Market Overview: Stimuli-Responsive Polymers Transition From Novelty Materials To System-Level Enablers

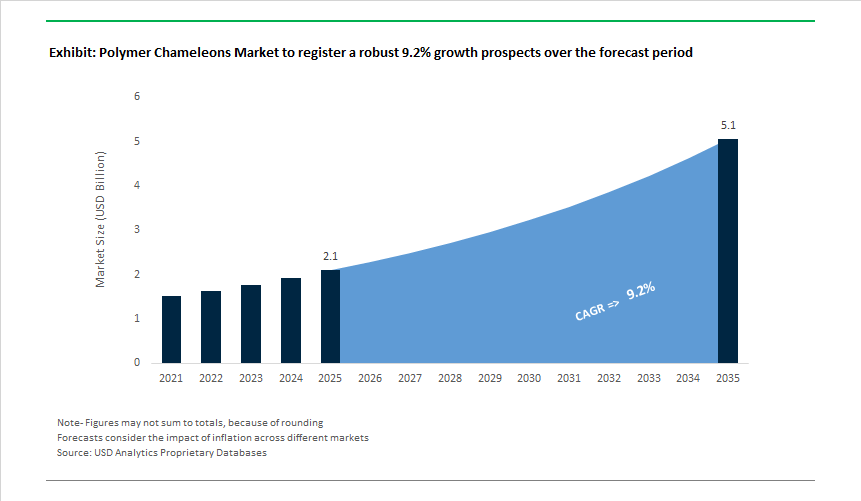

The Polymer Chameleons Market, valued at USD 2.1 billion in 2025 and projected to reach USD 5.1 billion by 2035 at a 9.2% CAGR, is entering a phase where commercial adoption is no longer driven by laboratory novelty but by measurable system-level value creation. Across pharmaceuticals, advanced textiles, aerospace structures, and protective coatings, OEMs are increasingly specifying polymers that can sense, respond, and adapt to operating conditions rather than remain mechanically static. For manufacturers, these materials compress functionality that previously required multi-component assemblies-actuators, sensors, coatings, and control systems-into a single material platform, reducing bill-of-materials complexity, assembly steps, and lifecycle maintenance costs.

Demand is being reshaped by a clear structural shift: responsiveness must now be repeatable, fast, and industrially reliable, not merely demonstrable. Thermo-responsive polymers with defined LCST behavior, photochromic systems, shape-memory polymers (SMPs), and self-healing chemistries are increasingly benchmarked against OEM performance specifications rather than academic proofs of concept. In addition, manufacturers report that buyers now require thousands of reversible cycles with low hysteresis for photo- and thermo-responsive systems, while self-healing coatings must restore ≥90% of fracture or barrier performance after micro-damage to justify replacing conventional protective layers in infrastructure, aerospace, and industrial assets.

Legacy static polymers and multi-layer assemblies are therefore being displaced where smart polymers can demonstrably reduce cost, weight, or maintenance intervention. In drug delivery and medical devices, stimuli-responsive polymers enable pulsatile release and self-deploying implants, eliminating mechanical pumps or complex assemblies but imposing stringent biocompatibility and degradation control requirements. In smart textiles and automotive interiors, adaptive color, permeability, or stiffness replaces electronics-heavy solutions, provided materials can survive washing, UV exposure, and repeated deformation. In industrial and infrastructure coatings, self-healing polymer networks are being adopted where they extend inspection intervals and asset life by autonomously mitigating micro-cracks and corrosion initiation.

Market Analysis: Key Industry Events and Technology Momentum

R&D commercialization accelerated through 2024-2025, driven by cross-sector funding and targeted product launches. In Jan 2025, private AI/materials startups secured Series A funding for ML platforms that reduce formulation cycles - enabling faster route-to-market for novel responsive chemistries. Mar 2025 and Jul 2025 saw concrete application moves: academic journals highlighted humidity/temperature sensing polymer coatings for e-textiles, and a global drug-delivery firm entered Phase II clinical trials (Jul 2025) for pH-responsive oral systems that target lower-intestinal release - signalling regulatory and clinical momentum for stimulus-activated therapeutics. In Apr 2025 the European Aerospace Agency allocated €10 million to shape-memory polymer research for deployable space structures, validating aerospace demand for weight-saving, autonomous morphing components.

