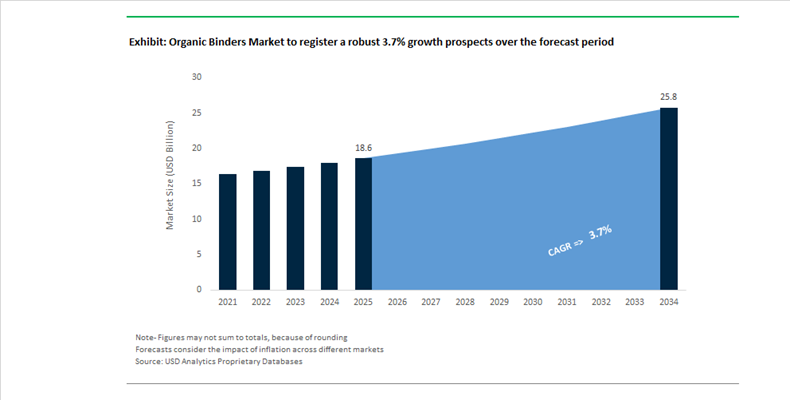

Organic Binders Market Valued at $18.6 Billion in 2025, Projected to Reach $25.8 Billion by 2034 at 3.7% CAGR Driven by Battery, Adhesives, and Bio-Based Polymer Innovation

The Organic Binders Market is valued at $18.6 billion in 2025 and is projected to reach $25.8 billion by 2034, expanding at a CAGR of 3.7%. Market momentum is anchored in lithium-ion battery manufacturing, sustainable coatings, paper and board processing, animal feed binders, and water-soluble polymer systems used in oilfield and municipal treatment applications. Increasing substitution of solvent-borne chemistries with water-based organic binders, combined with decarbonization mandates across Europe and North America, is reshaping product portfolios. Battery electrode binders, acrylic emulsions, styrene-butadiene latex, cellulose derivatives, PVDF binders, and bio-based rheology modifiers represent high-value growth segments. Supply chain localization in North America and Europe is accelerating to support EV battery gigafactories and circular packaging mandates.

In March 2025, BASF SE scaled up U.S. production of Licity® water-based anode binders at Monaca, Pennsylvania, and Chattanooga, Tennessee. These organic binders are engineered to replace solvent-borne systems in lithium-ion battery electrodes, improving capacity retention and fast-charging performance while supporting regional EV manufacturing. In June 2025, BASF transitioned its Rheovis® rheology modifiers to bio-based ethyl acrylate feedstock, achieving up to 35% biogenic content and reducing carbon footprint by approximately 30% for coatings and adhesive applications. In 2025, BASF further strengthened sustainable packaging chemistry with Basonal® PLUS 7988, a high-performance organic binder for paper and board topcoats targeting FMCG packaging decarbonization.

Battery-grade binder capacity also expanded at Arkema SA, which confirmed completion of its Kynar® PVDF binder expansion in the United States ahead of K 2025. PVDF binders remain critical for cathode integrity and thermal stability in high-energy-density lithium-ion systems. In late 2025, SNF Group signed an agreement to acquire Syensqo’s Oil & Gas division for €135 million, expanding its portfolio of water-soluble organic binders for enhanced oil recovery and fluid management, with closing expected in early 2026. Meanwhile, Solenis LLC continued integrating Diversey through 2024 and 2025, launching smart dosing systems to optimize binder consumption in paper and board manufacturing.

Agricultural and feed applications are also driving binder innovation. In November 2025, Cargill Incorporated expanded its Austrian micronutrition facility by 50%, strengthening feed binder production for high-integrity pelleted nutrition. In October 2025, Alltech Inc. introduced Mycosorb® Evo, a yeast-cell-wall-based organic binder designed to mitigate mycotoxins in livestock feed. Adhesive technologies remain resilient, with Henkel AG & Co. KGaA reporting 2.5% organic sales growth in Q3 2025, supported by automotive and electronics demand for advanced binder chemistries.

Sustainability-driven R&D continues to reshape binder chemistry. In late 2024, the CELLIGHT project launched by VTT in Finland began developing cellulose-based organic binders to replace mineral and synthetic systems in paints and cosmetics. In February 2026, Kemira Oyj completed its acquisition of SIDRA Wasserchemie, strengthening its European position in organic coagulant binders for municipal and industrial wastewater treatment.

Organic Binders Market Trends and Opportunities

Trend: Strategic Shift to Aqueous Bio-Binders in Lithium-Ion Battery Manufacturing

The lithium-ion battery industry is undergoing a structural transition away from solvent-based polyvinylidene fluoride binders toward aqueous, bio-derived organic binders, driven by cost pressure, safety imperatives, and decarbonization targets at Gigafactory scale. The elimination of N-Methyl-2-pyrrolidone from electrode processing has become a priority across Asia, Europe, and North America, as manufacturers seek to simplify production lines and reduce energy intensity. Industry transition data from 2024–2025 shows that replacing NMP-based PVDF systems with water-soluble binders such as carboxymethyl cellulose and starch-derived polymers can reduce solvent recovery energy consumption by up to 70%. This translates directly into lower operating expenditure while improving occupational safety and regulatory compliance.

A key catalyst accelerating adoption is the scaling of commercial, battery-grade aqueous binders. In April 2025, BASF expanded manufacturing capacity in Monaca, Pennsylvania and Chattanooga, Tennessee to support global demand for Licity® anode binders. These bio-compatible systems are engineered to accommodate silicon-rich anodes, which require higher elasticity and adhesion to manage volumetric expansion during cycling. Parallel academic and industrial validation has also closed the historical performance gap. Research published in 2024 confirmed that next-generation water-based binders for high-voltage NMC cathodes now achieve electrochemical stability comparable to PVDF, while reducing lithium leaching and current collector corrosion. Collectively, these advances position aqueous organic binders as a foundational material in next-generation battery manufacturing.

Trend: Premiumization of Animal Feed Pelleting with Multi-Functional Organic Binders

In animal nutrition, organic binders are evolving from commodity pellet aids into performance-critical formulation components, particularly in aquaculture and premium pet food. Modern feed mills operating at throughputs exceeding 30 metric tons per hour impose extreme thermal and mechanical stress during conditioning and pelleting, favoring high-purity natural binders such as modified starches, alginates, and plant gums. These binders maintain structural integrity at conditioning temperatures above 85°C, ensuring pellet durability and minimizing fines during transport and handling.

Aquaculture has emerged as a focal growth segment. In Southeast Asian shrimp and fish farming systems, alginate- and pectin-based binders are increasingly specified for their ability to prevent nutrient leaching for up to four hours in water, improving feed conversion ratios and reducing eutrophication risk. Beyond mechanical stability, 2025 formulations increasingly use organic binders as functional matrices for probiotics, enzymes, and micronutrients. By embedding heat-sensitive actives within the binder phase, feed producers report an average 15% reduction in fines and nutritional losses, reinforcing the role of organic binders as enablers of precision nutrition rather than passive additives.

Opportunity: Low-Temperature Cure Organic Binders for 3D Sand Printing and Binder Jetting

Additive manufacturing in foundries is creating a high-margin opportunity for organic binders optimized for low-temperature cure, rapid strength development, and minimal gas evolution. As engine blocks and aerospace castings shift toward complex geometries produced via 3D sand printing, traditional furan and phenolic systems face increasing regulatory pressure due to volatile organic compound and formaldehyde emissions. In response, foundries are adopting bio-based resins and modified organic systems compatible with updated OSHA and EU REACH requirements.

During 2024–2025, cold-hardening phenolic and hybrid organic-inorganic binder systems were optimized for cure-in-box workflows, reducing post-curing time by up to 30% for intricate cores. Recent studies show that incorporating organic modifiers such as methylcellulose and rice starch into inorganic binders significantly improves dimensional accuracy, achieving near-optimal desirability indices for aluminum and magnesium castings. When combined with topology-optimized printing software, these organic binder systems also enable 20–30% reductions in sand and binder consumption, improving both cost efficiency and sustainability metrics for foundry operations.

Opportunity: Eco-Benign Organic Binders for Dust Suppression and Soil Stabilization

Stricter enforcement of particulate matter limits in mining and construction is converting dust suppression into a regulated chemical application rather than a discretionary water-spraying practice. Organic binders derived from polymers, molasses, and lignosulfonates are increasingly specified to control PM2.5 and PM10 emissions in arid and semi-arid regions. Field data from 2025 mining operations shows that switching from water-only suppression to organic binder emulsions can reduce particulate emissions by more than 60%, forming durable surface crusts that remain effective for up to four weeks without reapplication.

Regulatory developments are reinforcing this demand. In late 2025, pollution control authorities in India and the United States mandated continuous air quality monitoring and fugitive dust control as conditions for mining permits, directly favoring biodegradable binders that meet PM10 and PM2.5 thresholds. Draft sustainable mining guidelines also emphasize groundwater protection, prioritizing environmentally benign organic binders over synthetic chemical stabilizers for haul roads, tailings management, and greenbelt development. As a result, dust suppression and soil stabilization represent a scalable, compliance-driven growth avenue for organic binder suppliers aligned with environmental and social governance expectations.

Organic Binders Market Share and Segmentation Insights

Synthetic Organic Binders Lead Market Demand with High-Performance Polymer Systems for Industrial Formulations

Synthetic organic binders accounted for 68.40% of the Organic Binders Market by material type in 2025, reflecting strong demand for high-performance polymer systems across industrial manufacturing sectors. Materials such as acrylics, polyurethanes, epoxies, vinyl polymers, and styrene-butadiene binders dominate due to their superior adhesion strength, durability, and formulation flexibility in coatings, adhesives, and construction chemicals. These engineered polymer binders enable manufacturers to tailor mechanical strength, chemical resistance, and curing performance to meet demanding industrial specifications. A notable 2025 innovation trend is the development of bio-based synthetic hybrid binders, where renewable monomers are incorporated into conventional polymer structures to increase renewable carbon content while maintaining the performance characteristics required for advanced industrial applications.

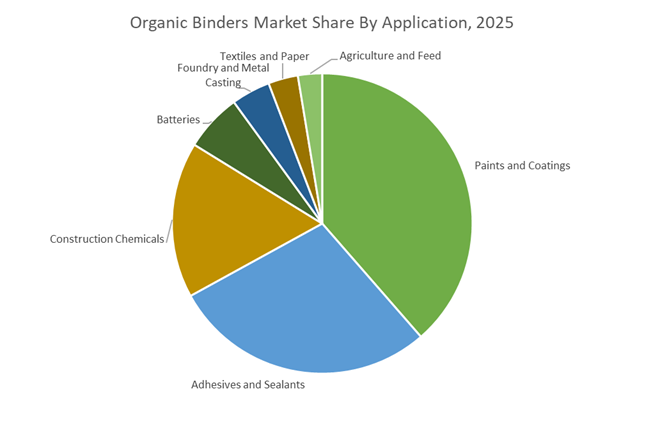

Paints and Coatings Segment Drives Organic Binder Consumption in Global Coating Production

Paints and coatings represented 38.60% of the Organic Binders Market by application in 2025, making it the largest demand segment due to the central role of binders as the film-forming component in coating formulations. Organic binders provide adhesion, durability, weather resistance, and protective barrier properties in architectural coatings, industrial finishes, and automotive paints. The scale of global coating production significantly influences binder consumption across multiple manufacturing sectors. In 2025, the industry is increasingly shaped by the low-VOC coating transition, where manufacturers are developing advanced water-based and high-solids binder technologies, including acrylic, polyurethane, and epoxy systems, designed to meet environmental regulations while preserving coating performance in demanding industrial and architectural applications.

Organic Binders Market Competitive Landscape

The organic binders market in 2026 is driven by bio-based dispersions, VOC-compliant formulations, and carbon footprint transparency. Competitive differentiation centers on mass-balance certified polymers, high-solids binder efficiency, and PCF-enabled solutions supporting Scope 3 reporting across coatings, construction, adhesives, and sustainable materials applications.

BASF drives carbon-transparent binder innovation through Verbund localization and cost-optimized production

BASF is reinforcing its leadership in organic binders through its “Winning Ways” strategy, combining Verbund integration with localized production in high-growth Asia-Pacific markets. The Zhanjiang Verbund site strengthens supply of high-performance water-based binders under a “local-for-local” model. With a projected 2026 EBITDA of €6.2–€7.0 billion, BASF continues to scale specialty binder solutions across coatings and construction sectors. Cost optimization initiatives have achieved €1.7 billion in savings, targeting €2.3 billion to maintain pricing competitiveness. Its Carbon Footprint Ledger enables precise PCF tracking, aligning with decarbonization mandates. This integration of scale, efficiency, and carbon transparency positions BASF as a dominant player in sustainable binder technologies.

Wacker enhances VAE binder competitiveness through PACE-driven efficiency and global polymer market resilience

Wacker Chemie is strengthening its position in VAE-based organic binders through its PACE program, targeting over €300 million in annual savings by 2026. Despite 2025 sales of €5.49 billion, the company expects stable growth supported by volume recovery and operational efficiency. Its Polymers division generated €1.38 billion, with strong demand for high-performance binders in construction and specialty applications. EBITDA is forecast between €550 million and €700 million, reflecting improved cost structures. With 83% of revenue generated خارج Germany, Wacker maintains a diversified global presence. This efficiency-led strategy ensures competitiveness in high-purity binder formulations and evolving construction markets.

Dow advances bio-based binder adoption with renewable feedstocks and circular polymer integration

Dow is leveraging its “Sustainability Science” platform to expand bio-based organic binders, including formulations with up to 35% renewable carbon content. These binders deliver performance parity with conventional acrylics while offering improved lifecycle emissions profiles. Its Ecolibrium™ and Decarbia™ brands support low-carbon and circular economy solutions, reinforced by ISCC-certified AFFINITY™ RE elastomers. With $43 billion in sales and global operations across 31 countries, Dow stabilizes feedstock supply for vinyl acetate and polymer dispersions. Strategic initiatives like MobilityScience™ highlight binder applications in automotive and electronics sectors. This innovation-driven approach positions Dow as a leader in sustainable polymer binder systems.

Sika accelerates construction binder growth through acquisition-led expansion and efficiency optimization

Sika is strengthening its organic binder portfolio through its “Fast Forward” program, targeting CHF 80 million in savings in 2026 and up to CHF 200 million by 2028. The company’s acquisition strategy, including seven bolt-on deals in 2025, enhances its manufacturing footprint and regional market penetration. With expected sales growth of 1% to 4% and EBITDA margins nearing 20%, Sika demonstrates strong financial resilience. Its focus on high-performance binders supports applications in sustainable construction and infrastructure. Growth momentum is expected to improve in the second half of 2026, particularly in emerging regions. This strategy positions Sika as a key player in construction-grade binder innovation.

Ashland expands biodegradable binder solutions with strategic partnerships and high-purity product focus

Ashland is advancing its organic binder portfolio through its “Innovate and Globalize” strategy, emphasizing high-purity, biodegradable polymer systems. The IMCD partnership enhances distribution of specialty binders across the U.S. market, improving customer access and technical support. With Q1 FY2026 sales of $386 million, the company is focusing on pharmaceutical excipients and advanced coatings applications. The EPA-approved agrimer™ eco-coat binder, derived from vegetable oils, addresses demand for sustainable and low-VOC solutions. Operating in over 100 countries, Ashland prioritizes R&D in clean-label and regulatory-compliant chemistries. This positions the company as a strong innovator in bio-based binder technologies.

Germany – Regulation-Led Circularity and High-Value Binder Innovation

Germany’s organic binders industry is being reshaped by a regulatory pivot toward circular material management and low-emission production systems. In January 2025, the European Union introduced an updated Best Available Techniques Reference Document that requires foundries to evaluate organic binder waste streams for composting as a route to solid waste reduction. German regulators have been instrumental in operationalizing this mandate, embedding waste-to-resource logic into foundry compliance audits. This shift gained industrial validation through the Green Foundry LIFE project, where large-scale 20-ton trials completed in 2025 demonstrated that spent organic binder sands can be remediated via controlled composting without compromising environmental safety or downstream reuse potential.

Parallel to regulatory change, Germany remains a focal point for high-value organic binder innovation. BASF SE advanced capital investments during 2024–2025 to scale production of anode binders engineered for high-capacity silicon-based lithium-ion batteries, reinforcing Germany’s position in next-generation electric vehicle materials. In adhesives, Henkel AG launched bio-based organic binders in 2025 that reduced lifecycle carbon footprint by roughly one-third versus conventional polyurethane systems. Regulatory pressure on volatile organic compounds has intensified, with Germany’s Federal Environment Agency tightening emission thresholds for industrial coatings in late 2025, accelerating substitution toward waterborne acrylic binder chemistries. Germany’s research ecosystem further supports transition, exemplified by collaborations led by the Technical University of Munich to develop protein-based wood binders that eliminate formaldehyde in engineered wood products.

China – Scale Leadership and Standards-Driven Quality Upgrades

China continues to dominate global organic binder production, particularly in battery-grade materials. As of 2025, the country leads PVDF organic binder output, with producers such as Shandong Huaxia Shenzhou expanding capacity to meet the majority of global demand generated by electric vehicle battery manufacturing. Quality control has become a strategic priority. In late 2025, the Ministry of Industry and Information Technology introduced stricter purity standards for organic binders used in nickel manganese cobalt cathodes, targeting improved thermal stability and safety in high-voltage battery platforms.

Structural reorganization is reinforcing these quality gains. Beijing is enforcing a 2026 deadline for consolidation of small-scale resin facilities, steering production into large green chemical parks equipped with AI-enabled process controls to reduce binder slurry waste and improve yield consistency. Beyond batteries, China is extending organic binder innovation into adjacent sectors. Participation in the Green Shipping Corridors initiative with Brazil and India is accelerating the adoption of zero-emission coatings that rely on organic binder systems. In agriculture, starch-based binders for fertilizer granulation gained momentum in 2025 under the Zero Growth policy, enabling biodegradable nutrient-release formulations that align with national soil and water protection goals.

United States – Supply Chain Localization and Battery Binder Commercialization

The United States organic binders market is increasingly defined by domestic supply chain security and application-led innovation. Under the Inflation Reduction Act, the Department of Energy awarded grants in 2025 to support localized production of advanced organic binders, with Ashland Inc. among the beneficiaries focused on cellulose-based systems for the domestic gigafactory network. Product development translated quickly into commercialization. In May 2025, Ashland introduced a new generation of water-soluble battery binders at The Battery Show Europe, designed to enhance mechanical integrity and cycling stability in high-silicon anode architectures.

Traditional industrial sectors are also modernizing. The U.S. foundry industry recorded a notable increase in adoption of cold-box organic binders during 2025, driven by automotive demand for complex, lightweight castings. Feedstock diversification is another defining trend. Cargill expanded industrial starch capacity in 2025 to supply modified organic binders for paper and packaging, replacing synthetic latex systems. Regulatory facilitation is supporting innovation, with mid-2025 updates to the Environmental Protection Agency’s TSCA inventory enabling faster approval of bio-polymer binders that demonstrate reduced toxicity profiles relative to incumbent chemistries.

