Muconic Acid Market 2025–2034: Bio-Based Adipic Acid Pathways, Fermentation Scale-Up, and Nylon-6,6 Decarbonization

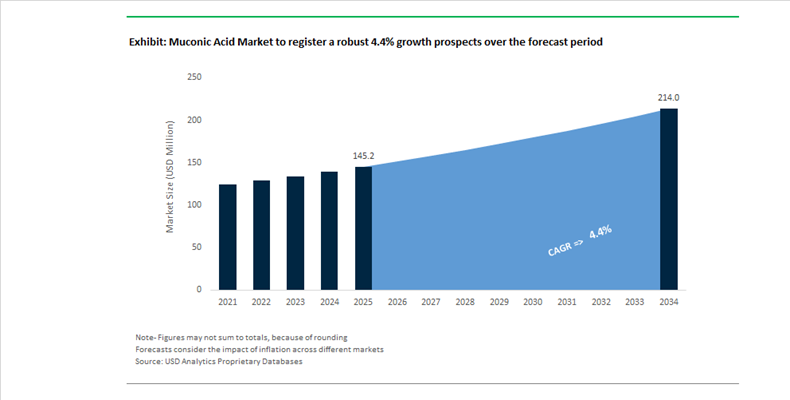

The Muconic Acid Market is projected to grow from $145.2 Million in 2025 to $213.9 Million by 2034, registering a CAGR of 4.4%. Muconic acid has transitioned from a niche biochemical intermediate to a strategic platform molecule for bio-based adipic acid, terephthalic acid substitutes, and sustainable nylon-6,6 value chains. The market’s structural expansion is being driven by three converging forces: decarbonization of engineering plastics, trade friction in petrochemical adipic acid, and rapid advances in precision fermentation and synthetic biology. As regulatory and ESG mandates intensify across Europe and North America, muconic acid is increasingly positioned as a renewable alternative to benzene-derived intermediates used in polyamides, polyesters, coatings, and specialty resins.

In November 2025, Amyris, Inc. unveiled its “Unlock The Chemistry of Life™” strategy, signaling a definitive pivot toward B2B renewable molecules, including fermentation-derived muconic acid derivatives. Earlier, in May 2025, Amyris acquired the remaining 31% stake in its Barra Bonita precision fermentation facility in Brazil, consolidating 100% ownership and announcing expansion of a fourth fermentation line. This move substantially increases industrial-scale capacity for bio-based intermediates and strengthens supply reliability for polymer, flavor, and specialty material customers. In September 2025, the return of Dr. Sunil Chandran as CTO reinforced the company’s focus on optimizing microbial yield efficiency and strain robustness, critical for lowering production costs in competitive bulk chemical markets.

Trade policy has amplified interest in local bio-based production. In late 2025, the European Union identified provisional dumping margins of 28.6%–46.8% on adipic acid imports from China. This development has accelerated European demand for fermentation-based muconic acid as a precursor to domestically produced “green” adipic acid, enabling nylon-6,6 manufacturers to mitigate tariff exposure and reduce lifecycle emissions. In parallel, BASF SE finalized its acquisition of Solvay’s polyamide 6.6 business in January 2025, strengthening its engineering plastics portfolio for e-mobility and autonomous systems. The integration enhances BASF’s capacity to incorporate renewable adipic acid pathways, including those derived from muconic acid, into advanced lightweight automotive components.

Strategic partnerships further validate commercialization momentum. Throughout 2025, Genomatica (Geno) advanced its collaboration with Asahi Kasei to develop plant-based Nylon-6,6 using muconic acid intermediates from sugar fermentation. Prototype fiber production milestones signal a viable shift from the conventional benzene-to-adipic acid petrochemical route. Meanwhile, India Glycols reported in late 2024 a surge in shipments of bio-based derivatives incorporating muconic acid stabilizers, serving the rapidly expanding Indian agrochemical sector seeking non-toxic additive systems.

Supply chain resilience has also strengthened. In 2024, Sigma-Aldrich expanded its Schnelldorf, Germany distribution hub by 25,000 square meters, stabilizing global availability of high-purity muconic acid isomers for pharmaceutical and advanced materials research. Concurrently, regulatory momentum in Europe intensified with the launch of ECHA’s first mandatory microplastic emission reporting cycle in early 2026. This policy environment increases R&D investment in biodegradable polymer systems, positioning muconic acid as a foundational building block for non-persistent polyesters and circular-material solutions.

