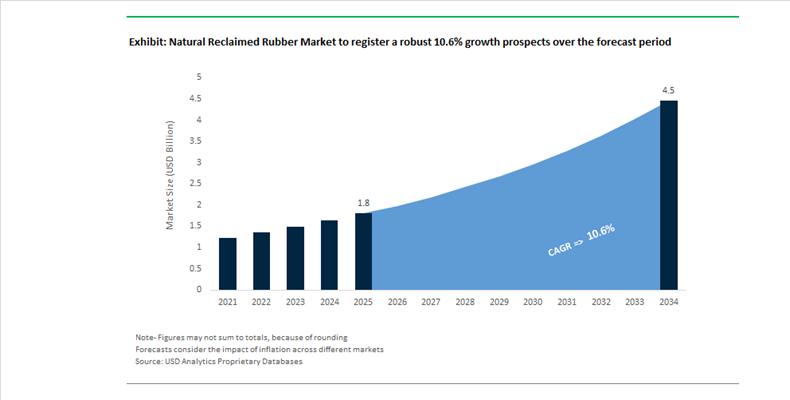

Natural Reclaimed Rubber Market Valued at $1.8 Billion in 2025 Projected to Reach $4.5 Billion by 2034 at 10.6% CAGR

The Natural Reclaimed Rubber Market is valued at $1.8 billion in 2025 and is projected to reach $4.5 billion by 2034, expanding at a robust CAGR of 10.6%. The market is undergoing structural transformation as reclaimed rubber shifts from a low-cost substitute to a performance-engineered raw material integrated into premium tire manufacturing, footwear, industrial matting, and automotive components. Rising global pressure on natural rubber supply chains, increasing raw material volatility, and aggressive circular economy mandates across Europe and Asia are accelerating the adoption of devulcanized and crumb rubber solutions.

India has emerged as a pivotal growth engine in this market. Between 2024 and 2025, the Government of India implemented updated Extended Producer Responsibility (EPR) regulations for waste tires, mandating the use of reclaimed or crumb rubber in new tire production. This regulatory shift triggered a surge in EPR credit trading activity. By the end of fiscal year 2025, GRP Limited reported approximately ₹220 million in EPR-related revenue, reflecting the monetization of compliance-driven recycling demand. Complementing this, the Rubber Board of India allocated ₹708.69 crore for the 2024–2026 period to strengthen sustainability across the natural rubber value chain, including downstream recycling and processing infrastructure. These measures are strategically positioned to reduce India’s reliance on imported natural rubber while expanding domestic reclaimed rubber output.

Technological innovation in devulcanization is redefining performance benchmarks. In 2024, Bridgestone and Tokai Carbon advanced their joint venture focused on chemical devulcanization capable of retaining 80% to 85% of original natural rubber tensile strength. This represents a significant improvement over conventional ambient grinding methods. In parallel, Michelin initiated pilot programs in 2024 integrating reclaimed rubber blends into commercial truck tire lines to meet European Union circularity requirements without compromising durability standards. Similarly, Tyromer Inc. expanded its partnership with Continental Tyres in 2024, scaling deployment of chemical-free heat-and-shear devulcanized rubber. These advancements demonstrate the sector’s evolution toward high-strength, application-grade reclaimed rubber suitable for Tier 1 OEM specifications.

Capacity expansion and consolidation are further reshaping competitive positioning. In early 2025, GRP Limited approved a ₹2.5 billion expansion plan through 2027, with ₹1.5 billion allocated to low-CO₂ emission technologies and crumb rubber capacity aligned with India’s EPR targets. By February 2026, the company confirmed commissioning of continuous pyrolysis and crumb rubber units. GRP also disclosed in 2025 that it supplies reclaimed rubber to 8 of the top 10 global tire manufacturers, underscoring the mainstream acceptance of reclaimed materials in premium tire formulations. In January 2026, SJ Corporation acquired a 99.99% stake in Fishfa Rubbers Limited for approximately ₹47.16 crore, gaining access to butyl, natural tube, and EPDM reclaim rubber capabilities.

