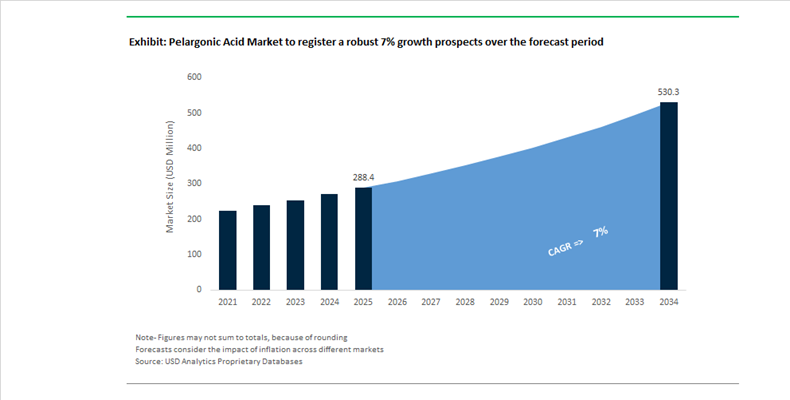

Pelargonic Acid Market Size 2025–2034: $288.4 Million to $530.2 Million at 7% CAGR Driven by Bio-Based Herbicide Commercialization and Regulatory Shifts

The global pelargonic acid market is projected to expand from $288.4 million in 2025 to $530.2 million by 2034, registering a robust CAGR of 7% during the forecast period. Market acceleration is directly linked to the rapid commercialization of bio-based non-selective herbicides, tightening glyphosate regulations, and rising adoption of sustainable carboxylic acids across agriculture, industrial cleaning, and specialty chemical applications. Pelargonic acid, also known as nonanoic acid, has gained structural relevance in the bio-herbicide market due to its rapid contact activity, zero soil residual profile, and compatibility with organic farming standards.

In October 2024, the New York State Department of Transportation issued its “Vegetation Management Guidance 2024,” explicitly recommending pelargonic acid for use in regulated arenas such as waterways and public infrastructure corridors. This regulatory endorsement materially increased municipal and infrastructure contractor adoption across the Northeast United States. In parallel, October 2024 marked a strategic inflection point when Emery Oleochemicals expanded its certified 100% bio-based pelargonic acid portfolio under the USDA BioPreferred® Program. The addition of EMERION® W 90 PA, 90 PA MUP, and 90 PA TG reinforced the shift toward high-performance, rapid-action, non-selective weed control solutions delivering visible effects within 15 minutes.

Field validation further strengthened the product’s commercial positioning. In late 2024, IR-4 Project trials confirmed that pelargonic acid applications leave no phytotoxic soil residues, enabling same-week crop rotation for sensitive greenhouse vegetables. This zero-residual trait has become a core marketing lever in 2025 targeting high-value horticulture, vertical farming, and protected cultivation markets where soil carryover risk directly impacts profitability.

Regulatory developments in October 2025 introduced temporary friction in Europe when the European Commission deferred the “low-risk” renewal status of pelargonic acid pending further validation of risk mitigation measures for non-target organisms. This decision has influenced bio-herbicide registration timelines through 2026 across EU member states. Despite this pause, market fundamentals remain strong, supported by government endorsements in North America and accelerating export activity in Asia and Latin America.

Financial restructuring and pricing dynamics are reshaping competitive supply chains. In September 2024, S&P Global upgraded OQ Chemicals following an amend-and-extend transaction that pushed debt maturities to December 2026, strengthening liquidity for continued carboxylic acid production. Subsequently, OQ Chemicals implemented pelargonic acid price increases in September 2025, followed by a further global adjustment in February 2026 for oxo-intermediates, citing raw material volatility and margin stabilization objectives amid corporate restructuring. These pricing recalibrations are influencing contract renegotiations across agrochemical distributors and industrial formulators entering 2026.

Leadership transitions are also shaping growth strategy. In July 2025, Emery Oleochemicals appointed Min Chong as Group CEO to expand the global footprint of its natural-based specialty chemicals portfolio, with pelargonic acid herbicides as a core strategic pillar. In August 2025, the company appointed a Global Sustainability Manager to align its pelargonic acid value chain with ESG compliance targets and EcoVadis Gold ambitions for 2026. Operational efficiency initiatives culminated in June 2025 with ISO 50001 certification at its Cincinnati plant, reinforcing low-carbon production credentials within the sustainable agrochemical market.

