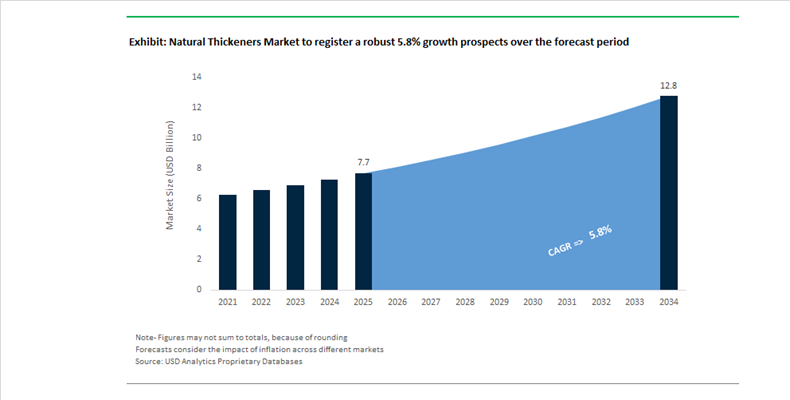

Natural Thickeners Market Valued at $7.7 Billion in 2025 Set to Reach $12.8 Billion by 2034 at 5.8% CAGR

The Natural Thickeners Market is valued at $7.7 billion in 2025 and is projected to reach $12.8 billion by 2034, expanding at a steady CAGR of 5.8%. The market is being reshaped by clean-label reformulation, supply chain realignment, and large-scale consolidation among global ingredient leaders. Food and beverage manufacturers are aggressively replacing synthetic emulsifiers and stabilizers with plant-derived gums, pectins, citrus fibers, and specialty starches to meet regulatory scrutiny and consumer demand for minimally processed formulations. At the same time, pharmaceutical and nutraceutical applications are driving demand for high-purity excipients and rheology modifiers with predictable viscosity control and functional stability.

A defining structural shift occurred in November 2024 when Tate & Lyle completed its $1.8 billion acquisition of CP Kelco. By early 2025, the combined organization began operating under a new structure focused on integrating sweetening systems with pectin and specialty gum technologies. This repositioned the group as a vertically integrated “mouthfeel systems” supplier capable of competing with multinational ingredient conglomerates. Parallel to this acquisition, Tate & Lyle finalized the sale of its remaining interest in Primient in June 2024, fully exiting commodity corn wet milling and transitioning toward high-margin specialty thickeners and texturizers.

In May 2025, Roquette completed the acquisition of IFF Pharma Solutions, significantly strengthening its natural excipients portfolio. Following the deal, Roquette reorganized into Health & Pharma and Nutrition & Bioindustry divisions, managing a global network of 40 manufacturing sites. This acquisition reinforces the pharmaceutical-grade natural thickener segment, where hydrocolloids and cellulose derivatives are critical for controlled-release drug delivery systems and clinical nutrition products.

Capacity expansion is intensifying across Asia-Pacific and the Americas. In late 2024, Ingredion concluded a $160 million multi-year expansion program, doubling starch production capacity in Shandong, China, while enhancing localized specialty starch manufacturing across the U.S. and Europe. In 2024, CP Kelco ramped up a $50 million investment in Matão, Brazil, bringing its NUTRAVA® Citrus Fiber line to full operation with a 5,000 metric ton annual capacity. This investment directly targets the clean-label shift, where citrus-derived fiber systems are replacing synthetic stabilizers in dairy alternatives, sauces, and plant-based beverages.

In January 2026, Cargill broke ground on a RMB 45 million expansion of its Beijing plant, adding new functional systems and thickener production lines to serve the Asia-Pacific convenience and foodservice sectors. Earlier, at AAHAR 2025, Cargill introduced a starch-based pectin replacer for gummy confectionery, mitigating citrus pectin price volatility and addressing supply instability. This development reflects a broader industry pivot toward hybrid gum-starch systems designed to stabilize input costs while maintaining chewiness and gel strength.

