sector Drives the Largest Demand for Metal Chelates in Micronutrient Fertilization

Agriculture accounted for 62.80% of the Metal Chelates Market share in 2025, making crop nutrition the dominant application segment for chelating agents. Metal chelates are widely used in micronutrient fertilizers and plant nutrition products, ensuring that essential trace metals including iron, zinc, manganese, and copper remain available for plant uptake in soil and hydroponic systems. Many agricultural soils suffer from micronutrient deficiencies or high pH conditions that limit metal solubility, which can reduce crop productivity and quality. Chelated nutrient formulations prevent metal precipitation and maintain stable, plant-available nutrient forms, improving nutrient absorption and crop performance. In 2025, the expansion of precision agriculture technologies has significantly influenced metal chelate usage patterns. Farmers increasingly apply chelated micronutrients through targeted foliar sprays, fertigation systems, and in-furrow delivery methods, enabling precise nutrient management based on soil testing and crop monitoring data. This targeted approach improves nutrient efficiency, reduces fertilizer waste, and supports higher crop yields in modern high-efficiency farming systems.

Metal Chelates Market Competitive Landscape

The metal chelates market in 2026 is driven by high-stability ligands (HBED, EDDHA), biodegradable chelating agents, and precision nutrient delivery systems. AI-enabled fertigation, drone-compatible liquid chelates, and pH-stable micronutrients are redefining agricultural productivity, reducing metal loading while improving bioavailability in alkaline and calcareous soils.

Nouryon leads high-stability HBED chelates for extreme alkaline soil performance

Nouryon dominates with its patented HBED iron chelate technology, delivering unmatched stability (up to pH 12), UV resistance, and 100% ortho-ortho bonding for maximum bioavailability in calcareous soils. Its ISCC PLUS-certified green chelates production supports biodegradable, renewable-based inputs aligned with EU Green Deal targets. Expansion via its Shanghai Innovation Center strengthens localized solutions for high-value crops, while Adsee® Flex 960 enhances foliar uptake efficiency. Nouryon’s focus on Precision Agriculture 2.0 positions it as the benchmark for high-performance, sustainable micronutrient chelation systems.

BASF integrates digital farming with biodegradable GLDA and MGDA chelates

BASF SE is advancing precision agriculture through drone-compatible chelated zinc-iron blends and its xarvio® platform, enabling real-time soil mapping and targeted micronutrient application. Its Verbund integration supports cost-efficient production of GLDA and MGDA biodegradable chelates, replacing EDTA in both agriculture and industrial applications. With a strong 2026 EBITDA outlook (€6.2–€7.0 billion), BASF is scaling prescriptive nutrient solutions that reduce environmental impact while improving yield efficiency in large-scale farming systems.

Haifa Group optimizes fertigation with high-efficiency EDDHA and HBED chelates

Haifa Group is a leader in specialty plant nutrition, combining water-soluble fertilizers with high-stability chelates such as EDDHA and HBED (HaiFer™ Max) for alkaline soil conditions. Its NutriNet™ Reci platform enables precise nutrient dosing in closed-loop irrigation, reducing runoff and improving water-use efficiency. Innovations like Haifa Soluble™ DUO stabilize root-zone pH and prevent nutrient lockout. With a strong push toward renewable energy integration, Haifa is advancing sustainable fertigation solutions for greenhouse and hydroponic agriculture.

Yara scales AI-driven chelated nutrition through global precision farming platforms

Yara International is leveraging AI-powered platforms like YaraIrix and Atfarm to deliver site-specific chelated micronutrient recommendations, shifting agriculture toward sub-field precision. Its YaraVita™ range, supported by a global logistics network across 140+ markets, ensures high-availability micronutrients with reduced Scope 3 emissions. With $15.7 billion in 2025 revenue and reinvestment into specialty nutrient R&D, Yara is integrating chelates with biostimulants to enhance crop resilience and productivity under climate stress conditions.