Sustainability-linked capital inflows are strengthening North American recycling infrastructure. In November 2024, Ecore International secured investment from General Atlantic’s BeyondNetZero fund to scale proprietary devulcanization and circular economy technologies for repurposing end-of-life tire rubber into high-value flooring and industrial surfaces. Product innovation is also targeting regulatory-driven odor and VOC limitations. During 2025, multiple reclaimers introduced low-odor natural reclaimed rubber grades tailored for footwear and indoor applications across EU and North American markets, addressing historical barriers to recycled rubber adoption in consumer-facing segments.

Natural Reclaimed Rubber Market Trends and Opportunities

Trend: Mandated Incorporation of Reclaimed Rubber in Public Works and Infrastructure

Public infrastructure policy is rapidly transforming reclaimed rubber from an optional sustainability input into a mandated construction material across roads, highways, and urban redevelopment projects. Governments are embedding recycled elastomer usage directly into procurement rules to address landfill saturation, improve pavement longevity, and reduce lifecycle carbon intensity. In April 2025, India’s Ministry of Environment notified updated Construction and Demolition Waste Management Rules that require infrastructure projects to progressively raise recycled material utilization from 25% in FY 2025–26 to full compliance by 2029. This regulatory architecture is reshaping demand for natural reclaimed rubber in rubberized bitumen, reclaimed asphalt pavement, and noise-reducing road layers.

Performance validation has reinforced policy momentum. Guidance from the Federal Highway Administration and India’s National Highways Authority of India confirms that rubberized asphalt materially improves resistance to rutting and thermal cracking under heavy traffic and temperature variation. In 2024 alone, NHAI diverted more than 3,300 tonnes of non-hazardous rubber waste into national highway construction, supporting a Mill and Fill approach where reclaimed rubber layers match or outperform virgin asphalt. Municipal circulars issued in July 2025 further emphasize reclaimed rubber’s role in preventing road elevation creep during resurfacing, a critical factor in mitigating urban flooding risk in dense city centers. Together, these mandates are converting reclaimed rubber into a structural input with guaranteed public-sector demand visibility.

Trend: Strategic Quality Standardization and Supply Integration by Tire Manufacturers

Leading tire manufacturers are redefining reclaimed rubber procurement from opportunistic sourcing to tightly controlled, specification-driven supply chains. Companies such as Michelin, Bridgestone, and CEAT are prioritizing devulcanized rubber with predictable polymer integrity for use in non-critical tire components, inner liners, and tread backing layers. This shift reflects the need to stabilize input costs while meeting internal sustainability targets without compromising safety or durability.

Supply security is being reinforced through consolidation and asset control. CEAT’s acquisition of Michelin’s Camso brand in late 2024 illustrates how tire producers are securing manufacturing footprints in high feedstock availability regions such as Sri Lanka to gain direct oversight of reclaimed rubber quality. On the regulatory front, the push for harmonized End-of-Waste criteria is gaining urgency. In July 2025, the European Tyre and Rubber Manufacturers’ Association and EuRIC jointly urged the European Commission to finalize EU-wide End-of-Waste definitions for rubber. This framework would declassify reclaimed rubber from waste status, enabling frictionless cross-border trade and accelerating adoption under the Ecodesign for Sustainable Products Regulation. Technologically, partnerships with innovators such as Bolder Industries are delivering reclaimed powders capable of replacing 10 to 15% of virgin synthetic rubber while preserving air permeability and fatigue performance.

Opportunity: High-Performance Reclaimed Rubber Blends for Sustainable Footwear and Fashion

Footwear has emerged as a high-margin proving ground for advanced reclaimed rubber formulations. Global brands are replacing petroleum-based EVA soles with engineered reclaimed rubber blends to meet ESG commitments and differentiate products in sustainability-conscious markets. Adoption of eco-soles accelerated by 28% in 2025, with manufacturers such as Eurosuole S.p.A. launching collections that integrate high recycled content while preserving premium aesthetics and comfort.

