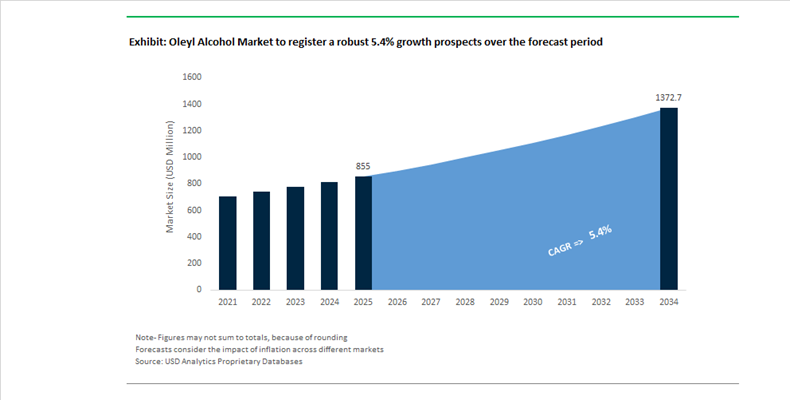

Oleyl Alcohol Market Valued at $855 Million in 2025, Forecast to Reach $1,372.6 Million by 2034 at 5.4% CAGR Driven by Bio-Based Surfactants and Specialty Emollients

The Oleyl Alcohol Market is valued at $855 Million in 2025 and is projected to reach $1,372.6 Million by 2034, expanding at a CAGR of 5.4%. Market growth is underpinned by accelerating demand for plant-derived fatty alcohols in personal care, pharmaceuticals, industrial lubricants, and specialty surfactants. Oleyl alcohol, a C18 unsaturated fatty alcohol derived primarily from natural oils, is increasingly positioned as a renewable alternative to petrochemical intermediates in emulsifiers, conditioning agents, and amine derivatives. Sustainability certifications, traceable palm oil sourcing, and EU Green Deal compliance requirements are reshaping procurement strategies across cosmetics and home care multinationals.

In July 2024, The Lubrizol Corporation signed a Memorandum of Understanding with the Government of Maharashtra to establish its largest Indian manufacturing site in Aurangabad. The facility is designed to support local-for-local supply of specialty performance additives and industrial oleyl alcohol derivatives in South Asia. In late 2024, BASF SE completed a multi-million-euro investment at its Düsseldorf site, which became fully operational in 2025. The upgrade included new reactor systems and advanced distillation units for high-purity fatty alcohols, directly strengthening production of specialty emollients for sun protection and dermocosmetic applications.

Capacity expansions accelerated in 2025. In April 2025, KLK OLEO announced a 20% expansion of its Johor fatty alcohol plant to meet rising Asia-Pacific demand for pharmaceutical and cosmetic-grade oleyl alcohol. In early 2025, Ecogreen Oleochemicals completed the addition of 180,000 tons per year at its Batam facility, effectively doubling its fatty alcohol capacity and reinforcing Indonesia’s position as a major global hub for plant-derived oleochemicals. In May 2025, Croda International advanced commissioning of its Guangzhou greenfield site, scheduled for mid-2025 start-up, featuring R&D laboratories dedicated to localized oleyl alcohol-based emulsifier development for Asian beauty markets. In August 2025, Kao Corporation inaugurated a new tertiary amine plant in the United States, expanding downstream demand for unsaturated fatty alcohol derivatives used in high-performance surfactants.

Application-side innovation reinforced structural demand. In 2024, Procter & Gamble expanded its European portfolio of shampoo bars under brands such as Herbal Essences, relying heavily on fatty alcohols including oleyl alcohol to deliver conditioning performance in water-reduced, plastic-free formats. In July 2025, KLK OLEO was upgraded to a Gold1 sustainability rating by RAM Sustainability, validating its traceable and deforestation-free sourcing model, a prerequisite for European cosmetic supply chains. In July 2025, Emery Oleochemicals appointed Min Chong as Group CEO, accelerating its ESG pivot and expanding DEHYPON® and EDENOR® lines built on oleic-derived alcohol chemistries. In January 2026, Croda International was recognized as Britain’s Most Admired Chemicals Company, reflecting momentum behind its 100% bio-based oleyl alcohol initiatives targeting clean beauty and biopharmaceutical formulations.