Technological acceleration continues. In early 2026, academic-industrial collaborations, including research teams at Zhejiang University, published a CRISPR/Cas9 toolkit for Pichia pastoris that enables rapid, marker-less multigene pathway integration. This breakthrough shortens strain engineering timelines and improves metabolic efficiency for industrial-grade muconic acid production from lignocellulosic waste streams. The convergence of fermentation scale-up, trade protectionism in petrochemicals, polymer decarbonization strategies, and synthetic biology innovation defines the competitive trajectory of the global muconic acid market through 2034.

Muconic Acid Market Trends and Opportunities

Trend: Strategic Scale-Up of Bio-Based Production for Nylon and PET Precursors

The muconic acid market is entering a decisive scale-up phase as chemical producers pursue fermentation-led routes to decarbonize nylon and polyester value chains. Muconic acid has emerged as a central bio-platform intermediate capable of replacing fossil-derived adipic acid and terephthalic acid, two of the most emissions-intensive building blocks in the global polymers industry. By leveraging lignocellulosic sugars and lignin-derived aromatics, manufacturers are targeting structural reductions in Scope 3 emissions across the $30 billion-plus nylon and PET ecosystem while maintaining compatibility with existing polymerization infrastructure.

Cost competitiveness is no longer a theoretical objective. Technical assessments released in 2024–2025 by leading U.S. bioenergy programs demonstrated that bio-based adipic acid synthesized via muconic acid hydrogenation can reach a target selling price of approximately $2.60 per kilogram. This represents a meaningful inflection point, narrowing the historical cost gap with petroleum-based adipic acid while delivering up to 80% lower greenhouse gas emissions on a life-cycle basis. From an investor and offtaker perspective, this cost parity milestone materially improves the bankability of large-scale bio-muconic acid assets.

Equally important is the progress in biological productivity and scale readiness. Engineered Pseudomonas putida strains have achieved titers exceeding 47 g/L and carbon yields of roughly 0.50 C-mol per C-mol from mixed glucose and xylose feedstocks. These metrics have now been validated in 150-liter bioreactors, signaling a credible pathway from pilot to commercial demonstration as early as 2026. Parallel breakthroughs in lignin valorization further strengthen the case. In late 2024, a consortium successfully demonstrated green PET derived from lignin through a muconate intermediate, positioning muconic acid as the molecular bridge that decouples plastic bottle production from fossil benzene. Collectively, these developments reposition muconic acid from a niche bio-chemical into a strategic decarbonization lever for global polymer supply chains.

Trend: Muconic Acid as a High-Performance Monomer for Specialty Coatings

Beyond bulk intermediates, muconic acid is gaining traction as a differentiated monomer for specialty and performance materials. Its conjugated diene backbone and dual carboxylic functionality enable polymer architectures with higher cross-link density, thermal stability, and mechanical resilience than conventional maleic or phthalic acid systems. This intrinsic chemistry advantage is driving interest from coatings and advanced materials formulators seeking durability without reliance on legacy aromatic feedstocks.

In 2025, industrial R&D activity expanded into UV-resistant and weather-stable coatings for automotive, aerospace, and industrial equipment applications. Polymers derived from muconic acid exhibit enhanced resistance to photodegradation and thermal cycling, attributes that are increasingly critical as OEMs extend warranty periods and demand coatings that perform under extreme operating conditions. The unsaturated structure of muconic acid enables controlled cross-linking during curing, resulting in tougher films with superior adhesion and longer service life.

Isomeric differentiation is also shaping market value. Among the three muconic acid isomers, trans,trans-muconic acid is emerging as the preferred building block for high-performance engineering plastics due to its higher melting point and efficient molecular packing. These characteristics translate into improved dimensional stability and electrical performance, supporting applications in electronics housings, connectors, and advanced manufacturing components. As a result, the market is evolving toward isomer-specific pricing and application-driven demand, reinforcing muconic acid’s transition from a commodity bio-intermediate to a specialty monomer with defensible margins.

