Market Overview: Pet Care Packaging Market Poised to Reach $23.8 Billion by 2034, Driven by Sustainability, Convenience, and Premiumization

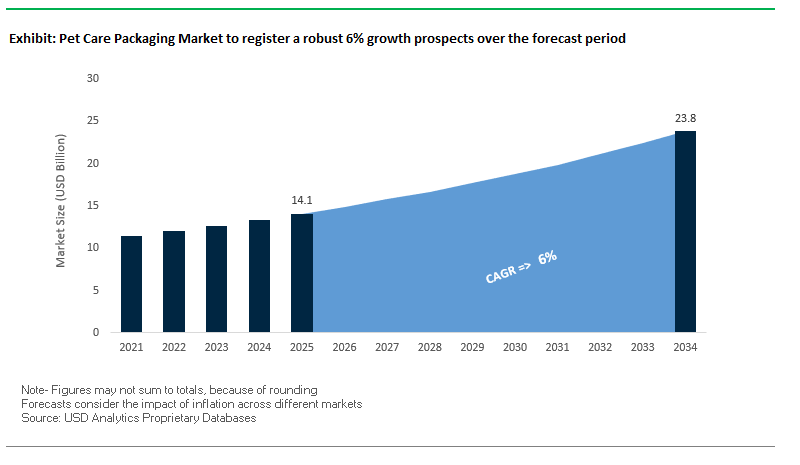

The Global Pet Care Packaging Market is evolving rapidly, reflecting the growing trend of pet humanization. Packaging is no longer just a protective container—it is an essential tool for brand storytelling, consumer engagement, and product integrity. The market is projected to expand from $14.1 billion in 2025 to $23.8 billion by 2034, at a CAGR of 6%, driven by demand for sustainable materials, convenience-focused designs, and e-commerce optimization.

Key Insights for industry professionals and buyers:

- Market Growth: Expanding at a 6% CAGR, highlighting robust demand across dry, wet, and snack pet food segments.

- Sustainability Imperative: Shift toward recyclable, mono-material, and paper-based packaging to meet environmentally conscious pet owners’ expectations.

- Convenience-Driven Formats: Single-serve pouches, stand-up bags with resealable zippers, and easy-pour spouts cater to busy lifestyles and premium pet snacks.

- Advanced Preservation Technologies: Packaging with high-barrier properties protects wet food and kibble from oxygen, moisture, and light, ensuring product freshness.

- E-Commerce Optimization: Durable, lightweight, and visually appealing packaging designed to survive shipping and appeal to online shoppers.

- Consumer-Centric Innovation: Focus on premium experience packaging, aligning with the emotional value consumers place on their pets.

Market Analysis

Sustainability, Innovation, and Strategic Partnerships Are Reshaping the Pet Care Packaging Landscape

The pet care packaging market is highly dynamic, with recent developments emphasizing sustainability, technological innovation, and strategic consolidation. In September 2025, Mondi partnered with Saga Nutrition to launch recyclable mono-material bags for dry pet food, replacing traditional multi-material packaging. In August 2025, ProAmpac released its Sustainability Impact Report, highlighting net-zero emissions targets and circular packaging initiatives, and simultaneously acquired a flexible packaging manufacturer in the U.S. Midwest to expand production capabilities. That same month, Mars Petcare launched recyclable pouches for its WHISKAS brand in the UK and Germany, signaling a major commitment to sustainable pet food solutions.

July 2025 showcased collaborative innovation, with AptarGroup, Inc. announcing partnerships to develop new pet care solutions, while the Pet Sustainability Coalition launched programs to assist companies in transitioning to eco-friendly packaging. Consumer insights in June 2025 revealed a strong preference for “less-plastic” approaches in pet food packaging, further driving sustainable product development. Earlier in the year, in February 2025, Berry Global and VOID Technologies collaborated to create high-performance, sustainable films tailored for pet food packaging, offering enhanced barrier protection to extend product freshness.

Emerging Trends and Growth Opportunities Reshaping the Pet Care Packaging Market

Mandated Shift to Recyclable Mono-Material Flexible Pouches

Regulatory mandates are accelerating the transition toward recyclable mono-material packaging in the pet care packaging market. Extended Producer Responsibility (EPR) frameworks, particularly under the EU’s Packaging and Packaging Waste Regulation (PPWR), are creating financial incentives for companies to switch from multi-material laminates to mono-polyethylene (PE) and mono-polypropylene (PP) pouches. By categorizing packaging based on recyclability grades, the PPWR imposes higher fees on harder-to-recycle structures, effectively pressuring companies to move toward mono-material designs. Industry leaders such as Mondi have highlighted that adopting high recyclability packaging will not only reduce EPR fees but also strengthen sustainability credentials. Pet food giants like Mars are redesigning entire packaging portfolios, with a pledge to make 100% of their packaging reusable, recyclable, or compostable by 2025. This push has also triggered rapid material science innovation. For example, TC Transcontinental Packaging is advancing Biaxially Oriented Polyethylene (BOPE), which enhances recyclability while delivering superior strength, durability, and printability compared to conventional mono-materials. These innovations are vital in ensuring barrier properties against moisture and oxygen are maintained, a critical requirement for maintaining product freshness in pet food.

Integration of Smart Packaging for Supply Chain Transparency and Freshness

The rise of digitalization is reshaping the role of packaging in the pet care industry, where smart packaging solutions are being leveraged for transparency, product safety, and authenticity. Brands are embedding QR codes and NFC tags into flexible packaging to provide real-time product traceability, allowing consumers to view details on sourcing, manufacturing processes, and nutritional profiles by simply scanning a package. This transparency is especially important in the premium pet food category, where trust and quality assurance are vital. Beyond traceability, smart packaging also enables food integrity monitoring. Freshness indicators, oxygen scavengers, and colorimetric sensors are being explored to alert consumers and retailers if pet food quality has been compromised during transport or storage. In addition, the surge in e-commerce pet food sales has heightened the risk of counterfeiting, and smart packaging offers a robust solution. Serialized NFC tags or unique QR codes allow consumers to instantly verify authenticity, safeguarding both brand integrity and consumer safety. As consumer demand for assurance grows, packaging is evolving into a key differentiator in customer trust-building strategies.

Development of High-Barrier, Compostable Bags for Pet Waste

The pet care packaging market holds a strong opportunity in the commercialization of high-barrier compostable bags for pet waste. With growing environmental awareness, consumers are increasingly seeking alternatives to conventional plastic bags. Compostable waste bags, made from plant-based feedstocks such as cornstarch, are gaining traction, particularly when certified under international standards like ASTM D6400 (U.S.) and EN 13432 (EU). Certification ensures complete biodegradation into non-toxic organic matter under industrial or home composting conditions. However, durability has historically been a barrier to adoption. Recent advancements in biopolymer engineering have addressed this issue, enabling compostable bags to achieve puncture resistance, leak-proofing, and tear resilience comparable to plastic alternatives. These improvements ensure that eco-friendly bags not only meet sustainability requirements but also provide the functional performance that consumers demand. The segment is also supported by municipal composting initiatives in Europe and North America, further boosting adoption potential.

Advanced PCR Incorporation in Rigid Packaging for Pet Food

The next wave of innovation in pet care packaging lies in advanced use of post-consumer recycled (PCR) content in rigid packaging formats such as tubs, trays, and jars. Traditionally, challenges around food safety, odor removal, and mechanical properties have restricted PCR adoption in food-contact applications. However, advancements in purification and deodorization processes are making it possible to incorporate higher percentages of food-grade PCR without compromising safety or performance. FDA favorable determinations are expected to unlock greater opportunities in this space. While recycled PET (rPET) dominates today, expansion into food-grade HDPE and PP resins through chemical recycling technologies offers significant growth potential. These advanced recycling methods produce near-virgin quality resins that meet stringent regulatory standards, enabling pet food brands to achieve ambitious recycled content targets. The shift aligns with global sustainability pledges, including commitments under the U.S. Plastics Pact and Ellen MacArthur Foundation’s circular economy initiatives, positioning PCR integration as a critical driver of innovation and competitive differentiation in the pet food packaging sector.

Competitive Landscape: Key Industry Players Are Driving Sustainability, Innovation, and Consumer-Centric Design in Pet Care Packaging

The global pet care packaging market is shaped by leading players leveraging expertise in materials science, manufacturing, and innovative design to deliver durable, high-performance, and eco-friendly solutions. These companies are setting benchmarks in sustainability, product preservation, and convenience-oriented formats.

Amcor plc: Leading the Market with Tailored Sustainable Pet Food Packaging Solutions

Amcor offers flexible and rigid packaging for pet treats and accessories, including EcoGuard™ heat-ready and recycle-ready bags and pouches. The company focuses on creating mono-material, high-barrier films that maintain freshness while being recyclable. With a global manufacturing network and material science expertise, Amcor supports both large-scale producers and niche brands. Its 2025 strategy emphasizes recyclable or reusable packaging and collaboration with pet food brands for environmentally responsible solutions.

Mondi Group: Championing Circular Economy Solutions with Innovative Mono-Material Designs

Mondi provides paper-based FlexiBag Recyclable solutions, stand-up pouches with resealable zippers, and custom pet care packaging. In September 2025, its collaboration with Saga Nutrition launched recyclable mono-material dry pet food bags, reinforcing the company’s commitment to sustainable packaging. Mondi leverages an integrated value chain to guide customers toward circular solutions and designs packaging aligned with its MAP2030 sustainability plan.

Silgan Holdings Inc.: Innovating Rigid and Flexible Packaging with Streamlined Supply Chain Integration

Silgan manufactures plastic bottles, jars, and pouches for pet shampoos, grooming products, and wet pet food. Its vertically integrated model ensures compatibility between containers and closures, simplifying the supply chain. The company’s ongoing investments in new technologies enhance its product diversity, supporting the growing demands of the pet care industry. Silgan emphasizes innovation and cost-effective solutions to maintain leadership in its core markets.

Huhtamaki Oyj: Delivering High-Barrier Flexible Solutions for Premium Pet Care Products

Huhtamaki produces retort pouches, stand-up pouches, and flexible rollstock for wet and dry pet food. Its partnership with SABIC and Mars Petcare aims to create flexible packaging from certified circular polypropylene. With a global manufacturing footprint, Huhtamaki provides high-quality, high-barrier films that protect product freshness and safety while supporting ambitious sustainability goals for 2030.

Constantia Flexibles Group GmbH: Advancing Specialized and Sustainable Flexible Packaging for Pet Treats

Constantia Flexibles offers aluminum foil containers, high-barrier laminates, and pouches for wet food and premium treats. The company invests in innovative materials and technology to develop packaging that is both eco-friendly and high-performing. Its tailored solutions meet specialized requirements of pet food brands, enabling safe storage and delivery while advancing sustainability objectives.

Pet Care Packaging Market Share Insights, 2025-2034

Bags & Pouches Dominate Product Type Share in the Pet Care Packaging Market

In the pet care packaging market, bags and pouches account for 45% of total share, cementing their position as the backbone of dry and semi-moist pet food packaging. Their dominance is driven by scalability—from single-serving pouches to bulk 20kg bags—paired with advanced barrier technologies that lock in freshness and nutrition. Stand-up pouches with resealable zippers, handles, and premium print finishes have become the industry benchmark, aligning with consumer demand for convenience, portability, and sustainable formats. Lightweight properties reduce logistics costs and carbon footprint, making pouches the go-to packaging solution for brand owners seeking efficiency and eco-friendly credentials. This segment’s versatility ensures it remains the default format for both mainstream and premium pet food products.

Pet Food Retains Overwhelming Market Share by Application in the Pet Care Packaging Industry

Pet food represents 78% of the total application share, making it the overwhelming driver of the pet care packaging industry. High consumption volumes, recurring purchases, and the expanding global pet ownership base ensure that food packaging accounts for the vast majority of demand compared to grooming or medication. The megatrend of “pet humanization” further amplifies the importance of packaging as a tool for communicating health benefits, freshness, and sustainability. Brand owners are investing heavily in eco-friendly formats, recyclable films, and resealable closures to meet consumer expectations for convenience and environmental responsibility. Packaging innovation in this segment also directly impacts brand loyalty, as consumers increasingly associate premium, protective, and sustainable packaging with product quality and pet well-being.

United States Pet Care Packaging Market Driven by Sustainability and E-Commerce

The United States pet care packaging market is undergoing a significant transformation as sustainability becomes a central priority for brands and consumers. Companies like Dow are pioneering down-gauging technologies that reduce material thickness while maintaining strength, lowering costs and environmental impact. Similarly, Procter & Gamble (P&G) has extended its use of recyclable packaging innovations from personal care into its pet care portfolio, setting benchmarks for eco-friendly product lines.

A strong consumer trend toward premiumization and pet humanization is fueling demand for resealable stand-up pouches, which offer convenience, freshness retention, and portability. Additionally, the rise of innovative barrier technologies is extending the shelf life of dry, moist, and freeze-dried foods without reliance on non-recyclable multi-material structures. The e-commerce boom further drives demand for lightweight yet durable formats, with brands investing in packaging capable of withstanding shipping stresses while minimizing costs. On-pack certifications and transparent labeling are becoming essential, as companies highlight sustainability achievements to connect with eco-conscious pet owners.

China Pet Care Packaging Market Expands with E-Commerce and Premiumization

The China pet care packaging market is heavily influenced by GB 23350-2021 regulations, which limit excessive packaging and encourage brands to adopt thinner walls and paperboard sleeves for secondary formats. As Chinese consumers increasingly embrace premium and sustainable pet care products, brands are investing in travel-friendly and convenient formats, such as single-serve packs and portable pouches.

The country’s booming e-commerce ecosystem plays a pivotal role, with online channels driving substantial packaging demand, particularly in ready-to-ship and bulk formats. Domestic manufacturers are scaling capacity and adopting innovative coating technologies to meet performance and sustainability goals. Moreover, rising investments in local production capabilities ensure that premium, customized pet packaging remains competitive against international imports. This convergence of policy-driven compliance, consumer demand, and domestic capacity-building is cementing China’s role as a leader in sustainable pet care packaging innovation.

United Kingdom Pet Care Packaging Market Reshaped by EPR and Recycling Mandates

The United Kingdom pet care packaging market is adapting rapidly under strict sustainability regulations. The Extended Producer Responsibility (EPR) framework places financial responsibility for packaging waste on producers, driving investment in recyclable and mono-material packaging. Government mandates requiring flexible plastics collection by March 2027 are accelerating the adoption of recyclable films and pouches.

Key players such as Mars have pioneered recyclable mono-material retort pouches for pet food, ensuring shelf life while improving recyclability. Additionally, projects funded by the Smart Sustainable Plastic Packaging (SSPP) Challenge are reducing single-use plastics and promoting reusable systems. Consumer demand for plastic-free solutions is pushing brands toward recycled PET, FSC-certified paperboard, and aluminum-based designs. The Flexible Plastic Fund’s 2025 report further strengthens industry direction, highlighting scalable collection systems that are expected to boost demand for eco-friendly pet care packaging across the UK.

Germany Pet Care Packaging Market Advances with Premium Materials and Digital Innovation

The Germany pet care packaging market is evolving alongside the country’s established reputation for engineering precision and sustainability. German manufacturers are leading the shift from needle perforation to advanced laser systems, ensuring consistent shelf-life extension for perishable pet foods. Additionally, the adoption of Polyethylene Terephthalate (PET) packaging aligns with EU recyclability goals, offering superior clarity and oxygen barrier properties.

Companies such as MM Group are integrating advanced printing and finishing technologies, including UV offset and digital printing, to deliver premium packaging designs for pet care. At the same time, refill systems and concentrates, long applied in the detergent sector, are gaining traction for pet care as a cost- and material-saving strategy. Innovations such as multi-material aluminum-paper hybrids are being tested for niche premium segments, while the broader market is moving toward eco-friendly, recyclable paper-based alternatives. This balance of premiumization, regulatory compliance, and advanced material science places Germany at the forefront of high-quality pet care packaging.

