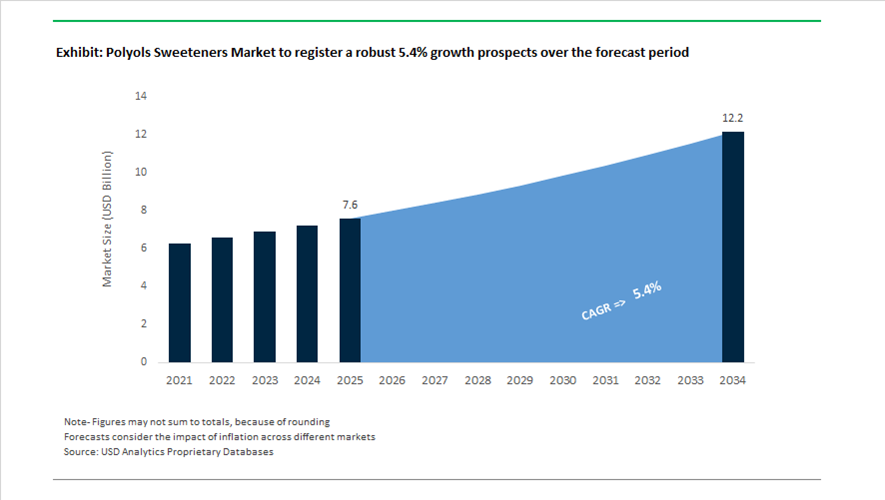

Polyols Sweeteners Market Valued at $7.6 Billion in 2025, Forecast to Reach $12.2 Billion by 2034 at 5.4% CAGR

The global polyols sweeteners market is valued at $7.6 billion in 2025 and is projected to reach $12.2 billion by 2034, expanding at a CAGR of 5.4%. Growth is driven by increasing demand for sugar alcohols such as erythritol, xylitol, sorbitol, maltitol, and isomalt across sugar-free confectionery, bakery, beverages, nutraceuticals, and diabetic-friendly formulations. Rising regulatory pressure on added sugars, front-of-pack labeling reforms, and consumer demand for low-glycemic, tooth-friendly, and clean-label sweeteners are reshaping formulation strategies globally. Polyols are increasingly positioned not only as bulk sweeteners but as functional ingredients delivering humectancy, mouthfeel, crystallization control, and caloric reduction in reduced-sugar systems.

Strategic integration across ingredient portfolios accelerated in 2024. In early 2024, Jungbunzlauer acquired Alliance Gums & Industries in France, enabling advanced blending of polyols with hydrocolloids to enhance texture and moisture stability in sugar-free confectionery and chewing gum. In July 2024, Ingredion EMEA launched the FIBERTEX CF citrus fiber line, designed to function synergistically with polyol sweeteners to restore viscosity and structure in sucrose-reduced applications. In June 2024, PureCircle, an Ingredion company, received UK approval for bioconversion-derived stevia ingredients, enabling the launch of polyol–stevia blends across Europe that combine high-intensity sweetness with the bulk and mouthfeel of sugar alcohols. In October 2023 and early 2024, NutraSweet introduced Reb M+ stevia extract formulated specifically to pair with erythritol and other polyols, mitigating the characteristic cooling effect while delivering a sucrose-like temporal sweetness profile.

Portfolio expansion and manufacturing localization intensified in 2025. In June 2025, Jungbunzlauer reported the commissioning of Austria’s largest photovoltaic power station, supplying renewable electricity to its polyol and organic acid production lines, strengthening its low-carbon polyol manufacturing credentials. In September 2025, Jungbunzlauer announced the acquisition of a multipurpose manufacturing site in Thomson, Illinois from International Flavors & Fragrances, with the transaction closing in November 2025. This move established Jungbunzlauer’s first major U.S. production footprint for bio-based polyols, enhancing supply chain resilience in North America. In November 2024, Tate & Lyle completed its $1.8 billion acquisition of CP Kelco, and throughout 2025 the company integrated specialty texturants with its existing sweetener systems to develop polyol–hydrocolloid synergy blends that improve mouthfeel and water-binding in reduced-sugar foods. In late 2025, Cargill expanded its non-GMO and traceable erythritol offerings following APAC consumer research showing heightened scrutiny of ingredient labels, reinforcing the clean-label positioning of fermentation-derived polyols.