Opportunity: Biodegradable Muconate Chelators for Precision Agriculture

A high-potential growth avenue is emerging in precision agriculture, where muconic acid derivatives are being developed as biodegradable chelating agents to address micronutrient deficiencies in alkaline and calcareous soils. Conventional chelators such as EDTA are increasingly scrutinized for environmental persistence and groundwater contamination, creating a regulatory and sustainability gap that muconate-based alternatives are well positioned to fill.

Academic and applied research published in 2025 demonstrates that muconate chelators can effectively complex essential micronutrients such as zinc, iron, manganese, and copper while achieving complete biodegradation within a single growing season. This combination of nutrient delivery efficiency and environmental compatibility directly addresses the micronutrient uptake challenges faced by high-intensity agriculture without introducing long-lived residues into the soil ecosystem.

Policy alignment further strengthens this opportunity. Under government-backed biomanufacturing initiatives such as the BioE3 Policy, funding is increasingly directed toward climate-resilient agricultural inputs. Muconate-based fertilizers and micronutrient blends are being positioned as next-generation solutions that prevent nutrient fixation, reduce runoff, and improve crop productivity by an estimated 15 to 20% in deficient regions. For muconic acid producers, this represents a pathway into recurring, high-volume agricultural demand anchored in sustainability-driven procurement.

Opportunity: Platform Chemistry for Pharmaceuticals and Cosmetic Actives

Muconic acid’s designation as a bioprivileged molecule is opening doors in pharmaceuticals and cosmetics, where demand is shifting toward renewable, multifunctional building blocks. Its rigid, unsaturated six-carbon framework offers synthetic versatility, enabling the construction of complex intermediates that are difficult to access through traditional petrochemical routes.

In pharmaceutical R&D, muconic acid is being explored as a precursor for antioxidant and anti-inflammatory compounds, as well as intermediates used in advanced drug delivery systems. Its structure facilitates efficient synthesis of caprolactone-related molecules and other functional building blocks, supporting innovation in controlled-release and specialty therapeutics. As highly potent and differentiated drug candidates dominate development pipelines, bio-based intermediates that offer structural novelty and sustainability credentials are gaining strategic relevance.

The cosmetics sector presents a parallel opportunity. Muconic acid derivatives are being patented as bio-based preservatives and stabilizers for premium skincare and personal care formulations. These compounds align with clean-label positioning while delivering functional performance comparable to synthetic antioxidants. With an estimated 40% of the chemical industry actively transitioning toward renewable ingredients to meet consumer and regulatory expectations, muconic acid is well positioned to serve as a foundational platform molecule across life sciences and beauty applications, extending its market relevance well beyond polymers and materials.

Muconic Acid Market Share and Segmentation Insights

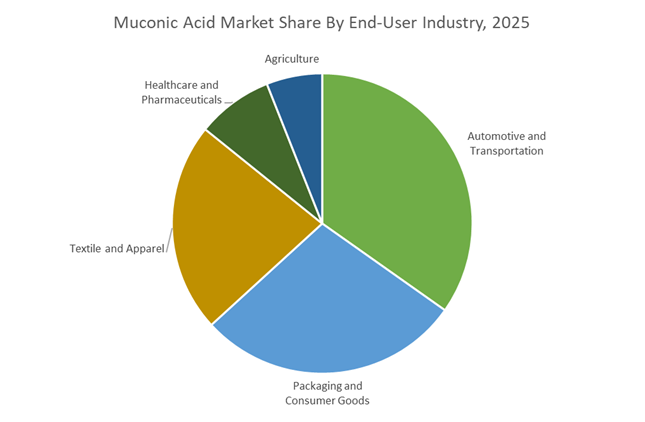

Automotive and Transportation Sector Leads Muconic Acid Market Through Demand for Bio-Based Engineering Plastics

Automotive and transportation accounted for 34.80% of the Muconic Acid Market share in 2025, making it the largest end-use industry for muconic acid-derived chemicals and polymers. Muconic acid serves as a critical intermediate for producing bio-based adipic acid and engineering polymers such as nylon and polyamides, which are widely used in automotive components that require high mechanical strength, thermal stability, and chemical resistance. These materials are commonly incorporated into under-hood engine components, fuel system parts, connectors, electrical housings, and interior structural elements, where performance under high temperature and mechanical stress is essential. The automotive industry’s shift toward lightweight polymer materials to replace heavier metal components continues to expand the use of advanced engineering plastics derived from renewable chemical intermediates such as muconic acid. In 2025, increasing focus on circular economy strategies and sustainable material sourcing has strengthened interest in muconic acid-based polymers, as they offer renewable carbon content while maintaining compatibility with existing polymer recycling systems used in automotive manufacturing supply chains.