On the formulation front, late 2025 saw Croda Agriculture release enhanced technical data for its Pelargonic Acid 500 g/L EC formulations utilizing advanced polymeric emulsifiers. These developments improve emulsion stability and dilution resilience, positioning pelargonic acid products for industrial-scale vegetation management and infrastructure weed control markets in 2026. Meanwhile, trade data from August 2024 to July 2025 indicates that Matrìca S.p.A. redirected 54% of its azelaic and pelargonic acid exports toward Indonesia, signaling Southeast Asia’s rising demand for bio-based intermediates in agricultural and industrial cleaning applications.

Strategic Trends and Scalable Opportunities Reshaping the Pelargonic Acid Market

Rapid Shift Toward Bio-Herbicides as Regulatory and Consumer Pressures Intensify

Pelargonic acid is emerging as a cornerstone ingredient in the global transition away from synthetic herbicides, driven by tightening pesticide regulations and a clear shift in consumer preferences toward biodegradable, low-residue crop protection solutions. In the European Union, increasing scrutiny of glyphosate and other systemic herbicides has elevated pelargonic acid to a preferred non-selective contact herbicide for municipal weed control, organic farming, and specialty crops. Its ability to biodegrade in soil within roughly 48 hours positions it as a low-persistence solution aligned with sustainable land management objectives.

Regulatory engagement has been a defining catalyst. In October 2025, the Standing Committee on Plants, Animals, Food and Feed under the European Commission reviewed the renewal status of pelargonic acid, reaffirming its classification as a low-risk active substance while introducing targeted mitigation measures to protect non-target organisms. This approach is effectively filtering the market toward higher-quality, sustainably sourced nonanoic acid and raising the compliance bar for suppliers serving Europe.

Momentum is equally visible in North America. In March 2025, the Pest Management Regulatory Agency of Health Canada proposed the registration of additional pelargonic acid-based products, citing an acceptable environmental risk profile. These approvals support its use as a desiccant in potato and cereal crops and as a vineyard and orchard maintenance herbicide. Field-level validation further strengthens the case. Mediterranean trials conducted during 2024–2025 demonstrated that pelargonic acid applied at 16 to 18 liters per hectare achieved near-complete cotton defoliation, matching synthetic alternatives and enabling mechanical harvesting in organically certified cotton systems. Collectively, these developments are repositioning pelargonic acid from a niche bio-herbicide to a mainstream tool in low-impact agriculture.

Direct Corporate Investment Drives Sustainable and Circular Supply Chains

The pelargonic acid market is also being reshaped by a shift from transactional sourcing to direct asset ownership and vertical integration. Tier-1 chemical producers are increasingly acquiring production capabilities to secure long-term access to bio-based feedstocks and reduce exposure to petrochemical price volatility. This strategic pivot reflects growing confidence in sustained demand for fatty-acid-derived actives across agriculture, personal care, and industrial applications.

A clear signal of this trend emerged in April 2025 when AlphaBio Control divested its pelargonic acid business, including its sunflower oil-based MiSSiTO formulation. This transaction highlights a broader realignment in which specialized firms streamline portfolios while larger chemical groups acquire proven bio-based technologies to scale production globally. On the manufacturing front, green chemistry improvements are expected to lift production efficiency by up to 20% by 2027. Plant-derived sources such as sunflower, rapeseed, and tallow now account for more than 69% of global pelargonic acid supply, reflecting a decisive move away from fossil-based routes.

Looking ahead, fermentation-based production is gaining strategic attention. Updates from IEA Bioenergy in 2025 indicate that microbial synthesis pathways have reached pilot-scale viability, with the potential to cut lifecycle emissions to as low as 5 kilograms of CO2 equivalent per kilogram produced. While still emerging, these routes offer a long-term pathway to circular, low-carbon pelargonic acid supply.