India Pet Care Packaging Market Strengthened by Plastic Ban and Rising Middle-Class Demand

The India pet care packaging market is witnessing strong growth driven by regulatory reforms and lifestyle changes. The July 1, 2022 ban on single-use plastics has forced pet care brands to transition toward sustainable alternatives, while companies like Hindustan Unilever and Procter & Gamble India set precedents with recyclable packaging initiatives. Amway India and other leading brands have also introduced eco-friendly solutions to align with consumer preferences.

The rising middle-class population and disposable incomes are fueling demand for premium pet food packaging, with emphasis on convenience and durability. E-commerce expansion further necessitates tamper-evident, visually appealing packaging for online sales and deliveries. Additionally, the Bureau of Indian Standards (IS 11968:2019) has introduced voluntary specifications for pet food packaging, ensuring hygiene and quality standards. Together, these dynamics are fostering a market where sustainability, affordability, and regulatory compliance drive innovation in India’s pet care packaging sector.

Japan Pet Care Packaging Market Driven by Freshness Preservation and Circular Economy Goals

The Japan pet care packaging market is shaped by the country’s focus on food freshness, hygiene, and convenience, which directly extends to pet food packaging. Health-conscious consumers and an aging population are fueling demand for advanced preservation technologies, including breathable and protective packaging for long shelf life.

The rise of vertical farming and micro-portion pet food packaging highlights a niche but fast-growing demand for specialized solutions. Meanwhile, the expansion of e-commerce and home delivery services is driving the adoption of protective perforated and breathable packaging formats to ensure safety during transit. The Japanese government’s circular economy initiatives are compelling companies to adopt eco-friendly, recyclable, and biodegradable materials, ensuring alignment with both sustainability goals and consumer expectations. Japanese firms continue to innovate with high-performance functional materials, setting global standards in premium, sustainable pet care packaging.

Pet Care Packaging Market Report Scope

Pet Care Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.1 Billion

|

|

Market Size (2034)

|

$23.8 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Material (Plastic, Glass, Metal, Paper & Paperboard, Others), By Product Type (Bags & Pouches, Cans, Bottles & Jars, Folding Cartons, Trays & Bowls), By Pet Type (Dogs, Cats, Other Pets), By Food Type (Dry Food, Wet Food, Pet Treats), By Application (Pet Food, Pet Grooming Products, Pet Medications, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Berry Global, Inc., Silgan Holdings Inc., Sealed Air Corporation, Sonoco Products Company, Huhtamaki Oyj, ProAmpac, Coveris, Guala Pack S.p.A., Winpak Ltd., AptarGroup, Inc., Greif, Inc., Mondi Group, Crown Holdings Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pet Care Packaging Market Segmentation

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

- Others

By Product Type

- Bags & Pouches

- Cans

- Bottles & Jars

- Folding Cartons

- Trays & Bowls

By Pet Type

By Food Type

- Dry Food

- Wet Food

- Pet Treats

By Application

- Pet Food

- Pet Grooming Products

- Pet Medications

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pet Care Packaging Market

- Amcor plc

- Mondi Group

- Berry Global, Inc.

- Silgan Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Huhtamaki Oyj

- ProAmpac

- Coveris

- Guala Pack S.p.A.

- Winpak Ltd.

- AptarGroup, Inc.

- Greif, Inc.

- Mondi Group

- Crown Holdings Inc.

* List Not Exhaustive

Methodology

The Pet Care Packaging Market report by USDAnalytics is developed using a comprehensive methodology that combines both primary and secondary research approaches to deliver highly accurate, actionable, and professional insights for industry stakeholders. Our research team analyzed company annual reports, press releases, investor presentations, sustainability disclosures, and regulatory filings to capture the latest developments in packaging innovation, material usage, and sustainability practices. Secondary sources included industry associations, government publications, and trade journals to ensure data accuracy and completeness. Primary interviews with key market participants, packaging designers, and supply chain experts further validated market trends, growth drivers, and emerging opportunities, particularly in sustainable and e-commerce-optimized formats. USDAnalytics employs a robust data triangulation process to reconcile supply-side and demand-side information, ensuring reliable projections for market value, CAGR, and segment growth across key geographies. All findings are enriched with insights on regulatory mandates, technological innovation, competitive landscape, and consumer behavior patterns, providing a detailed roadmap for decision-makers in pet care packaging investments, strategic partnerships, and product development initiatives.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.