Muconic Acid Market Competitive Landscape

The muconic acid market in 2026 is driven by precision fermentation, CRISPR-based metabolic engineering, and lignin-derived feedstocks. Competitive advantage centers on high-titer production (>50 g/L), process intensification, and integration into adipic acid and nylon-6,6 value chains for low-carbon bio-based chemicals.

Amyris scales precision fermentation capacity to accelerate bio-based muconic acid commercialization

Amyris, Inc. is emerging as a key biomanufacturing leader by scaling precision fermentation infrastructure for high-value bio-based intermediates. Its expanded Barra Bonita facility, featuring new 2x80m³ fermentation lines alongside existing 200m³ capacity, enables rapid commercialization of engineered molecules. Full ownership of the plant strengthens operational control and accelerates lab-to-market deployment of CRISPR-optimized yeast strains. Amyris leverages AI-driven synthetic biology and robotics to enhance yield optimization and strain performance. Its vertically integrated model supports sustainable production of polymer precursors, including muconic acid derivatives. The company’s focus on scalability and process automation positions it strongly in the transition from pilot to industrial-scale fermentation.

BASF integrates biomass-balanced intermediates with Verbund systems to advance bio-based chemical production

BASF SE is leveraging its Verbund integration to incorporate muconic acid pathways into its biomass balance (BMB) chemical portfolio. Its Geismar facility expansion supports commercial-scale production of sustainable polyether polyols, aligning with automotive and coatings demand. BASF’s ISCC EU and REDcert² certifications enable supply of traceable bio-based intermediates across regulated markets. Carbon Trust validation of reduced product carbon footprint strengthens its ESG positioning in specialty chemicals. Through participation in the MUCOFORM project, BASF is advancing lignin-based and industrial sidestream feedstocks for muconic acid conversion. Its strategy focuses on integrating renewable feedstocks into large-scale chemical infrastructure.

Merck supplies high-purity muconic acid isomers for pharmaceutical and advanced polymer research

Merck KGaA plays a critical role in the muconic acid ecosystem as a supplier of high-purity isomers for R&D and pilot-scale applications. Its cis,cis-muconic acid offers up to 92% conversion efficiency to adipic acid, making it essential for nylon precursor research. The company’s focus on API intermediates aligns with the growing use of bio-based organic acids in drug formulation. Merck supports over 40 global partnerships through its life science distribution network, enabling widespread access to research-grade materials. Its emphasis on purity, long shelf life, and consistency ensures reliability in specialty polymer and pharmaceutical development. This positions Merck as a foundational enabler of innovation in the bio-based chemicals market.

Myriant advances high-titer microbial fermentation for cost-competitive bio-based adipic acid production

Myriant Corporation is focusing on industrial-scale feasibility of muconic acid through advanced microbial fermentation technologies. Its engineered Pseudomonas putida strains achieve accumulation rates of 1.5 g/L/hour and production titers up to 50 g/L, significantly improving process efficiency. The company targets adipic acid replacement in nylon-6,6 production, aiming to reduce greenhouse gas emissions and dependency on petrochemicals. Myriant’s process intensification strategy addresses cost barriers, targeting a reduction of the current 20–30% premium over conventional methods. Its glucose-based feedstock conversion efficiency of 60% supports scalable production economics. The company’s integration-ready approach ensures compatibility with existing downstream chemical infrastructure.

Mitsubishi Chemical integrates muconic acid pathways into bio-based engineering plastics and decarbonization strategy

Mitsubishi Chemical Group is embedding muconic acid innovation within its “Planet Positive Chemicals” framework, targeting sustainable polymer markets. The adoption of DURABIO™ bio-based plastics in automotive and electronics applications highlights its commercialization capabilities. Strategic partnerships with Asahi Kasei and Mitsui Chemicals aim to decarbonize ethylene production, supporting renewable chemical intermediates. Mitsubishi is optimizing energy efficiency through technologies like ZEBREX™ zeolite membranes, reducing refining energy consumption by over 20%. Its shift toward healthcare and life sciences aligns with high-value applications of bio-based materials. The company’s integration of sustainability, advanced materials, and process efficiency strengthens its long-term competitive position.