Industrial diversification and sustainability initiatives are influencing long-term market dynamics. In late 2023 and early 2024, Gulshan Polyols secured contracts to supply alternative polyols and ethanol processing solutions to oil marketing firms, highlighting cross-sector applications in biofuels and green chemistry. In October 2025, Nouryon doubled triethylaluminum capacity in China, a critical input in the production of high-purity polymer-grade polyols used in food-contact and industrial systems. In early 2026, Roquette reported progress toward achieving 100% ISO 14001 certification across production sites by 2030, targeting decarbonization of starch hydrogenation processes central to sorbitol and maltitol production.

The polyols sweeteners market is increasingly defined by bio-based sugar alcohol production, polyol–stevia blend optimization, clean-label erythritol expansion, renewable energy integration in polyol plants, hydrocolloid-polyol texturizing systems, and diversification into biofuel and industrial-grade polyols. Manufacturing localization in North America, regulatory alignment in Europe, and consumer-driven clean-label reformulation in Asia-Pacific are reinforcing sustained demand across food, beverage, nutraceutical, and industrial applications.

Trends and Opportunities Shaping the Polyols Sweeteners Market

Strategic Reformulation and Portfolio Expansion in Sugar-Reduced Beverages

The polyols sweeteners market is becoming structurally embedded in beverage reformulation strategies as global brands move away from single-molecule, high-intensity sweeteners toward multi-component systems that deliver sweetness, bulk, and mouthfeel simultaneously. This shift has accelerated following the WHO 2023–2024 guidance discouraging the long-term use of non-sugar sweeteners for weight management, prompting manufacturers to favor nutritive, fermentation-derived ingredients that support clean-label positioning without sacrificing sensory performance.

In September 2025, PepsiCo confirmed that 67% of its global beverage portfolio had achieved fewer than 100 calories from added sugars per 12-ounce serving ahead of its original 2025 target. This milestone was driven largely by reformulation programs in China, Saudi Arabia, and India, where erythritol- and xylitol-based blends were deployed to preserve viscosity and sweetness curves in reduced-sugar colas, sports drinks, and flavored waters. Polyols are increasingly valued not as primary sweeteners, but as structural components that replace the bulking function of sucrose in low-calorie liquids.

Ingredient suppliers are responding with integrated systems rather than single ingredients. Ingredion’s late-2025 launch of Dulcent™ sweetener solutions illustrates this trend, combining erythritol with Reb M stevia to replace aspartame and Ace-K while maintaining comparable cost-in-use. This innovation aligns with consumer data from 2025 indicating that 72% of global consumers are actively reducing sugar intake, yet remain sensitive to aftertaste and texture degradation in beverages.

Sustainability considerations are reinforcing adoption. Cargill’s EverSweet®, produced via precision fermentation and expanded across the EU in 2025, delivers an estimated 81% reduction in greenhouse gas emissions compared to conventional sugar. This resonates with the 64% of consumers who now rank environmental impact alongside naturality when evaluating beverage ingredients, positioning polyol-stevia systems as both nutritionally and environmentally defensible.

Enhanced Risk Mitigation and Safety Validation in Erythritol Supply Chains

Following the high-profile 2023 Witkowski et al. publication linking erythritol consumption to cardiovascular risk markers, the polyols market entered a phase of heightened scientific scrutiny and reputational risk management. Rather than triggering a structural exit from erythritol, the response from manufacturers and regulators has been characterized by dosage optimization, expanded clinical review, and portfolio diversification.

In January 2025, the U.S. International Trade Commission noted that while short-term consumption patterns fluctuated after the 2023 headlines, erythritol remained a core industrial input across tabletop sweeteners, beverages, and pharmaceuticals. FDA internal reviews cited limitations in causal inference within the original study, stabilizing erythritol’s GRAS positioning and supporting its continued use in granular sweetener formats. As of late 2024, the U.S. tabletop erythritol segment alone was valued at approximately USD 145.3 million, underscoring the molecule’s entrenched commercial role.

At the same time, producers are actively reducing dependency on any single polyol. D-Allulose has emerged as a strategic hedge. In July 2025, China’s National Health Commission formally approved D-Allulose as a new food material with a recommended daily intake cap of 20 grams. This regulatory approval has catalyzed immediate downstream investment, particularly in Asia. Ingredient suppliers such as BSH Ingredients are now developing polyol-allulose co-crystal systems for bakery and confectionery applications, allowing brands to balance sweetness intensity, glycemic response, and safety perception within a single formulation platform.