Penetration into Premium Personal Care, Sanitization, and Biolubricants

Beyond agriculture, pelargonic acid is finding growing traction in non-agricultural applications that value purity, biodegradability, and performance. The most immediate expansion is in cosmetics and personal care, currently the fastest-growing end-use segment. Pelargonic acid esters are increasingly formulated as natural emollients in anti-aging and skin-barrier repair products, supported by strong demand for non-GMO and clean-label ingredients. Industry data from 2025 shows accelerated adoption by premium brands seeking multifunctional, plant-derived actives.

Industrial and institutional cleaning is another high-value avenue. Pelargonic acid serves as a precursor to peroxynonanoic acid, a powerful antimicrobial and bleaching agent used in food processing and hygiene-critical environments. Leading sanitation suppliers are highlighting its efficacy as a biodegradable alternative to chlorine-based disinfectants, aligning with stricter wastewater and worker-safety standards. In parallel, high-purity nonanoic acid is being utilized to synthesize polyol ester biolubricants for offshore wind turbines, marine equipment, and other environmentally sensitive installations. These lubricants are essential where mineral oil leakage is restricted, creating a durable demand base tied to renewable energy and maritime infrastructure growth.

Leveraging Government-Backed Bioeconomy Programs to Accelerate Scale-Up

Public policy is actively lowering the risk profile for investments in bio-based chemicals, creating a favorable environment for pelargonic acid capacity expansion and downstream innovation. In August 2024, India approved its BioE3 Policy, positioning bio-based chemicals and enzymes as priority sectors within the national objective to build a USD 300 billion bioeconomy by 2030. This framework provides public–private partnership platforms that can support domestic pelargonic acid production, formulation R&D, and export-oriented growth.

In the United States, the USDA BioPreferred Program continues to mandate federal procurement of bio-based products across a wide range of categories, including lubricants and cleaners. Pelargonic acid-based products carrying USDA certification gain preferential access to this demand pool, helping offset the higher upfront cost of natural fatty acid feedstocks. Regulatory stability in Europe further strengthens the investment case. The European Chemicals Agency maintains approved status for pelargonic acid under the biopesticide framework through 2026 to 2028 depending on application, offering a clear three- to five-year planning horizon for manufacturers.

Pelargonic Acid Market Share and Segmentation Insights

Natural Grade Pelargonic Acid Leads Market Demand in Bio-Based Chemical Applications

Natural grade pelargonic acid accounted for 58.60% of the Pelargonic Acid Market by grade in 2025, reflecting increasing demand for renewable fatty acids derived from vegetable oil feedstocks such as palm, coconut, and rapeseed. This bio-based chemical intermediate is widely used in herbicides, personal care formulations, and industrial cleaning products where natural origin provides regulatory and marketing advantages. Natural grade pelargonic acid supports sustainability initiatives across agricultural and consumer product industries. In 2025, manufacturers are strengthening certified renewable supply chains using ISCC Plus and RSPO standards, enabling product traceability and verified renewable content claims that support premium product positioning in bio-based chemical markets.

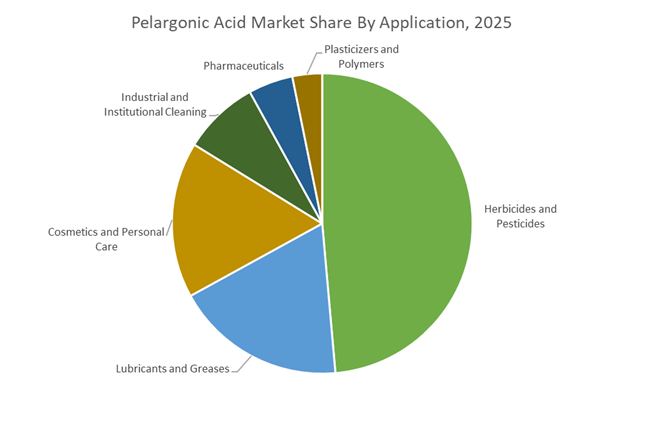

Herbicides and Pesticides Segment Drives Pelargonic Acid Consumption in Sustainable Crop Protection

Herbicides and pesticides represented 48.60% of the Pelargonic Acid Market by application in 2025, making it the largest demand segment across agricultural and vegetation management applications. Pelargonic acid functions as an active ingredient in contact herbicides used in organic farming, landscape maintenance, and residential weed control. Its rapid biodegradability and plant derived origin make it suitable for environmentally sensitive applications where synthetic herbicides face regulatory restrictions. In 2025, the expansion of organic agriculture and natural lawn care products is accelerating demand for pelargonic acid based herbicides that provide effective weed suppression while meeting consumer and regulatory expectations for bio-based crop protection solutions.

