North America Mining & Mineral Processing Chemicals Market: Industry Growth Analysis and Value Forecast to 2034

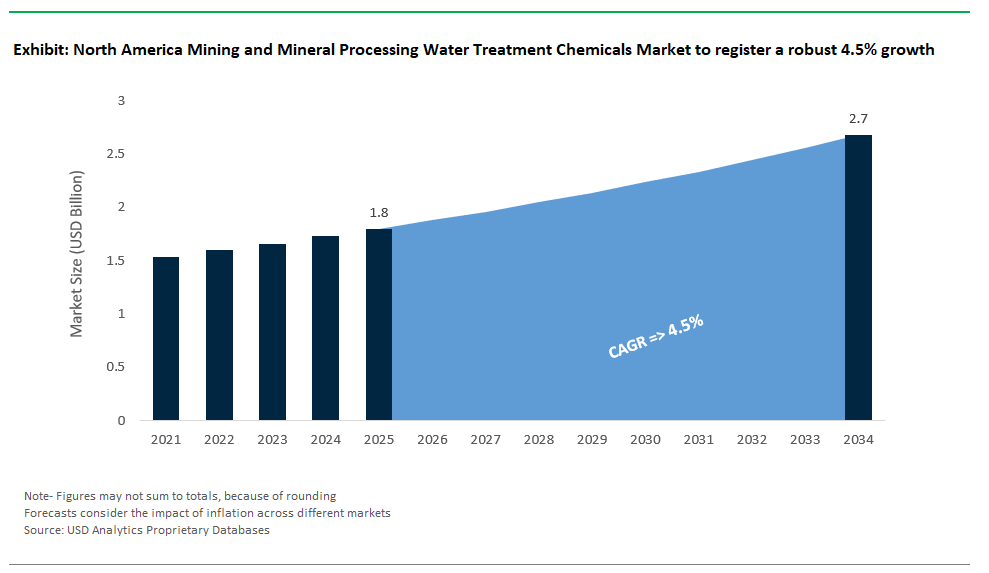

North America Mining and Mineral Processing Water Treatment Chemicals Market Size is estimated at $1.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 4.5% to reach $2.7 Billion by 2034.

The North American mining and mineral processing chemicals market plays a vital role in addressing environmental compliance, water reuse, and operational efficiency across one of the world’s most regulated and resource-intensive extractive industries. Acid rock drainage (ARD) remains a key concern, particularly in metal mining, where lime slurry is the standard treatment, as cited by EPA 530-R-94-036.

For more selective removal of toxic metals like mercury and arsenic, sulfide precipitation using sodium sulfide or sodium hydrosulfide is widely employed, dosed at 1.2–2x stoichiometric ratios to meet <0.01 mg/L effluent thresholds under NPDES discharge permits. In tailings management and mineral processing circuits, high molecular weight anionic polyacrylamide (PAM) flocculants are standard, delivering >70% underflow density in thickener operations, as validated by the Canadian MEND program. Cyanide destruction, essential for gold mining operations, relies on the SO₂/air process, which oxidizes free and complexed cyanide in alignment with Oregon DEQ's toxic control guidelines.

Water reuse and ZLD adoption are accelerating across high-TDS mines, where crystallization inhibitors particularly terpolymer blends enable system operation above 300,000 ppm TDS while limiting scaling to <0.1 mm/year per ASTM D5111 standards. As the sector faces mounting environmental scrutiny and freshwater constraints, North America’s mining chemical market is increasingly defined by precision dosing, selective removal technologies, and robust chemical formulations that enable both compliance and resource efficiency.