Material science advances are closing the performance gap. Modern reclaimed rubber microcellular structures now achieve weight reductions of approximately 31% while maintaining shock absorption and tensile strength benchmarks aligned with ASTM D1278 and D1646. Regulatory labeling regimes in Europe and parts of Asia are reinforcing demand, driving innovation in translucent and resin-modified reclaimed rubber that delivers contemporary design appeal alongside verified recycled content. For fashion and athletic footwear brands, reclaimed rubber is evolving from a sustainability signal into a functional differentiator with margin upside.

Opportunity: Non-Toxic, Shock-Attenuating Surfaces for Recreational and Public Safety

Heightened scrutiny of crumb rubber toxicity is catalyzing demand for certified, non-toxic reclaimed rubber systems in playgrounds, hospitals, and public facilities. Poured-in-place surfaces formulated with natural reclaimed rubber are increasingly specified to meet ASTM F1292 impact attenuation standards, with current systems capable of protecting falls from heights up to 20 feet using only three inches of material. This performance significantly exceeds that of traditional wood chips or sand.

Indoor air quality and lifecycle metrics are strengthening the value proposition. In 2025, architects and municipal planners prioritized flooring certified under FloorScore and Fitwel, accelerating adoption of reclaimed rubber flooring from manufacturers such as U.S. Rubber. These products are low-VOC, PVC-free, and consume up to 72% less energy to manufacture than virgin rubber alternatives, delivering substantial embodied carbon savings. With warranties exceeding 20 years, reclaimed rubber safety surfaces align directly with LEED v4.1 credits and long-term public asset management strategies, positioning this segment as one of the most durable and defensible growth avenues in the natural reclaimed rubber market.

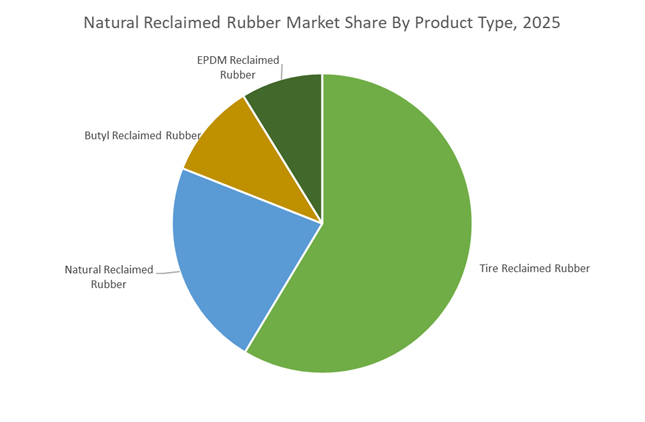

Natural Reclaimed Rubber Market Share and Segmentation Insights

Tire Reclaimed Rubber Leads Circular Rubber Economy with High-Volume Feedstock Utilization

Tire reclaimed rubber accounted for 58.60% of the Natural Reclaimed Rubber Market by product type in 2025, driven by the abundance of end-of-life tires as the largest global rubber waste stream and the presence of well-established collection and recycling infrastructure. Reclaimed tire rubber is widely used in automotive components, new tire production, and industrial rubber goods due to its cost advantage over virgin rubber. It supports material circularity while maintaining acceptable performance in various applications. In 2025, circular economy initiatives in tire manufacturing are accelerating adoption, with advanced devulcanization technologies enabling higher-quality reclaimed rubber suitable for use in treads, sidewalls, and performance-sensitive applications.

Automotive and Aviation Sector Drives Demand with Expanding Use of Reclaimed Rubber Components

Automotive and aviation accounted for 42.80% of the Natural Reclaimed Rubber Market by application in 2025, reflecting strong demand for reclaimed rubber in tires, hoses, belts, gaskets, seals, and vibration control components. The sector benefits from cost savings and sustainability advantages associated with recycled rubber integration. Increasing regulatory and corporate focus on sustainable materials is encouraging higher reclaimed rubber usage across transportation applications. Improved processing technologies have enhanced material consistency and mechanical performance. In 2025, quality improvements in reclaimed rubber are expanding automotive adoption, with manufacturers specifying higher recycled content in under-hood components and critical rubber parts that require durability and thermal resistance.

Natural Reclaimed Rubber Market Competitive Landscape

The natural reclaimed rubber market in 2026 is driven by high-performance devulcanization, green tire mandates, and circular economy integration. Competitive advantage centers on high-tensile reclaim quality, molecular integrity preservation, and export agility, enabling up to 15% substitution of virgin natural rubber in automotive, aerospace, and industrial applications.