Low-Glycemic, Fiber-Enhancing Bakery and Snack Formulations

The convergence of metabolic health awareness, GLP-1 drug adoption, and demand for indulgent yet permissible foods has created a premium growth corridor for polyols in bakery and snack formulations. Polyols such as maltitol, isomalt, and polydextrose are increasingly positioned as functional carbohydrates that deliver sweetness, fiber-like behavior, and process stability rather than as simple sugar substitutes.

In 2025, major FMCG players including Mondelez International and General Mills expanded health-forward snack portfolios that rely on isomalt to control moisture migration and crystallization in sugar-free cookies and biscuits. These formulations enable “low-glycemic” and “high-fiber” claims while preserving browning and crunch, a technical hurdle that has historically limited sugar reduction in baked goods. Bakery and confectionery already account for approximately 38.4% of global sweetener demand, making this segment the single largest volume opportunity for advanced polyol systems.

Supply-side investments are reinforcing this opportunity. Cargill’s 60% expansion of its Deventer facility in the Netherlands in 2025 was specifically aimed at low-sugar chocolate coatings and fillings. By leveraging polyols with tailored thermal and hygroscopic profiles, Cargill has enabled sugar reductions of up to 50% while achieving improved Nutri-Score ratings, without compromising mouthfeel or shelf stability.

High-Growth Penetration in Gummy-Format Nutraceuticals

The nutraceutical sector’s transition from tablets to chewable and experiential formats has created one of the fastest-growing demand pockets for polyols. Gummies, chewables, and orally disintegrating formats rely on polyols such as sorbitol, mannitol, and xylitol to provide bulk, structural integrity, and non-cariogenic properties without triggering insulin spikes.

With the global pharmaceutical excipients market projected to reach USD 10.96 billion in 2025, polyols are capturing an increasing share of the functional delivery sub-segment. Suppliers such as Evonik and BASF have prioritized pharmaceutical-grade polyols, supported by BASF’s GMP Solution Centre opened in June 2025, to serve nutraceutical and OTC manufacturers seeking consistent particle size, low hygroscopicity, and regulatory-grade purity.

Demographic trends are further accelerating adoption. Clinical preference data from October 2025 indicates strong uptake of gummy and liquid supplements among geriatric and pediatric populations. Polyols, particularly xylitol, are being favored in diabetic-friendly vitamin D, calcium, and omega-3 gummies due to their low glycemic response and dental health benefits. This positions polyols not just as sweeteners, but as enabling excipients at the intersection of nutrition, compliance, and patient experience.

Polyols Sweeteners Market Share and Segmentation Insights

Sorbitol Leads Polyol Sweetener Production Due to Cost Efficiency and Versatile Industrial Applications

Sorbitol accounted for 42.80% of the Polyols Sweeteners Market by product type in 2025, reflecting its widespread use as a bulk sweetener, humectant, pharmaceutical excipient, and chemical intermediate across multiple industries. Produced primarily through hydrogenation of glucose derived from corn wet milling, sorbitol benefits from established global production infrastructure and cost-effective feedstock availability. Its multifunctional properties make it suitable for sugar-free confectionery, oral care formulations, pharmaceutical tablets, and cosmetic products. In 2025, integrated sorbitol production within corn processing complexes is strengthening supply chain efficiency, allowing manufacturers to optimize production costs through energy integration and co-product utilization while maintaining sorbitol's pricing advantage over alternative polyol sweeteners.

Food and Beverage Industry Drives Polyol Sweetener Demand in Sugar Reduction Formulations

Food and beverages represented 58.60% of the Polyols Sweeteners Market by application in 2025, driven by the growing global demand for reduced sugar and sugar-free food products. Polyols such as sorbitol, erythritol, xylitol, and maltitol are widely used in chewing gum, sugar-free confectionery, baked goods, ice cream, and beverage formulations due to their ability to provide sweetness, bulk, and texture while reducing caloric content. Increasing consumer awareness of sugar intake and rising prevalence of lifestyle diseases continue to support polyol adoption in modern food product development. In 2025, clean label sweetener positioning is strengthening market demand, with polyols benefiting from their natural occurrence in fruits and vegetables, allowing food manufacturers to promote reduced sugar formulations while maintaining recognizable ingredient profiles.

Polyols Sweeteners Market Competitive Landscape

The global polyols sweeteners market is rapidly evolving toward low-glycemic, clean-label sugar alcohols and fermentation-derived ingredients. Competitive dynamics are shaped by GLP-1-driven dietary trends, erythritol-stevia synergies, and demand for dental-friendly, low-calorie sweeteners across functional foods, nutraceuticals, and pharmaceutical applications.

