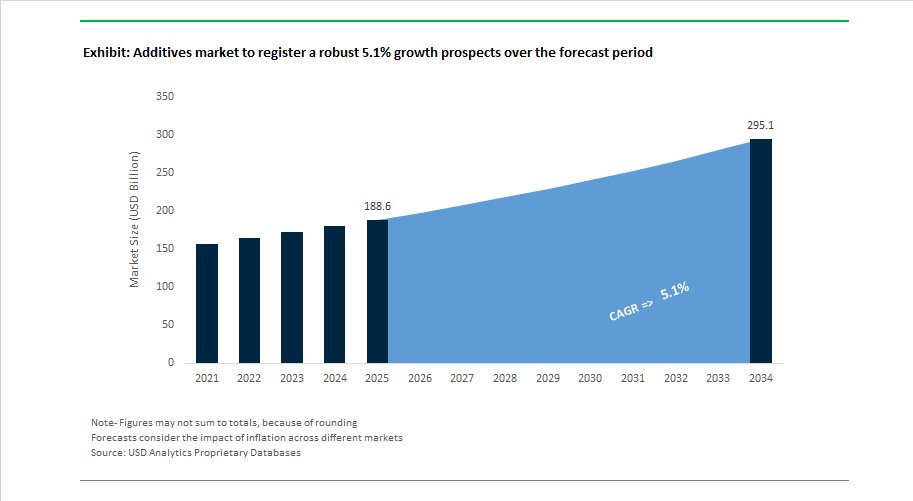

Market Overview: Additives Market Valuation to Reach $295.1 Billion by 2034 Supported by Circular Chemistry, PFAS Substitution, and Specialty Performance Materials

The global additives market is projected to expand from $188.6 billion in 2025 to $295.1 billion by 2034, reflecting a 5.1% CAGR driven by structural shifts in polymer additives, flame retardants, plasticizers, stabilizers, pigments, processing aids, and specialty performance modifiers. Market momentum is closely linked to decarbonization initiatives, circular polymer processing, EV material safety requirements, medical-grade compliance standards, and elimination of hazardous chemistries such as PFAS and phthalates. Additives are becoming performance enablers rather than secondary formulation inputs, influencing mechanical strength, thermal stability, flame resistance, optical clarity, recyclability, and regulatory compliance across automotive plastics, electronics housings, medical polymers, packaging films, construction materials, and advanced composites. Competitive intensity is rising as producers reposition portfolios toward bio-based additives, halogen-free flame retardants, chemical recycling catalysts, and high-purity specialty modifiers that command premium margins.

Circularity-led innovation gained momentum in November 2024 when ExxonMobil invested $200 million to expand Exxtend advanced recycling operations in Texas, including catalyst additive systems enabling efficient polymer waste conversion. Consolidation accelerated in March 2025 as Nippon Paint Holdings acquired AOC Resins, strengthening control over specialty composite additives, followed by Sudarshan Chemical Industries acquiring Heubach Group, creating a major global supplier of pigments and functional additives. Ownership shifts continued in May 2025 when The Goodyear Tire & Rubber Company divested its Polymer Chemicals business to Gemspring Capital, transferring antioxidant and rubber additive assets. Portfolio expansion in engineered materials followed in September 2025 with Arclin acquiring Polymer Solutions Group, integrating additive dispersions into industrial resins. Structural realignment intensified in November 2025 when ADNOC completed its $14.7 billion acquisition of Covestro, committing major capital toward circular, mass-balance certified polymer additives.

Technology-driven portfolio upgrades accelerated through January 2026. The Dow Chemical Company expanded bio-based plasticizer capacity, replacing phthalates in sensitive packaging and toy applications. BASF strengthened EV materials safety by acquiring a halogen-free flame retardant specialist, aligning with non-toxic battery enclosure requirements. Polytives GmbH entered the Indian market with migration-stable PFAS-free processing aids that integrate into existing production lines without equipment modification. Medical-grade material innovation advanced in February 2026 as SABIC launched SILTEM HU resins positioned as fluoropolymer alternatives. The same month, Lummus Technology and Sumitomo Chemical commercialized PMMA chemical recycling, restoring acrylic waste to ultra-high-purity MMA monomer. Process efficiency additives also advanced in February 2026 when Milliken & Company introduced next-generation clarifiers and nucleating agents that lower polypropylene processing temperatures and reduce energy demand, reinforcing the role of advanced additives in sustainable polymer manufacturing.

