Market Overview: Biodegradability, High VI Performance, and Biofuel Mandates Strengthen the Natural Fatty Acids Market Outlook

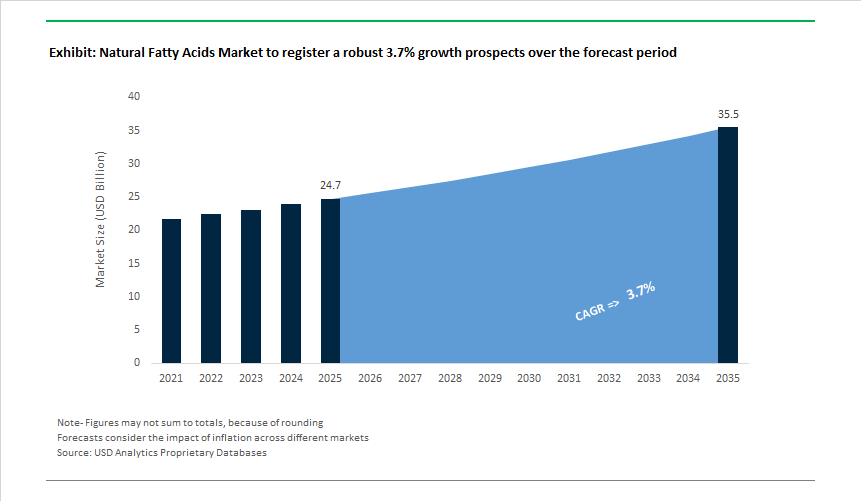

The Global Natural Fatty Acids Market is valued at USD 24.7 billion in 2025 and is expected to reach USD 35.5 billion by 2035, expanding at a 3.7% CAGR as natural fatty acids consolidate their role as mainstream, regulation-aligned alternatives to petrochemical intermediates. Market momentum is not being driven by novelty, but by a combination of regulatory certainty, performance parity (or superiority), and supply-chain familiarity that allows manufacturers to scale bio-based solutions without disrupting cost structures.

At a structural level, natural fatty acids benefit from built-in sustainability credentials that increasingly translate into commercial advantage. High biodegradability and renewable feedstock origins make fatty acids a preferred input across lubricants, surfactants, detergents, and personal care, particularly in regions where environmental compliance is shaping procurement decisions. Rather than relying on subsidies, demand is being reinforced by customer and regulatory preference for ingredients that meet environmental thresholds by default, reducing reformulation risk for downstream producers.

Performance economics are equally important. In industrial and specialty lubricant applications, fatty-acid-derived esters deliver high viscosity stability and reliable thermal behavior, enabling longer drain intervals and improved energy efficiency compared with mineral-oil-based systems. This allows equipment operators in agriculture, metalworking, and hydraulic systems to justify bio-based lubricants on total cost of ownership. As a result, adoption is expanding steadily even in cost-sensitive industrial segments.

The market is also undergoing value stratification. While commodity fatty acids continue to serve soaps, detergents, and bulk oleochemicals, fractionated and high-purity fatty acids are capturing disproportionate value growth. Medium-chain fatty acids such as C8 and C10 are increasingly specified in nutraceuticals, specialty lubricants, food additives, and high-performance formulations, where purity, consistency, and functional benefits support 40-60% pricing premiums. This is shifting competitive dynamics toward producers with fractionation capability, quality control, and application development expertise, rather than simple scale.

Regulation provides an additional demand anchor. In fuels, mandatory biodiesel blending requirements in major markets ensure long-term baseline consumption of fatty-acid-derived intermediates, while in personal care and home care, clean-label and plant-based positioning has moved from niche to norm. Today, an estimated 60% of global fatty acid volumes flow into personal care and cleaning applications, reflecting stable, consumer-driven demand rather than cyclical industrial exposure.

Market Analysis: Strategic Acquisitions, Fractionation Expansion, and Bio-Lubricant Innovation Drive Advancements

The Natural Fatty Acids industry recorded significant expansion and diversification, shaped by strategic acquisitions, new application breakthroughs, and regulatory momentum. A major development occurred in December 2025, when Louis Dreyfus Company executed a binding acquisition of BASF’s Food & Health Performance Ingredients business, consolidating global supply capacity for omega-3 fatty acids and specialty lipid formulations. Fractionation capacity continued growing in November 2025, as a leading Malaysian oleochemical producer announced a USD 50 million investment to expand high-purity Palmitic and Stearic Acid output, strengthening supply for plastics, rubber, and industrial processing markets. Regulatory progress followed in October 2025, when CEN advanced revisions to the EN 590 diesel standard-potentially lifting allowable FAME blending to 10% v/v-reinforcing future growth prospects in biofuel and energy markets.