Pelargonic Acid Market Competitive Landscape

The Pelargonic Acid Market is transitioning toward bio-based oleochemicals, ISCC Plus-certified production, and sustainable herbicide applications. Leading players are leveraging oxidative cleavage technologies, vertical integration, and green chemistry to serve organic agriculture, personal care, and EV lubricant markets under tightening global regulatory frameworks.

Emery Oleochemicals leads bio-based pelargonic acid production with ozone cleavage technology

Emery Oleochemicals is a global leader in pelargonic acid production, leveraging proprietary ozone-based oxidative cleavage of vegetable oils to deliver high-purity bio-based acids. The expansion of its EMERION® portfolio with USDA BioPreferred-certified products strengthens its position in eco-friendly herbicides. Its EMERY® 1202 and 1210 grades provide enhanced performance in lubricants and corrosion inhibitors due to unique odd-chain structures. Sustainability credentials, including EcoVadis Silver and ISO 50001 certification, reinforce its low-carbon production model. Strategic leadership transition is driving focus toward specialty esters for EV fluids and high-growth applications. This integration of innovation, certification, and product diversification solidifies Emery’s market leadership.

Oxea strengthens specialty acid portfolio with ISCC Plus-certified bio-based pelargonic acids

Oxea is repositioning itself as a key player in specialty pelargonic acid through strategic realignment and sustainability integration. Its ISCC Plus-certified OxBalance portfolio enables production of bio-based pelargonic acids for EV lubricants and battery materials. The company’s pricing strategy, including a $95/mt increase, reflects strong demand and cost pass-through capability in specialty acids. Divestment of non-core assets and leadership restructuring enhance operational focus on core carboxylic acid production. Oxea’s solutions are also integral to carbon reduction programs, particularly in advanced coatings and energy storage applications. This combination of pricing power, sustainability, and industrial relevance strengthens its competitive positioning.

Croda expands bio-herbicide applications and specialty derivatives for agriculture and polymers

Croda International Plc is advancing its pelargonic acid portfolio through high-value applications in crop protection and specialty materials. Its Crop Protection segment achieved 14% growth in 2025, driven by increasing adoption of pelargonic acid as a biodegradable contact herbicide and desiccant. The company is investing in delivery systems to improve rain-fastness and leaf penetration, enhancing field performance. Pelargonic acid is also utilized as a key intermediate in high-performance polyamides for automotive lightweighting. Croda’s transformation program is reallocating resources toward bio-based surfactants and sustainable pesticide formulations. This focus on innovation and application diversification strengthens its position in premium markets.

Matrica advances biodegradable pelargonic acid formulations through integrated biorefinery model

Matrica S.p.A. is a leader in green chemistry-based pelargonic acid production, leveraging an integrated biorefinery model in Italy. Its BELOUKHA® formulations meet strict biodegradability standards, achieving 60% degradation within 28 days, aligning with global environmental regulations. Field trials demonstrate its effectiveness as a sustainable defoliant, matching synthetic alternatives while degrading rapidly in soil. Patented high-concentration formulations (40–90%) improve logistics efficiency and application performance. The company’s zero-waste model maximizes value by co-producing azelaic acid and glycerine. This integration of sustainability, innovation, and process efficiency strengthens Matrica’s competitive edge.

Kao integrates pelargonic acid into green consumer products and regional agriculture solutions

Kao Corporation is leveraging its strong presence in Asia to expand applications of pelargonic acid across personal care, agriculture, and specialty chemicals. The company utilizes high-purity pelargonic acid for flavor, fragrance, and ester synthesis in beauty and hygiene products. Investments in fermentation and green chemistry technologies are reducing production costs by up to 15%, improving competitiveness against petrochemical alternatives. Kao is also expanding its Integrated Pest Management portfolio, promoting pelargonic acid-based herbicides for public and domestic use. Participation in Japan’s Green Technology Initiative supports its sustainability-driven growth strategy. This integration of consumer applications and green innovation positions Kao as a key regional player.