Market Trend: PFAS-Free and AI-Driven Closed-Loop Water Systems Reshape North American Mining

North America’s mining water treatment chemicals market is transitioning toward sustainable, closed-loop systems, propelled by a mix of regulatory tightening, resource scarcity, and ESG mandates from institutional investors. The EPA’s 2024 Effluent Guidelines and Canada’s Toxic Substances Reduction Act are forcing mines to phase out toxic depressants, sulfides, and PFAS-based formulations in favor of bio-based coagulants, starch-derived depressants, and non-toxic scale inhibitors. Leading operations like Rio Tinto’s Kennecott site are integrating AI-based dosing platforms, enabling real-time optimization of flocculant use and achieving >90% water recycling, reducing freshwater intake and cutting operational costs by millions annually. Technologies like Ecolab’s Nalco Water 360™, used in lithium brine extraction, not only align with sustainability goals but also deliver 35% reductions in sludge volumes, making them cost-effective and environmentally compliant. The trend reflects a deeper market realignment where carbon-neutral water management, ZLD infrastructure, and machine learning are no longer optional, but essential to remain competitive and compliant in the critical minerals value chain.

Market Opportunity: Lithium and Rare Earth Mining Catalyze $350M+ Demand for Advanced Water Treatment Chemicals

The rapid expansion of lithium and rare earth element (REE) recovery across North America is driving a $350M+ market opportunity for specialized water treatment chemicals by 2030. As Direct Lithium Extraction (DLE) becomes central to U.S. battery supply chains backed by DOE and DoD investments chemical solutions that can handle high-TDS, silica-rich brines are gaining traction. Innovations like EnergyX’s LiTAS™ system, supported by selective antiscalants and silica control agents, are boosting lithium yields by over 20% in Nevada pilot projects. Simultaneously, legacy REE tailings, particularly at sites like MP Materials’ Mountain Pass, are being re-mined using chitosan-based coagulants that enable both water recycling and neodymium recovery. Gold and silver mines are also shifting away from cyanide leaching, with companies like Barrick piloting thiosulfate-based biocides and microbial extraction techniques to meet TSCA and EPA compliance. With Inflation Reduction Act (IRA) tax credits, premium lithium prices exceeding $70,000/tonne, and ESG-linked financing contingent on sustainable water strategies, the chemical treatment segment has emerged as a critical enabler for the future of low-carbon, resource-secure mining in North America.

Competitive Analysis: North America Mining & Mineral Processing Water Treatment Chemicals Market

The competitive landscape in the North American mining and mineral processing water treatment chemicals market is changing due to a demand for precise formulations, local production models, and eco-friendly strategies. Tier 1 players, which include global specialists like Ecolab (Nalco), Solenis, BASF, and Kemira, hold more than half of the market. They provide mine-specific solutions and use unique technologies for tailings, process water, and wastewater treatment. Their advantage comes from distinct technologies like Ecolab’s “TailingsIQ” real-time monitoring systems and Solenis' high-MW flocculants for thickening. Additionally, their investments in regionally tailored chemicals for base metals, lithium, and rare earth processing, along with their expertise in zero-liquid discharge (ZLD) and PFAS-free reagents, have helped them secure contracts with major companies such as Freeport-McMoRan, Newmont, and Rio Tinto.

Tier 2 competitors, which include regional experts like ChemTreat, Clearwater Tech, and Accepta, make up 30% of the market. They provide niche solutions for challenging geographies and specific ore types. These companies use modular deployment models like mobile chemical blending units for Appalachian coal and bitumen recovery boosters in Canadian oil sands. They also form strategic alliances with Indigenous communities, which not only helps them comply with regulations but also makes operations feasible near remote and contested mining areas. Their capability to offer toll manufacturing and TOC-compliant chemicals sets them apart in smaller, compliance-sensitive markets such as Mexican silver and Central American gold.

Tier 3 participants, while fragmented, are vital in legacy and aggregate mines where cost is critical. This group consists of over 50 local blenders that supply low-cost, generic reagents, often undercutting larger competitors by 30% to 50%. Even though they lack strong R&D capabilities, they succeed in price-sensitive niches especially in abandoned coal mines and non-critical mineral operations where basic effectiveness is more important than innovation.

Competition is especially fierce in the process water segment (including frothers, depressants, and pH control) and the wastewater/tailings treatment segments, which together cover the entire market. Leading innovations such as BASF’s lithium-selective nanobubble flotation, Solenis’ “DryStack” polymers, and enzyme-assisted dewatering from the Novozymes-Ecolab partnership are setting new standards for recovery efficiency and environmental compliance. In addition, optimizing the supply chain has become a key way to stand out. On-site production units, like Kemira’s mobile SBR plants, rail-to-mine delivery hubs, and circular sourcing of chemicals like sulfuric acid, are cutting costs and ensuring consistent supply to remote mines.