Application innovations also intensified. In August 2025, a Brazilian bio-energy firm introduced soy-based bio-lubricants derived from oleic fatty acid esters, certified readily biodegradable and tailored for agricultural machinery and marine equipment-segments increasingly adopting bio-based lubricants to meet emission and environmental guidelines. R&D investment expanded further in June 2025, with Croda International opening an advanced lipid facility in Pennsylvania to develop high-purity fatty acid derivatives and C8-rich lipid systems for nutraceutical markets. In April 2025, Japanese research demonstrated enzyme-catalyzed hydroxy fatty acid production with >90% yield, improving sustainability and reducing dependence on chemical synthesis. Upstream supply chain capability strengthened in February 2025, when Cargill completed modernization of its Sidney, Ohio soybean processing facility, significantly boosting crush capacity to support food, feed, and FAME markets.

The foundational investment cycle was initiated earlier with December 2024 palm fractionation expansions at Port Klang, where Indonesian producers funded new dry-fractionation facilities tailored for food-grade and specialty chemical applications.

Natural Fatty Acids Market Trends and Opportunities

Trend 1: Shift Toward MCTs in Medical and Performance Nutrition

Medium-chain triglycerides (MCTs), derived from natural fatty acids, are increasingly becoming the preferred lipid source in clinical nutrition, metabolic therapy, and performance supplementation, driven by their rapid absorption and unique metabolic pathway. Unlike long-chain fatty acids, medium-chain fatty acids bypass lymphatic transport and are directly oxidized in the liver, making them highly efficient energy substrates. By late 2025, caprylic acid (C8) has emerged as the dominant MCT component, accounting for an estimated ~40% of MCT formulations, primarily due to its superior ketogenic efficiency. C8 converts into ketone bodies faster than C10 or C12, making it a core ingredient in medical foods targeting glucose metabolism disorders, mild cognitive impairment, and early-stage Alzheimer’s disease. Clinical evidence from 2024–2025 meta-analyses indicates that MCT-rich diets deliver ~1.5% greater weight loss versus long-chain fat diets, while endurance studies demonstrate improved lipid oxidation and delayed glycogen depletion in high-intensity athletic protocols. Commercially, North America has become the epicenter of MCT innovation, driven by clean-label positioning and the explosive growth of keto RTD beverages, functional coffees, and “edible beauty” supplements, where MCTs act as both an energy source and a bioavailability enhancer for fat-soluble actives such as vitamins A, D, E, K, and curcumin. This convergence of medical validation and lifestyle-driven demand is structurally embedding natural MCT fatty acids into premium nutrition value chains.

Trend 2: Development of Fatty Acid–Based Biopesticides and Plant Elicitors

Natural fatty acids are rapidly gaining traction in agriculture as biodegradable, residue-free alternatives to synthetic herbicides and insecticides, aligning with tightening regulatory frameworks and the global shift toward sustainable farming. Pelargonic acid (C9), a naturally occurring nonanoic fatty acid, has become a cornerstone of this transition due to its fast-acting, non-systemic herbicidal properties. By 2025, technical-grade pelargonic acid (>75% purity) dominates agricultural usage, particularly in vineyards, orchards, and specialty crops where precision weed control is essential. Its mode of action—disrupting plant cell membranes—delivers visible “burndown” within 2 to 24 hours, while leaving no long-term soil residues, making it highly compatible with organic and regenerative farming systems. In parallel, potassium salts of fatty acids (insecticidal soaps) have become standard tools in Integrated Pest Management (IPM), effectively controlling soft-bodied pests such as aphids and whiteflies through physical membrane disruption rather than neurotoxicity. Importantly, these compounds continue to benefit from regulatory exemptions in key markets, allowing last-day application without harvest delays. As regulatory pressure mounts against synthetic actives, fatty acid–based crop protection solutions are transitioning from niche organic inputs to mainstream agronomic tools, supported by their safety profile, rapid efficacy, and environmental compatibility.