Roquette Strengthens Specialty Polyols Leadership with SweetPolyol™ and Pharma Integration

Roquette Frères is reinforcing its leadership in the polyols sweeteners market through its "Shift & Lead" strategy focused on plant-based, high-value ingredients. The company reported €4.88 billion in 2025 revenue with an 8% growth, supported by a disciplined shift toward specialty polyols and a 12.6% EBITDA margin. Its acquisition of IFF Pharma Solutions enhances its position in pharmaceutical excipients using polyol-based formulations. The SweetPolyol™ portfolio is being optimized for premium applications such as crystalline maltitol in sugar-free chocolate, ensuring superior mouthfeel and digestive tolerance. Roquette continues to invest in sustainable processing infrastructure across Europe and North America. Strategy centers on high-purity polyols, pharma-grade integration, and premium sugar reduction solutions.

Cargill Expands Functional Polyol Applications with India-Centric Innovation and Supply Chain Strength

Cargill is leveraging its global supply chain and innovation ecosystem to expand polyol applications in functional foods and emerging markets. Through its Gurgaon Innovation Center, the company is developing erythritol and sorbitol blends that reduce oil absorption while maintaining taste and texture in snacks. Its AAHAR showcase highlighted polyol-based bakery and confectionery solutions targeting value-conscious consumers. Products such as Gemini Plus systems and NatureFresh Professional leverage polyols as humectants to extend shelf life in sugar-reduced foods. Cargill remains a dominant supplier of liquid sorbitol for oral care and personal care applications. Strategy focuses on application-driven innovation, emerging market expansion, and functional ingredient systems.

ADM Enhances Polyol Efficiency with Digital Manufacturing and GLP-1 Aligned Nutrition Systems

ADM is advancing its polyols business through operational efficiency and digital transformation within its Carbohydrate Solutions segment. The company reported 2025 EPS of $3.43 and expects improved performance in 2026, supported by rising demand for reduced-calorie sweeteners. Its cost optimization program aims to generate up to $750 million in savings, partially reinvested into advanced polyol production technologies. ADM’s Fibrosol® and polyol-based fiber systems are positioned to address GLP-1-driven dietary shifts by reducing caloric intake while maintaining satiety. The company’s long-standing dividend growth reflects strong financial resilience. Strategy emphasizes process optimization, functional nutrition, and scalable polyol solutions.

Tate & Lyle Drives Next-Gen Sweetener Systems with Yume™ and GLP-1 Consumer Insights

Tate & Lyle is redefining the polyols sweeteners landscape through its focus on "permissible indulgence" and next-generation sweetener systems. The launch of Yume™, in partnership with Manus, introduces stevia-polyol synergistic solutions targeting premium sugar reduction. Its acquisition of CP Kelco strengthens its ability to combine polyols with texturants, delivering full sugar-like mouthfeel in reduced-calorie products. Proprietary GLP-1 research indicates a 2.5x higher adoption of healthier diets, guiding product innovation toward satiety-focused formulations. With operations in over 120 countries, Tate & Lyle provides global formulation support. Strategy centers on sweetener synergy, texture optimization, and health-driven product design.

Südzucker (BENEO) Dominates Isomalt Segment with Vertical Integration and Functional Nutrition Focus

Südzucker AG, through its BENEO brand, is a global leader in functional polyols, particularly isomalt. The company reported €6.36 billion in revenue for the first nine months of FY2025/26, with its Special Products segment driving growth. BENEO’s isomalt, derived from beet sugar, offers a zero-glycemic index and is widely used in sugar-free confectionery, including 90% of hard candies globally. Südzucker’s vertically integrated supply chain ensures control from raw material sourcing to final polyol production. The company is increasingly focusing on medical nutrition and customized functional ingredients to enhance margins. Strategy emphasizes functional health benefits, vertical integration, and specialty ingredient leadership.

Jungbunzlauer Leads Clean-Label Erythritol Innovation with ERYLITE® and Fermentation-Based Production

Jungbunzlauer Suisse AG is the industry leader in non-GMO, fermentation-derived erythritol, setting the benchmark for clean-label polyols. Its ERYLITE® portfolio, including the recently launched ERYLITE® Bronze, provides natural sugar alternatives with zero glycemic index and high digestive tolerance. The company’s fermentation-based production ensures regulatory compliance and GRAS approval across major global markets. Jungbunzlauer emphasizes erythritol’s synergy with high-intensity sweeteners like stevia for balanced sweetness profiles. Its sustainability initiatives focus on bio-based feedstocks and reduced carbon footprint manufacturing. Strategy centers on clean-label innovation, fermentation technology, and global regulatory leadership.