Between 2025 and early 2026, Archer Daniels Midland invested $41 million in its Erlanger, Kentucky campus, expanding innovation and production capabilities for natural color and thickener systems aligned with global “better-for-you” reformulation initiatives. Meanwhile, Ashland Inc. divested its Avoca nutraceuticals business in 2025 to refocus on rheology modifiers, including its Natrosol™ and Aqualon™ cellulosic lines. Its Kentucky world-scale facility reached mechanical completion in 2024, strengthening supply security for natural cellulose-based thickeners. In February 2026, Ashland’s Agrimer™ ECO-coat polymer platform received U.S. EPA approval, highlighting the rise of vegetable oil–derived thickening chemistries as alternatives to petroleum-based polymers.

Raw material volatility remains a structural variable. In August 2024, guar gum prices increased approximately 20% due to weather disruptions in India and Pakistan combined with rising demand from animal feed sectors. This price instability accelerated the adoption of blended hydrocolloid systems, reinforcing the importance of diversified sourcing strategies and formulation flexibility.

Natural Thickeners Market Trends and Opportunities

Trend: Precision Texturization Systems Redefining Plant-Based Meat and Dairy Analogues

The natural thickeners market is undergoing a structural shift as alternative protein producers move beyond basic viscosity control toward precision texturization and sensory engineering. In 2024–2025, leading food innovators increasingly abandoned single-hydrocolloid solutions in favor of synergistic systems that combine gums, starches, and plant proteins to replicate muscle fiber alignment, fat melt, and elastic bite. This transition reflects the maturation of the plant-based sector, where consumer acceptance is now driven by mouthfeel parity rather than novelty. At Anuga FoodTec 2025, companies such as Juicy Marbles and Novameat showcased 3D-assembled “whole-cut” analogues that rely on high-purity natural thickeners to bind millions of plant-based fibers simultaneously, delivering chew and shear behavior comparable to animal meat.

Hybrid protein innovation is accelerating this trend. Industry disclosures from Beneo Meatless in late 2024 confirm that hybrid products blending plant and animal proteins are entering retail at a pace of roughly one launch per month. These formulations depend heavily on natural thickeners such as cellulose derivatives, guar gum, and modified starches to stabilize fat-protein matrices under thermal stress in applications like pizza toppings and processed meats. Parallel to this, clean-label pressure is reshaping formulation philosophy. Startups including The Green Farm in Denmark are commercializing patties built on fermented oats and vegetables that act as intrinsic thickening matrices, eliminating synthetic binders altogether. This strategy aligns with a documented 22% rise in consumer preference for products containing fewer than five recognizable ingredients, positioning natural thickeners as both functional and brand-critical inputs.

Trend: Supply Chain Verticalization and Certified Sustainability in Guar Gum

Guar gum, one of the most strategic natural thickeners, is entering a new phase of supply chain consolidation and transparency following repeated price shocks and demand volatility. The July 2025 spot-market surge, driven by overlapping demand from food processing and green energy applications, triggered a decisive shift among major buyers toward direct farm-to-factory integration. India’s policy response has been pivotal. In July 2025, the Indian Union Cabinet approved an additional ₹1,920 crore under the Pradhan Mantri Kisan Sampada Yojana to strengthen cold-chain and value-addition infrastructure in guar-producing regions such as Rajasthan. This investment is directly improving gum quality, reducing post-harvest losses, and supporting export-grade traceability.

Digital traceability has become a competitive requirement rather than a differentiator. By late 2025, blockchain-based verification systems were widely adopted across guar supply chains, allowing industrial buyers to authenticate origin, cultivation practices, and ESG compliance through QR-enabled documentation. This capability is increasingly essential as ESG-linked procurement policies tighten, particularly among multinational food, oilfield, and pharmaceutical customers. Despite climate volatility, guar sowing in Rajasthan increased by 7% in the 2025 season, supported by long-term contract farming models. Food conglomerates and oilfield service providers have shifted 15–20% of sourcing to direct cooperative contracts, stabilizing prices while securing clean-label and sustainability-certified output.

Opportunity: Natural Thickeners as Functional Binders in Silicon-Anode Battery Slurries

Beyond food applications, natural thickeners are emerging as critical functional materials in next-generation lithium-ion batteries, particularly for silicon-based anodes. Silicon-carbon composites represented roughly 30% of the anode market in 2024, but their extreme volumetric expansion during charge-discharge cycles creates severe slurry stability and mechanical integrity challenges. Natural thickeners such as xanthan gum and carboxymethyl cellulose are being engineered to meet these demands, functioning simultaneously as rheology modifiers and flexible binding matrices.