Opportunity 1: Feedstock for Bio-Based Polymers and Epoxidized Oils

Natural fatty acids—particularly oleic, linoleic, and erucic acids—are emerging as critical feedstocks for the expanding bio-based polymer, lubricant, and plasticizer ecosystem. Government-led bioeconomy strategies between 2023 and 2025 have accelerated this shift, with policy frameworks explicitly prioritizing renewable carbon substitution in industrial materials. In the United States, federal biomanufacturing initiatives are actively supporting the conversion of fatty acids into epoxidized oils and bio-lubricants, targeting the displacement of petroleum-derived plasticizers in flexible PVC and elastomers. Parallel investment programs have allocated nearly $200 million toward facilities that upgrade agricultural feedstocks into bio-resins, bio-CNG, and specialty oleochemicals, creating a structurally favorable demand environment for high-purity fatty acid producers. From a materials-performance perspective, recent 2025 research has demonstrated that fatty acid–derived polyols—often blended with lignin or other bio-aromatics—deliver comparable thermal stability and mechanical strength to fossil-based equivalents, while reducing lifecycle carbon intensity by ~25%. These attributes position natural fatty acids as foundational building blocks in net-zero construction materials, sustainable packaging, and industrial lubricants, where regulatory compliance and carbon accounting are becoming procurement prerequisites rather than differentiators.

Opportunity 2: High-Oleic Oils as Functional Fats in Plant-Based Foods

High-oleic fatty acid profiles are reshaping formulation strategies across the plant-based meat, dairy alternative, and functional food sectors as manufacturers seek to eliminate trans fats while maintaining sensory performance. Oils containing >70% oleic acid, such as high-oleic canola and sunflower, have become the preferred replacements for partially hydrogenated oils due to their superior oxidative stability, neutral flavor, and extended shelf life. These characteristics are particularly critical in plant-based burgers, creamers, and ready-to-eat products, where lipid oxidation directly impacts taste, aroma, and consumer acceptance. A major breakthrough during 2024–2025 has been the development of oleogels, where high-oleic oils are structured using natural waxes or biopolymers to mimic the melting behavior and mouthfeel of animal fats like tallow or lard. This allows product developers to achieve “juiciness” and thermal behavior comparable to meat, while significantly lowering saturated fat content. Additionally, high-oleic oils are increasingly produced under Identity Preservation (IP) programs, ensuring traceability, non-GMO status, and clean-label compliance from seed to final product. This traceability enables suppliers to command price premiums and positions high-oleic fatty acids as strategic formulation assets rather than interchangeable commodity inputs in the rapidly scaling plant-based food economy.

Market Share Analysis: Natural Fatty Acids Market

Market Share by Type: Unsaturated Fatty Acids Anchor Specialty Oleo Growth

Unsaturated fatty acids command approximately 58% of the Natural Fatty Acids Market in 2025 because they align precisely with the performance and sustainability requirements of premium downstream formulations. Oleic- and linoleic-rich profiles remain liquid at ambient temperatures, enabling consistent dosing, superior oxidative behavior, and broad compatibility across cosmetics, lubricants, and nutraceuticals—advantages saturated grades cannot replicate without chemical modification. Scale and purity reinforce this dominance: Wilmar International anchors the segment with ~1.5 million tons of integrated capacity, maintaining 90%+ oleic purity through plantation-to-refinery control—an operational benchmark that de-risks supply for high-spec buyers. Growth dynamics further tilt share toward unsaturated chains; KLK OLEO tracks a 6.6% CAGR for the segment, materially outpacing saturated alternatives as formulators prioritize plant-based “omega” profiles and cleaner labels. Performance metrics translate directly into procurement decisions: data from Emery Oleochemicals show ~30% better cold-flow in bio-lubricants versus saturated fats, a decisive advantage for machinery operating across variable climates. On the chemistry side, the double-bond reactivity of unsaturated chains underpins adoption in bio-derivatives; 2025 manufacturer tracking indicates ~40% of new bio-based surfactants now originate from unsaturated feedstocks, enabling milder detergents and lower skin irritation—key value drivers that explain the segment’s structural majority.