United States – Bio-Preferred Scale-Up and Rapid-Action Agrochemical Adoption

The United States remains a lead market for pelargonic acid due to its early integration into bio-based chemical portfolios and fast regulatory acceptance in crop protection. In October 2024, Emery Oleochemicals expanded its USDA BioPreferred certified portfolio by adding four pelargonic acid products, achieving full 100% bio-based certification across its EMERION® and EMERY® 1202 lines. This move has materially strengthened the positioning of nonanoic acid as a compliant, renewable alternative across agriculture, home and garden, and industrial segments. Technical data released in 2025 demonstrated visible burn-down weed control within 15 minutes of application, reinforcing pelargonic acid’s role as a high-speed, non-selective herbicide suitable for food crops and specialty agriculture where glyphosate alternatives are actively sought.

Regulatory and downstream diversification trends are reinforcing demand. The U.S. Environmental Protection Agency updated its Aquatic Life Benchmarks in September 2025, influencing formulation design for pelargonic acid products used near sensitive water bodies and driving investment in optimized esterification and buffering systems. Beyond agrochemicals, domestic manufacturers are increasingly deploying pelargonic acid as a feedstock for bio-based esters in metalworking fluids and corrosion inhibitors, aligned with the 2025–2026 policy push toward renewable lubricants. Leadership changes at Emery Oleochemicals, including the July 2025 appointment of Min Chong as Group CEO, further signal a strategic pivot toward higher-margin specialty applications built around nonanoic acid derivatives.

Canada – Regulatory Validation Unlocking Commercial Greenhouse Demand

Canada has emerged as a structurally important market following decisive regulatory clarity. In April 2025, Health Canada’s Pest Management Regulatory Agency finalized Registration Decision RD2025-06, approving Beloukha Herbicide for greenhouse-grown vegetables and ornamentals. This approval formally validated pelargonic acid as an acceptable active ingredient for intensive, controlled-environment agriculture, opening the Canadian commercial greenhouse sector to scaled adoption. The accompanying risk assessment concluded that health and environmental risks associated with technical-grade pelargonic acid are acceptable when used as directed, removing a key barrier to market entry.

Policy alignment has further strengthened Canada’s attractiveness. Health Canada confirmed in 2025 its commitment to reducing animal testing for pesticide evaluations, favoring validated in-vitro data where possible. Pelargonic acid has benefited from this shift due to its well-characterized toxicological profile and rapid environmental degradation. As a result, Canada is positioning itself as a regulatory reference market for ethically assessed, bio-based herbicides, with spillover implications for multinational product registrations.

Italy – Circular Economy Feedstocks and Process Innovation

Italy represents a critical innovation hub for bio-based pelargonic acid within the European circular economy framework. Matrìca, the Novamont and Versalis joint venture, continues to scale its Sardinia monomer plant using vegetable oils as renewable feedstock. Pelargonic acid produced through this route is increasingly positioned as a biodiversity-friendly alternative to synthetic herbicides, aligning with EU agricultural transition objectives. In 2025, Matrìca optimized its oxidative cleavage process to deliver higher-purity pelargonic acid grades, extending its addressable market into industrial sanitization and bleaching agents, including precursors for nonaneperoxoic acid.

Academic and field research has reinforced Italy’s strategic relevance. Studies published in 2025 confirmed that natural pelargonic acid formulations exhibit zero residual soil activity, enabling immediate replanting after application. This characteristic directly supports regenerative agriculture and crop rotation practices, strengthening pelargonic acid’s role in European sustainability narratives and driving interest from both specialty crop producers and policy stakeholders.

Germany – Regulatory Scrutiny and Biomass-Balanced Transition

Germany’s pelargonic acid market is shaped by regulatory rigor and decarbonization commitments. In October 2025, the EU Standing Committee on Plants, Animals, Food and Feed advanced discussions on the renewal of pelargonic acid as a regular active substance rather than classifying it as low-risk. The debate centered on mitigation measures for non-target organisms, signaling stricter stewardship requirements but also confirming pelargonic acid’s continued regulatory viability within the EU. This has prompted German formulators to invest in precision application technologies and refined ester derivatives to meet compliance expectations.