Strategic Market Trends and Emerging Commercial Opportunities Transforming the Additives Market

Market Trend: Reformulation Acceleration Driven by Global Phase-Out of PFAS and Hazardous Plasticizers

A defining transformation in the additives industry is the urgent reformulation of legacy chemistries, triggered by environmental scrutiny and cross-regional regulation. The August 2025 EU REACH proposal, covering over 10,000 PFAS substances, and the February 2025 Packaging and Packaging Waste Regulation (PPWR) limiting PFAS presence in food-contact packaging have forced additive suppliers to develop PFAS-free alternatives at scale. Compliance deadlines beginning mid-2026 have accelerated R&D cycles across packaging, consumer goods, and medical-grade plastics.

Parallel regulatory pressure is building in North America. The U.S. EPA’s June 2025 draft determination of “unreasonable risk” for DEHP and DBP is reshaping demand in healthcare and children’s product markets, redirecting procurement toward bio-based and non-phthalate plasticizers. To compete in this new operating landscape, chemical leaders are deploying AI-accelerated additive discovery. BASF’s December 2025 announcement revealed 20x faster candidate-screening capabilities, powered by automated chemistry platforms aligned with its €2 billion R&D engine. The result is a new speed standard, where additive companies must innovate rapidly or risk material delisting by OEMs and converters.

Market Trend: Localization and Onshoring of Additive Production to Eliminate Strategic Supply Chain Risk

Supply chain fragility exposed between 2022 and 2023 has permanently altered additive sourcing strategy. Global manufacturers are shifting to localized, self-reliant production ecosystems, where additives critical to EV battery binders, medical polymers, and advanced materials are manufactured closer to end-use hubs.

In March 2025, BASF expanded U.S. output through Monaca (Pennsylvania) and Chattanooga (Tennessee) investments dedicated to Licity anode-binder additives, supporting a domestic EV battery supply chain without dependence on Asian imports. Furthermore, $85 million in capital expenditure in Upstate South Carolina is positioning the region as an advanced materials hub aligned with U.S. industrial decarbonization mandates.

Europe is mirroring this structure. Under the EU Chemicals Industry Action Plan (July 2025), the Critical Chemicals Alliance is mapping and prioritizing essential additive production sites to avoid bottlenecks similar to those seen in the semiconductor sector. Localization is becoming a competitive advantage, improving delivery timelines, raw-material security, carbon footprint compliance, and customer qualification rates.

Market Opportunity: Additive Systems Enabling Silicon-Dominant Battery Anode Commercialization

As EV competitiveness becomes defined by range, charge-time, and cycle durability, silicon-dominant anodes have emerged as the most disruptive material shift in battery design. Their adoption demands new binder additive systems engineered to manage silicon’s extreme expansion, which can reach several hundred% during charging.

Zeon Corporation’s November 2025 binder release exemplifies the new performance bar. These additives stabilize electrodes during expansion, eliminating cracking and conductivity loss that traditionally limited silicon adoption. Strategic supply-side moves reinforce this direction: OCI is building a 1,000-ton SiH₄ feedstock plant under a five-year supply agreement with Nexeon, signaling that additives will scale in tandem with silicon supply infrastructure.

Performance benchmarks released by Sionic Energy and Group14 Technologies demonstrate the commercial power of premium additive packages, enabling 400 Wh/kg energy densities and over 1,200 cycles, far exceeding graphite-based systems. This is the most lucrative specialty additive segment, expected to drive pricing premiums and long-term OEM contracts through 2030.

Market Opportunity: Advanced Additives for Soil-Biodegradable Agricultural Films and Regenerative Agriculture

A second high-growth opportunity is emerging from biodegradable mulch film regulation, which is transforming global agricultural plastic consumption. Soil-biodegradable films require precision-engineered additive packages that control UV stability, decomposition rate, and tensile strength across 12-to-18-month cultivation cycles.

European and North American mandates now require certified soil-degradable films to eliminate microplastic accumulation and reduce land restoration costs. These films commonly contain 75 to 95% PBAT or PLA, with the balance composed of specialty additives such as biodegradable fillers and UV stabilizers. Innovation is rapidly scaling, highlighted by nanocellulose-reinforced PBAT composites enabling sub-15-micron film thickness and improved tensile performance.

Novamont’s Mater-Bi platform delivered 38% mass loss after six months in soil-burial trials in 2025, demonstrating the commercial viability of additive-controlled decomposition. Incentive programs across Europe are accelerating adoption, where subsidies are helping farmers avoid manual plastic-waste removal costs, creating a sizeable revenue runway in the $3.5 billion agricultural additive sub-sector.

Additives Market Share and Segmentation Insights

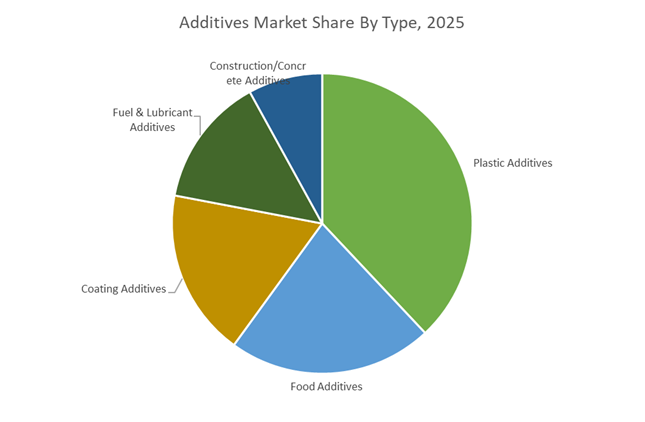

Market Share by Type: Plastic Additives Dominate as Food Systems and Energy Transition Reshape Demand

Plastic additives account for approximately 38% of the global additives market in 2025, driven by the relentless replacement of glass, metal, and wood with polymers across packaging, automotive, construction, and electronics. Stabilizers, plasticizers, and flame retardants remain core volume drivers as polymer penetration deepens worldwide. Food additives rank second, supported by clean-label trends that paradoxically increase demand for natural preservation systems, while emerging economies rapidly scale processed food production despite softer synthetic antioxidant usage in developed regions. Fuel & lubricant additives face structural pressure from electric vehicle adoption reducing passenger car engine oil demand, although industrial lubricants and aviation fuels remain resilient growth pockets. Construction additives hold the smallest value share but represent high-volume consumption, with concrete superplasticizers and air-entraining agents essential for modern infrastructure, even as cement’s commodity nature keeps additive pricing comparatively low.

Market Share by Application: Packaging Leads While Healthcare Delivers the Fastest Growth

Packaging represents roughly 31% of total additives consumption in 2025, making it the largest application segment as plastic additives enable polymer processing, coating additives enhance printability and barrier performance, and food additives support preservation. The global push toward a plastic circular economy is accelerating demand for additive solutions that improve recyclability and recycled-content quality. Automotive & transportation show bifurcated demand, with ICE platforms relying on fuel additive packages while EV platforms increase usage of plastic additives for lightweighting and coating additives for battery thermal management. Healthcare & medical is the fastest-growing application at +7.1% CAGR, driven by high-purity plastic additives for sterilization stability and expanding food additive use in pharmaceutical excipients. Electrical & electronics growth is fueled by miniaturization, requiring flame-retardant plastics and thermally conductive coatings for 5G and high-performance computing. Agriculture remains the smallest segment, with steady demand constrained by margin sensitivity.

Competitive Landscape: Sustainability-Led Innovation Reshaping the Global Additives Market

The global Additives Market is increasingly defined by regulatory compliance, circular economy alignment, and high-performance material engineering across plastics, coatings, electronics, and E-mobility. Leading suppliers are moving beyond commodity stabilizers toward biomass-balanced additives, PFAS-free processing aids, halogen-free flame retardants, and advanced antioxidant systems. Competitive differentiation now centers on upstream integration, localized Asian manufacturing, and specialty portfolios for EV batteries, agricultural films, high-voltage cables, and premium packaging. Strategic investments in India, China, the Middle East, and Europe highlight how global producers are positioning for long-term growth in sustainable polymer additives and next-generation materials.

BASF SE dominates plastic additives through Verbund integration and VALERAS® sustainability platforms

BASF SE remains the largest player in plastic additives, leveraging its Verbund production model and VALERAS® sustainability framework to deliver antioxidants, light stabilizers, and thermal stabilizers at global scale. Flagship offerings include Irganox®, Tinuvin®, and Irgastab®, serving packaging, agriculture, solar, and cable insulation applications. During 2025–2026, BASF scaled Tinuvin® NOR® 211 AR for plasticulture films, delivering resistance to aggressive agrochemicals such as sulfur and chlorine. The launch of BMBcert™ biomass-balanced additives further replaced fossil feedstocks with renewable inputs without performance trade-offs. BASF also intensified partnerships in India and China to support durable solar pontoons and high-voltage cable systems.

Clariant AG accelerates PFAS-free additives and halogen-free flame retardant adoption

Clariant AG leads regulatory-driven innovation, actively transitioning markets away from PFAS and halogenated substances. In June 2025, the company introduced AddWorks® PPA, a PFAS-free polymer processing aid platform for polyolefin film extrusion, anticipating global regulatory bans. Strategically, Clariant is shifting toward antimony-free polyester catalysts, launching titanium-based AddWorks™ solutions in 2026 to mitigate supply-chain volatility. Its Exolit® OP halogen-free flame retardants and Licocare® rice-bran waxes support electronics and E-mobility applications. Expanded operations at Daya Bay, China in late 2025 strengthened local EV battery additive supply and reinforced Clariant’s Asia-Pacific footprint.

Evonik Industries AG expands specialty additives for coatings, adhesives, and automated recycling

Evonik Industries AG focuses on high-margin specialty additives with strong exposure to automotive and advanced coatings. In early 2026, Evonik streamlined its North American distribution network to enhance technical support for its Coating Additives division. The company is ramping global hydroxyl-terminated polybutadiene production, adding capacity in Germany and Shanghai to meet demand for high-performance adhesives and sealants. Core offerings include TEGO® dispersants and VESTAGON® crosslinkers for radiation-curable and waterborne systems. Capital deployment is increasingly directed toward the Next Markets Program, targeting bio-based materials and automated polymer recycling as emerging growth pillars.

Songwon Industrial Co., Ltd. strengthens polymer stabilization with upstream integration and One-Pack Systems

Songwon Industrial ranks second globally in antioxidants and is a leader in polymer stabilization, backed by strong upstream independence. In October 2025, Songwon announced a greenfield One-Pack Systems facility in Saudi Arabia to serve Middle Eastern polyolefin markets. Recent developments include XP2121 and SONGNOX® PQ additives designed to enhance processing consistency of mechanically recycled LDPE, LLDPE, and polypropylene. Vertical integration in DAP production ensures raw material security amid volatile markets. Songwon’s tailored OPS blends combine multiple stabilizers into single, dust-free formulations, improving manufacturing efficiency for global converters and compounders.

Adeka Corporation advances clarifiers and recycled-polyolefin stabilizers for electronics and packaging

Adeka Corporation is a technical leader in Asia, specializing in high-performance stabilizers and clarifiers for automotive, electronics, and premium packaging. Its ADK STAB HALS and UV absorber series, alongside ADK CYCLOAID grades for recycled polyolefins, address durability and circularity requirements. In late 2025, Adeka launched Transparex, an advanced clarifier improving polypropylene transparency and stiffness. February 2026 marked the establishment of a global renewable plastics supply chain in partnership with Sony, targeting electronic components. Adeka is also a major supplier of heavy-metal-free Ca-Zn stabilizers for wire and cable applications.

Lanxess AG reinforces fire protection additives amid EV and infrastructure expansion

Lanxess AG concentrates on protection-oriented additives, leading in flame retardants and inorganic pigments. Its Bayferrox® pigments and Emerald Innovation® flame retardants support thermal insulation, construction plastics, and automotive systems. Lanxess holds strong positions in phosphorus-based, halogen-free flame retardants critical for EV battery housings and charging infrastructure. With China projected to represent half of the global chemical market by 2030, Lanxess has prioritized Asian CAPEX while upgrading assets in India and Germany to deliver lower-carbon additive variants. This strategy positions Lanxess to benefit from accelerating EV adoption and infrastructure-driven polymer demand.

China Additives Market: Regulatory Tightening, Standards Harmonization, and Integrated Cost Leadership

China’s additives market is undergoing one of the most comprehensive regulatory restructurings globally. In May 2025, the State Council Food Safety Commission introduced the Comprehensive Governance Plan for the Abuse of Food Additives, establishing a “positive list” system for imported additives alongside a circuit breaker mechanism that immediately halts imports from non-compliant suppliers. This has significantly tightened oversight across food additives, functional ingredients, and processing aids, forcing multinational suppliers to revalidate formulations and documentation.

Regulatory pressure intensified further in September 2025 when the National Health Commission (NHC) and State Administration for Market Regulation (SAMR) released revised national standards for high-volume additives such as xanthan gum, L-malic acid, and ammonium carbonate, with mandatory enforcement from March 2, 2026. On the materials side, packaging-focused subsidies are accelerating demand for intrinsic viscosity enhancers and color-corrective masterbatches to support high-quality recycled PET (r-PET). Simultaneously, government restrictions on antimony exports have disrupted traditional polyester catalyst supply chains, driving global shifts toward alternative catalyst chemistries. Compliance risks have also increased following the inclusion of 144 entities from XUAR and other provinces under the UFLPA Entity List, reshaping global sourcing strategies. To offset regulatory and cost pressures, Chinese producers are expanding integrated “Verbund-style” petrochemical complexes in Zhejiang and Guangdong, lowering unit costs for specialty antioxidants and stabilizers through feedstock integration.

United States Additives Market: Clean-Label Momentum, Circular Plastics, and Advanced Transparency

The United States additives market is increasingly defined by clean-label approvals, sustainability mandates, and advanced compliance transparency. In May 2025, the U.S. Food and Drug Administration approved Gardenia Blue, a natural dye derived from gardenia fruit, for use in sports drinks, teas, and confectionery—signaling a decisive regulatory shift toward naturally sourced food additives. This approval has accelerated reformulation pipelines across beverages and functional foods.

On the polymer side, California’s mandate requiring 65% post-consumer recycled (PCR) content in rigid plastic containers by 2025 is driving robust demand for compatibilizers, decontamination additives, and odor scavengers. Healthcare remains a high-margin growth segment; in October 2025, LyondellBasell expanded its Purell healthcare portfolio with new medical-grade polyolefin additives for diagnostic labware. Infrastructure investment—particularly federal funding for EV charging networks—is boosting demand for halogen-free flame retardants meeting UL 94 V-0 ratings. Meanwhile, PFAS phase-outs effective from 2026 are accelerating the transition toward silicone-based and fluoropolymer-free processing aids. U.S. producers are also differentiating through transparency, increasingly deploying ISO 14067-certified carbon footprint calculators to provide full life-cycle analysis per ton of additive sold.

India Additives Market: Regulatory Modernization, Domestic Capacity Expansion, and Consumption Upshift

India’s additives industry is transitioning from import dependence toward domestic scale and regulatory maturity. The Food Safety and Standards Authority of India (FSSAI) notified the First Amendment Regulations, 2025, effective February 1, 2026, introducing new microbial sources for enzyme production and revising purity limits for bleaching agents—broadening the innovation space for food additives while tightening compliance.

From an industrial standpoint, energy and petrochemical investments are strengthening the additive supply base. In February 2025, Bharat Petroleum Corporation Limited announced a ₹5,000 crore polypropylene unit in Kochi, expected to serve as a critical domestic feedstock source for polymer additives and masterbatches. Electrical safety upgrades are also influencing demand; Finolex’s FinoGreen halogen-free flame retardant cables highlight the shift toward safer additive systems in dense urban environments. Manufacturing incentives under the Production Linked Incentive (PLI) scheme are accelerating local production of antioxidants and UV stabilizers. Concurrently, rapid growth in organized food processing—particularly in Tier 2 cities—is driving higher consumption of emulsifiers, acidulants, and shelf-life extenders as disposable incomes rise.

Germany Additives Market: Regulatory Benchmarking, Bio-Derived Additives, and Precision Automation

Germany continues to set the regulatory and technological benchmark for the European additives market. At the K 2025 trade fair in Düsseldorf, German leaders showcased titanium-based catalyst solutions and low-halogen flame retardants such as Halolite 527, engineered to comply with EN 50642 standards and upcoming EU chemical safety revisions. These innovations reflect Germany’s proactive stance ahead of regulatory enforcement cycles.

Sustainability is embedded at the production level. Industrial sites are transitioning to 100% renewable electricity for masterbatch extrusion to mitigate cost exposure under the EU Carbon Border Adjustment Mechanism (CBAM). R&D is increasingly focused on cellulose-derived flame retardants and phosphorus-grafted bio-polymers to replace brominated additives. On the food side, Germany leads Europe in clean-label adoption, with strong consumer rejection of synthetic colorants and flavor enhancers. Digitally, German processors are integrating AI-enabled micro-dosing systems into extrusion lines, reducing additive consumption by up to 10% while maintaining consistent performance in high-speed operations.