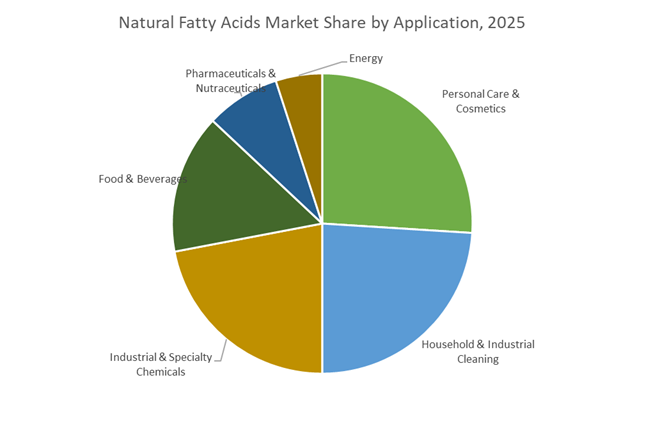

Market Share by Application: Personal Care & Cosmetics Lead Natural Substitution

Personal care and cosmetics hold around 26% of total demand, the largest single application, as global brands accelerate substitution away from petrochemical emollients toward traceable, bio-compatible fatty acid derivatives. Procurement momentum is demand-led and auditable: suppliers report that ~35% of fatty acid offtake is now cosmetic-grade, driven by a 31% rise in preference for RSPO-certified inputs in everyday products. Sustainability execution is no longer a marketing claim but a buying filter—Cargill reports 84% water recovery in hydrolysis operations, a hard metric Tier-1 OEMs use to qualify suppliers at scale. Regulatory risk mitigation also consolidates share; Cargill’s 2025 move to eliminate 100% of industrial trans-fatty acids (iTFAs) from edible and cosmetic streams establishes a “zero-iTFA” baseline that simplifies EU and North American compliance. Ethical sourcing closes the loop on brand risk: Musim Mas posted a 9.3/10 social impact score, placing it among the top global performers—an ESG credential increasingly embedded in long-term supply agreements. Together, verifiable sustainability, regulatory certainty, and formulation performance keep personal care the demand anchor, sustaining its market leadership as natural fatty acids displace fossil-based incumbents.

Competitive Landscape: Integrated Agribusiness Leaders and High-Purity Oleochemical Specialists Shape Global Progress

The Natural Fatty Acids market is defined by vertically integrated agribusiness giants and specialty chemical formulators that combine extensive feedstock control with advanced fractionation and derivatization technologies. Competitive advantage is increasingly shaped by RSPO-certified supply chains, bio-based ingredient innovation, global distribution networks, and investments in high-purity fatty acid derivatives for nutraceuticals, personal care, and engineered lubricants.

Cargill Incorporated - Integrated Oilseed Processing and Specialty Fat Innovation Strengthen Global Fatty Acid Leadership

Cargill operates one of the industry’s most fully integrated supply chains, transforming soybean, canola, and palm feedstocks into a broad portfolio of Natural Fatty Acids and tailored derivative systems. Its continued investment in dry fractionation technology enhances purity for specialty stearic and hydroxy stearic acid applications. Cargill’s direct linkage between raw material sourcing and biodiesel/FAME production provides strong resilience against commodity volatility. Its proprietary reduction of trans fatty acids to <0.5 g per serving in food-grade applications positions it as a preferred supplier in regulated markets.

KLK Oleo - Vertically Integrated Palm-Based Oleochemical Producer Powering Sustainable Global Supply Chains

KLK Oleo benefits from full upstream-to-downstream integration, delivering RSPO-certified Natural Fatty Acids and derivatives into personal care, detergents, elastomers, and industrial chemical markets. Its product range spans C8-C18 fatty acids, supporting specialty surfactants and performance formulations. With production hubs in Malaysia, Germany, and China, KLK Oleo serves both global and regional customers with localized blending and tailored fatty acid specifications for plastics, rubber, and technical-grade additive markets. Its commitment to sustainable surfactant technologies enhances its competitive positioning.

Croda International Plc - High-Purity Bio-Based Specialty Ingredient Innovator Advancing Premium Fatty Acid Derivatives

Croda’s leadership is anchored in high-purity fatty acid derivatives for premium personal care, healthcare, lubricants, and nutraceutical products. Its flagship brands (Priolube®, Cithrol®) dominate high-value application niches. The company is pioneering fermentation and biotechnology pathways to produce long-chain and hydroxy fatty acids from algae and renewable feedstocks. Croda also offers custom esterification services, producing complex mono- and diglycerides of Caprylic Fatty Acid (C8) for medical nutrition and high-performance supplements. Its 2030 target of achieving 75% bio-based raw materials reinforces internal demand for advanced oleochemical feedstocks.

Wilmar International Ltd. - Global Palm and Lauric Oil Powerhouse Driving High-Volume Fatty Acid and Glycerin Production

Wilmar leverages the world’s most extensive palm and lauric oil processing network to supply bulk Natural Fatty Acids and glycerin for soap, detergents, and global FAME markets. Its scale efficiencies support low-cost production and make it a dominant supplier of palm-derived oleochemicals. Downstream investments in refining and value-added derivatives enable Wilmar to participate in higher-margin personal care ingredient markets. Broad RSPO and ISCC certifications make Wilmar a strategic supplier for multinational corporations requiring transparent, sustainable ingredient sourcing.