Parallel shifts are underway in specialty chemicals. Croda International, with a significant operational footprint in Germany, entered a strategic agreement with Amino GmbH in December 2025 to strengthen global supply chains for high-purity amino acids. Pelargonic acid derivatives are increasingly used as intermediates in these pharmaceutical synthesis routes. At the cluster level, German producers adopted updated Science Based Targets in late 2025, accelerating the replacement of petroleum-derived nonanoic acid with biomass-balanced alternatives.

United Kingdom – High-Purity Biopharma and Regenerative Agriculture Positioning

The United Kingdom is positioning pelargonic acid within high-value pharmaceutical and agricultural innovation streams. In September 2025, Croda International expanded its Super Refined™ facility in Leek to support the production of ultra-high-purity specialty ingredients, including lipid delivery systems derived from pelargonic acid. These applications demand exceptional impurity control and traceability, elevating pelargonic acid from a commodity herbicide input to a pharmaceutical-grade building block.

Agricultural thought leadership is reinforcing this trajectory. In October 2025, Croda Agriculture published a regenerative agriculture white paper identifying pelargonic acid as a core tool for the 2026 transition away from persistent synthetic pesticides. The document emphasized its rapid degradation, zero soil residue, and compatibility with integrated pest management frameworks. As a result, the UK market is increasingly characterized by science-led adoption rather than volume-driven substitution.

Comparative Snapshot – Pelargonic Acid Industry by Country

Pelargonic Acid Market County Level Snapshot

|

Country

|

Strategic Focus

|

Primary Driver

|

Structural Impact

|

|

United States

|

Bio-based expansion and fast-acting herbicides

|

USDA BioPreferred and EPA benchmarks

|

Diversification into lubricants and specialty esters

|

|

Canada

|

Regulatory validation

|

PMRA registration for greenhouses

|

Accelerated adoption in controlled-environment agriculture

|

|

Italy

|

Circular economy production

|

Vegetable-oil feedstocks and process purity

|

Expansion into sanitization and bleaching precursors

|

|

Germany

|

Regulatory compliance and decarbonization

|

EU renewal scrutiny and SBTi targets

|

Shift toward biomass-balanced nonanoic acid

|

|

United Kingdom

|

High-purity and regenerative systems

|

Biopharma investment and agriculture innovation

|

Premium positioning beyond commodity agrochemicals

|

Pelargonic Acid Market Report Scope

Pelargonic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$288.4 Million

|

|

Market Size (2034)

|

$530.2 Million

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Grade (Natural Grade, Synthetic Grade), By Purity Level (Standard Purity, High Purity), By Application (Herbicides and Pesticides, Lubricants and Greases, Pharmaceuticals, Cosmetics and Personal Care, Plasticizers and Polymers, Industrial and Institutional Cleaning)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Emery Oleochemicals, Croda International, Matrica, OQ Chemicals, Wilmar International, Kao Corporation, Sinopec Nanjing Chemical Industries, Zhengzhou Yibang Industry, Godrej Industries, Chongqing Yuanda Industrial, KLK Oleo, Glentham Life Sciences, Central Drug House, Hebei Jingu Group, Bio-Pesticides

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pelargonic Acid Market Segmentation

By Grade

- Natural Grade

- Synthetic Grade

By Purity Level

- Standard Purity

- High Purity

By Application

- Herbicides and Pesticides

- Lubricants and Greases

- Pharmaceuticals

- Cosmetics and Personal Care

- Plasticizers and Polymers

- Industrial and Institutional Cleaning

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Pelargonic Acid Industry

- Emery Oleochemicals

- Croda International

- Matrica

- OQ Chemicals

- Wilmar International

- Kao Corporation

- Sinopec Nanjing Chemical Industries

- Zhengzhou Yibang Industry

- Godrej Industries

- Chongqing Yuanda Industrial

- KLK Oleo

- Glentham Life Sciences

- Central Drug House

- Hebei Jingu Group

- Bio-Pesticides

*- List not Exhaustive