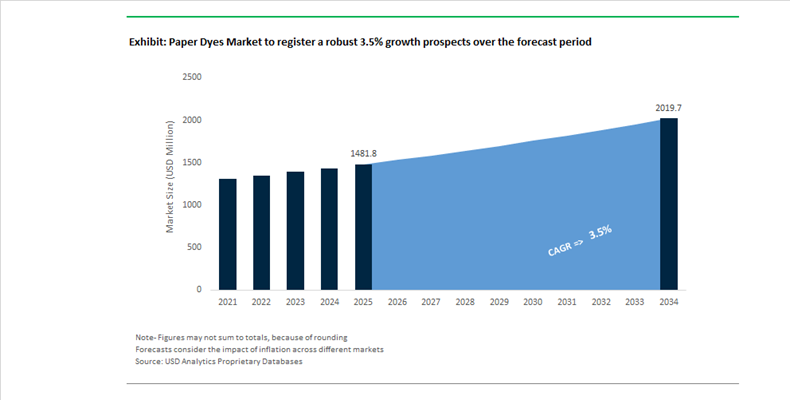

Paper Dyes Market Valued at $1,481.8 Million in 2025 with 3.5% CAGR Amid Sustainable Packaging Shift and Global Capacity Realignment

The Paper Dyes Market is valued at $1,481.8 Million in 2025 and is projected to reach $2,019.5 Million by 2034, expanding at a CAGR of 3.5%. Market momentum is being driven by structural growth in paper-based packaging, regulatory pressure to replace plastics, and accelerating investment in low-carbon, food-contact-compliant color chemistries. Paper dyes—comprising direct dyes, basic dyes, pigment dispersions, and functional colorants—are critical in decorative printing, tissue, cartonboard, specialty packaging, and barrier-coated paper substrates. As global FMCG brands transition toward recyclable and compostable packaging formats, dye manufacturers are being forced to meet stricter migration, heavy metal, and VOC standards, particularly in Europe and North America.

In March 2025, Sudarshan Chemical Industries Limited completed its ₹1,180 crore acquisition of Heubach Group, creating a global colorant leader with 19 manufacturing sites across 11 countries. This consolidation integrates Heubach’s high-end paper and packaging pigment technologies into Sudarshan’s portfolio, significantly strengthening its European and American footprint. In April 2025, DyStar consolidated manufacturing operations in the Americas, integrating production into optimized sites in North Carolina and Wyoming to improve supply chain efficiency for paper and specialty dyes.

Capacity expansion in Asia is reshaping regional supply. In March 2025, Kemira announced a multi-million euro expansion at its Wellgrow site in Thailand, targeting 100,000 tons of additional annual capacity for strength agents and dyes, with operations scheduled by August 2026. On February 13, 2026, BASF added a new high-performance dispersion production line at its Mangalore, India facility, introducing Basonal® PLUS low-Product Carbon Footprint (PCF) binders specifically designed for paper coatings. This expansion aligns with BASF’s broader shift following its October 2025 divestment of its decorative paints business to Sherwin-Williams, enabling deeper focus on industrial performance chemicals and packaging applications.

Sustainability certification and bio-based innovation are emerging as competitive differentiators. In May 2024, Archroma achieved Cradle to Cradle Material Health GOLD (4.0) certification for key dye products under its PLANET CONSCIOUS+ strategy, reinforcing compliance for food-contact and circular packaging applications. In August 2024, Vipul Organics formally entered the paper segment with pigment dispersions and direct dyes tailored for paperboard and packaging converters. Throughout 2025, regional producers across Asia-Pacific advanced plant-derived pigment dispersions designed to meet stringent migration and compostability standards for paper-based coffee cups and takeout containers. Meanwhile, Solenis’ integration of Ipackchem through 2024–2025 is accelerating the development of barrier-enhanced paper dyes and coatings capable of replacing plastic laminates in moisture- and grease-resistant packaging. The competitive environment is increasingly defined by low-carbon production, supply chain consolidation, bio-based dispersion technologies, and compliance with evolving global food-contact regulations.

Paper Dyes Market: Trends and Opportunities Redefining Compliance and Value Creation

Mandatory Transition to Non-Toxic, Heavy-Metal-Free Paper Dyes

The paper dyes market is being reshaped by tightening global regulations targeting substances of very high concern in consumer-facing applications. The EU Packaging and Packaging Waste Regulation, effective February 11, 2025, mandates the minimization of hazardous substances in packaging, including new limits on heavy metals and a phased ban on PFAS in food-contact materials. These requirements are forcing the complete reformulation of grease-resistant and colored paper products.

Additional pressure is coming from the toy and childcare sectors. The EU Toy Safety Regulation 2025/2509 introduces stricter chemical controls and requires Digital Product Passports to track dye composition in children’s books and colored cardboards. Regulatory alignment is global. In October 2025, India’s food safety authority proposed new restrictions on harmful additives in food-contact materials, aligning domestic standards with international migration limits for metals such as lead and antimony. Collectively, these measures are driving demand toward non-toxic, heavy-metal-free paper dyes that offer regulatory certainty across multiple end-use sectors.

Investment Shift Toward High-Performance Dyes for Digital Paper Printing

A second structural trend is the migration of paper coloration from bulk pulp processes to digital printing platforms. The global digital packaging printing market exceeded USD 33 billion in 2024, driven by short runs, customization, and on-demand production. This shift requires liquid dyes capable of operating reliably within high-speed inkjet systems.

To capture this growth, leading players are investing aggressively in digital dye capabilities. In March 2025, Sudarshan Chemical Industries completed the acquisition of the pigments and dyes business of Heubach Group, significantly expanding its portfolio of high-performance colorants for digital applications. These dyes must meet demanding performance metrics, including ultra-low viscosity and stable jetting at firing frequencies of up to 50 kHz. At the same time, collaborations between paper producers and automation specialists are increasing demand for dyes that deliver strong rub-fastness on unbleached kraft papers, supporting the visual and durability requirements of e-commerce packaging.

Bio-Based and Natural Dyes for Eco-Labeled Paper Products

The circular economy is opening a high-margin niche for bio-based and natural paper dyes derived from renewable waste streams. Recent studies indicate that natural dyes sourced from agricultural residues such as indigo and henna are now achieving lightfastness comparable to conventional acid dyes, enabling their use in specialty packaging applications.

Sustainability benchmarks underscore the opportunity. In 2025, CHT Group reported that 84% of its revenues were generated from sustainable solutions, reflecting a broader industry shift toward compliant, renewable inputs. Luxury and premium retail brands are increasingly adopting naturally dyed, recycled paper bags at cost parity with virgin alternatives. This trend is supported by initiatives such as Green Lab, which expanded into the U.S. market in 2025 to supply FSC-certified, naturally dyed paper packaging to high-end retailers.

Functional and Smart Dyes for Security and Sensing Applications

Beyond aesthetics, paper dyes are increasingly being engineered for functional performance. Anti-counterfeiting has become a critical cost center for converters, driving adoption of UV-fluorescent, thermochromic, and invisible security dyes embedded directly into paper fibers for pharmaceutical and electronics packaging.

Smart packaging represents a parallel opportunity. Intelligent dyes that change color in response to pH or gas composition are being explored as real-time indicators of food freshness, helping retailers reduce spoilage-related losses. In parallel, digital authentication platforms are creating demand for dye-based watermarks that enable instant verification via smartphone cameras without altering package design. These applications are repositioning paper dyes from commodity colorants to value-added functional components within secure and intelligent packaging systems.

Paper Dyes Market Share and Segmentation Insights

Direct Dyes Lead Paper Coloring Applications Through High Affinity for Cellulosic Fibers

Direct dyes accounted for 48.60% of the Paper Dyes Market by dye type in 2025, establishing them as the dominant dye class used in paper manufacturing. These dyes exhibit strong affinity for cellulose fibers, enabling efficient coloration without the need for mordants or complex fixation processes. Direct dyes deliver bright shades, strong substantivity, and consistent color performance in packaging paper, tissue products, and writing paper grades. Their cost effectiveness and ease of application make them suitable for high volume paper production environments. In 2025, manufacturers are introducing high purity direct dye formulations for food contact paper, reducing heavy metal content and impurities to comply with global regulations governing colored paperboard used in food packaging applications.

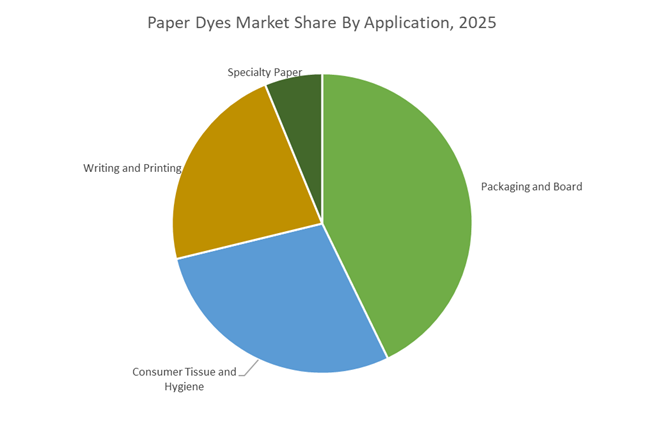

Packaging and Board Segment Drives Paper Dye Demand in Sustainable Paper-Based Packaging

Packaging and board represented 42.80% of the Paper Dyes Market by application in 2025, reflecting strong demand for colored paper materials used in corrugated containers, folding cartons, and branded paper packaging. Coloration supports brand identity, product differentiation, and visual appeal across retail packaging formats. Growth in e commerce logistics and the shift toward sustainable fiber based packaging are increasing consumption of paper dyes across packaging production lines. In 2025, dye suppliers are addressing the recycled fiber coloration challenge, developing advanced dye systems capable of delivering consistent shades on recycled pulp where fiber variability, yellowing, and grayness can affect final color performance in paperboard manufacturing.

Paper Dyes Market Competitive Landscape

The Paper Dyes Market is transitioning toward bio-based dyes, PFAS-free chemistries, and recyclable fiber-compatible colorants. Leading players are integrating circular economy solutions, water-efficient processing, and high-performance non-toxic dyes to support the global paperization trend and sustainable packaging demand.

Archroma leads bio-based paper dyes with circular chemistry and zero-liquid discharge systems

Archroma AG is positioning itself as a sustainability leader in the paper dyes market through its system-centric approach and circular dye technologies. The company achieved Cradle to Cradle Certified® Material Health Gold for key product lines such as DIRESUL® and AVITERA®, reinforcing its focus on non-toxic, compliant colorants. Its DIRSOL® RD chemistry enables high-intensity, laser-compatible shades for specialty paper applications, addressing digital printing requirements. Archroma’s EarthColors® technology converts agricultural waste into high-performance dyes, supporting bio-based packaging solutions with reduced water footprint. Its Mahachai plant’s Zero Liquid Discharge system recovers up to 95% of wastewater, enhancing operational sustainability. This integration of green chemistry, innovation, and water efficiency strengthens Archroma’s market leadership.

Kemira integrates bio-based coatings and dyes to enable plastic-to-paper packaging transition

Kemira Oyj is strengthening its competitive position by combining functional additives and paper dyes to support recyclable packaging solutions. Its strategic partnership with Bluepha enables commercialization of PHA-based bio-barrier coatings integrated with dye systems for the Asia-Pacific market. The company maintained a strong 19.1% EBITDA margin in 2025 while launching a €100 million share buyback program to support strategic growth. The acquisition of Water Engineering expands its capability to deliver integrated water treatment and dyeing solutions for paper mills. Kemira’s biomass-balanced wet strength additives enable production of durable, high-color paper products derived from renewable feedstocks. This integrated chemistry-plus-service model positions Kemira as a key enabler of sustainable paper packaging.

BASF scales sustainable dye intermediates with Verbund integration and mass-balanced solutions

BASF SE is leveraging its Verbund production model to supply high-performance paper dyes and intermediates with improved cost efficiency and sustainability. The startup of its Zhanjiang site enhances supply capacity for the rapidly growing Asian paper packaging market. BASF’s innovation in advanced pigments, including interference and metallic effects, is expanding into premium specialty paper and printing applications. The company is transitioning toward BMBcert™ mass-balanced dye intermediates, reducing carbon footprint across its product portfolio. With 74% of revenue linked to sustainability-driven solutions, BASF is aligning strongly with circular economy requirements. Its projected EBITDA of €6.2–€7.0 billion in 2026 supports continued investment in low-carbon dye technologies.

Solenis builds integrated paper dye and barrier coating ecosystem through acquisitions

Solenis is expanding its footprint in the paper dyes market by integrating process chemistry, water treatment, and barrier coatings into a unified offering. The acquisition of NCH Corporation significantly enhances its ability to deliver end-to-end solutions for paper mills. Its TopScreen™ barrier coatings, including bio-wax formulations, enable replacement of plastic laminates while maintaining recyclability. Collaboration with HEIDELBERG has enabled flexographic technologies that combine dye application and barrier coating in a single step, improving efficiency and reducing material usage. With 78 global manufacturing sites, Solenis ensures localized supply and technical support. This integrated approach strengthens its position as a comprehensive solutions provider.

Sun Chemical advances high-purity pigments for food-safe and premium paper applications

Sun Chemical, part of the DIC Group, is a global leader in high-performance pigments and dyes for paper and packaging applications. Its Lumina HD mica-based pigments deliver superior chroma and visual effects for luxury and premium paper packaging. Investments in perylene pigment production have stabilized supply for high-saturation color applications, particularly reds and oranges. Its Heliogen phthalocyanine pigments meet stringent EU Article 3 compliance standards, making them suitable for food-contact and sensitive printing applications. Expansion of the HYDRAN GP portfolio supports low-VOC, amine-free coatings that reduce environmental impact. This focus on high-purity, regulatory compliance, and premium aesthetics positions Sun Chemical strongly in specialty paper dyes.

China – Dispersant-Led Upgrading and Sustainability-Driven Reform

China’s paper dyes industry is undergoing a structural upgrade anchored in high-performance chemistry and regulatory tightening. In November 2025, BASF commissioned a high-performance dispersant production line in Nanjing based on Controlled Free Radical Polymerization technology. This infrastructure directly improves dye stabilization, color yield consistency, and runnability in high-speed paper machines, particularly for packaging grades where visual uniformity is commercially critical. BASF also consolidated its Asian PolyTHF and intermediate operations into the Caojing site during 2025, addressing global overcapacity while creating a vertically integrated supply hub for specialty paper additives and dye precursors. These moves signal a shift away from fragmented regional sourcing toward centralized, efficiency-driven chemical ecosystems.

Policy pressure is accelerating this transformation. The Ministry of Industry and Information Technology released a 2025–2027 “Green and Low-Carbon Standardization” roadmap that prioritizes tighter VOC limits for industrial dyes, aligning domestic production with international ESG benchmarks. In response, major paper producers such as Nine Dragons and Lee & Man Paper rapidly increased adoption of water-based, low-VOC dyes in late 2025 to meet rising demand for plastic-free e-commerce packaging. At the mill level, AI-driven color-matching systems deployed across Zhejiang and Jiangsu have reduced dye waste by roughly 15%, reinforcing cost efficiency amid export headwinds. Trade dynamics remain a constraint, with India’s June 2025 anti-dumping duties on Chinese decor paper forcing pricing recalibration and indirectly impacting dye demand tied to export-oriented grades.

United States – PFAS-Free Transition and Liquid Dye Dominance

The U.S. paper dyes market is being reshaped by capital investment, regulatory clarity, and operational modernization. In May 2025, Solenis announced an additional USD 76 million investment in its Suffolk, Virginia facility, bringing total committed capital to USD 269 million. The expansion supports polymer and dye systems essential for global paper and cardboard manufacturing, strengthening domestic supply reliability. Regulatory change is equally influential. By January 2026, the U.S. paper dye industry completed its transition to fluorine-free technologies, with Solenis commercializing Contour SM solutions that deliver oil and grease resistance for molded pulp without intentionally added PFAS.

Operational preferences are also shifting. The 2025–2026 period marks a decisive move toward liquid direct dyes over powders, driven by automated dosing compatibility, lower airborne particulates, and improved worker safety. BioPreferred certifications expanded sharply in 2025 under the USDA program, particularly for dyes and barrier coatings derived from agricultural side-streams. On the demand side, sustainable e-commerce packaging is a key driver. The late-2024 joint initiative between Mondi and CMC Packaging Automation continues to influence dye demand for high-purity brown and black shades used in premium kraft shipping materials.

India – Consolidation, Import Protection, and Cluster Development

India’s paper dyes industry is consolidating rapidly while benefiting from policy-backed industrial clustering. In March 2025, Sudarshan Chemical Industries completed its USD 138 million acquisition of the Heubach Group’s pigments and dyes business, materially enhancing India’s export capability for high-performance paper colorants into Europe and the Americas. Domestic demand momentum is evident. In 2024, Vipul Organics secured a significant blue and violet dye contract from Tamil Nadu Newsprint and Papers Limited, highlighting recovery in the printing and writing segment alongside packaging growth.

Policy support is reinforcing this trajectory. Under the 2025 NITI Aayog “Powering India’s GVC” framework, the government is developing eight high-potential chemical clusters with viability gap funding to foster green chemistry innovation. Trade protection also plays a role. Anti-dumping duties imposed in June 2025 on decor paper and selected chemical catalysts aim to shield domestic dye producers from underpriced imports, improving pricing stability and encouraging capacity utilization within India.

Germany – Circular Economy and Bio-Derived Dye Leadership

Germany continues to set the benchmark for sustainability-led innovation in paper dyes. At FACHPACK 2025 in Nuremberg, German and European players showcased PHA-based coatings and dyes that are home-compostable and marine-biodegradable, directly supporting compliance with the EU Single-Use Plastics directive. BASF expanded its EcoBalanced portfolio in 2025, applying a biomass balance approach to colorants used in melamine resin foams and specialty paper, reducing product carbon footprints while maintaining performance parity.

Innovation recognition further underlines Germany’s role. In October 2025, Archroma received the ITMF Sustainability and Innovation Award for its EarthColors range, which derives dyes from agricultural waste such as nutshells and plant residues. These developments position Germany as a preferred sourcing hub for brands seeking traceable, low-impact paper dyes aligned with circular economy objectives.

Finland – Water Chemistry Expertise and Portfolio Refocusing

Finland’s paper dyes landscape is closely linked to advanced water chemistry and strategic portfolio management. Kemira Oyj, headquartered in Helsinki, announced in late 2025 its ambition to double water-related revenue by 2030, targeting over EUR 500 million from renewable solutions. As a top global supplier to the pulp and paper sector, Kemira’s strategy emphasizes dyes and additives that improve water efficiency and reduce effluent loads in highly water-intensive mills.

To sharpen focus, Kemira divested its main colorants business to ChromaScape in 2024, while retaining its high-growth APAC-related colorants activities. This selective divestment reflects a strategic shift toward regions and applications where sustainability-driven demand growth is strongest, reinforcing Finland’s role as a technology and process innovation hub rather than a volume colorant producer.

Comparative Summary – Paper Dyes Industry by Country

Paper Dyes Market County Level Snapshot

|

Country

|

Strategic Focus

|

Policy or Market Driver

|

Structural Impact

|

|

China

|

Dispersant performance and low-VOC dyes

|

MIIT green standards, export duties

|

Centralized, efficiency-driven supply chains

|

|

United States

|

PFAS-free, liquid dye systems

|

EPA regulation, BioPreferred program

|

Safer mills and automated dosing adoption

|

|

India

|

Consolidation and domestic protection

|

Anti-dumping duties, chemical clusters

|

Export-ready capacity and pricing stability

|

|

Germany

|

Circular and bio-derived dyes

|

EU sustainability directives

|

Premium, low-carbon dye innovation

|

|

Finland

|

Water-efficient dye solutions

|

Corporate portfolio optimization

|

Technology-led specialization

|

Paper Dyes Market Report Scope

Paper Dyes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1481.8 Million

|

|

Market Size (2034)

|

$2019.5 Million

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Dye Type (Direct Dyes, Basic Dyes, Acid Dyes, Reactive Dyes), By Form (Liquid Dyes, Powder Dyes), By Application (Packaging and Board, Consumer Tissue and Hygiene, Writing and Printing, Specialty Paper), By Chemical Origin (Synthetic Dyes, Bio-Based and Natural Dyes)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, BASF, Solenis, Kemira, Indulor Chemie, Sudarshan Chemical Industries, Atul, DyStar Group, Vipul Organics, ChromaScape, Standard Colors, Synthesia, Axyntis, Chromatech, Organic Dyes and Pigments

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Dyes Market Segmentation

By Dye Type

- Direct Dyes

- Basic Dyes

- Acid Dyes

- Reactive Dyes

By Form

By Application

- Packaging and Board

- Consumer Tissue and Hygiene

- Writing and Printing

- Specialty Paper

By Chemical Origin

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Paper Dyes Industry

- Archroma

- BASF

- Solenis

- Kemira

- Indulor Chemie

- Sudarshan Chemical Industries

- Atul

- DyStar Group

- Vipul Organics

- ChromaScape

- Standard Colors

- Synthesia

- Axyntis

- Chromatech

- Organic Dyes and Pigments

*- List not Exhaustive