Malaysia remains the global processing nucleus of the natural fatty acids market, but its 2025 trajectory is decisively oriented toward high-margin fractionation and downstream oleochemical specialization rather than bulk palm-based exports. A pivotal milestone was achieved with KLK OLEO reaching stable operations at its West Port specialty oleochemicals facility, which is engineered to produce refined fatty acid fractions and fatty alcohols tailored for premium European and North American personal care formulations. This shift underscores Malaysia’s strategy of defending margins amid tightening sustainability scrutiny by moving deeper into value-added processing.

At the policy level, the Malaysian Palm Oil Board (MPOB) renewed its 2025 R&D mandate to improve C16 and C18 yield profiles, reinforcing Malaysia’s competitiveness against soybean- and tallow-based fatty acids. Parallel to cosmetics and home care, Malaysia is also embedding itself into the Sustainable Aviation Fuel (SAF) value chain. In Q4 2025, EcoCeres successfully exported SAF from its Johor facility using waste-based natural fatty acids via the HEFA pathway, positioning Malaysia as both a fractionation hub and low-carbon fuel feedstock supplier.

Indonesia – Capacity Scale and Feedstock Resilience

Indonesia continues to anchor the volume end of the global natural fatty acids market, leveraging unmatched access to palm-based feedstocks to consolidate its role as the largest producer of distilled fatty acids and glycerin. In 2025, industrial momentum was reinforced by the commissioning of PT Lotte Chemical Indonesia’s IDR 59.37 trillion Cilegon complex. Although primarily petrochemical, the site integrates upstream chemical streams that support Indonesia’s soap, detergent, and surfactant industries, where natural fatty acids remain irreplaceable organic intermediates.

Export-linked growth remains robust. The Indonesian Ministry of Industry projects 6.5% expansion in the chemical and pharmaceutical sector in 2025, driven in part by strong overseas demand for fatty acid methyl esters (FAME). Supporting infrastructure is also being reinforced: the Chandra Asri chlor-alkali project, now one-third complete, will provide critical caustic soda inputs for domestic fatty acid processing, reducing reliance on imports and stabilizing operating economics across Indonesia’s oleochemical ecosystem.

United States – Enzymatic Processing and Green Chemistry Acceleration

The United States natural fatty acids market in 2025 is defined less by feedstock dominance and more by process innovation and regulatory pull-through. A major inflection point came with the Novonesis–thyssenkrupp Uhde collaboration, which introduced advanced enzymatic fat-splitting technology capable of materially lowering energy intensity in fatty acid separation. This development is strategically important for U.S. producers seeking to compete on carbon efficiency and flexibility, particularly for specialty oleochemicals and bio-lubricants.

Regulatory alignment has further accelerated adoption. Amendments under the Environmental Protection Agency (EPA) to the TSCA framework in early 2025 streamlined approvals for bio-based fatty acid derivatives, expanding their use in green cleaners, coatings, and industrial fluids. Simultaneously, the continued enforcement of the Renewable Fuel Standard (RFS)—targeting 36 billion gallons of renewable fuel blending—has structurally increased demand for soybean- and tallow-derived fatty acids as biodiesel and renewable diesel feedstocks, reinforcing fatty acids’ role in the U.S. energy transition.

Brazil – HEFA Biorefining and Soy-Based Feedstock Leadership

Brazil is rapidly ascending as a strategic SAF feedstock and conversion hub, underpinned by its dominance in global soybean production. A defining 2025 development was the Asian Infrastructure Investment Bank (AIIB) backing of Project HEFACo in Bahia—a biorefinery designed to process 20,000 barrels per day of natural oils and fatty acids into SAF using the HEFA route. This positions Brazil as a critical supplier of renewable aviation fuels at scale.

Feedstock security further strengthens this trajectory. According to Conab, Brazil’s 2025–26 soy planting reached 94.1% completion by December, ensuring stable oil availability despite earlier weather disruptions. Complementing HEFACo, Acelen finalized environmental approvals for a renewable fuels expansion at Mataripe, signaling a broader industrial push toward vegetable-oil side-stream valorization and long-term demand growth for natural fatty acids.