Commercial players also announced product programs in 2025: Oct 2025 Dow launched responsive polymers for smart healthcare textiles (real-time body monitoring), while Nov 2025 BASF introduced an eco-adaptive chameleon polymer line aimed at sustainable industrial coatings that dynamically modulate heat-transfer or surface appearance. Academic and institutional breakthroughs - for example, the Dec 2025 joint University Consortium/Dow proof of reversible bio-compatible SMPs in simulated biological environments - indicate convergence of materials science and bioengineering enabling resorbable, deployable medical devices.

Polymer Chameleons Market Trends and Opportunities

pH- and Enzyme-Responsive Polymer Systems Enabling Precision Drug Delivery

The polymer chameleons market is rapidly aligning with precision medicine, as drug developers move from passive carriers toward stimuli-responsive polymer architectures that function as biochemical logic gates. These systems are engineered to remain inert during circulation and activate only when exposed to disease-specific cues such as acidic pH, elevated enzyme concentrations, or localized hyperthermia—dramatically improving therapeutic index while reducing systemic toxicity.

In early 2025, pH-responsive synthetic cell platforms demonstrated site-selective protein synthesis and release triggered exclusively in acidic microenvironments typical of tumors and infected tissue. These platforms rely on pH-sensitive DNA–polymer conjugates that undergo conformational switching, activating translation only under pathological conditions. Parallel commercialization is underway in chronic wound care, where ROS- and MMP-responsive hydrogels—validated in 2025 studies—combine moisture management with on-demand antimicrobial release only when infection biomarkers are present, reducing unnecessary antibiotic exposure.

A further layer of sophistication is emerging through dual-stimuli systems that integrate thermoresponsive cores (e.g., PNIPAm) with pH-sensitive shells. Clinical and preclinical data from 2024–2025 show these architectures protecting fragile biologics from gastric degradation and releasing payloads selectively at hyperthermic tumor sites. Collectively, these advances position polymer chameleons as enabling materials for oncology, inflammatory disease management, and next-generation biologics—applications where dosing precision is now a commercial requirement, not a differentiator.

Light-Activated, Self-Healing Polymers for Aerospace and Electronics Durability

In electronics and aerospace, polymer chameleons are being adopted as dynamic covalent polymers (DCPs) capable of autonomous self-repair under light, heat, or mechanical stress. Unlike traditional coatings, these materials exploit reversible bond chemistry to heal micro-damage before it propagates into structural failure—directly extending service intervals in extreme environments.

In May 2025, researchers at Texas A&M University reported a light-responsive polymer that absorbs kinetic energy from high-velocity impacts and rapidly reforms covalent bonds, leaving punctures smaller than the impacting particle. This behavior is highly relevant for orbital satellite windows and reusable launch systems, where micrometeoroid damage is a persistent risk.

Commercial aerospace adoption is accelerating. By 2025, Airbus and COMAC had integrated capsule-filled epoxies and DCP-based thermoplastics into radomes and cabin interiors, with patent activity in self-healing aerospace materials nearly doubling since 2022. In arid operating environments, maintenance centers are deploying light-activated erosion-control films designed to withstand sand abrasion, targeting up to 50% reductions in repainting and MRO downtime over the next decade. These use cases underscore polymer chameleons’ role as cost-containment materials.

Phase-Change Polymer Systems for Dynamic, Low-Energy Building Insulation

Decarbonization mandates across Europe are opening a high-impact opportunity for thermochromic and phase-change polymer systems in buildings. Polymer chameleons embedded in glazing and envelope materials dynamically modulate optical transmittance and thermal conductivity, providing zero-power thermal regulation that complements or replaces active HVAC control.

Studies published in 2025 confirm that LCST-based thermoresponsive hydrogels can autonomously regulate solar gain—an important lever given that windows account for nearly half of building energy loss in mixed climates. New formulations of hydroxypropyl cellulose and PNIPAm are already being integrated into smart glazing units that reversibly shift from transparent to opaque once temperature thresholds are crossed, flattening peak cooling loads without external power.

Policy alignment is accelerating adoption. In 2025, the EU Innovation Fund earmarked substantial funding for AI-integrated physical systems, explicitly welcoming waste-heat utilization and carbon-substituting materials. Polymer chameleons sit squarely at this intersection, positioning them as cornerstone materials for net-zero architecture and deep-retrofit strategies under Green Deal and REPowerEU frameworks.