Japan Additives Market: Advanced Materials, Aging-Demographic Nutrition, and Circular PET Technologies

Japan’s additives industry is characterized by advanced material science and application-specific specialization. In 2025, a collaboration involving Sumitomo Corporation enabled the launch of Japan’s first graphene-enhanced polyethylene additive masterbatch, targeting high-strength industrial films with superior mechanical performance.

Japan also remains a global hub for enzyme-based preservatives and specialized amino acids, driven by nutritional requirements of its aging population. Semiconductor re-shoring initiatives are boosting investment in antistatic and conductive masterbatches for clean-room construction materials. In parallel, circular economy initiatives are accelerating development of intrinsic viscosity enhancers that allow recycled PET to be processed on high-speed bottle-to-bottle lines, narrowing the performance gap between recycled and virgin polymers.

Saudi Arabia Additives Market: Additive Manufacturing Scale-Up and Export-Oriented Integration

Saudi Arabia is rapidly emerging as a strategic additives manufacturing hub for the Middle East and beyond. In October 2025, SONGWON announced a major investment to establish a One Pack Systems (OPS) production facility in the Kingdom, strengthening regional supply of pre-blended additive solutions for polymer processors.

Aligned with Vision 2030, the Kingdom is leveraging low-cost ethane feedstocks to localize production of UV stabilizers and antioxidants, improving cost competitiveness versus imports. Export infrastructure development is positioning Saudi Arabia as a key supplier of additive packages to African and European plastic conversion markets, reinforcing its role as a bridge between energy integration and downstream specialty chemicals manufacturing.

Country-Level Strategic Positioning in the Additives Industry

Additives market County Level Snapshot

|

Country

|

Core Strategic Drivers

|

Impact on Global Additives Market

|

|

China

|

Food safety governance, standards overhaul, petrochemical integration

|

Supply chain tightening and cost-efficient specialty output

|

|

United States

|

Clean-label approvals, PCR mandates, PFAS bans

|

High-value reformulation and transparency-led differentiation

|

|

India

|

Regulatory reform, domestic PP expansion, PLI incentives

|

Import substitution and demand-driven scale-up

|

|

Germany

|

EU compliance leadership, bio-based R&D, automation

|

Premium regulatory-ready additive innovation

|

|

Japan

|

Advanced materials, aging nutrition, circular PET

|

Specialty, high-performance additive leadership

|

|

Saudi Arabia

|

OPS investment, ethane integration, export focus

|

Emerging global hub for pre-blended additive systems

|

Additives Market Report Scope

Additives market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$188.6 Billion

|

|

Market Size (2034)

|

$295.1 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type (Plastic Additives, Food Additives, Coating Additives, Fuel & Lubricant Additives, Construction/Concrete Additives), By Functionality (Performance Additives, Processing Additives, Specialty/Functional Additives), By Application (Packaging, Automotive & Transportation, Building & Construction, Healthcare & Medical, Electrical & Electronics, Agriculture), By Physical Form (Powder, Liquid/Slurry, Pellet/Granule, Masterbatch)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Evonik Industries AG, Arkema S.A., Songwon Industrial Co., Ltd., Clariant AG, LyondellBasell Industries N.V., Avient Corporation, Nouryon, Mitsubishi Chemical Group, Adeka Corporation, Shandong Rike Chemical Co., Ltd., Plastiblends India Limited, Fine Organics, Sabic

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Additives Market Segmentation

By Type

- Plastic Additives

- Food Additives

- Coating Additives

- Fuel & Lubricant Additives

- Construction/Concrete Additives

By Functionality

- Performance Additives

- Processing Additives

- Specialty/Functional Additives

By Application

- Packaging

- Automotive & Transportation

- Building & Construction

- Healthcare & Medical

- Electrical & Electronics

- Agriculture

By Physical Form

- Powder

- Liquid/Slurry

- Pellet/Granule

- Masterbatch

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Additives market

- BASF SE

- Dow Inc.

- Evonik Industries AG

- Arkema S.A.

- Songwon Industrial Co. Ltd.

- Clariant AG

- LyondellBasell Industries N.V.

- Avient Corporation

- Nouryon

- Mitsubishi Chemical Group

- Adeka Corporation

- Shandong Rike Chemical Co. Ltd.

- Plastiblends India Limited

- Fine Organics

- SABIC

*- List not Exhaustive