Navigating regulations is another important skill that affects market share. Leaders are actively working with the EPA’s CWA Section 402 mandates, Canadian mining effluent rules, and Mexican wastewater standards. Companies like Ecolab and Kemira that provide bioassay-certified and pre-approved chemical solutions are more likely to win contracts in a procurement environment that increasingly focuses on ESG concerns.

Looking ahead, the growth of critical minerals such as lithium and rare earth elements opens new opportunities for competitive differentiation. Suppliers that can offer brine-selective reagents and flotation systems designed for high-value mineral separation will likely gain an edge. Additionally, engaging with Indigenous communities is shifting from a matter of social license to a strategic barrier to entry, with tribe-owned chemical supply businesses and co-managed infrastructure gaining regulatory and public support rapidly. Finally, there are emerging opportunities within the water-food-energy nexus, including the agricultural reuse of mine water and geothermal-lithium co-location, where chemical solutions will connect with priorities of the circular economy, further redefining the competitive landscape.

North America Mining & Mineral Processing Water Treatment Chemicals Market– Segmentation Insights (2025–2034)

By Type of Chemical: Coagulants Dominate, Heavy Metal Precipitants Accelerate

In the North American mining sector, coagulants and flocculants are expected to lead the market with a 2025 share of 29.8%, primarily driven by their essential role in tailings pond clarification, slurry dewatering, and suspended solids removal. These chemicals are critical to maintaining environmental compliance and process efficiency, especially in high-volume operations like copper and phosphate mining. Their effectiveness in solid-liquid separation and sedimentation makes them foundational to water treatment strategies in mineral processing plants across the United States and Canada.

However, the fastest-growing chemical type is heavy metal precipitants and chelating agents, projected to expand at a CAGR of 6.4% through 2034. This rapid growth is fueled by increasingly stringent environmental discharge regulations such as the U.S. EPA's Effluent Limitations Guidelines (ELGs) targeting selenium, mercury, arsenic, and other heavy metals. Mining operations are investing in advanced treatment systems using chelating agents and precipitating compounds like sodium dimethyldithiocarbamate (DMDTC) and TMT15 to meet zero-discharge mandates. Their adoption is accelerating in tailings management, mine dewatering, and groundwater remediation across both base and precious metal mining.

By Mineral Type: Base Metals Lead, Rare Earth Elements Show Fastest Growth

Base metals mining, including copper, zinc, lead, and nickel, is expected to hold the largest market share at 34.2% in 2025, solidifying its dominant role in North America’s water treatment chemicals market. Regions like Arizona, Utah, and northern Canada continue to host major copper and nickel mining operations where water treatment is essential for managing acid mine drainage, tailings pond water, and flotation circuits. These operations require extensive use of coagulants, scale inhibitors, and biocides to maintain water quality and meet environmental discharge standards.

Meanwhile, rare earth and specialty minerals are projected to grow at the fastest CAGR of 6.9% between 2025 and 2034, driven by the surge in electric vehicle (EV) and renewable energy supply chains. With mounting pressure to localize the critical minerals supply chain, mining operations for lithium, cobalt, and rare earths in North America are scaling rapidly particularly in Nevada, California, and Quebec. These operations demand high-purity process water and effective treatment systems to manage elevated concentrations of metals and radionuclides. This trend is positioning rare earth mineral processing as a high-growth niche for advanced water treatment solutions, including chelating agents, membrane cleaners, and specialty defoamers.