India – Capacity Build-Out and Bio-Based Binder Development

India’s organic binders industry is scaling rapidly, supported by infrastructure investment and policy-driven green chemistry initiatives. In 2025, ARCL Organics Ltd. completed a significant capacity upgrade incorporating high-efficiency formalin technology to produce higher solid-content binders for plywood and foundry applications. Demand fundamentals remain strong. India’s expanding automotive manufacturing base drove a double-digit increase in consumption of phenolic resin binders for friction materials and brake linings by late 2025, reinforcing the role of organic binders in mobility-related value chains.

Public funding is catalyzing bio-based innovation. Under Mission Anveshan, government-backed programs are supporting lignin-derived organic binders sourced from agricultural residues for iron ore pelletization, reducing reliance on fossil-based inputs. Industry collaboration is also intensifying. Sudarshan Chemical Industries announced strategic partnerships in 2025 to integrate advanced organic binder technologies into high-performance pigment dispersions, linking binder functionality directly to color strength, dispersion stability, and end-use durability.

Brazil – Bio-Feedstock Advantage and Construction-Led Demand

Brazil’s organic binders industry benefits from abundant agricultural feedstocks and expanding infrastructure demand. Leveraging large-scale sugarcane and soy production, Brazil has emerged as a leading supplier of ethanol-derived and soy-protein organic binders. Exports to the European Union increased markedly in 2025, reflecting demand for renewable and traceable binder solutions that comply with tightening sustainability standards. This bio-feedstock advantage positions Brazil favorably as global buyers seek alternatives to petrochemical-derived binders.

The country is also advancing application diversity. Alongside China and India, Brazil launched green shipping corridor initiatives in late 2025, prioritizing bio-based anti-fouling coatings that rely on organic binder matrices for marine durability. Domestically, a federal housing stimulus program triggered a sharp rise in demand for polymer-modified organic binders used in construction mortars and tile adhesives. These developments underscore Brazil’s dual role as both a raw-material-driven exporter and a fast-growing consumer market for organic binder technologies.

Strategic Country Comparison – Organic Binders

Organic Binders Market County Level Snapshot

|

Country

|

Primary Structural Driver

|

Key Binder Applications

|

Strategic Position

|

|

Germany

|

Circular regulation and VOC limits

|

Foundry, batteries, wood adhesives

|

Compliance-led innovation hub

|

|

China

|

Scale and purity standards

|

Battery electrodes, fertilizers

|

Global volume and quality leader

|

|

United States

|

Supply chain localization

|

Batteries, foundry, packaging

|

Application-driven commercialization

|

|

India

|

Capacity expansion and green policy

|

Automotive, mining, plywood

|

Rapidly scaling domestic market

|

|

Brazil

|

Bio-feedstock availability

|

Construction, marine coatings

|

Renewable binder export base

|

Organic Binders Market Report Scope

Organic Binders Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.6 Billion

|

|

Market Size (2034)

|

$25.8 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Material Type (Natural Organic Binders, Synthetic Organic Binders), By Form (Liquid, Powder, Granulates, Solid Resin), By Application (Paints and Coatings, Adhesives and Sealants, Foundry and Metal Casting, Batteries, Construction Chemicals, Agriculture and Feed, Textiles and Paper)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Arkema, Ashland, Dow, Wacker Chemie, Hexion, Evonik Industries, Solvay, Kureha, DIC, Celanese, Cargill, ARCL Organics, Zeon, Huntsman

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Binders Market Segmentation

By Material Type

- Natural Organic Binders

- Synthetic Organic Binders

By Form

- Liquid

- Powder

- Granulates

- Solid Resin

By Application

- Paints and Coatings

- Adhesives and Sealants

- Foundry and Metal Casting

- Batteries

- Construction Chemicals

- Agriculture and Feed

- Textiles and Paper

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organic Binders Industry

- BASF

- Arkema

- Ashland

- Dow

- Wacker Chemie

- Hexion

- Evonik Industries

- Solvay

- Kureha

- DIC

- Celanese

- Cargill

- ARCL Organics

- Zeon

- Huntsman

*- List not Exhaustive