Germany – Biotechnology-Led Sustainable Formulation

Germany’s natural fatty acids market is firmly positioned at the innovation and formulation frontier, where renewable carbon is displacing fossil-based inputs across chemicals and personal care. A key pillar is the BASF–Acies Bio partnership, which advances fermentation technologies capable of producing fatty alcohols and acids from methanol—creating a scalable bridge between bio-based and industrial chemistry.

Downstream commercialization is equally active. Emery Oleochemicals expanded European distribution via LEHVOSS Functional Fluids, targeting automotive and industrial lubricants with high-performance fatty acid esters. Meanwhile, BASF’s launch of Emulgade® Verde aligns directly with EU clean beauty and deforestation-free sourcing mandates, reinforcing Germany’s leadership in high-spec, sustainability-certified fatty acid derivatives.

China – Capacity Discipline and Bio-Methanol Integration

China’s natural fatty acids market in 2025 is characterized by controlled growth and scientific capacity management rather than unchecked expansion. The joint 2025–2026 petrochemical growth plan issued by the National Development and Reform Commission and the Ministry of Industry and Information Technology targets >5% annual sector growth while tightly restricting new refining capacity. This policy explicitly favors refining-to-chemicals conversion and bio-based intermediates.

A tangible outcome is the commissioning of CIMC Enric’s 50,000 t/yr bio-methanol plant in Zhanjiang, which uses biomass gasification to supply low-carbon building blocks for bio-based esters and fatty acid derivatives. Pricing dynamics reflect this transition: mid-2025 FOB Shanghai prices for C8–C10 fatty acids corrected to around $3,730/MT, indicating efficiency-driven oversupply rather than structural demand weakness, as China recalibrates toward higher-quality, lower-carbon fatty acid outputs.

2025 Strategic Matrix: Natural Fatty Acids National Benchmarking

Natural Fatty Acids National Benchmarking

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

Malaysia

|

Downstream refining

|

KLK OLEO West Port specialty plant

|

Specialty fractions & personal care

|

|

Indonesia

|

Capacity scale

|

Lotte Chemical Cilegon COD ($3.6B)

|

FAME, soaps & detergents

|

|

United States

|

Enzymatic processing

|

Novonesis–thyssenkrupp enzyme launch

|

Biolubricants & green solvents

|

|

Brazil

|

SAF biorefining

|

Project HEFACo (20 kbpd HEFA)

|

Sustainable aviation fuel

|

|

Germany

|

Biotechnology leadership

|

BASF–Acies Bio fermentation rollout

|

Clean beauty & specialty esters

|

|

China

|

Capacity discipline

|

2-year petrochemical stabilization plan

|

Bio-based materials & fine chemicals

|

Natural Fatty Acids Market Report Scope

Natural Fatty Acids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.7 Billion

|

|

Market Size (2035)

|

$35.5 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Type (Saturated Fatty Acids, Unsaturated Fatty Acids), By Source (Plant-Based, Animal-Based, Non-Traditional), By Form (Oil/Liquid, Powder/Flakes, Beads/Prills, Capsules), By Application (Personal Care & Cosmetics, Household & Industrial Cleaning, Food & Beverages, Pharmaceuticals & Nutraceuticals, Industrial & Specialty Chemicals, Energy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Wilmar International Limited, Kuala Lumpur Kepong Berhad, Musim Mas Group, Emery Oleochemicals, IOI Oleochemicals, Godrej Industries, BASF SE, Oleon N.V., Kao Corporation, Cargill Inc., Vantage Specialty Chemicals, Croda International Plc, AAK AB, P&G Chemicals, Pacific Oleochemicals Sdn Bhd

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Natural Fatty Acids Market Segmentation

By Type

- Saturated Fatty Acids

- Unsaturated Fatty Acids

By Source

- Plant-Based

- Animal-Based

- Non-Traditional

By Form

- Oil / Liquid

- Powder / Flakes

- Beads / Prills

- Capsules

By Application

- Personal Care & Cosmetics

- Household & Industrial Cleaning

- Food & Beverages

- Pharmaceuticals & Nutraceuticals

- Industrial & Specialty Chemicals

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Natural Fatty Acids Market

- Wilmar International Limited

- Kuala Lumpur Kepong Berhad

- Musim Mas Group

- Emery Oleochemicals

- IOI Oleochemicals

- Godrej Industries

- BASF SE

- Oleon N.V.

- Kao Corporation

- Cargill, Incorporated

- Vantage Specialty Chemicals

- Croda International Plc

- AAK AB

- P&G Chemicals

- Pacific Oleochemicals Sdn Bhd

*- List not Exhaustive