Organic Substrate Packaging Material Market Expected to Reach $24.2 Billion by 2034 at 4.3% CAGR

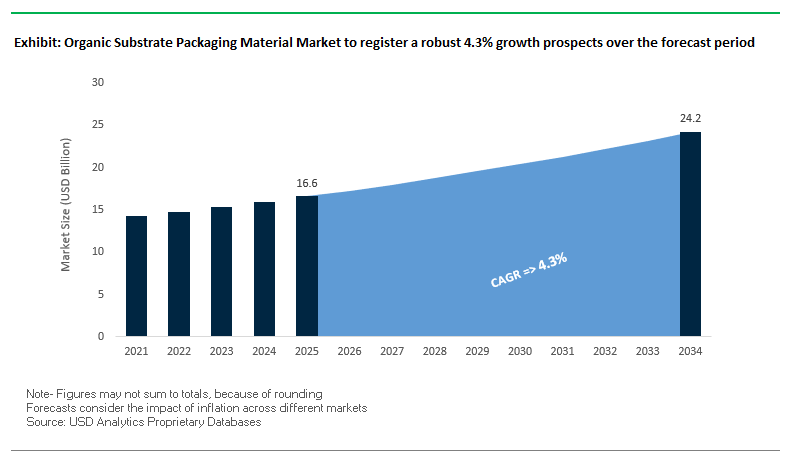

The global organic substrate packaging material market is projected to grow from $16.6 billion in 2025 to $24.2 billion by 2034, at a CAGR of 4.3%. This market is a critical segment within the electronics and semiconductor industries, providing foundational materials for printed circuit boards (PCBs) used across consumer electronics, automotive, AI, and HPC applications. Organic substrates are increasingly valued for their superior electrical performance, thermal management, and miniaturization support, enabling next-generation electronic devices and high-density multi-chip packaging.

Key Insights for Industry Professionals:

- Consumer electronics growth: Rising demand for smarter, thinner, and lighter devices drives the adoption of high-performance organic substrates.

- Sustainable material trends: Shift toward bio-based and halogen-free substrates to comply with ESG goals and government regulations.

- Advanced semiconductor packaging: Growing need for AI chips, HPC processors, and automotive radar systems fuels demand for substrates with excellent electrical and thermal performance.

- AI-driven manufacturing: Integration of machine learning for predictive quality control reduces material waste and enhances production efficiency.

- Global manufacturing expansion: Key regions, including South Korea, Austria, Canada, and the U.S., are witnessing increased substrate production capacity.

Recent Developments Highlight Advancements in High-Performance and Sustainable Substrates

The organic substrate packaging material industry has experienced dynamic developments, emphasizing innovation, sustainability, and government-backed growth. In August 2025, reports indicated that intelligent packaging solutions with embedded sensing elements are increasingly used to maintain substrate integrity during storage and transit. July 2025 saw a surge in demand in the U.S., supported by the CHIPS and Science Act, incentivizing domestic semiconductor production and increasing demand for organic substrates.

June 2024 marked the launch of TOPPAN Inc.’s Coreless Organic Interposer, the first to support standalone electrical inspection for next-generation semiconductors. In May 2024, Celestica introduced recyclable organic packaging substrates for mid-range computing systems, highlighting sustainability trends in Canada. April 2024 witnessed AT&S expanding production in Austria for high-end automotive radar and AI chip substrates, while LG Innotek unveiled substrates optimized for 5G and high-speed data processing in South Korea. Earlier, in September 2024, Amkor Technology introduced S-SWIFTTM technology, enabling high-density die-to-die interconnects, and Intel announced plans for glass substrates to support next-generation advanced packaging.

Trends and Opportunities Redefining the Organic Substrate Packaging Material Market

Massive Capital Expenditure Directed Towards Advanced Substrate Manufacturing Capacity

The organic substrate packaging material market is experiencing unprecedented investment as semiconductor and packaging leaders respond to the soaring demand for heterogeneous integration and high-performance computing (HPC). In January 2024, Intel launched Fab 9 in New Mexico, backed by a $3.5 billion investment, to enable advanced semiconductor packaging using its Foveros 3D stacking technology, which relies heavily on organic substrates for vertical chiplet integration. Expansions are not limited to the U.S.—in March 2025, TSMC announced a $100 billion expansion in the United States, raising its total U.S. investment to $165 billion, which includes two new advanced packaging facilities that will rely on high-end organic substrates for AI accelerators and HPC applications. In parallel, Samsung explored a strategic alliance with Intel in August 2025, reportedly focused on investing in Intel’s packaging lines and exploring next-generation glass substrates, reinforcing the competitive race to secure dominance in the organic substrate space. These capital expenditures underscore how organic substrates have become a strategic bottleneck in advanced packaging, essential for enabling the next wave of semiconductor innovation.