Patent activity in 2025 highlights this transition from laboratory-scale experimentation to industrial adoption. U.S. Patent US11329289B2 describes thickener systems with water-insoluble fractions below 1% by mass, specifically designed to prevent particle settling in high-solids electrode slurries. As silicon anode production scales across the United States, South Korea, and China, battery manufacturers are demanding technical-grade natural thickeners with ultra-low impurity profiles and consistent molecular weight distribution. This creates a high-margin opportunity for suppliers capable of meeting battery-sector specifications, positioning natural thickeners as enablers of higher energy density and improved cycle retention in EV platforms.

Opportunity: Clinical Nutrition and Precision Thickeners for Dysphagia Management

Demographic aging and rising neurological disorder prevalence are transforming dysphagia management into a regulated, high-growth segment for natural thickeners. Healthcare systems are standardizing on gum-based solutions that deliver consistent viscosity and safety across care settings. In 2025, the International Dysphagia Diet Standardisation Initiative continued to serve as the global benchmark, with health services such as the National Health Service favoring gum-based thickeners over starch-based alternatives due to their resistance to salivary amylase and superior viscosity stability.

Clinical evidence is expanding into pediatric care. Research published in early 2025, including studies referenced by the Radboud Repository, confirmed that locust bean gum and xanthan gum provide stable consistency without altering taste in breast milk or infant formula, improving nutritional outcomes for infants with swallowing disorders. At the same time, the shift toward home-based care is strengthening demand for ready-to-drink thickened beverages in North America and Europe. These products rely on precisely calibrated natural thickeners to deliver consistent, pre-measured viscosity, supporting safer at-home nutrition for patients with Parkinson’s disease, stroke-related complications, and age-related dysphagia.

Natural Thickeners Market Share and Segmentation Insights

Gums and Hydrocolloids Lead Natural Thickeners Market Through High Functional Efficiency and Multi-Industry Applications

Gums and hydrocolloids accounted for 38.60% of the Natural Thickeners Market share in 2025, making them the most widely used category of natural viscosity modifiers across food, pharmaceutical, and personal care formulations. This group includes xanthan gum, guar gum, locust bean gum, gum arabic, and gellan gum, which are valued for their exceptional thickening performance even at very low concentrations. Hydrocolloids provide multiple functional properties such as viscosity control, suspension stability, emulsification support, gel formation, and water-binding capability, enabling manufacturers to achieve consistent texture and product stability across diverse formulations. Their compatibility with a wide range of food ingredients and processing conditions makes them essential components in modern formulation science. In 2025, fermentation-derived hydrocolloids have gained significant industry attention. Ingredients such as xanthan gum and gellan gum produced through microbial fermentation offer consistent quality, controlled production independent of agricultural conditions, and strong positioning within vegan and clean label ingredient trends, making them increasingly preferred by manufacturers seeking reliable and sustainable natural thickening solutions.

Food and Beverage Industry Drives the Largest Demand for Natural Thickeners

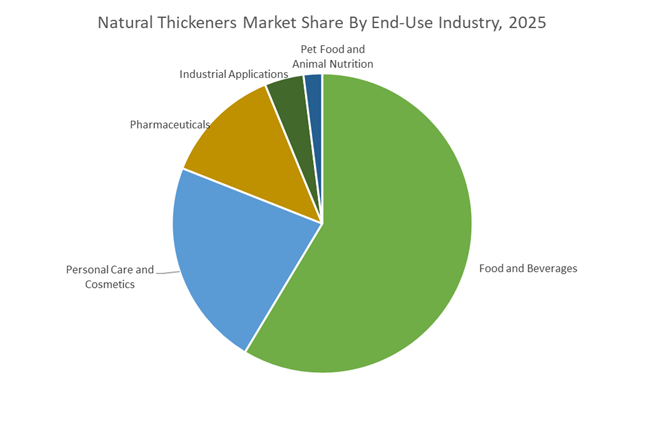

Food and beverages accounted for 58.60% of the Natural Thickeners Market share in 2025, establishing the sector as the primary consumer of hydrocolloids and other natural thickening agents. Natural thickeners play a critical role in determining the texture, mouthfeel, stability, and visual consistency of a wide range of processed food products. They are widely used in sauces, dressings, dairy products, soups, beverages, confectionery, bakery fillings, and frozen desserts, where they regulate viscosity, prevent ingredient separation, and improve sensory characteristics that influence consumer acceptance. Increasing consumer demand for clean label food products with recognizable plant-based ingredients has further strengthened the use of natural thickening agents as alternatives to synthetic stabilizers. In 2025, the rapid growth of plant-based dairy and meat alternatives has created new demand for specialized hydrocolloid systems capable of replicating the texture and structural properties of animal-based foods. Formulators are increasingly developing multi-hydrocolloid systems that deliver stretch in vegan cheeses, creaminess in plant-based yogurts, and fibrous textures in meat analog products, supporting the expansion of the global plant-based food market.

Natural Thickeners Market Competitive Landscape

The natural thickeners market in 2026 is driven by clean-label demand, fermentation-derived hydrocolloids, and multi-functional texture systems. Competitive differentiation centers on sensory resilience, emulsion stability, and upcycled plant-based ingredients, enabling manufacturers to replace synthetic additives while maintaining mouthfeel in high-protein, low-sugar formulations.

Ingredion drives clean-label texture systems with fermentation innovation and specialty starch expansion

Ingredion is leading the natural thickeners market through its high-growth Texture & Healthful Solutions segment, which generated US$405 million operating income in 2025, up 16%. The company is scaling specialty starch capacity via its Indianapolis modernization, targeting multi-sensory food applications. Its partnership with Cosaic enables fermentation-derived emulsifiers that replicate dairy-like creaminess in plant-based products. Ingredion’s Clean Label ATLAS insights guide the development of label-friendly starches with superior freeze-thaw stability. With declining sweetener demand, the company is strategically repositioning toward high-margin natural texturants. This focus strengthens its leadership in clean-label, functional ingredient systems.

Tate & Lyle integrates CP Kelco portfolio to deliver advanced hydrocolloids and citrus fiber solutions

Tate & Lyle has emerged as a global leader in natural hydrocolloids following its US$1.8 billion acquisition of CP Kelco. Its expanded portfolio includes high-acyl gellan gum, pectin, and fermentation-derived diutan gum for stable, low-dose thickening across food and personal care applications. The company is scaling Nutrava® Citrus Fiber as an upcycled, clean-label emulsifier alternative in sauces and dressings. Its system solutions approach combines fibers and gums to address syneresis and texture challenges in plant-based dairy and meat. Cross-industry applications enhance revenue diversification and market penetration. This integrated strategy positions Tate & Lyle at the forefront of nature-based thickening systems.

Cargill expands functional system integration and regional production to capture convenience food demand

Cargill is strengthening its position through a “local-for-local” strategy and integrated functional systems combining starches, gums, and proteins. Its RMB 45 million Beijing expansion supports growing demand for convenience foods and beverage systems in Asia-Pacific. The company’s specialty starches are engineered to prevent syneresis in packaged soups and ready meals, enhancing shelf stability. Cargill is aligning its supply chain with regenerative agriculture, offering low-carbon corn and seaweed-derived thickeners. Its focus on system-based solutions rather than standalone ingredients improves formulation efficiency for global food manufacturers. This approach reinforces its competitiveness in scalable, sustainable texturants.

Roquette advances plant-based thickening with pea-derived starch innovation and pharmaceutical applications

Roquette is reinforcing its plant-based leadership through innovations such as AMYSTA™ L 123, a thermally soluble pea starch designed for clean-label thickening. Its NUTRALYS® protein range functions as structural thickeners in plant-based meat, improving texture and moisture retention. The company is expanding into pharmaceutical excipients through its Brazil Innovation Center, utilizing natural thickeners for drug delivery systems. Recognition with EcoVadis Gold highlights its sustainability credentials, critical for organic and green beauty markets. Roquette’s focus on plant-derived, high-performance ingredients supports its positioning in premium clean-label applications. This diversified strategy enhances both food and pharma market reach.

ADM scales precision fermentation and low-carbon biorefinery systems for next-generation natural thickeners

ADM is leveraging its Carbohydrate Solutions division to drive innovation in natural thickeners through precision fermentation and integrated biorefinery systems. The company has invested over US$41 million in reformulation-focused capacity expansions, targeting global demand for clean-label ingredients. Its Nebraska biorefinery, integrated with carbon capture and storage (CCS), enables low-carbon starch derivatives. ADM is shifting toward high-margin bio-based texturants, replacing commodity volumes with specialty ingredients. Consumer insights showing 83% preference for recognizable ingredients are guiding its R&D in texture and flavor optimization. This strategy positions ADM as a leader in sustainable, next-generation thickening solutions.

United States: Regulatory Recalibration and Portfolio Consolidation Drive Reformulation

The United States natural thickeners market is entering a structurally different regulatory phase following the U.S. FDA’s September 2025 Notice of Proposed Rulemaking on Generally Recognized as Safe criteria. The planned elimination of self-affirmed GRAS status is forcing manufacturers of novel natural thickeners to substantiate safety through third-party scientific consensus by late 2026. This shift materially raises the entry threshold for emerging ingredients while favoring incumbent suppliers with robust toxicological datasets, established usage histories, and transparent supply chains. As a result, procurement teams in food, beverage, and nutraceutical manufacturing are increasingly prioritizing thickeners with validated regulatory resilience rather than experimental functionality alone.

At the same time, supplier consolidation is reshaping product innovation pathways. The Tate & Lyle and CP Kelco integration, highlighted at IFT FIRST 2025, has streamlined North American access to citrus fibers and pectins, strengthening supply reliability for clean-label reformulation programs. Ingredion’s October 2025 launch of FIBERTEX CF underscores the growing role of citrus fibers as multifunctional natural thickeners, enabling up to 15% fat reduction in dressings without compromising viscosity or mouthfeel. Parallel R&D momentum is visible in alternative protein applications, where ADM’s 2025 Protein Report confirms that hydrocolloids and plant fibers are being engineered to deliver specific textural attributes such as chew, juiciness, and bite for whole-cut plant-based meats. Capacity investments, including CP Kelco’s $60 million citrus fiber expansion, further signal confidence in sustained demand for high-purity pectin and fiber systems across beverages, supplements, and reduced-sugar formulations.

Brazil: Upcycled Feedstocks and Sustainable Export Alignment

Brazil has consolidated its position as a strategic upstream hub in the natural thickeners market through scale, feedstock access, and sustainability credentials. The CP Kelco Matão facility reached full operational status for its second NUTRAVA Citrus Fiber line in 2025, anchoring Brazil’s role as a global center for nature-based texturizers derived from upcycled citrus peels. This investment aligns with growing international demand for circular economy inputs, particularly from European and North American buyers seeking traceable, low-waste ingredient solutions.

Policy support is reinforcing this trajectory. Late-2025 incentives for cassava and specialty maize cultivation are strengthening domestic supply chains for native starch thickeners, reducing dependence on chemically modified starch imports. Brazil’s dominance in pectin production remains intact, with more than 30 percent of global pectin exports now meeting sustainably sourced certification standards required by European retailers ahead of the 2026 selling season. This combination of agricultural integration, processing scale, and sustainability compliance positions Brazil as a preferred origin for clean-label thickeners in global food and beverage formulations.

China: Public Health Framing and Fermentation-Led Scale-Up

China’s natural thickeners market is increasingly shaped by public health objectives and industrial biotechnology investment. The February 2025 fiber fortification study conducted by Tate & Lyle and Creme Global demonstrated that fiber-based thickeners could help nearly half of Chinese adults achieve recommended daily fiber intake levels. This evidence base is influencing policy discussions around the inclusion of soluble fibers in sauces, condiments, and staple food products, creating structural demand beyond traditional texture modification.

Regulatory and industrial momentum is also visible on the export front. The 2025 FDA “no questions” GRAS response for Yantai Oriental Protein Tech’s pea-based formulation aids has enabled Chinese-origin pea starches to compete in high-performance plant-protein applications in the United States. Domestically, the Wuhan government’s $150 million allocation for a fermentation-focused industrial park is accelerating capacity for xanthan, gellan, and other microbial thickeners. This cluster strategy emphasizes yield optimization, traceability, and process transparency, positioning China as both a volume producer and an innovation center for fermentation-derived natural thickeners.

France: Enzyme-Driven Functionality and Regulatory Precision

France’s role in the natural thickeners market is defined by process innovation and regulatory alignment rather than scale alone. Roquette’s October 2025 launch of AMYSTA L 123 represents a notable advance in enzyme-driven starch processing, delivering thermal solubility and viscosity without chemical modification. This positions functional native starches as direct replacements for modified starches in instant beverages and soups, supporting clean-label reformulation initiatives scheduled for 2026.

Ingredion’s expansion of its NOVATION Lumina functional native starch range across EMEA further reinforces this trend, offering gel strength and viscosity performance comparable to modified variants while preserving simple ingredient declarations. Regulatory clarity is tightening in parallel. The European Food Safety Authority’s December 2025 guidance to reassess algal-derived functional additives signals heightened scrutiny of carrageenan and agar purity. Anticipated mid-2026 updates are expected to reshape sourcing and processing standards for seaweed-based thickeners, favoring suppliers with robust purification and documentation protocols.

India: Cost Sensitivity Meets Domestic Processing Scale

India’s natural thickeners market reflects a convergence of affordability, domestic processing expansion, and sector-specific innovation. At AAHAAR 2025, Cargill introduced a dent corn-based starch tailored to Indian sauces, addressing sensorial expectations such as color stability and fresh tomato aroma retention. This localization strategy acknowledges the importance of region-specific texture and flavor profiles in driving adoption.

Cost pressures are catalyzing alternative solutions. Cargill’s 2025 launch of a pectin replacer for confectionery applications targets value-conscious gummy and jelly producers seeking to reduce reliance on imported pectin. On the supply side, increased government allocations under the 2025–2026 Mega Food Parks scheme are accelerating the processing of guar and tamarind seeds into high-viscosity natural thickeners. These investments are strengthening India’s position as both a consumer and producer of plant-based thickening agents for food, textiles, and industrial applications.

Summary Table: Natural Thickeners Market – Country-Level Strategic Dynamics

Natural Thickeners Market County Level Snapshot

|

Country

|

Core Strategic Driver

|

Key Developments

|

Market Implication

|

|

United States

|

Regulatory tightening and supplier consolidation

|

FDA GRAS reform, citrus fiber and pectin expansions

|

Favors validated, clean-label incumbents

|

|

Brazil

|

Circular feedstocks and export sustainability

|

Citrus fiber scale-up, native starch incentives

|

Preferred origin for certified natural thickeners

|

|

China

|

Public health focus and fermentation scale

|

Fiber fortification studies, biotech parks

|

Expanding demand and global competitiveness

|

|

France

|

Enzyme processing and regulatory precision

|

Functional native starch innovation

|

Replacement of modified starches

|

|

India

|

Cost efficiency and domestic processing

|

Pectin replacers, Mega Food Parks

|

Broad-based adoption across food categories

|

Natural Thickeners Market Report Scope

Natural Thickeners Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.7 Billion

|

|

Market Size (2034)

|

$12.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Type (Starch-Based Thickeners, Gums and Hydrocolloids, Pectin, Seaweed-Derived Thickeners, Plant Fibers, Animal-Derived Thickeners), By Functionality (Thickening and Viscosity Control, Gelling, Stabilization and Suspension, Emulsification, Fat Replacement), By Source (Plant-Based, Microbial, Marine, Animal-Based), By Form (Dry Powder, Liquid), By End-Use Industry (Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Industrial Applications, Pet Food and Animal Nutrition)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ingredion, Cargill, Tate & Lyle, Archer Daniels Midland, Roquette, Kerry Group, International Flavors and Fragrances, Darling Ingredients, DSM-Firmenich, Jungbunzlauer, Gelymar, Nexira, Ashland, FMC, Wengfu Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Natural Thickeners Market Segmentation

By Type

- Starch-Based Thickeners

- Gums and Hydrocolloids

- Pectin

- Seaweed-Derived Thickeners

- Plant Fibers

- Animal-Derived Thickeners

By Functionality

- Thickening and Viscosity Control

- Gelling

- Stabilization and Suspension

- Emulsification

- Fat Replacement

By Source

- Plant-Based

- Microbial

- Marine

- Animal-Based

By Form

By End-Use Industry

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Industrial Applications

- Pet Food and Animal Nutrition

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Natural Thickeners Market

- Ingredion

- Cargill

- Tate & Lyle

- Archer Daniels Midland

- Roquette

- Kerry Group

- International Flavors and Fragrances

- Darling Ingredients

- DSM-Firmenich

- Jungbunzlauer

- Gelymar

- Nexira

- Ashland

- FMC

- Wengfu Group

*- List not Exhaustive