Ionic-Strength Responsive Polymers for Water Treatment and Critical Mineral Recovery

Resource security and circular-economy goals are driving demand for ionic-strength and pH-responsive polymer chameleons in water treatment and mining. These materials enable selective adsorption and release of target ions under mild conditions, dramatically lowering energy input compared to conventional separation technologies.

By late 2025, ion-imprinted polymers (IIPs) had emerged as leading candidates for extracting rare earth elements from acid mine drainage, demonstrating high selectivity for neodymium even amid overwhelming concentrations of calcium and magnesium. This capability directly supports U.S. and EU strategies for domestic critical-mineral supply without new primary mining.

At the membrane level, pH- and salt-responsive ultrafiltration systems reported in 2025 overcome the traditional permeability–selectivity tradeoff by dynamically adjusting pore size in response to feed chemistry. These smart membranes enable efficient removal of heavy metals and dyes using minimal pressure, reducing operational costs in industrial wastewater treatment. Complementing this, bio-based polymer adsorbents are gaining traction in nutrient-management programs across Mediterranean regions, supported by targeted EU grants, to regulate nitrogen and phosphorus cycles and mitigate eutrophication.

Market Share Analysis: Polymer Chameleons Market

Market Share by Stimulus Type: Physical Stimuli-Responsive Polymers Set the Control and Reliability Benchmark

Physical stimuli-responsive polymers account for approximately 50% of the global Polymer Chameleons Market, reflecting their position as the most controllable, scalable, and application-ready class of smart polymers. This dominance is driven by their ability to respond to temperature and light triggers with high precision and reversibility, without relying on chemical additives or external reagents that increase system complexity and regulatory burden. Thermo-responsive polymers, particularly those engineered around human-relevant transition thresholds, enable predictable phase changes that align naturally with environmental or physiological conditions, making them especially valuable in biomedical and wearable systems. Market share is further reinforced by tight switching windows, which allow materials to activate within narrow temperature or light ranges—an essential requirement for high-precision sensors, adaptive coatings, and responsive surfaces in electronics and automotive platforms. Durability also plays a decisive role, as physically triggered polymers maintain performance across thousands of activation cycles with minimal structural fatigue, supporting long service lives in aerospace, robotics, and 4D-printed components. The elimination of external power or chemical triggers further strengthens adoption, enabling energy-free actuation driven purely by ambient conditions. Together, these attributes—precision, reversibility, durability, and low system complexity—position physical stimuli-responsive polymers as the dominant stimulus platform in the polymer chameleons market.

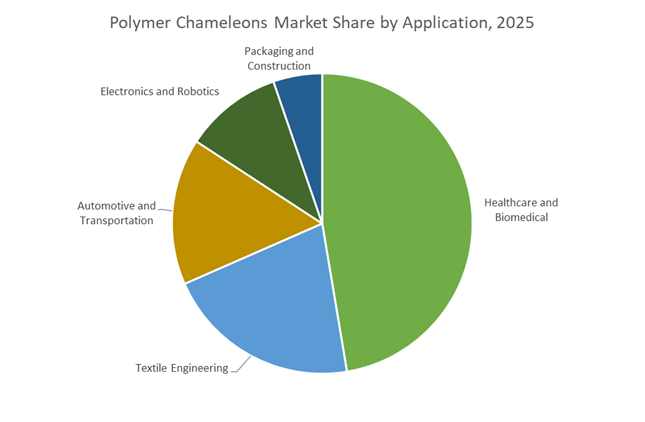

Market Share by Application: Healthcare and Biomedical Applications Anchor High-Value Demand

The healthcare and biomedical segment represents approximately 45% of total demand in the Polymer Chameleons Market, making it the largest and most value-intensive application area. This leadership is rooted in the sector’s need for targeted, responsive therapies that minimize systemic exposure while maximizing treatment efficacy. Stimuli-responsive polymers enable drug delivery systems that activate only under specific physiological conditions, dramatically reducing off-target toxicity and improving patient outcomes—particularly in oncology, inflammation, and chronic disease management. Market share is further reinforced by the rise of on-demand wound care and regenerative materials, where smart polymers respond dynamically to infection, temperature, or tissue growth signals, accelerating healing while reducing antibiotic overuse. Regulatory readiness also supports adoption, as leading biomimetic polymer systems are engineered to meet stringent biocompatibility and sterilization standards without compromising trigger sensitivity. In tissue engineering, adaptive polymer scaffolds that adjust stiffness and porosity in response to cellular activity deliver superior cell proliferation and integration compared to static materials. As healthcare systems increasingly prioritize precision medicine, safety, and long-term cost reduction, biomedical applications remain the primary commercial anchor for polymer chameleons, sustaining their dominant market share.