ICL Group advances controlled-release chelates with AI-driven nutrient optimization

ICL Group is strengthening its position through controlled-release and high-solubility chelate technologies, including Osmocote 5 with NutriTrace™ for sustained micronutrient delivery. Its Micromax range targets root-zone efficiency in intensive horticulture and greenhouse systems. Backed by $7.15 billion in 2025 sales, ICL is investing in AI-powered soil analytics and specialty crop nutrition, enabling ROI-driven precision farming. Its shift toward execution-focused climate-tech solutions reinforces its role in next-generation, data-driven chelated nutrient systems.

United States: Biodegradable Chelation and Supply Chain Localization

The United States metal chelates market is advancing through regulatory alignment and domestic capacity reinforcement. Tightening EPA and Safer Choice criteria during 2025–2026 have accelerated the transition away from persistent aminopolycarboxylates toward biodegradable alternatives. In April 2025, BASF introduced Trilon G, a GLDA-based chelating agent designed for Home Care and Industrial and Institutional cleaning applications, positioning biodegradable chelation as a default specification rather than a niche option. This shift is reducing regulatory risk while maintaining sequestration efficiency across hard-surface cleaning and water treatment formulations.

Supply chain resilience is becoming a parallel priority. BASF announced the start-up of a new Cincinnati, Ohio production line scheduled for 2026 to scale bio-based surfactants and chelating solutions for North America. Tariff pressures in 2025, including up to 25% duties on certain steel and aluminum imports, have further catalyzed localization of metal alkyl and complex metalorganic synthesis to protect margins. Downstream demand is strengthening in precision agriculture and pharmaceuticals. By late 2025, U.S. ag-tech platforms combining satellite imagery with precision delivery improved micronutrient uptake efficiency by 28% for zinc and iron chelates in poor-soil Midwest regions. Pharmaceutical integration is also rising, with North American labs reporting a doubling of chelated mineral production volumes between 2023 and 2025 as clinical evidence shows higher absorption for iron and magnesium chelates in metabolic therapies.

China: Catalyst Localization and Green Chemistry Scale-Up

China’s metal chelates market is expanding through high-performance polymer demand and policy-led green chemistry initiatives. In October 2025, Nouryon completed a major capacity expansion at its Jiaxing site, doubling output of triethylaluminum, a chelation-enabled co-catalyst critical for packaging and automotive polymers. This expansion aligns with China’s push to localize advanced catalyst supply chains amid growing domestic consumption.

Strategic localization continues with Nouryon’s plan to begin Modified Methylaluminoxane production domestically by 2027, with 2026 designated as the infrastructure build-out year to support the solar panel value chain. Policy support under the Ministry of Industry and Information Technology 2026 work plan is accelerating Eco-Smart fermentation hubs in Jiangsu, where bio-sourced chelators are achieving purities of 99.5%. Innovation capacity is being reinforced through a new organic peroxides and metal alkyls center scheduled to open in Tianjin in 2026, enabling faster Asia-Pacific product development and customization.

India: Chemical Hubs and Agrochemical Value Chain Upgrading

India’s metal chelates market is being reshaped by industrial policy and investment incentives that prioritize specialty chemicals. Under the NITI Aayog 2025 Chemical Industry Strategy, the country is developing world-class chemical hubs with shared infrastructure and a dedicated Chemical Fund to stimulate production of high-value chelates. This framework supports domestic synthesis of micronutrient chelates and specialty catalysts, reducing reliance on imports.

The Production-Linked Incentive scheme is translating policy into capital deployment across agrochemicals and micronutrients, supporting India’s ambition to increase its share of the global chemicals value chain by 2030. Corporate stabilization is also improving execution capacity. Nouryon India earned Great Place to Work Certification in 2025, signaling a maturing operational environment for chelating agent production in Mahad and Mumbai. These developments collectively position India as a scalable producer for agriculture and specialty formulations rather than a contract manufacturing base alone.

Netherlands: Certified Green Chelates and Water Treatment Leadership

The Netherlands continues to lead Europe’s transition toward certified sustainable chelation. In January 2025, Nouryon achieved ISCC PLUS certification at its Herkenbosch site, validating the use of bio-based and sustainable raw materials in GLDA and MGDA product lines. This certification is increasingly decisive for procurement in home care, industrial cleaning, and water management applications across the EU.