GRP scales circular tire recycling and export-led growth with advanced reclaim and rCB integration

GRP Limited is emerging as a fully integrated circular economy leader, combining high-capacity reclaim production with advanced recycling technologies. The company reported 17% YTD revenue growth in FY26, supported by strong domestic demand and €12 million ECB funding for infrastructure expansion. Its Solapur facility adds over 30,000 MT processing capacity, reinforcing supply scalability. GRP’s diversification into recovered carbon black (rCB) and pyrolysis oil enables a “total tire circularity” model, enhancing value capture across the rubber lifecycle. Reduced U.S. tariffs (~18%) have strengthened its export competitiveness, reopening Tier-1 automotive supply opportunities. Its integration of reclaim, rCB, and energy recovery positions it as a global sustainability-driven supplier.

Fishfa delivers nitrosamine-free high-purity reclaim for EU-compliant premium rubber applications

Fishfa Rubbers Ltd. is positioned as a premium export-focused manufacturer specializing in high-purity, nitrosamine-free natural reclaimed rubber. Its products comply with stringent REACH and ECHA regulations, making them suitable for European tire, consumer goods, and indoor applications. The company’s reclaim blends are optimized for inner liners and automotive tubes, ensuring superior air retention and impermeability. Fishfa’s Sustainability Roadmap 2030 targets carbon neutrality and 30% reductions in water and waste intensity, enhancing ESG positioning. Its advanced devulcanization processes produce high-tensile reclaim with minimal odor and toxicity. With exports spanning 25+ countries, Fishfa maintains strong traction in regulated global markets.

Sun Exim drives customized reclaim compounds with processing efficiency and global supply flexibility

Sun Exim differentiates itself through customized reclaimed rubber solutions tailored for industrial and specialty applications. Its reclaim grades deliver 5–10% improvements in extrusion rates and reduce energy consumption during mixing by lowering compound viscosity. The company serves over 30 global markets, offering tailored ash and nitrogen content for conveyor belts, adhesives, and battery containers. Its “Supreme Grade” reclaim is being evaluated for aerospace anti-static rubber sheets, emphasizing high tear strength and controlled hardness. Sun Exim’s focus on pre-plasticized reclaim reduces mastication time, accelerating manufacturing cycles. This customization-driven model enhances performance efficiency across diverse end-use industries.

Rolex Reclaim expands global footprint with odor-controlled reclaim and closed-loop feedstock integration

Rolex Reclaim Pvt. Ltd. is strengthening its position as a global exporter by focusing on high-tensile reclaim and sustainable sourcing models. The company has expanded its presence across Asia Pacific, supplying footwear and molded goods manufacturers seeking cost-stable alternatives to virgin rubber. Its odor-controlled reclaim grades are gaining traction in automotive interiors, including floor mats and pedal systems, where sensory performance is critical. Rolex operates a closed-loop ELT collection system, ensuring consistent feedstock quality and reduced contamination risk. Its alignment with “Perpetual Planet” sustainability initiatives enhances brand value in international markets. This integrated approach supports scalable, high-quality reclaim production.

Rubber Resources leads high-performance devulcanization for green tire and automotive sealing applications

Rubber Resources, part of Hexpol Group, sets the benchmark for advanced devulcanization and high-performance reclaimed rubber in Western markets. Its proprietary chemical devulcanization enables higher reclaim loading in tire treads, expanding beyond traditional sidewall applications. The company benefits from EU circular economy mandates, supplying materials for green tires with up to 20% recycled content. AI-driven quality control and automated sorting ensure consistent material properties required by Tier-1 OEMs such as Michelin and Continental. Its reclaim is widely used in automotive seals and weather-stripping, offering superior UV resistance and elasticity. Rubber Resources’ focus on precision and high-end applications reinforces its leadership in premium reclaim segments.