United States: Bioprocess Scale, Nylon Chain Substitution, and State-Led Packaging Trials

The United States is emerging as a technology and commercialization anchor for the muconic acid market, driven by fermentation breakthroughs and strong policy alignment around low-carbon intermediates. In 2024–2025, National Renewable Energy Laboratory demonstrated a scalable bioprocess using Pseudomonas putida to convert renewable sugars into muconic acid. The process enables bio-adipic acid production at approximately $2.60 per kilogram while delivering an estimated 80% reduction in greenhouse gas emissions versus fossil-derived routes. This milestone materially improves the economic viability of muconic acid as a drop-in intermediate for the U.S. nylon 6,6 value chain and elevates its role in decarbonization strategies for engineered polymers.

Federal funding is reinforcing the transition from pilot to industrial scale. Under 2025 funding cycles, the U.S. Department of Energy directed grants toward upgrading large-scale fermentation units, including optimization programs led by Genomatica, to enable petroleum-free intermediates in domestic polymer production. Regulatory pull is also strengthening adoption. New 2026 EPA sustainable labeling guidelines are accelerating the use of cis,cis-muconic acid in high-performance polymers, adhesives, and lubricants that seek green chemistry certification. At the innovation frontier, U.S. biotech firms expanded intellectual property portfolios in late 2025 around cofactor engineering, pushing muconate yields toward 92% of theoretical maxima. In parallel, California’s plastics reduction mandates are catalyzing pilot-scale trials of muconic acid-derived bio-PET for food packaging, with commercial validation targeted for Q3 2026.

Germany: Co-Culture Fermentation, Biorefinery Integration, and Pharma-Grade Targeting

Germany’s muconic acid strategy is centered on advanced fermentation science, integration with existing industrial assets, and compliance-driven material substitution. In alignment with EU sustainability directives, German chemical groups are prioritizing cis,trans-muconic acid as a precursor for biodegradable resins that replace persistent aromatic compounds. Regulatory reporting obligations for 2026 under EU chemicals policy are reinforcing the shift toward bio-based dicarboxylic acids, positioning muconic acid as a preferred platform molecule.

On the technology side, research teams from the University of Stuttgart and industrial partners announced a modular co-culture fermentation breakthrough in August 2025. By deploying two specialized E. coli strains in sequence, researchers significantly increased muconic acid concentration in pilot reactors, improving volumetric productivity without proportional energy penalties. Infrastructure investment is following innovation. The German government allocated €200 million in late 2025 under its Circular Bioeconomy initiative, with a portion earmarked for embedding muconic acid production into wood-pulping and lignin-processing facilities. Strategic collaborations, including partnerships involving Evonik, are also advancing high-purity muconic acid grades for pharmaceutical synthesis, particularly as intermediates for anti-inflammatory compounds.

China: SynBio Acceleration, Dedicated Bio-Zones, and Agrochemical Diversification

China’s muconic acid market is advancing rapidly through state-backed industrial planning and synthetic biology optimization. Under the 2026 Green Manufacturing Blueprint issued by the Ministry of Industry and Information Technology, China is prioritizing the substitution of petrochemical dicarboxylic acids with bio-based alternatives. This policy has triggered the development of dedicated bio-chemical zones in Jiangsu and Wuhan, designed to co-locate fermentation, downstream purification, and polymer conversion assets.

Technological progress is reinforcing cost competitiveness. In August 2025, researchers at Hubei University of Technology reported the successful use of artificial intelligence to optimize enzyme pathways for muconic acid production, cutting enzyme degradation rates by 22% and materially lowering unit costs. Capacity scale-up is being supported by the National “111” Center in Wuhan, which received additional funding in 2025 to expand microbial consortia capable of converting complex industrial waste streams into muconic acid. Beyond polymers, China is also positioning muconic acid as a building block for next-generation bio-pesticides. Multiple state-linked enterprises filed patents in late 2025 for muconate-based fungicides that demonstrate higher soil biodegradability, broadening the domestic application base.

India: Fermentation Infrastructure Reuse and Carbon Capture Adjacencies

India’s muconic acid trajectory is shaped by indirect policy support, fermentation capacity availability, and emerging climate applications. Under the Scheme for Special Assistance to States for Capital Investment (SASCI) 2025–26, reforms in the mining and mineral sector are stabilizing access to catalytic materials used in purification steps for bio-acid production. While not a direct subsidy, this feedstock security improves the economics of domestic muconic acid initiatives.