U.S. CHIPS Act Funding Prioritizing Domestic Advanced Packaging Ecosystem

Federal policy is reshaping the market landscape by prioritizing domestic capabilities for advanced packaging materials. The CHIPS and Science Act of 2022, with $11 billion earmarked for semiconductor R&D, directly targets packaging as a critical supply chain segment. In February 2024, the U.S. Department of Commerce released a Notice of Funding Opportunity (NOFO) under the National Advanced Packaging Manufacturing Program (NAPMP), designed to accelerate onshore capacity for organic and glass substrates. The program’s fact sheet explicitly states its mission to “establish and accelerate domestic capacity for advanced packaging substrates and substrate materials,” recognizing them as vital to U.S. semiconductor competitiveness. This policy push addresses the historical reliance on overseas manufacturing by incentivizing companies to build domestic substrate supply chains, strengthening resilience against geopolitical risks. The alignment of massive private sector investment with CHIPS Act funding is creating a dual engine of growth, ensuring the U.S. secures leadership in next-generation organic substrate packaging.

Co-Development of Substrates for Next-Generation AI and Networking ASICs

The rise of AI-driven accelerators and networking ASICs is creating a major opportunity for collaborative substrate innovation. With chip design shifting from monolithic architectures to chiplet-based systems-in-package (SiP), demand is surging for large-format organic substrates that can integrate multiple chiplets into a cohesive high-performance module. This requires substrates with ultra-fine line widths (as small as 9µm) and high layer counts, enabling complex interconnects essential for AI training clusters, cloud servers, and routers. Kyocera’s FC-BGA substrates, offering up to 10 build-up layers, already demonstrate the performance required for servers, GPUs, and networking devices. The co-development model between substrate manufacturers and chip designers ensures that substrates are not standardized components but rather application-specific enablers, tailored for unique power, signal integrity, and bandwidth requirements. For material suppliers, this trend represents a lucrative growth path, as advanced organic substrates become indispensable to the AI and HPC revolution.

Material Innovation for High-Density Power Delivery in Mobile & IoT Devices

The miniaturization of wearables, smartphones, and IoT sensors is fueling demand for substrates that can efficiently manage thermal performance and power density in increasingly compact designs. Traditional substrates served as passive interposers, but the next wave of innovation involves embedding passive and active components directly into the substrate, enabling system-in-package (SiP) configurations that integrate power management ICs, RF modules, and logic dies. Organic substrates offer unique advantages such as flexibility, cost efficiency, and compatibility with bendable devices, making them well-suited for medical wearables and consumer IoT devices. The CHIPS Act NOFO explicitly encourages proposals for embedded substrate designs, signaling government support for R&D in this area. New material innovations focused on thermal conductivity, signal integrity, and low-power operation will be critical to achieving reliable high-density power delivery. This positions advanced organic substrates not merely as carriers but as active system components, central to the future of mobile and IoT device packaging.

Competitive Landscape Highlights Leading Players Shaping Organic Substrate Innovation

The organic substrate packaging material industry is dominated by global players leveraging expertise in materials science, advanced manufacturing, and semiconductor design. These companies focus on delivering high-performance, thermally efficient, and increasingly sustainable organic substrates for electronics, AI, automotive, and HPC applications.

Amkor Technology Inc. Focuses on High-Density Dielectrics for HPC and AI Applications

Amkor Technology Inc. is a leading provider of advanced semiconductor packaging solutions, specializing in high-density organic substrates. In September 2024, Amkor unveiled S-SWIFTTM technology, enhancing die-to-die interconnect performance for data centers, AI, and HPC chips. Its offerings include BGA and CSP substrates, supporting smartphones, automotive electronics, and industrial systems. Amkor’s strategy emphasizes heterogeneous integration, miniaturization, and thermal management, with ongoing investments in new materials and advanced processes.

Kyocera Corporation Leverages Versatile Substrate Portfolio for Automotive and Industrial Applications

Kyocera Corporation is a diversified technology leader, offering both ceramic and organic substrates for complex electronic applications. In 2024, the company announced developments in its organic substrate business to address AI chip supply chain requirements. Kyocera provides BGA and multi-chip modules (MCMs) for automotive control units, industrial machinery, and high-frequency communications. Its strategy focuses on broad material portfolios and innovation to meet the evolving demands of automotive, telecom, and industrial sectors.

LG Innotek Co., Ltd. Drives High-Performance 5G and AI Substrate Solutions

LG Innotek Co., Ltd. specializes in high-density interconnects and high-performance organic substrates for advanced electronics. In April 2024, it unveiled substrates optimized for 5G and high-speed data processing, alongside a new AI-driven quality control line in its Gumi facility. The company offers FC-BGA components for consumer electronics, automotive, and data processing applications. LG Innotek’s strategy prioritizes expanding manufacturing capacity and R&D investments to meet growing 5G and AI market demands.

AT&S Expands Production for High-End Automotive and AI Applications in Europe

AT&S (Austria Technologie & Systemtechnik AG) is a leading manufacturer of high-end PCBs and IC substrates, focusing on automotive, industrial, and medical applications. In April 2024, AT&S expanded its Leoben, Austria facility to produce high-performance substrates for automotive radar and AI chips. Its offerings include flexible, rigid-flexible, and multi-layer boards, used in autonomous driving modules, medical devices, and industrial sensors. The company’s strategy emphasizes innovation, strategic expansion, and growth in high-performance segments.

Shinko Electric Industries Co., Ltd. Delivers Ultra-Fine Circuitry Substrates for Next-Generation Electronics

Shinko Electric Industries Co., Ltd. provides high-reliability organic substrates for consumer electronics, AI, and HPC applications. Recent developments include substrates with ultra-fine circuitry and improved heat resistance, addressing increasing power densities in next-generation processors. Shinko Electric offers flip-chip and LGA packages for smartphones, automotive, and high-performance computing systems. The company’s strategy focuses on technical leadership, innovation, and meeting complex semiconductor packaging requirements.

Organic Substrate Packaging Material Market Share Insights

Grid Array Packages Dominate Market Share by Technology in the Organic Substrate Packaging Industry

Grid Array (GA) packages command the largest share at 45% in 2025, underscoring their central role in high-pin-count and high-performance semiconductor applications. Ball Grid Array (BGA) and its derivatives provide dense interconnection, superior thermal management, and short electrical paths, making them irreplaceable for CPUs, GPUs, and ASICs in advanced computing, data centers, and AI hardware. Flat No-Leads Packages (FNPs), with a 25% share, are the fastest-growing segment due to their compact form factor, cost-effectiveness, and strong thermal/electrical performance, positioning them as the go-to choice for smartphones, wearables, and IoT devices. Quad Flat Packages (15%) retain relevance in automotive and industrial microcontroller units (MCUs), where proven reliability and ease of assembly sustain demand despite miniaturization pressures. Small Outline (SO) packages, at 10%, remain entrenched in mainstream memory and mid-density ICs, balancing cost efficiency with adequate performance. Dual In-Line Packages (5%) persist in legacy and mission-critical industrial and aerospace systems, where through-hole robustness is still essential. This segmentation highlights how GA packages dominate cutting-edge applications, while legacy formats maintain specialized niches in reliability-driven markets.

Consumer Electronics Command Market Share by Application in the Organic Substrate Packaging Industry

Consumer electronics hold the largest share at 40% of the organic substrate packaging industry in 2025, driven by insatiable demand for smartphones, laptops, tablets, and wearables that integrate multiple ICs in compact architectures. The push for miniaturization, higher data transfer speeds, and thermal management cements the dominance of BGAs and QFNs in this segment. Automotive applications follow with 25%, fueled by electric vehicle (EV) adoption, ADAS integration, and infotainment systems that dramatically increase semiconductor content per vehicle. This segment requires substrates offering ultra-high reliability under heat and vibration, making it the fastest-growing end-user. Telecommunications, at 15%, anchors demand from 5G infrastructure and high-frequency network hardware, where substrate performance in power and signal integrity is paramount. Industrial applications account for 12%, using a mix of legacy QFPs and newer packages for automation, control, and power systems, driven by steady global adoption of Industry 4.0 solutions. The remaining 8% includes aerospace, defense, and high-performance computing, which require specialized, mission-critical substrates capable of extreme reliability and thermal endurance. Collectively, this segmentation underscores how consumer electronics remain the volume leader, while automotive and telecom applications increasingly shape future substrate innovation.

United States: Regulatory Push and High-Performance Demands Shape Organic Substrate Packaging Materials

The United States is a crucial hub for the organic substrate packaging material market, driven by regulatory oversight and the growing performance requirements of the semiconductor industry. The U.S. Environmental Protection Agency (EPA) and Food and Drug Administration (FDA) regulate chemicals and materials used in packaging, while state-level Extended Producer Responsibility (EPR) laws are accelerating the shift toward recyclable and sustainable materials. This regulatory environment ensures that manufacturers not only meet environmental standards but also innovate to maintain performance and reliability.

Technological advancements remain a key focus, as companies seek to enhance existing organic substrates even while exploring alternatives like glass substrates for long-term adoption. Intel, for example, is evaluating glass for future high-performance computing, but immediate market demand continues to revolve around improved organic materials that can handle the thermal and compact design needs of 5G base stations, AI accelerators, and next-generation consumer electronics. With corporate investments driving innovations in thermally stable and cost-efficient materials, organic substrates are indispensable in smartphones, wearables, gaming devices, and automotive applications such as ECUs, infotainment systems, and ADAS in electric vehicles.

Germany: Circular Economy Policies Accelerate Adoption of Sustainable Organic Substrate Materials

Germany’s organic substrate packaging material market is governed by the European Union’s stringent sustainability regulations, particularly the Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging be recyclable by 2030. Coupled with strong national waste management policies, this framework creates an ecosystem where recyclable and sustainable substrate materials are prioritized. This alignment with the EU’s environmental agenda strengthens Germany’s role as a leader in eco-friendly packaging technologies.

Technological innovation is another hallmark of the German market, with local firms leading R&D efforts in advanced films, extrusion processes, and sustainable materials science. These innovations support industries such as electronics and automotive, where organic substrates are critical for reliable, high-performance components. Combined with Germany’s world-class recycling infrastructure and commitment to circular economy principles, the country offers a strong foundation for the expansion of next-generation substrate technologies that balance functionality with environmental responsibility.

China: Government Policies and Manufacturing Scale Propel Organic Substrate Packaging Industry

China has positioned itself as a global powerhouse in the organic substrate packaging material market, thanks to its combination of governmental support and large-scale manufacturing capacity. National policies emphasize the reduction, standardization, and recycling of packaging materials, aligning with broader environmental goals while strengthening the competitiveness of domestic manufacturers. This policy direction is particularly relevant for high-end manufacturing and semiconductor packaging, where organic substrates are indispensable.

Chinese manufacturers are heavily investing in automation and artificial intelligence to enhance production efficiency and ensure consistent quality in packaging materials. The government’s push for self-reliance in advanced manufacturing, paired with the rapid expansion of consumer electronics and telecommunications, fuels market growth. As a global leader in smartphone, laptop, and electronic device production, China represents one of the largest end-use markets for organic substrates. The steady flow of capital into the sector underscores its strategic importance in both domestic and international supply chains.

India: Policy Incentives and Circular Economy Drive Growth in Organic Substrate Materials

India’s organic substrate packaging material market is gaining momentum through strong government initiatives and rising domestic demand. The “Make in India” program and Production Linked Incentive (PLI) scheme have positioned the country as an attractive base for electronics and semiconductor manufacturing. New Extended Producer Responsibility (EPR) guidelines for plastics are also reshaping the packaging landscape, encouraging companies to adopt recyclable and circular solutions, including organic substrates.

Technological and corporate initiatives further reinforce this shift. The Indian government’s emphasis on a circular economy promotes the use of recyclable packaging, while leading businesses are voluntarily committing to reduce their plastic footprint and enhance recyclability. The market is particularly robust in consumer electronics and automotive applications, supported by the rise of supermarkets, organized retail, and e-commerce platforms. This combination of regulatory push and industry-led innovation is making India a fast-emerging destination for sustainable packaging technologies.

Japan: High-Tech Innovation and Sustainability Goals Strengthen Organic Substrate Packaging

Japan’s organic substrate packaging material market is defined by regulatory stringency and high-tech innovation. New rules for food containers and packaging, combined with the country’s broader sustainability agenda, are encouraging the adoption of safe and recyclable materials. With national targets to cut greenhouse gas emissions by 46% by 2030 and achieve net-zero by 2050, companies are under pressure to innovate packaging solutions that align with these long-term climate goals.

Technological leadership distinguishes Japan in this field, with companies like Toppan introducing a high-reliability coreless organic interposer in 2024 to support advanced semiconductor applications. This addresses the challenges of heterogeneous semiconductor integration, reinforcing the importance of organic substrates in high-performance computing. Furthermore, Japanese firms like Nissui are actively reducing CO2 and plastic consumption, ensuring sustainability is embedded in production. With demand surging in electronics and automotive industries, Japanese companies maintain their reputation for delivering premium, reliable, and high-quality substrate materials that enhance device performance while supporting environmental commitments.

Organic Substrate Packaging Material Market Report Scope

Organic Substrate Packaging Material Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.6 Billion

|

|

Market Size (2034)

|

$24.2 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Material Type (ABF, BT Resin, RCC), By Technology (SO Packages, GA Packages, FNPs, QFP, DIP), By Application (Consumer Electronics, Automotive, Industrial, Telecommunications, Others), By End-User (Semiconductor Manufacturers, Electronics Companies, Automotive Manufacturers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ajinomoto Co., Inc., Ibiden Co., Ltd., Unimicron Technology Corporation, Shennan Circuits Company Limited, ASE Technology Holding Co., Ltd., AT&S Austria Technologie & Systemtechnik AG, Shinko Electric Industries Co., Ltd., Kyocera Corporation, Nanya Technology Corporation, Fujitsu Interconnect Technologies Limited, Eastern Company Ltd., TTM Technologies, Inc., Zhaolong Interconnect Technology Co., Ltd., Daeduck Co., Ltd., Tripod Technology Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Substrate Packaging Material Market Segmentation

By Material Type

By Technology

- SO Packages

- GA Packages

- FNPs

- QFP

- DIP

By Application

- Consumer Electronics

- Automotive

- Industrial

- Telecommunications

- Others

By End-User

- Semiconductor Manufacturers

- Electronics Companies

- Automotive Manufacturers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Organic Substrate Packaging Material Market

- Ajinomoto Co., Inc.

- Ibiden Co., Ltd.

- Unimicron Technology Corporation

- Shennan Circuits Company Limited

- ASE Technology Holding Co., Ltd.

- AT&S Austria Technologie & Systemtechnik AG

- Shinko Electric Industries Co., Ltd.

- Kyocera Corporation

- Nanya Technology Corporation

- Fujitsu Interconnect Technologies Limited

- Eastern Company Ltd.

- TTM Technologies, Inc.

- Zhaolong Interconnect Technology Co., Ltd.

- Daeduck Co., Ltd.

- Tripod Technology Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver precise insights into the global organic substrate packaging material market, combining primary research, secondary data, and advanced analytics. Primary research encompasses in-depth interviews with semiconductor engineers, PCB designers, electronics manufacturers, and packaging material experts across automotive, consumer electronics, AI, HPC, and industrial applications. Secondary research integrates corporate filings, patent databases, trade publications, regulatory frameworks, government policies such as the U.S. CHIPS Act, EU sustainability directives, and Make in India initiatives, as well as market intelligence reports. Market sizing and forecasts are derived from historical trends, regional manufacturing expansions, adoption of bio-based and halogen-free substrates, and investments in high-density, multi-layer PCB solutions. USDAnalytics evaluates technological advancements, including AI-driven manufacturing, embedded passive and active substrate components, thermal management, and signal integrity improvements, while assessing the impact of emerging high-performance packaging technologies such as FNPs, GA packages, and coreless interposers. Competitive landscape analysis focuses on strategic expansions, R&D investments, sustainability initiatives, and innovative solutions by leading players including Amkor Technology, Kyocera, LG Innotek, AT&S, and Shinko Electric Industries, providing industry professionals with actionable insights for product development, capacity planning, and market positioning.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.