India: Policy-Led Feedstock Security and Rapid Technology Upgrading

India has emerged as the most policy-driven growth engine for the natural reclaimed rubber market, with regulatory enforcement now directly shaping material flows. The Ministry of Environment, Forest and Climate Change finalized the 2025–2026 Extended Producer Responsibility framework for waste tires, mandating minimum reclaimed rubber incorporation in new tire manufacturing. This regulation is structurally improving domestic feedstock security for reclaimers and shifting reclaimed rubber from a cost-driven substitute to a compliance-critical input across the tire value chain.

Capacity expansion and cost optimization are reinforcing this regulatory tailwind. In late 2025, Gujarat-based Home Zone Rubber Solutions announced an IPO to fund the doubling of its processing capacity, leveraging Danish Eldan technology to convert more than 500,000 scrap tires annually into high-purity natural reclaim. Upstream integration has further lowered operating costs. The stabilization of caustic soda supply following the GACL-NALCO joint venture in May 2025 reduced reclaiming input costs by an estimated 12% for regional processors. Complementing this, the 2026 Sustainable Rubber Mission introduced subsidies for SMEs adopting energy-efficient devulcanization units, modernizing decentralized hubs in Kerala and Maharashtra. Strategic demand pull is also strengthening, highlighted by Michelin’s October 2025 collaboration with an Indian reclaimer to supply high-performance natural reclaim for eco-friendly radial tires scheduled for 2026. On the technology front, research at the Rubber Research Institute of India successfully piloted Narrow Range Ethoxylates as processing aids, improving reclaim dispersion in virgin natural rubber matrices and enabling higher blend ratios.

Germany: High-Performance Reclaim and Circular Tire Architecture

Germany’s natural reclaimed rubber landscape is defined by advanced chemistry and OEM-led circularity targets rather than volume recovery mandates. Evonik’s 2024–2025 breakthrough in sulfur-bond cleavage using vinyl silanes marked a structural shift, enabling up to 20% reclaimed rubber inclusion in new tire formulations. This represents a fourfold increase over prior industry norms and materially changes the technical ceiling for natural reclaim usage in premium applications.

Automotive OEMs are embedding these advances into global strategies. Continental AG expanded its R&D focus in August 2025 to accelerate advanced rubber recycling technologies, with Germany serving as the blueprint center for circularity models to be deployed across European plants by 2026. The strategic direction will be visible at The Tire Cologne 2026, positioned as the primary launch platform for circular tire prototypes utilizing 99.7% contamination-free natural reclaimed rubber. Parallel investments are strengthening the regional ecosystem. Bolder Industries’ planned Antwerp expansion, commencing construction in 2026, will produce reclaimed rubber materials using wind power, delivering an estimated 80% reduction in greenhouse gas emissions compared with virgin rubber processing.

China: Mandated Recycling Ratios and Infrastructure-Led Demand

China’s natural reclaimed rubber market is being reshaped by mandatory recycling targets and infrastructure-driven demand. Under the Ministry of Industry and Information Technology Green Manufacturing roadmap, 60% of rubber waste must be recycled by 2026. This mandate has accelerated the deployment of AI-powered optical sorting systems in Shandong-based reclaim facilities, enabling the production of ultra-high-purity reclaimed rubber grades suitable for structural and automotive applications.

Demand is increasingly diversified beyond tires. The 2025 national urban rail stimulus has driven significant consumption of reclaimed rubber in seismic bearings and expansion joints used in transit infrastructure. On the processing side, manufacturers such as Tianyu Rubber transitioned to continuous pyrolysis reactors in 2025, improving output consistency and reclaim quality versus legacy batch systems. Innovation is also opening adjacent markets. In December 2025, Chinese chemical groups successfully developed rubber-based substitutes for PFAS in paper coating resins, creating a new sustainability-driven outlet for refined reclaimed rubber in packaging applications.

United States: Infrastructure Pull and Traceable Circular Models

In the United States, the reclaimed rubber market is anchored by infrastructure policy and institutional investment rather than federal recycling mandates. According to 2025 Environmental Protection Agency data, North American reclaimed rubber production reached approximately 37,671 tons, supported by state-level requirements for rubberized asphalt in highway construction. This has provided stable baseline demand for natural reclaim in public works.