Oleyl Alcohol Market Trends and Opportunities

Trend: Capacity Expansion for Pharma-Grade Oleyl Alcohol in mRNA Therapeutics

Oleyl alcohol has moved decisively up the value chain, shifting from a conventional excipient to a strategically critical intermediate in the rapidly expanding mRNA therapeutics ecosystem. Its role in synthesizing ionizable cationic lipids positions oleyl alcohol at the core of Lipid Nanoparticle (LNP) delivery systems, which are essential for protecting mRNA payloads and enabling efficient intracellular delivery. As of December 2025, the global mRNA clinical pipeline has crossed 350 active trials spanning oncology, rare genetic disorders, and protein replacement therapies, structurally elevating demand for pharmaceutical-grade oleyl alcohol.

High-purity oleyl alcohol is a key building block for unsaturated ionizable lipids such as DLin-MC3-DMA, which are clinically preferred due to their superior endosomal escape performance. Industry benchmarks indicate that these lipids can improve transfection efficiency and therapeutic efficacy by roughly 25% compared to earlier-generation delivery chemistries. This performance dependency has forced chemical suppliers to re-engineer production lines toward injectable-grade specifications, where impurity control is non-negotiable.

A notable signal of this shift is the distillation upgrade investment announced by BASF at its Düsseldorf site. Operational by 2025, these upgrades focus on producing unsaturated fatty alcohols with ultra-low peroxide values, controlled acid numbers, and narrow isomer distributions tailored for LNP stability. Beyond capacity, purity itself has become the binding constraint. Injectable-grade oleyl alcohol is now expected to meet trans-isomer thresholds below 0.5%, pushing suppliers toward advanced molecular distillation technologies capable of isolating the cis-9 isomer. This purity-driven investment cycle is structurally tightening supply and supporting premium pricing across the pharmaceutical oleyl alcohol segment.

Trend: Clean Beauty Reformulation Toward Traceable and Non-Palm Feedstocks

Parallel to pharmaceutical demand, the personal care industry is reshaping oleyl alcohol sourcing under intense consumer and regulatory scrutiny of palm oil supply chains. Premium cosmetic and dermatological brands are increasingly mandating palm-free, traceable feedstocks to comply with sustainability reporting frameworks and deforestation regulations. This has accelerated the transition toward high-oleic sunflower and rapeseed-derived oleyl alcohol, particularly in Europe, North America, and advanced Asian markets.

The operationalization of this trend is visible in investments by Croda International, which commissioned a multi-purpose Active Beauty ingredients facility in Guangzhou, fully operational by 2025. The site prioritizes oleyl alcohol derivatives sourced from non-palm seed oils, aligning with EU Deforestation Regulation requirements that have fundamentally altered procurement strategies. For formulators, this shift is not merely reputational. Traceable non-palm oleyl alcohol offers more consistent oxidative stability and enables cleaner INCI labeling, which is increasingly tied to shelf placement and brand trust.

At the formulation level, derivatives such as Oleyl Erucate are gaining traction as functional replacements for natural Jojoba oil. Laboratory studies published in 2024 show that Oleyl Erucate delivers comparable skin-feel, spreadability, and oxidative resistance while reducing formulation costs by up to 15% in premium skincare. Supply-side confidence is further reinforced by capacity expansion from Ecogreen Oleochemicals, which doubled fatty alcohol capacity to 360,000 tons annually through its Batam expansion. While large in scale, this investment includes advanced fractionation units designed to serve high-end cosmetic markets that demand unsaturated, specialty-grade oleyl alcohol rather than bulk commodity output.

Opportunity: Bio-Based Carrier Oils for Precision Agricultural Adjuvants

A high-growth opportunity for oleyl alcohol is emerging in precision agriculture, as regulators tighten restrictions on petroleum-based surfactants and conventional methylated seed oils. Oleyl alcohol-derived alkoxylates are increasingly recognized as low-toxicity, high-performance adjuvants that enhance agrochemical delivery while aligning with sustainability mandates.

Field studies conducted in 2024 demonstrate that oleyl alcohol-based adjuvants significantly improve herbicide penetration through waxy leaf cuticles. This enhanced uptake enables a reduction in active ingredient loading by up to 10% without compromising weed control efficacy, directly supporting European Green Deal targets for chemical reduction. From a regulatory standpoint, recent reviews by the USDA Agricultural Marketing Service indicate growing acceptance of plant-derived fatty alcohol blends as growth regulators and contact agents, positioning oleyl alcohol favorably for organic and low-residue crop protection programs.

Environmental performance further strengthens this opportunity. Unlike nonylphenol ethoxylates that are being phased out globally due to aquatic toxicity, oleyl alcohol derivatives consistently meet OECD 301B “readily biodegradable” criteria. This classification enables their use in environmentally sensitive zones and buffer areas where legacy surfactants are prohibited, opening structurally protected demand channels in high-compliance agricultural markets.

Opportunity: Synthetic Lubricants for Arctic and Aerospace Environments

Oleyl alcohol derivatives also present a compelling opportunity in synthetic lubricants designed for extreme operating environments. Esters such as Oleyl Oleate exhibit exceptional low-temperature fluidity and high viscosity index stability, addressing performance gaps where mineral oils and conventional synthetics fail.

In Arctic energy exploration, these esters maintain pour points below −20°C, ensuring pumpability and film integrity during sub-zero operations. By 2025, they are increasingly specified in cutting oils and shear lubricants used in polar drilling and remote pipeline maintenance. Their naturally high viscosity index allows them to resist thinning at elevated temperatures while remaining fluid in extreme cold, a combination that is particularly valuable in aerospace actuators and defense systems exposed to rapid thermal cycling.

Data from suppliers such as Lubrizol and Sasol highlights growing adoption of oleyl alcohol-based esters in aerospace and marine equipment. In the North Sea, operators are actively substituting mineral-based deck lubricants with synthetic oleate esters to comply with 2025 environmental audit rules. These bio-lubricants eliminate surface sheen during incidental spills, reducing environmental liability while meeting performance requirements. Collectively, these factors position oleyl alcohol as a strategic feedstock in the next generation of high-performance, regulation-resilient lubricant systems.

Oleyl Alcohol Market Share and Segmentation Insights

Plant-Based Oleyl Alcohol Leads Supply with Certified Renewable Feedstocks and Clean Beauty Demand

Plant-based oleyl alcohol accounted for 78.60% of the Oleyl Alcohol Market by source in 2025, reflecting strong demand for renewable fatty alcohol ingredients across cosmetics, pharmaceuticals, and specialty chemical applications. Produced primarily from vegetable oils such as rapeseed, palm, and soybean, plant-derived oleyl alcohol aligns closely with clean beauty, vegan formulation, and sustainable ingredient sourcing requirements. Cosmetic manufacturers increasingly prioritize plant-based oleochemicals to ensure consistent quality and regulatory acceptance in global personal care formulations. A key development in 2025 is the expansion of supply chain traceability and sustainability certification programs, including RSPO and ISCC Plus, enabling cosmetic brands to validate renewable sourcing claims and strengthen premium product positioning in environmentally conscious consumer markets.

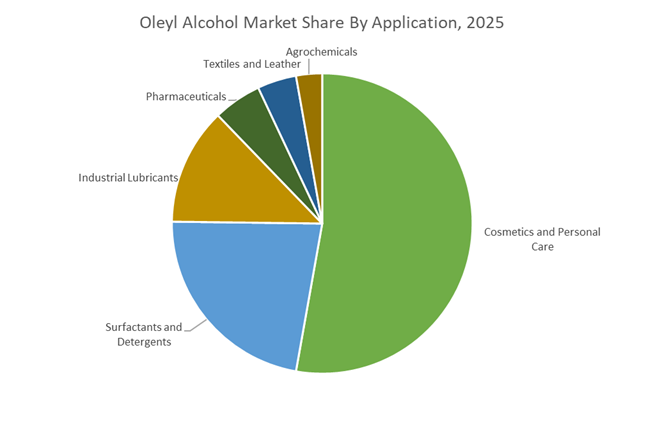

Cosmetics and Personal Care Segment Drives Oleyl Alcohol Consumption in High-Performance Skincare Formulations

Cosmetics and personal care represented 52.80% of the Oleyl Alcohol Market by application in 2025, making it the dominant demand segment supported by widespread use in skincare, haircare, and cosmetic formulations. Oleyl alcohol functions as a multifunctional ingredient, providing emolliency, texture stabilization, emulsifier support, and conditioning performance in creams, lotions, and hair treatment products. Its unsaturated fatty alcohol structure delivers a lightweight sensory profile and excellent compatibility with active cosmetic ingredients. A significant 2025 trend is the increasing use of high-purity oleyl alcohol in premium skincare formulations, particularly in serums, moisturizers, and targeted treatment products where smooth skin feel, stability, and ingredient transparency support high-value cosmetic product development.

Oleyl Alcohol Market Competitive Landscape

The oleyl alcohol market in 2026 is driven by high-purity unsaturated fatty alcohol demand, REACH compliance, and formula-lock partnerships in cosmetics and pharmaceuticals. Competitive advantage lies in feedstock precision, oxidation stability, and localized production hubs in Asia to support surfactant and personal care growth.

Croda drives high-purity oleyl alcohol demand through consumer care innovation and NPP-led growth strategy

Croda International is strengthening its leadership in premium oleyl alcohol through its “Refocusing Innovation” strategy, prioritizing high-margin consumer care and life sciences applications. With £1,699.4 million in 2025 sales and 6.6% growth, its Consumer Care segment expanded by 8%, driven by strong demand for high-purity emollients and penetration enhancers. NPP sales increased by 10%, supported by a 12% rise in co-creation pipeline value, reinforcing its formula-lock partnerships. Operational efficiencies delivered £28 million in benefits, with a target of £100 million by 2028 to fund advanced R&D. Croda’s focus on oxidation stability and sensory performance positions it strongly in waterless cosmetics. This innovation-led model secures its premium positioning in oleyl alcohol markets.

Ecogreen accelerates global fatty alcohol supply with large-scale expansion and RSPO-certified production

PT Ecogreen Oleochemicals is scaling its global footprint through a 180,000 TPA expansion at its Batam facility, reinforcing its position as a key supplier in the €1.08 billion fatty alcohol market. The company is targeting both personal care and industrial lubricants, leveraging oleyl alcohol’s biodegradability for metalworking fluids and surfactants. Its 2026 product pipeline emphasizes natural, clean-label fatty alcohols aligned with consumer and regulatory trends. Ecogreen’s adoption of RSPO-certified feedstocks ensures compliance with the European Deforestation Regulation (EUDR). Participation in global exhibitions highlights its focus on innovation and market visibility. This scale-driven and sustainability-aligned strategy strengthens its dominance in mass and specialty segments.

BASF strengthens regional supply with Verbund integration and cost-efficient specialty oleochemical production

BASF is leveraging its Zhanjiang Verbund site to provide localized oleyl alcohol supply across Asia-Pacific, which accounts for over 43% of global demand. With a projected EBITDA of €6.2–€7.0 billion in 2026, the company is focusing on high-margin oleochemical derivatives within its Nutrition & Care segment. Cost optimization efforts achieved €1.7 billion in savings, targeting €2.3 billion by 2026 to enhance pricing competitiveness. BASF’s strategy emphasizes low-VOC, high-purity formulations aligned with regulatory requirements. Its decarbonization roadmap supports sustainable production amid capacity expansion. This integrated and localized approach reinforces BASF’s leadership in specialty oleochemicals.

Wilmar secures global fatty alcohol supply with traceability leadership and downstream integration

Wilmar International is leveraging its scale and traceability advantage to dominate the oleyl alcohol supply chain, targeting 100% Traceability to Plantation (TtP) by 2026. With projected revenues of US$83.58 billion and strong volume growth in its Feed and Industrial Products segment, the company maintains robust market momentum. Its US$70 million acquisition of PZ Wilmar enhances downstream integration in surfactants and specialty chemicals. A 9.6% reduction in net debt strengthens its financial flexibility for renewable energy and oleochemical investments. Wilmar’s traceability and ESG alignment provide a competitive edge in regulated markets. This vertically integrated model ensures consistent supply and compliance.

Sasol advances high-purity oleyl alcohol innovation with digital R&D and sustainable feedstock diversification

Sasol is focusing on high-purity oleyl alcohol through its NACOL® and NOVEL® product lines, targeting pharmaceutical and specialty surfactant applications. The company is divesting low-margin assets to prioritize differentiated, high-specification products. Its “Digital Leap” strategy leverages AI to optimize ethoxylation processes, enhancing performance predictability in complex formulations. Sasol is increasing the use of bio-based feedstocks to mitigate geopolitical supply risks and align with sustainability mandates. Its European operations remain strong in hygiene and eco-friendly applications, where biodegradable oleyl alcohol derivatives are preferred. This focus on innovation and sustainability strengthens Sasol’s competitive positioning.

Indonesia – Biodiesel Prioritization Reshaping Fatty Alcohol Availability

Indonesia’s oleyl alcohol industry is entering a structurally constrained phase as national energy policy increasingly diverts palm-based feedstocks toward biodiesel production. In December 2025, the Ministry of Energy and Mineral Resources allocated 15.65 million kiloliters of palm-based biodiesel for 2026, materially tightening the availability of lauric oils and palm-derived fatty alcohol intermediates for industrial oleyl alcohol synthesis. This pressure is expected to intensify as the government accelerates implementation of the B50 mandate, with road testing initiated in early December 2025 to validate vehicle compatibility and supply readiness. As a result, oleochemical producers are recalibrating output toward higher-margin specialty alcohols rather than bulk volumes.

Domestic value addition and sustainability compliance are now decisive competitive levers. Ecogreen Oleochemicals continues to expand production at its Batam complex, enhancing capacity for its ECOROL® range to serve rising demand for blended saturated and unsaturated fatty alcohols across Asia Pacific. At the regulatory level, intensified enforcement is reshaping sourcing practices. In late 2025, the Attorney General’s Office identified potential state revenue of USD 8.5 billion from administrative fines linked to forest land-use violations, reinforcing a stricter deforestation-free compliance environment ahead of the 2026 export cycle. Parallel policy initiatives mandating full traceability to plantation by 2026 are compelling exporters to deploy digital monitoring systems to meet European Union Deforestation Regulation requirements, directly influencing the cost structure and export readiness of Indonesian oleyl alcohol suppliers.

United States – Clean Beauty Demand and Localized Supply Chain Realignment

The United States oleyl alcohol market is increasingly downstream driven, shaped by clean-label consumer trends, pharmaceutical purity requirements, and trade realignments. Infrastructure investment remains a key signal. In March 2025, BASF announced significant upgrades to its U.S. manufacturing assets to support growing demand for long-life lubricants and performance additives, with completion milestones extending into 2026. At the same time, new tariff measures introduced in early 2025 have disrupted traditional import flows, prompting domestic producers to reinforce local-for-local supply chains for oleyl alcohol derivatives and related surfactants.

Innovation is centered on purity enhancement and sustainability. Ashland and peer manufacturers are advancing enzymatic synthesis routes to achieve higher-purity oleyl alcohol grades suited for advanced pharmaceutical drug delivery systems. Renewable energy integration is accelerating across U.S. chemical sites, with producers targeting 15 to 20% lifecycle carbon emission reductions in fatty alcohol manufacturing by 2026. On the demand side, clean beauty formulations are acting as a strong pull factor. Industry data indicates a double-digit increase in cosmetic formulations incorporating natural fatty alcohols, driving substitution of synthetic cetyl alcohol with biodegradable oleyl alcohol. Regulatory tightening around PFAS is also reinforcing adoption in bio-based lubricant blends for automotive and industrial applications.

Malaysia – Traceability Leadership and Portfolio Consolidation

Malaysia’s oleyl alcohol industry continues to differentiate itself through traceability depth, strategic expansion, and consolidation across the oleochemical value chain. Market access remains a strategic priority. KLK OLEO expanded its international footprint in February 2025 by opening a representative office in India, strengthening export pathways for oleyl-based esters and specialty fatty alcohols into South Asia. Innovation branding is also evolving. Croda International marked its centenary in early 2025 by reinforcing its Smart Science platform, with a sharper focus on transitioning high-performance ingredients away from petrochemical feedstocks toward renewable oleyl alcohol derivatives.

Supply chain governance is now a prerequisite for market continuity. Wilmar International reported traceability levels exceeding 98% to mill and over 90% to plantation by late 2024, with full NDPE compliance targeted by the end of 2025. This governance push has been complemented by portfolio consolidation. In June 2025, Wilmar moved to acquire the remaining stake in its joint venture with PZ Cussons, consolidating control over consumer-facing oleochemical operations. Digitalization has become embedded, with AI-enabled satellite monitoring and supplier reporting platforms now standard for Malaysian exporters seeking continued access to European personal care and detergent markets in 2026.

Germany – Margin Protection Through Specialization and Regulatory Alignment

Germany’s oleyl alcohol market is defined by strategic specialization and regulatory-driven portfolio optimization. In 2025, Evonik Industries advanced its Tailor Made efficiency program, restructuring the majority of its business lines to prioritize high-margin Custom Solutions, including specialty oleyl alcohol derivatives for coatings, textiles, and industrial formulations. This repositioning is occurring against a backdrop of subdued demand conditions in late 2025, prompting German producers to consolidate non-core Asian operations while safeguarding European production hubs through 2026.

Sustainability reporting and regulatory compliance are shaping product strategy. Kao Corporation, through its European operations, emphasized accelerated growth in environmentally compliant product lines in its 2025 sustainability disclosures, reinforcing demand for responsibly sourced fatty alcohols. Concurrently, German manufacturers are refining portfolios to align with updated European Biocidal Products Regulation requirements and revised ECHA fee structures, particularly for cleaning and textile applications using oleyl alcohol. This regulatory environment favors suppliers capable of delivering compliant, high-purity derivatives with documented environmental performance.

India – Manufacturing Scale-Up and Downstream Consumption Growth

India’s oleyl alcohol industry is transitioning from an import-reliant model toward localized manufacturing and downstream diversification. Capacity expansion is a central theme. Lubrizol entered into an agreement with the Maharashtra state government to develop its largest global manufacturing site in Aurangabad, securing domestic supply of industrial-grade oleyl alcohol and derivatives for lubricants and performance additives. This investment aligns with the government’s broader Science and Technology Clusters initiative, which aims to expand innovation hubs from eight to twenty-five by 2028, supporting localized R&D in oleochemicals and specialty surfactants.

Policy incentives are accelerating demand across multiple end-use sectors. The Make in India program is catalyzing growth in agrochemicals, textiles, and coatings, all of which rely heavily on oleyl alcohol-based surfactants and dispersants. At the formulation level, adoption of oleyl amine derivatives is rising in the Indian paints and coatings industry as manufacturers seek low-VOC alternatives to meet tightening environmental norms. These combined factors position India as a high-growth consumption and manufacturing base for oleyl alcohol over the medium term.

Strategic Country Comparison – Oleyl Alcohol Industry

Oleyl Alcohol Market County Level Snapshot

|

Country

|

Core Structural Driver

|

Supply or Technology Focus

|

Strategic Direction

|

|

Indonesia

|

Biodiesel mandates and traceability

|

Palm-derived fatty alcohols

|

Value-added processing under supply constraints

|

|

United States

|

Clean beauty and tariff shifts

|

High-purity and bio-based derivatives

|

Localized supply chains and premium applications

|

|

Malaysia

|

Traceability and consolidation

|

Certified palm oleochemicals

|

Premium export hub for regulated markets

|

|

Germany

|

Margin protection and regulation

|

Specialty oleyl alcohol derivatives

|

Compliance-led specialization

|

|

India

|

Industrial expansion and incentives

|

Domestic manufacturing and low-VOC chemistries

|

Rapid demand and capacity growth

|

Oleyl Alcohol Market Report Scope

Oleyl Alcohol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$855 Million

|

|

Market Size (2034)

|

$1372.6 Million

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Source (Plant-Based, Animal-Based), By Grade (Pharmaceutical Grade, Cosmetic Grade, Industrial Grade), By Application (Cosmetics and Personal Care, Surfactants and Detergents, Pharmaceuticals, Industrial Lubricants, Textiles and Leather, Agrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Croda International, Kao, BASF, Wilmar International, KLK OLEO, Evonik Industries, Ecogreen Oleochemicals, Lubrizol, Sasol, Stepan, Ashland, Procter & Gamble, Emery Oleochemicals, Nouryon, Godrej Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oleyl Alcohol Market Segmentation

By Source

By Grade

- Pharmaceutical Grade

- Cosmetic Grade

- Industrial Grade

By Application

- Cosmetics and Personal Care

- Surfactants and Detergents

- Pharmaceuticals

- Industrial Lubricants

- Textiles and Leather

- Agrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oleyl Alcohol Industry

- Croda International

- Kao

- BASF

- Wilmar International

- KLK OLEO

- Evonik Industries

- Ecogreen Oleochemicals

- Lubrizol

- Sasol

- Stepan

- Ashland

- Procter & Gamble

- Emery Oleochemicals

- Nouryon

- Godrej Industries

*- List not Exhaustive