Competitive Landscape: Who’s Leading Polymer Responsiveness Commercialization

The Polymer Chameleons competitive set is a mix of chemical giants with broad monomer/additive portfolios, specialty biomaterials firms, and focused innovators in microencapsulation and SMP manufacturing. Leaders combine scale, regulatory experience, and targeted R&D to convert stimuli-responsive chemistries into manufacturable formulations.

BASF SE - Supplying Eco-Adaptive, Large-Scale Responsive Polymer Platforms

BASF leverages deep polymer and additive chemistry to deliver thermo- and photo-responsive building blocks and formulated coatings. Its 2025 eco-adaptive polymer initiative targets sustainable, heat-responsive coatings for industrial heat-exchanger optimization and adaptive insulation surfaces. BASF’s scale allows rapid global supply of monomers and pigment systems while ensuring environmental compliance - a critical advantage for customers seeking to replace static coatings with intelligent, low-VOC alternatives in automotive interiors and large-volume industrial uses.

Dupont De Nemours, Inc. - High-Performance Fluoropolymers and Electroactive Systems For Harsh Environments

DuPont combines specialty fluoropolymers with dielectric elastomer expertise to produce materials that withstand aggressive conditions while delivering repeatable actuation or sensing. Its patent portfolio in electroactive polymers (EAPs) and dielectric elastomers supports miniaturized actuators and artificial muscles for robotics, plus resilient responsive films for aerospace and industrial monitoring. DuPont’s strengths lie in enabling responsive materials that retain optical clarity and mechanical integrity across thousands of cycles - a must for aerospace sensors and high-reliability industrial devices.

Evonik Industries AG - Medical-Grade Responsive Polymers and Degradable Systems

Evonik is a market leader for high-purity, medical-grade responsive polymer systems including PLGA-based and enzyme-sensitive materials used in long-acting injectables and implantables. The company targets 3D-printed patient-specific scaffolds and resorbable devices where precise, predictable response and biocompatibility are essential. Evonik’s expertise in degradable polymer chemistries and regulatory know-how positions it to serve pharmaceutical and medical device OEMs adopting stimulus-responsive drug delivery and implant technologies.

Autonomic Materials, Inc. - Microencapsulation Pioneers For Autonomous Self-Healing Coatings

Autonomic Materials focuses on microencapsulated healing agents integrated into coatings and composites. Their capsule-based systems rupture on crack initiation, releasing healing chemistry that restores barrier properties and corrosion protection - achieving measurable extension of asset life in oil & gas and defense sectors. The company’s licensing model enables coatings OEMs to adopt self-healing functionality without in-house capsule manufacture, accelerating deployment in high-maintenance industrial infrastructure.

SMP Technologies Inc. - Precision Shape-Memory Polymers For Medical and Consumer Devices

SMP Technologies specializes in polyurethane-based SMPs and newer electro/magnetically-triggerable variants. Their products offer sharp, tightly controlled glass transition temperatures (±1°C), ultra-fast recovery rates and high thermal stability - enabling self-folding implants, self-tightening connectors, and adaptive consumer components. SMP Technologies’ focus on tunable Tg control and remote triggering (electric/magnetic) meets OEM demands for wireless actuation and reliable performance in both biomedical and industrial applications.

The United States represents the most advanced commercialization environment for polymer chameleons, particularly across biomedical devices, aerospace systems, and adaptive building materials. In 2025, federal grant expansion by the National Science Foundation (NSF) and Department of Energy (DOE) has materially shortened the path from stimuli-responsive polymer research to deployable products. Funding programs increasingly prioritize bio-based smart polymers capable of autonomously responding to thermal, pH, and mechanical stimuli-supporting national objectives around energy efficiency, lightweighting, and advanced healthcare delivery. This policy alignment has strengthened demand for self-healing elastomers, electroactive polymers, and thermoresponsive insulation materials across defense, infrastructure, and life sciences.