.png)

North America Mining and Mineral Processing Water Treatment Chemicals Report Scope

North America Mining and Mineral Processing Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$2.7 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, pH Adjusters and Neutralizers, Scale and Corrosion Inhibitors, Biocides and Disinfectants, Heavy Metal Precipitants and Chelating Agents, Filter Aids and Dewatering Aids, Defoamers and Antifoaming Agents, Other Specialty Chemicals), By Application in Mining and Mineral Processing (Tailings Management, Process Water Treatment, Wastewater Treatment, Dust Control, Cooling Water Treatment, Boiler Water Treatment, Water Reuse and Recycling), By Mineral Type (Base Metals Mining, Precious Metals Mining, Non-Metallic Minerals Mining, Iron Ore Mining, Rare Earth Elements and Specialty Minerals Mining, Uranium Mining), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Holding Company (U.S.), BASF SE (Germany), The Dow Chemical Company (U.S.), Veolia Water Technologies (France), ChemTreat, Inc. (U.S.), Buckman (U.S.), AECI Mining Chemicals (South Africa), Clariant (Switzerland),

|

|

Countries

|

US, Canada, Mexico

|

North America Mining and Mineral Processing Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- pH Adjusters and Neutralizers

- Scale and Corrosion Inhibitors

- Biocides and Disinfectants

- Heavy Metal Precipitants and Chelating Agents

- Filter Aids and Dewatering Aids

- Defoamers and Antifoaming Agents

- Other Specialty Chemicals

By Application in Mining and Mineral Processing

- Tailings Management

- Process Water Treatment

- Wastewater Treatment

- Dust Control

- Cooling Water Treatment

- Boiler Water Treatment

- Water Reuse and Recycling

By Mineral Type

- Base Metals Mining

- Precious Metals Mining

- Non-Metallic Minerals Mining

- Iron Ore Mining

- Rare Earth Elements and Specialty Minerals Mining

- Uranium Mining

By Form of Chemical

By Country

- United States

- Canada

- Mexico

Top Companies in North America Mining and Mineral Processing Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Holding Company (U.S.)

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- Veolia Water Technologies (France)

- ChemTreat, Inc. (U.S.)

- Buckman (U.S.)

- AECI Mining Chemicals (South Africa)

- Clariant (Switzerland)

* List Not Exhaustive

Research Coverage

This report investigates the North America Mining and Mineral Processing Water Treatment Chemicals Market in detail, delivering analysis reviews on key trends, regulatory drivers, and competitive dynamics shaping the sector from 2025 to 2034. It highlights breakthroughs such as PFAS-free chemistries, AI-driven dosing, and advanced ZLD systems that are redefining water management strategies in mining. USDAnalytics ensures the report serves as an essential resource for decision-makers seeking actionable insights into market opportunities across base metals, rare earths, and lithium mining. This comprehensive study addresses challenges in tailings management, process water optimization, and compliance frameworks, making it an indispensable tool for industry professionals navigating this rapidly evolving market.

Key Research Details:

- Segmentation:

- By Type of Chemical: Coagulants & Flocculants, pH Adjusters & Neutralizers, Scale & Corrosion Inhibitors, Biocides & Disinfectants, Heavy Metal Precipitants & Chelating Agents, Filter Aids & Dewatering Aids, Defoamers & Antifoaming Agents, Other Specialty Chemicals.

- By Application: Tailings Management, Process Water Treatment, Wastewater Treatment, Dust Control, Cooling Water Treatment, Boiler Water Treatment, Water Reuse & Recycling.

- By Mineral Type: Base Metals, Precious Metals, Non-Metallic Minerals, Iron Ore, Rare Earth Elements & Specialty Minerals, Uranium Mining.

- By Form: Liquid, Powder/Solid.

- Geographic Scope: United States, Canada, Mexico.

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Top Companies: Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Holding Company (U.S.), BASF SE (Germany), The Dow Chemical Company (U.S.), Veolia Water Technologies (France), ChemTreat, Inc. (U.S.), Buckman (U.S.), AECI Mining Chemicals (South Africa), Clariant (Switzerland).

Methodology

USDAnalytics applies a hybrid research approach that combines primary interviews with industry stakeholders—including mine operators, chemical formulators, and environmental compliance officers—with extensive secondary research from EPA, NPDES, and ASTM standards. Market estimations are derived through bottom-up modeling validated against capital spending trends in mining water management, ESG-driven investment patterns, and ZLD adoption rates. Forecasting uses advanced econometric models that incorporate regulatory shifts, commodity price scenarios, and technology penetration curves. Data triangulation ensures accuracy through validation with financial disclosures, technical white papers, and real-world case studies from leading mining regions across North America.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements