Oxidizing Bleaching Agents Market Anchored by Semiconductor-Grade Peroxides and Pulp Sector Investments

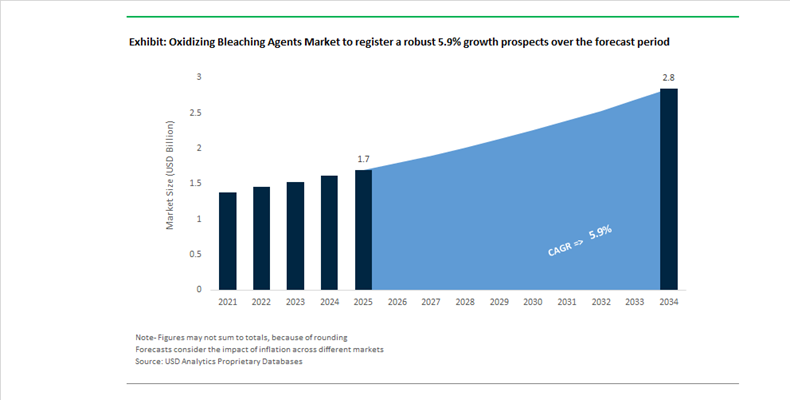

The Oxidizing Bleaching Agents Market is projected to grow from $1.7 billion in 2025 to $2.8 billion by 2034, expanding at a CAGR of 5.9%. Market growth is underpinned by rising demand for hydrogen peroxide (H₂O₂), sodium chlorate, and peracetic acid (PAA) across pulp and paper, semiconductors, wastewater treatment, food sterilization, and photovoltaic manufacturing. Structural demand is shifting toward high-purity, application-specific oxidants, particularly in electronics and renewable energy supply chains, while traditional pulp bleaching continues to provide volume stability.

In September 2025, Solvay inaugurated a major expansion at its Zhenjiang facility in China, doubling capacity for electronic-grade hydrogen peroxide. Ultra-pure H₂O₂ is critical in semiconductor fabrication for wafer cleaning and etching, where metallic impurities must be measured in parts per billion. This move aligns with China’s domestic semiconductor push and the broader global effort to localize chip supply chains. Earlier, in January 2024, Solvay partnered with Shandong Huatai Interox Chemical to expand photovoltaic-grade peroxide production to 48 kilotons annually by 2025, targeting the fast-scaling solar cell manufacturing industry in Northern China. These developments signal a structural rebalancing of peroxide demand from pulp-centric to electronics and renewable applications.

In January 2025, Evonik and Fuhua Tongda Chemicals formed the Evonik Fuhua New Materials joint venture in Leshan, China. The partnership upgrades industrial hydrogen peroxide into specialty grades for semiconductors, solar panels, and aseptic food packaging, with commercial supply commencing in 2026. Evonik’s Active Oxygens business line contributed significantly to its 2025 financial stability, as reflected in its February 2026 dividend policy announcement. The integration of specialty oxidation chemistry into high-growth sectors improves margin resilience compared to bulk pulp-grade supply.

The pulp and paper segment remains foundational. In February 2026, Kemira reported €2.75 billion in 2025 revenues, highlighting bleaching chemicals as a core contributor. Kemira maintains the #2 global position in bleaching solutions, serving European and North American fiber producers. Its 2024 investment in upgrading the Oulu hydrogen peroxide plant improved operational efficiency for Nordic pulp customers. Meanwhile, Nouryon expanded sodium chlorate capacity in Brazil by 20% in August 2025 and brought its Mato Grosso do Sul facility to full scale by early 2025. The integrated manufacturing model—co-locating bleaching chemical plants adjacent to pulp mills—reduces logistics cost and enhances supply reliability, particularly for large-scale projects like the new Arauco pulp mill.

Environmental compliance is accelerating the shift toward alternative oxidants. Throughout 2025, adoption of peracetic acid surged in municipal wastewater treatment across Europe and North America as regulators tightened limits on chlorine-based disinfection byproducts. Producers including Evonik and Solvay expanded PAA offerings positioned as low-residual, biodegradable oxidizing agents. Nouryon’s new Brazilian Innovation Center, operational by late 2026, is expected to focus on eco-friendly bleaching formulations for home and personal care, reinforcing diversification beyond industrial pulp applications.

Structural Trends and High-Growth Opportunities in the Oxidizing Bleaching Agents Market

Accelerated Decarbonization and Chlorine-Free Conversion in Pulp and Paper Bleaching

The global pulp and paper industry is entering a structurally enforced transition phase as regulatory pressure accelerates the shift from Elemental Chlorine Free (ECF) bleaching toward Totally Chlorine Free (TCF) sequences. This conversion is no longer discretionary. The revised EU Urban Wastewater Treatment Directive, effective from January 1, 2025, has materially tightened discharge thresholds for Adsorbable Organic Halides and reinforced the Polluter Pays principle. As a result, pulp mills across Europe are increasingly required to implement quaternary treatment processes for micropollutants, significantly raising the cost burden of chlorine-based bleaching chemistries.

Hydrogen peroxide-based bleaching sequences are emerging as the most economically rational alternative. By eliminating dioxin and AOX formation at the source, peroxide bleaching allows mills to avoid long-term environmental levies that could cumulatively reach €6.6 billion annually by 2040 across the European pulp sector. From a cost-structure perspective, hydrogen peroxide has also demonstrated greater pricing stability compared to chlorine derivatives. During Q2 2025, sodium chlorate prices experienced heightened volatility due to early summer production disruptions, while hydrogen peroxide prices recorded a relatively controlled increase of 2.5% to 13.8% across North America and Europe. This stability is underpinned by localized production strategies and structurally rising demand from mills migrating away from chlorine dioxide.

Process innovation is reinforcing this trend. Industrial-scale studies published in 2025 highlight the growing adoption of the Ozone–Peroxide (OZP) bleaching sequence, which reduces chlorinated organic discharges by nearly tenfold compared to conventional ECF routes. Crucially, the OZP approach preserves fiber strength and brightness while lowering the variable operating costs associated with ozone-only systems. As a result, oxidizing bleaching agents are transitioning from compliance enablers to core inputs in next-generation, low-emissions pulp production models.

Cold-Water Optimization Drives Reformulation Toward Stabilized Solid Peroxygen Bleaches

Energy efficiency mandates and evolving consumer behavior are reshaping the detergent and homecare sector, with cold-water washing emerging as a central pillar of decarbonization strategies. To meet performance expectations at temperatures as low as 20°C to 30°C, manufacturers are increasingly reformulating heavy-duty laundry powders and unit-dose pods around stabilized solid peroxygen bleaches, particularly sodium percarbonate.

Breakthroughs in percarbonate stabilization have materially expanded its addressable market. Research published in early 2025 demonstrated that optimal shelf-life performance in humid environments is achieved using a precise stabilizer composition of 2.2% magnesium sulfate and 1.2% sodium silicate. This formulation enables the incorporation of oxygen bleach into highly concentrated all-in-one pods without premature decomposition, supporting consistent oxidative performance in cold-wash cycles.

Demand-side dynamics are reinforcing adoption. By late 2024, surveys across the United States and Western Europe indicated that 78% of industry stakeholders prioritize environmentally friendly cleaning agents. This preference has translated into a 60% adoption rate of sodium percarbonate in premium laundry formulations across Europe, driven by its biodegradable profile and chlorine-free chemistry. Policy alignment is further accelerating uptake. In 2025, government-led initiatives in the EU and South Korea actively promoted low-temperature laundry practices to reduce household energy consumption. In response, formulators are deploying coated sodium percarbonate grades that resist moisture ingress during storage while dissolving rapidly in cold water, ensuring cleaning efficacy without reliance on heated wash cycles.

Stable Oxidizing Biocides Gain Traction Under IMO Ballast Water Enforcement

The maritime sector represents a structurally attractive growth avenue for oxidizing bleaching agents as regulatory enforcement tightens around ballast water treatment. The International Maritime Organization, in coordination with the Paris and Tokyo Memoranda of Understanding, has launched a Concentrated Inspection Campaign from September to November 2025 to strictly enforce compliance with the Ballast Water Management Convention. This enforcement wave is driving demand for oxidizing biocides that combine high microbial efficacy with environmental neutrality.

Hydrogen peroxide has emerged as a leading candidate for ballast water disinfection. Research published in August 2025 confirms that peroxide-based systems effectively neutralize invasive marine species without generating persistent toxic residues. Species-sensitivity distribution studies indicate that hydrogen peroxide concentrations below 10 mg/L are sufficient to inactivate marine invertebrates, positioning it as a clean biocide solution for global shipping fleets. During the 2025 inspection campaign, port state authorities are verifying real-time performance of Ballast Water Management Systems, creating a premium merchant market for marine-grade, stabilized peroxide formulations capable of maintaining efficacy over voyages exceeding three months.

Beyond maritime applications, sodium percarbonate is gaining traction in municipal wastewater treatment. With global wastewater volumes surpassing 380 billion cubic meters annually, utilities are increasingly seeking solid oxygen-releasing agents that degrade complex organic pollutants without forming chlorinated byproducts. This dual exposure to shipping and wastewater infrastructure positions oxidizing bleaching agents at the intersection of regulatory compliance and scalable environmental remediation.

Ultra-Pure Peroxygen Agents Become Critical Enablers for Advanced Semiconductor Manufacturing

The semiconductor industry’s transition toward 3nm and 2nm logic nodes and advanced 3D NAND architectures is creating a high-margin demand segment for ultra-pure oxidizing agents. As of early 2025, approximately 46% of global fabrication facilities have migrated to sub-7nm processes, driving a 37% increase in consumption of high-purity hydrogen peroxide for wafer cleaning and photoresist removal. At these technology nodes, oxidizer purity requirements exceed 99.9999%, with metallic impurity tolerances falling below parts-per-trillion thresholds.

Supply chain localization is emerging as a strategic differentiator. In mid-2025, Mitsubishi Gas Chemical scheduled expanded output at its Texas facility, following a similar capacity ramp-up in Oregon in late 2024. These investments are designed to support closed-loop, localized delivery of ultra-pure hydrogen peroxide to North American fab clusters, minimizing contamination risks associated with long-distance transport.

The commercial upside is material. Industrial manufacturing data indicates that adoption of ultra-high-purity oxidizing agents has improved wafer yields by 15% to 22% in advanced logic production. As contamination tolerance tightens below 0.1 ppb, leading semiconductor manufacturers such as TSMC and Intel are increasingly securing long-term, high-margin supply contracts for electronic-grade oxidizing agents. This shift is repositioning the oxidizing bleaching agents market away from volume-driven commodity supply toward precision-critical, technology-aligned growth.

Oxidizing Bleaching Agents Market Share and Segmentation Insights

Hydrogen Peroxide Leads Oxidizing Bleaching Agents Market with Environmentally Compatible Oxidation Chemistry

Hydrogen peroxide accounted for 48.60% of the Oxidizing Bleaching Agents Market by chemical type in 2025, making it the most widely used oxidizing bleach across industrial and consumer applications. Its dominance is supported by strong oxidation efficiency and an environmentally compatible decomposition profile that breaks down into water and oxygen, which aligns with sustainability priorities in chemical manufacturing. Hydrogen peroxide is extensively used in pulp and paper bleaching, textile processing, electronics cleaning, water treatment, and home and personal care formulations. In 2025, the green chemistry positioning of hydrogen peroxide is strengthening its adoption, particularly in pulp and paper bleaching processes where elemental chlorine free and totally chlorine free technologies rely on peroxide based oxidation to meet strict environmental regulations and eco-friendly product standards.

Pulp and Paper Industry Drives Oxidizing Bleaching Agent Consumption in Global Paper Production

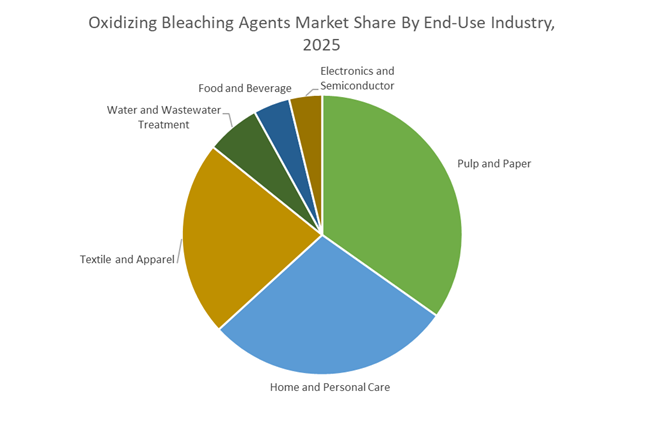

The pulp and paper industry represented 34.80% of the Oxidizing Bleaching Agents Market by end-use industry in 2025, reflecting the large-scale demand for bleaching chemicals in pulp delignification and brightness improvement processes. Hydrogen peroxide and sodium chlorate are widely used in mechanical pulp bleaching and chemical pulp processing to achieve the whiteness levels required for printing paper, packaging grades, and tissue products. Global paper production continues to sustain strong demand for high-performance oxidizing bleaching agents. In 2025, the industry shift toward elemental chlorine free bleaching technologies is reinforcing demand for hydrogen peroxide and chlorine dioxide derived from sodium chlorate, enabling pulp mills to meet environmental regulations while improving process sustainability in modern paper manufacturing systems.

Oxidizing Bleaching Agents Market Competitive Landscape

The Oxidizing Bleaching Agents Market is shifting toward oxygen-based chemistries, including hydrogen peroxide and peracetic acid, driven by green chemistry mandates and wastewater treatment demand. Key players are investing in low-carbon production, digital dosing systems, and semiconductor-grade oxidants to enhance efficiency, sustainability, and application-specific performance.

Solvay expands hydrogen peroxide and PAP portfolio with digital dosing optimization

Solvay S.A. maintains leadership in oxidizing bleaching agents through its vertically integrated hydrogen peroxide value chain and INTEROX® portfolio, widely used in pulp bleaching, wastewater treatment, and aseptic packaging. The company is expanding its EURECO™ peracid range, targeting low-temperature bleaching applications that reduce energy consumption in home and personal care formulations. Its “circular-ready” hydrogen peroxide solutions decompose into water and oxygen, eliminating harmful disinfection byproducts and aligning with sustainability regulations. The introduction of digital dosing tools in 2026 enables real-time optimization of chemical usage, reducing oxidative waste by up to 15% in industrial operations. Solvay’s strong global supply chain ensures consistent delivery across Europe and North America. This combination of process optimization, sustainability, and application breadth reinforces its market leadership.

Evonik targets semiconductor-grade oxidants and green chemistry-driven growth

Evonik Industries AG is strengthening its position in high-performance oxidizing agents through specialty oxidants and semiconductor-grade hydrogen peroxide. Following the PeroxyChem acquisition, the company has built a strong portfolio of ultra-high-purity oxidants used in silicon wafer cleaning and etching processes. Its Advanced Technologies segment generated €5.97 billion in 2025, reflecting strong demand for high-margin specialty chemicals. Evonik’s €1.87 billion EBITDA performance supports continued investment in green chemistry and advanced materials. Expansion of production infrastructure in Asia enhances its ability to serve regional electronics and polymer markets. The shift toward performance-linked capital allocation from 2026 further supports R&D in sustainable oxidizing systems. This focus on purity, innovation, and electronics applications strengthens Evonik’s competitive positioning.

BASF accelerates transition to oxygenated bleaching agents through Verbund optimization

BASF SE is repositioning its oxidizing bleaching agents portfolio by shifting from traditional hydrosulfite chemistries toward oxygen-based solutions and low-carbon intermediates. The divestment of hydrosulfite-related assets to Silox allows BASF to focus on high-growth oxygenated bleaching platforms. Its Verbund integration supports large-scale production efficiency, with expanded capacity at the Zhanjiang site enhancing supply to Asia-Pacific textile and paper industries. BASF is introducing reduced product carbon footprint variants to de-fossilize its bleaching value chain by 2030. The deployment of AI-driven reactor systems accelerates optimization of oxidation reactions, improving yield and reducing time-to-market. This integration of digitalization, sustainability, and scale strengthens BASF’s leadership in next-generation bleaching agents.

Nouryon strengthens pulp bleaching leadership with low-carbon hydrogen peroxide innovation

Nouryon is reinforcing its global leadership in pulp and paper bleaching through a combination of chlorine dioxide and sustainable hydrogen peroxide technologies. The company’s 20% expansion in sodium chlorate capacity supports large-scale pulp production in South America, particularly for the Arauco mill. Nouryon’s low-carbon hydrogen peroxide, produced using renewable energy in Scandinavia, reduces Scope 3 emissions for customers. Its product innovations, showcased at SEPAWA 2025, integrate oxidative performance with bio-based surfactants for home care and industrial cleaning applications. New innovation centers in Shanghai and Brazil enhance localized product development for emerging markets. This focus on sustainability, capacity expansion, and regional customization strengthens Nouryon’s competitive advantage.

Mitsubishi Gas Chemical advances high-purity oxidants with circular methanol integration

Mitsubishi Gas Chemical (MGC) is differentiating itself through proprietary technologies and high-purity oxidizing agents tailored for electronics and pharmaceutical applications. Its collaboration on methanol-to-hydrogen systems supports the development of green feedstocks for hydrogen peroxide production. Expansion of electronic materials capacity in 2025 positions MGC to meet growing semiconductor demand for ultra-pure oxidants. The company’s Carbopath™ circular methanol platform enables a low-carbon approach to chemical manufacturing. Its OXYCAPT™ technology demonstrates innovation at the intersection of oxidation chemistry and pharmaceutical packaging. With over 90% of products based on proprietary technology, MGC maintains strong control over process efficiency and product quality. This positions it as a key player in high-purity oxidant markets.

Arkema expands peroxygen chemicals and battery recycling applications

Arkema S.A. is leveraging its Specialty Materials segment to capture demand for high-purity oxidizing agents in energy transition and healthcare applications. With €1.25 billion EBITDA in 2025 and a €600 million capital expenditure plan for 2026, the company is prioritizing high-return projects in peroxygen chemicals. Its hydrogen peroxide plays a critical role in lithium-ion battery recycling, enabling efficient metal recovery processes. Expansion of Kynar® PVDF capacity in China supports infrastructure for handling aggressive oxidizing chemistries in industrial systems. Arkema’s cost optimization program, targeting €250 million in savings, is being reinvested into bio-based and low-carbon initiatives. This strategic alignment with energy transition trends strengthens its position in advanced oxidizing solutions.

China Oxidizing Bleaching Agents Market: Photovoltaic-Grade Expansion, ECF Transition, and Integrated Feedstock Security

China continues to dominate the global oxidizing bleaching agents market, accounting for over 60% of global production capacity for key agents such as sodium percarbonate as of late 2025. The country’s strategic pivot toward “Green Transformation” in large-scale chemical industrial parks is accelerating the adoption of peroxide-based bleaching technologies and advanced oxidation systems. A key growth driver is the joint venture expansion between Solvay and Huatai, targeting 48,000 tons/year of photovoltaic-grade hydrogen peroxide capacity by late 2025. This is directly aligned with surging demand from the solar cell cleaning and semiconductor-grade wafer processing markets, reinforcing China’s leadership in high-purity oxidizing agents.

Regulatory enforcement on industrial water discharge and chlorate residue elimination has triggered a 7.1% increase in demand for peroxide-based Elemental Chlorine Free (ECF) bleaching sequences across pulp and textile hubs. Concurrently, Evonik’s upcoming 30 kiloton specialty capacity facility in Leshan (2026) underscores the country’s move toward high-value, precision-controlled bleaching chemistries. Technological convergence is also evident, with ozone-based advanced oxidation systems (AOPs) gaining traction in major municipalities like Shanghai and Shenzhen. To mitigate raw material price volatility (35% fluctuation in anthracene feedstocks during 2025), Chinese producers are increasingly adopting vertical integration strategies with coal-tar and coking operations, ensuring supply chain resilience and cost stability in the oxidizing agents ecosystem.

Germany Oxidizing Bleaching Agents Market: Green Hydrogen Integration and Advanced Oxidation Processes (AOP) Leadership

Germany stands at the forefront of the European oxidizing bleaching agents market, driven by its commitment to low-carbon chemical production, green hydrogen integration, and advanced oxidation processes (AOPs). BASF SE’s commissioning of a 54 MW PEM electrolyzer at Ludwigshafen (2025) marks a significant milestone in green hydrogen-powered oxidizing agent production, enabling low-emission hydrogen peroxide synthesis for industrial applications. This infrastructure is instrumental in scaling next-generation AOP reactors, particularly for water treatment, specialty chemicals, and industrial cleaning applications.

Product innovation remains robust, with LANXESS introducing Oxone™ monopersulfate compound, a high-efficiency oxidizing agent for cold-wash detergents, aligning with EU energy efficiency regulations and low-temperature washing trends. Meanwhile, Solvay’s electronic-grade hydrogen peroxide facility in Bernburg is catering to the rapidly expanding European semiconductor ecosystem (Silicon Saxony), highlighting Germany’s critical role in ultra-high purity oxidizing chemicals. Regulatory developments such as the European Medicines Agency (EMA) mandate on Vaporized Hydrogen Peroxide (VHP) disinfection protocols are further driving demand in healthcare sterilization markets. Additionally, the rise of on-site decentralized oxidant generation systems (up 3.9%) reflects industry efforts to reduce logistics costs, improve safety, and enhance process efficiency, reinforcing Germany’s leadership in sustainable oxidizing bleaching technologies.

United States Oxidizing Bleaching Agents Market: Semiconductor Boom, FDA VHP Protocols, and Water Treatment Modernization

The United States oxidizing bleaching agents market is being reshaped by domestic semiconductor expansion, evolving FDA sterilization standards, and stringent EPA water treatment regulations. The expansion of high-purity hydrogen peroxide production by Mitsubishi Gas Chemical (2025) is directly linked to the growth of semiconductor fabrication hubs in Arizona and Texas, supported by CHIPS Act initiatives. This is significantly boosting demand for electronic-grade oxidizing agents used in wafer cleaning and microelectronics manufacturing.

Healthcare applications are also a major growth vector, with updated FDA guidelines on Vaporized Hydrogen Peroxide (VHP) disinfection increasing peroxide consumption to 1.5–2.5 kg per day per 500-bed hospital. This reflects a structural shift toward continuous sterilization protocols and high-purity oxidants in clinical environments. In water treatment, updated EPA regulations are accelerating the deployment of portable sodium hypochlorite generation systems, reducing reliance on hazardous chlorine gas storage and enhancing urban water safety infrastructure. Despite mild pricing pressure in Q4 2025, U.S. producers maintained disciplined operating rates, ensuring market stability for FMCG and institutional cleaning sectors. Additionally, rising consumer demand for clean-label food processing is driving the adoption of non-migratory oxidizing systems in bakery and dairy applications, strengthening the market for food-safe bleaching agents.

India Oxidizing Bleaching Agents Market: PLI-Led Pharma Growth, Water Disinfection Programs, and Textile Compliance Modernization

India is the fastest-growing oxidizing bleaching agents market in South Asia, supported by government-led industrial expansion, healthcare infrastructure growth, and tightening environmental compliance frameworks. The ₹41,920 crore investment under the PLI scheme (2025) has significantly accelerated the pharmaceutical and bulk drug manufacturing sectors, driving demand for high-purity hydrogen peroxide and sterilization-grade oxidizing agents. This is particularly relevant for cleanroom sterilization and aseptic processing environments, where VHP-based systems are becoming standard.

Water sanitation initiatives led by the Department of Drinking Water & Sanitation are expanding the use of tablet-based and liquid chlorine dosing technologies, especially in rural programs such as Single Village Schemes (SVS). In parallel, India’s textile export hubs like Tirupur are adopting advanced chemical dosing and micropollutant control systems to meet Zero Liquid Discharge (ZLD) compliance standards, enhancing competitiveness in global markets. Capacity expansion by players such as Gujarat Alkalies and Chemicals (GACL) at Dahej is strengthening domestic supply of hydrogen peroxide for pulp, paper, and textile bleaching applications. Looking ahead, the addition of 1.2 million hospital beds across India and Asia (2026–2030) is expected to embed VHP sterilization infrastructure at scale, locking in long-term demand for medical-grade oxidizing bleaching agents.

Netherlands & Nordic Oxidizing Bleaching Agents Market: Carbon-Neutral Hydrogen Peroxide and Circular Chemical Business Models

The Netherlands and Nordic region are emerging as global pioneers in carbon-neutral oxidizing bleaching agents, driven by decarbonization mandates, green hydrogen adoption, and circular chemical production models. Evonik’s partnership with VoltH2 to deploy a 50 MW electrolyzer (2025) aims to produce hydrogen peroxide with carbon intensity below 0.5 kg CO₂-e/kg, targeting premium buyers willing to pay a 15%–20% green premium. This positions the region at the forefront of low-carbon oxidizing agent innovation and sustainable chemical manufacturing.

Nouryon’s launch of Eka HP Puroxide, offering a 40% lower carbon footprint, is gaining traction in the Nordic pulp and paper industry, where mills are transitioning to Elemental Chlorine Free (ECF) bleaching sequences and achieving brightness levels above 92 ISO while meeting strict EU environmental standards. The region is also pioneering build-own-operate (BOO) on-site oxidant generation models, enabling industrial users to reduce supply chain risks and ensure consistent chemical availability. Additionally, regulatory leadership in bio-based crystallization and boron nitride-assisted oxidation processes is driving up to a 46% increase in process efficiency, reinforcing the Netherlands and Nordic countries as innovation hubs for next-generation oxidizing bleaching technologies.

Oxidizing Bleaching Agents Market Report Scope

Oxidizing Bleaching Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Chemical Type (Hydrogen Peroxide, Sodium Chlorate, Sodium Percarbonate, Sodium Perborate, Organic Peroxides, Other Oxidizing Agents), By Functionality (Bleaching, Oxidizing, Disinfecting and Sanitizing, Catalysis), By End-Use Industry (Pulp and Paper, Textile and Apparel, Electronics and Semiconductor, Home and Personal Care, Food and Beverage, Water and Wastewater Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Solvay, Evonik Industries, Nouryon, Arkema, Kemira, Mitsubishi Gas Chemical, Ecolab, Hansol Chemical, Sinopec, OCI, PeroxyChem, Aditya Birla Chemicals, Gujarat Alkalies and Chemicals, Hodogaya Chemical, Taekwang Industrial

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oxidizing Bleaching Agents Market Segmentation

By Chemical Type

- Hydrogen Peroxide

- Sodium Chlorate

- Sodium Percarbonate

- Sodium Perborate

- Organic Peroxides

- Other Oxidizing Agents

By Functionality

- Bleaching

- Oxidizing

- Disinfecting and Sanitizing

- Catalysis

By End-Use Industry

- Pulp and Paper

- Textile and Apparel

- Electronics and Semiconductor

- Home and Personal Care

- Food and Beverage

- Water and Wastewater Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oxidizing Bleaching Agents Industry

- Solvay

- Evonik Industries

- Nouryon

- Arkema

- Kemira

- Mitsubishi Gas Chemical

- Ecolab

- Hansol Chemical

- Sinopec

- OCI

- PeroxyChem

- Aditya Birla Chemicals

- Gujarat Alkalies and Chemicals

- Hodogaya Chemical

- Taekwang Industrial

*- List not Exhaustive