Research and private capital are accelerating the transition toward higher-value outputs. The National Science Foundation’s $26 million funding to the TARDISS Engineering Research Center is advancing domestic rubber crop alternatives and advanced recycling technologies, with pilot-scale thermoplastic rubber intermediates from scrap tires expected by 2026. At the commercial level, a major U.S. recycling firm secured equity investment from Tiger Infrastructure Partners in 2025 to scale traceable, OEM-aligned circular solutions for the automotive sector. These developments indicate a shift toward transparency-driven supply chains where reclaimed rubber is specified and audited by end users.

Thailand: Feedstock Stability and Processing Aids for Regional Manufacturing

Thailand’s role in the natural reclaimed rubber market is defined by upstream feedstock quality and processing support rather than large-scale reclaim capacity. In April 2025, the Rubber Authority of Thailand launched the Young Smart Rubber Farmer Camp to integrate automation into rubber harvesting and processing, addressing labor shortages and stabilizing the supply of high-grade latex essential for reclaim applications.

Downstream capability has been strengthened through chemical input availability. BASF’s expanded Bangpakong facility, inaugurated in November 2025, now supplies regional reclaimers with bio-based surfactants and specialized processing aids. These inputs are critical for producing odor-free reclaimed rubber grades required by footwear and consumer goods manufacturers across Southeast Asia, positioning Thailand as a quality-focused support hub within the regional circular rubber ecosystem.

Comparative Summary: Natural Reclaimed Rubber Market by Country

Natural Reclaimed Rubber Market County Level Snapshot

|

Country

|

Primary Market Driver

|

Key Developments

|

Strategic Impact

|

|

India

|

EPR enforcement and OEM demand

|

Capacity doubling, Michelin partnership, SME subsidies

|

Rapid scale-up with improving quality standards

|

|

Germany

|

Advanced chemistry and OEM circularity

|

Sulfur-cleaving technology, circular tire prototypes

|

High-performance reclaim for premium applications

|

|

China

|

Mandatory recycling and infrastructure spend

|

AI sorting, continuous pyrolysis, rail projects

|

Volume-driven adoption with expanding use cases

|

|

United States

|

Infrastructure policy and private capital

|

Rubberized asphalt, TARDISS funding

|

Traceable, higher-value circular supply chains

|

|

Thailand

|

Feedstock quality and processing aids

|

Farmer automation, BASF expansion

|

Regional support for odor-free, high-grade reclaim

|

Natural Reclaimed Rubber Market Report Scope

Natural Reclaimed Rubber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

10.6%

|

|

Segments

|

By Product Type (Tire Reclaimed Rubber, Butyl Reclaimed Rubber, EPDM Reclaimed Rubber, Natural Reclaimed Rubber), By Form (Sheets, Powder, Granules), By Process (Chemical Devulcanization, Mechanical Reclaiming, Advanced Reclaiming Technologies), By Application (Automotive and Aviation, Construction, Footwear, Industrial Goods, Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

GRP, Rolex Reclaim, Fishfa Rubbers, J. Allcock & Sons, HUXAR, Tianyu Rubber and Plastic Products, Swani Rubber Industries, Minar Reclamation, High Tech Reclaim, Balaji Rubber Industries, Bolder Industries, Evonik Industries, Bridgestone, Michelin, Lehigh Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Natural Reclaimed Rubber Market Segmentation

By Product Type

- Tire Reclaimed Rubber

- Butyl Reclaimed Rubber

- EPDM Reclaimed Rubber

- Natural Reclaimed Rubber

By Form

By Process

- Chemical Devulcanization

- Mechanical Reclaiming

- Advanced Reclaiming Technologies

By Application

- Automotive and Aviation

- Construction

- Footwear

- Industrial Goods

- Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Natural Reclaimed Rubber Market

- GRP

- Rolex Reclaim

- Fishfa Rubbers

- J. Allcock & Sons

- HUXAR

- Tianyu Rubber and Plastic Products

- Swani Rubber Industries

- Minar Reclamation

- High Tech Reclaim

- Balaji Rubber Industries

- Bolder Industries

- Evonik Industries

- Bridgestone

- Michelin

- Lehigh Technologies

*- List not Exhaustive