Commercial momentum is strongest in precision medicine and aerospace-grade materials. U.S.-based material leaders such as Lubrizol and DuPont continue to translate laboratory-scale polymer intelligence into scalable solutions, exemplified by DuPont’s 2025 launch of ultra-low-temperature TPE tubing for biopharmaceutical cold-chain processing. Parallel to this, venture-backed startups are rapidly advancing shape-memory and self-healing polymer systems designed to withstand extreme pressure, radiation, and temperature fluctuations-capabilities essential for next-generation aircraft structures and space systems. This convergence of federal funding, venture capital, and high-value end-use sectors positions the U.S. as the global benchmark for premium polymer chameleon applications.

Germany: Bionic Engineering and Circular Economy Integration

Germany remains the innovation nucleus of Europe’s polymer chameleons market, driven by strict sustainability mandates and a strong industrial-academic collaboration model. In 2025, national priorities emphasize biodegradable and recyclable smart polymers that align with circular economy principles while delivering adaptive performance. German chemical leaders, including BASF, Covestro, and Evonik, are refocusing portfolios toward stimuli-responsive additives and functional polymer modifiers that reduce material usage and energy intensity across automotive and construction sectors. Evonik’s “Smart Effects” launch in early 2025 exemplifies this strategic consolidation toward intelligent material platforms.

Automotive remains Germany’s most influential demand engine. The integration of photochromic and thermochromic polymers into vehicle exteriors-most notably by BMW-highlights how polymer chameleons are transitioning from novelty features to functional systems that improve thermal regulation and aesthetic differentiation. Supporting this industrial uptake is Germany’s dense research infrastructure, led by institutions such as RWTH Aachen and the University of Bayreuth, where digital polymer blending and microwave-assisted polymerization are cutting manufacturing energy consumption by up to 40%. This combination of regulatory pressure, OEM adoption, and process innovation cements Germany’s leadership in sustainable, high-performance smart polymers.

China: Mass Manufacturing and Infrastructure-Led Polymer Intelligence

China’s polymer chameleons market in 2025 is defined by scale, speed, and infrastructure-driven demand. Under directives from the Ministry of Industry and Information Technology (MIIT), smart polymers are increasingly embedded into national infrastructure, construction, and textile modernization programs. State-backed initiatives emphasize self-cleaning, anti-tampering, and adaptive coatings-applications where large volumes and cost efficiency are decisive. This has positioned China as the world’s dominant producer of functional coatings and smart polymer intermediates, particularly for polyurethane, epoxy, and silicone-based responsive systems.

Strategic partnerships are accelerating industrial adoption. The opening of the NEXCEL center in Beijing, supported by Aramco and the China Building Materials Academy, underscores China’s focus on polymer-modified concrete, waterproofing systems, and infrastructure-scale chameleon materials. Concurrently, export momentum remains strong, with China supplying a significant share of global silicone elastomers and specialty resins used in responsive matrices. As infrastructure resilience and “Dual Carbon” objectives converge, China’s ability to industrialize polymer chameleons at scale is reshaping global supply dynamics.

Japan: Robotics, Electroactive Polymers, and Super Engineering Plastics

Japan’s polymer chameleons strategy centers on high-precision applications where performance consistency and material intelligence are mission-critical. In 2025, electroactive polymers (EAPs) and shape-responsive engineering plastics are increasingly deployed across robotics, sensors, and advanced electronics. Japanese firms are leveraging decades of polymer science expertise to move beyond laboratory prototypes into mass-production platforms that reduce greenhouse gas emissions while improving functional responsiveness.

Sumitomo Chemical’s 2025 launch of mass-production technology for liquid crystal polymers (LCPs) represents a pivotal milestone, enabling scalable production of electro-responsive materials for smartphones, automotive sensors, and robotic actuators. In parallel, Mitsubishi Chemical Group’s bio-based DURABIO continues to gain traction in automotive exterior components, combining weather resistance with sustainability credentials. Government subsidies further reinforce this transition, incentivizing the shift from petroleum-based plastics toward bio-derived, stimuli-responsive polymers. Japan’s emphasis on reliability and precision ensures its leadership in high-end polymer chameleon applications.

South Korea: Smart Healthcare and Electronic-Grade Polymer Systems

South Korea occupies a strategically important position in the polymer chameleons market by focusing on electronic-grade and healthcare-responsive materials. The government’s MPE 2030 roadmap provides up to 25% R&D tax credits for companies developing bio-printed scaffolds, pH-responsive hydrogels, and enzyme-activated polymers. These materials are increasingly critical for smart wound care, diagnostic devices, and wearable medical sensors that autonomously signal physiological changes.

In 2025, South Korea has also emerged as a global convening hub for smart polymer research, hosting major international conferences that bridge biomedical polymers and electrical engineering. Domestic manufacturers are translating this research into precision polymers that integrate seamlessly with semiconductors and flexible electronics-an advantage reinforced by South Korea’s strong electronics manufacturing base. This specialization positions the country as a key supplier of polymer chameleons for next-generation healthcare and sensor-driven applications.

India: Textile Modernization and Bio-Packaging Expansion

India’s polymer chameleons market is gaining momentum through large-scale textile modernization and sustainable packaging initiatives. The inclusion of smart polymer technologies under the Technology Upgradation Fund Scheme (TUFS) in 2024–2025 has enabled textile manufacturers to invest in machinery capable of producing thermo-regulating and moisture-responsive fabrics. These developments are accelerating India’s transition from conventional apparel manufacturing to value-added smart textiles.

Beyond textiles, India is rapidly expanding its bio-packaging and healthcare polymer base. CSIR-IICT’s licensing of nanocellulose-engineered compostable plastics has already resulted in multiple commercial product launches utilizing responsive polymer behavior for sustainability-driven packaging. At the same time, rising public healthcare expenditure is stimulating domestic demand for responsive drug-delivery gels and bioseparation membranes. Collectively, these factors position India as a fast-growing, cost-competitive hub for polymer chameleon applications in textiles, packaging, and healthcare.

Strategic Comparison Matrix – Polymer Chameleons Market (2025)

Polymer Chameleons Market Matrix

|

Country

|

Primary Technical Focus

|

Key 2024–2025 Development

|

Strategic Driver

|

|

United States

|

Biomedical & Aerospace Polymers

|

Ultra-low-temperature TPE tubing launch

|

Federal R&D and Venture Capital

|

|

Germany

|

Automotive & Circular Materials

|

OEM adoption of color-changing polymers

|

Sustainability Mandates

|

|

China

|

Infrastructure & Functional Coatings

|

NEXCEL Beijing smart materials center

|

Mass Industrialization

|

|

Japan

|

Electroactive & Engineering Plastics

|

LCP mass-production technology

|

Precision Manufacturing

|

|

South Korea

|

Smart Healthcare & Sensors

|

MPE 2030 tax incentives for responsive polymers

|

High-Tech Localization

|

|

India

|

Smart Textiles & Bio-Packaging

|

TUFS upgrade and nanocellulose plastic licensing

|

Manufacturing Modernization

|

Polymer Chameleons Market Report Scope

Polymer Chameleons Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.1 Billion

|

|

Market Size (2035)

|

$5.1 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Stimulus Type (Physical, Chemical, Biological), By Material Class (Shape Memory Polymers, Self-Healing Polymers, Electroactive & Magnetically Responsive Polymers, Hydrogels & Aerogels, Conducting & Liquid Crystal Polymers), By Application (Healthcare & Biomedical, Automotive & Transportation, Textile Engineering, Packaging, Electronics & Robotics, Construction)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Covestro AG, Evonik Industries AG, Merck KGaA, DuPont de Nemours Inc., Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, Arkema S.A., LyondellBasell Industries N.V., Spintech Holdings Inc., Autonomic Materials Inc., SMP Technologies Inc., Solvay S.A., The Lubrizol Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymer Chameleons Market Segmentation

By Stimulus Type

- Physical Stimuli

- Chemical Stimuli

- Biological Stimuli

By Material Class

- Shape Memory Polymers

- Self-Healing Polymers

- Electroactive and Magnetically Responsive Polymers

- Hydrogels and Aerogels

- Conducting and Liquid Crystal Polymers

By Application

- Healthcare and Biomedical

- Automotive and Transportation

- Textile Engineering

- Packaging

- Electronics and Robotics

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymer Chameleons Market

- BASF SE

- Dow Inc.

- Covestro AG

- Evonik Industries AG

- Merck KGaA

- DuPont de Nemours, Inc.

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Arkema S.A.

- LyondellBasell Industries N.V.

- Spintech Holdings, Inc.

- Autonomic Materials, Inc.

- SMP Technologies Inc.

- Solvay S.A.

- The Lubrizol Corporation

*- List not Exhaustive