Application leadership is evident in wastewater treatment. During 2025, Dutch municipal utilities deployed advanced metal chelates within circular management systems to address heavy metal contamination, achieving a 42% reduction in metal ion concentrations in treated water. This outcome reinforces the Netherlands’ role as a reference market where sustainability credentials and measurable performance converge.

Thailand: Southeast Asian Supply Hub for Personal Care and I&I

Thailand is consolidating its position as a regional supply hub for metal chelates and specialty surfactants serving Southeast Asia. In November 2025, BASF inaugurated expanded production capacity in Bangpakong, enhancing proximity to fast-growing personal care and industrial markets. The site’s role as a distribution and formulation node supports shorter lead times and localized product specifications across ASEAN economies.

Brazil: Renewable Manufacturing and Formulation Innovation

Brazil’s metal chelates market is differentiating through low-carbon manufacturing and customer-centric innovation. By late 2024 and early 2025, domestic production of sodium chlorate and related chelating agents transitioned to 100% renewable electricity, significantly lowering the carbon footprint for the pulp and paper supply chain. This shift aligns chelation chemistry with decarbonization commitments across forestry-based industries.

Innovation capacity expanded in December 2025 when Nouryon opened a customer experience and innovation center in Brazil. The center is designed to accelerate development of sustainable home and personal care formulations tailored to South American market needs, strengthening Brazil’s role as both a manufacturing base and an application development hub.

Country-Level Strategic Positioning in the Metal Chelates Market

Metal Chelates Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Chelate Types

|

Policy or Institutional Driver

|

Competitive Differentiation

|

|

United States

|

Biodegradable substitution and localization

|

GLDA, iron, zinc chelates

|

EPA Safer Choice, tariffs

|

Regulatory-led innovation with domestic capacity

|

|

China

|

Catalyst localization and green chemistry

|

Aluminum alkyls, bio-chelators

|

MIIT Eco-Smart mandate

|

Scale with high-purity production

|

|

India

|

Specialty chemical hubs and agrochemicals

|

Micronutrient chelates

|

NITI Aayog, PLI

|

Integrated growth platform

|

|

Netherlands

|

Certified sustainable chelates

|

GLDA, MGDA

|

ISCC PLUS, water standards

|

Sustainability and performance benchmark

|

|

Thailand

|

Regional supply and formulation

|

Chelates for personal care

|

ASEAN demand growth

|

Proximity-driven agility

|

|

Brazil

|

Renewable manufacturing and innovation

|

Sodium chlorate-based chelates

|

Renewable energy transition

|

Low-carbon differentiation

|

Metal Chelates Market Report Scope

Metal Chelates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$750.6 Million

|

|

Market Size (2034)

|

$1577.2 Million

|

|

Market Growth Rate

|

8.6%

|

|

Segments

|

By Type (Aminopolycarboxylic Acid Chelates, Organic Acid Chelates, Polyphosphate Chelates, Bio-Based Chelators), By Metal Ion (Iron, Zinc, Manganese, Copper, Magnesium, Calcium), By Form (Powder, Liquid), By Application (Agriculture, Industrial Processing, Healthcare, Consumer Products), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Turf and Ornamentals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Nouryon, Dow, AkzoNobel, Mitsubishi Chemical Group, Nippon Shokubai, Yara International, Valagro, Kemira, Innospec, LANXESS, Jungbunzlauer, Haifa Group, Hexion

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Chelates Market Segmentation

By Type

- Aminopolycarboxylic Acid Chelates

- Organic Acid Chelates

- Polyphosphate Chelates

- Bio-Based Chelators

By Metal Ion

- Iron

- Zinc

- Manganese

- Copper

- Magnesium

- Calcium

By Form

By Application

- Agriculture

- Industrial Processing

- Healthcare

- Consumer Products

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Turf and Ornamentals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Metal Chelates Market

- BASF

- Nouryon

- Dow

- AkzoNobel

- Mitsubishi Chemical Group

- Nippon Shokubai

- Yara International

- Valagro

- Kemira

- Innospec

- LANXESS

- Jungbunzlauer

- Haifa Group

- Hexion

*- List not Exhaustive