Academic and industrial research is opening new use cases. In 2025, researchers at IIT Guwahati demonstrated that muconate-based adsorbents exhibit higher CO₂ affinity than conventional amine systems under high-moisture conditions, highlighting potential roles in carbon capture applications. Infrastructure synergies are also material. India’s aggressive ethanol blending targets for 2026 have created surplus fermentation capacity. By Q4 2025, several biotech firms announced diversification strategies to repurpose this excess capacity for muconic acid synthesis using sugarcane bagasse, enabling faster entry without greenfield investment.

Netherlands: Polymer Platform Convergence and Circular PET Pathways

The Netherlands is leveraging platform chemical convergence to accelerate muconic acid commercialization. Avantium confirmed in 2025 that its FDCA production technology is being adapted to trial muconic acid-based polyesters. This dual-pathway approach allows shared infrastructure to support multiple bio-monomers, improving capital efficiency at pilot and demonstration plants. The objective is to deliver fully recyclable bottle-grade materials for the European beverage sector by 2027.

Research institutions are reinforcing circularity ambitions. Wageningen-led projects funded during 2025–2026 are focusing on thermo-chemical conversion routes that transform muconic acid into terephthalic acid. This work is critical for establishing a closed-loop, bio-based alternative to fossil-derived PET within the EU. Together, these initiatives position the Netherlands as a systems integrator that bridges bio-based monomer production with downstream packaging applications.

Comparative Snapshot: Country-Level Positioning in the Muconic Acid Market

Muconic Acid Market County Level Snapshot

|

Country

|

Primary Strategic Lever

|

Core Application Focus

|

Structural Outcome

|

|

United States

|

Fermentation scale and policy pull

|

Nylon intermediates, bio-PET

|

Commercial readiness and IP leadership

|

|

Germany

|

Co-culture science and biorefinery integration

|

Biodegradable resins, pharma

|

High-purity, compliance-led supply

|

|

China

|

State-backed bio-zones and AI optimization

|

Polymers, agrochemicals

|

Cost-competitive, multi-application growth

|

|

India

|

Infrastructure reuse and CCUS adjacencies

|

Bio-acids, carbon capture

|

Capital-light entry and diversification

|

|

Netherlands

|

Platform convergence and circular polymers

|

Bio-PET, recyclable packaging

|

Integrated circular materials pathway

|

Muconic Acid Market Report Scope

Muconic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$145.2 Million

|

|

Market Size (2034)

|

$213.9 Million

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Product Type (Muconic Acid), By Production Method (Microbial Fermentation, Biomass-Derived Chemical Synthesis, Petroleum-Based Chemical Synthesis), By Application (Polymer Precursors, Plastics and Resins, Chemical Intermediates, Pharmaceuticals, Textiles), By End-User Industry (Automotive and Transportation, Textile and Apparel, Packaging and Consumer Goods, Healthcare and Pharmaceuticals, Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Genomatica, Myriant, Avantium, DSM-Firmenich, Amyris, Lygos, Deinove, Merck, Santa Cruz Biotechnology, Tokyo Chemical Industry, Hangzhou Dayangchem, Toronto Research Chemicals, Alfa Aesar, Zhongxing Flavors and Fragrance, Kyowa Hakko Bio

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Muconic Acid Market Segmentation

By Production Method

- Microbial Fermentation

- Biomass-Derived Chemical Synthesis

- Petroleum-Based Chemical Synthesis

By Application

- Polymer Precursors

- Plastics and Resins

- Chemical Intermediates

- Pharmaceuticals

- Textiles

By End-User Industry

- Automotive and Transportation

- Textile and Apparel

- Packaging and Consumer Goods

- Healthcare and Pharmaceuticals

- Agriculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Muconic Acid Market

- Genomatica

- Myriant

- Avantium

- DSM-Firmenich

- Amyris

- Lygos

- Deinove

- Merck

- Santa Cruz Biotechnology

- Tokyo Chemical Industry

- Hangzhou Dayangchem

- Toronto Research Chemicals

- Alfa Aesar

- Zhongxing Flavors and Fragrance

- Kyowa Hakko Bio

*- List not Exhaustive