France: Formulation-Led Innovation and Regulatory-Driven Polyol Adoption

France represents a structurally advanced and regulation-responsive market within the polyols sweeteners industry, driven by formulation innovation, sugar tax dynamics, and sustainability-led manufacturing upgrades. In April 2024, Roquette Frères completed a flagship capacity expansion at its Lestrem site, significantly increasing output of maltitol and crystalline sorbitol to meet rising demand from European confectionery, bakery, and sugar-reduced food applications. Building on this scale-up, Roquette introduced Lycasin® HBC in 2025, a next-generation maltitol syrup engineered for hard-boiled candies and sugar-free gummies, offering improved tooth-friendliness and lower caloric contribution while maintaining process stability during high-temperature cooking.

Beyond confectionery, collaborative innovation is shaping broader polyol usage. BENEO, with substantial French operations, launched a 2025 research consortium with European bakers to optimize isomalt performance in high-fiber and reduced-sugar artisanal baked goods. Regulatory alignment remains a key market accelerator. French manufacturers are actively reformulating products to improve Nutri-Score ratings, leveraging xylitol and erythritol to reduce total sugar-equivalent carbohydrates and move products from Grade C or D into A or B classifications. On the manufacturing side, French sorbitol plants implemented closed-loop hydrogen recovery systems in late 2024, cutting the carbon footprint of hydrogenation processes by an estimated 12%. Beverage reformulation is also pronounced, with more than 65% of new drink launches in 2025 utilizing erythritol-stevia blends to remain below national Soda Tax thresholds. Collectively, France’s market is characterized by premium polyol applications tightly aligned with labeling, health policy, and low-carbon production priorities.

United States: Labeling Reform, Trade Policy, and Medical-Grade Polyol Demand

The United States polyols sweeteners market in 2025 is undergoing a structural shift driven by regulatory redefinition, trade realignment, and expanding pharmaceutical applications. On January 16, 2025, the U.S. Food and Drug Administration issued a revised definition for “Healthy” food claims, sharply limiting added sugars and prioritizing nutrient density. This regulatory change has triggered a rapid pivot toward erythritol and allulose as primary bulking agents in snacks, beverages, and nutrition products. Momentum intensified further in May 2025 with the FDA’s proposed Front-of-Package labeling framework, which highlights high sugar content and incentivizes manufacturers to keep added sugars within the “Low” threshold of 5% daily value using polyol-based reformulation.

On the supply side, investment and trade dynamics are reshaping sourcing strategies. ADM reported in 2025 that a growing share of its capital expenditure is being redirected toward precision fermentation platforms aimed at lowering the cost of bio-based erythritol. Meanwhile, the U.S. International Trade Commission finalized its erythritol anti-dumping investigation in early 2025, resulting in duty adjustments that strengthened the competitiveness of domestic production, including operations at Cargill’s Blair, Nebraska facility. Product innovation remains active, with Cargill’s EverSweet™ plus erythritol platform enabling zero-calorie sweetness profiles with full sugar-like taste. Beyond food and beverage, pharmaceutical demand is rising sharply, as U.S. drug manufacturers increased procurement of spray-dried mannitol in 2025 for orally disintegrating tablets, reinforcing the country’s role as a high-value, multi-sector polyol consumption market.

India: Domestic Capacity Expansion and Oral Care-Led Polyol Penetration

India’s polyols sweeteners industry is experiencing rapid structural growth, supported by domestic manufacturing investment, regulatory tightening, and strong downstream demand from oral care and pharmaceuticals. In January 2025, Gulshan Polyols commissioned a new hydrogenation facility dedicated to 70% liquid sorbitol and maltitol syrup, targeting domestic toothpaste, oral hygiene, and pharmaceutical formulations. This capacity expansion aligns with India’s position as a global hub for polyol-based oral care, where sorbitol penetration reached approximately 85% in the premium gel toothpaste segment by late 2025.

Regulatory clarity is reinforcing compliant growth. The Food Safety and Standards Authority of India implemented Version XI of its Prohibition and Restrictions on Sales regulations in April 2025, tightening labeling requirements for sugar-free and reduced-sugar foods containing polyols. Policy support is also material. Under the Production Linked Incentive scheme, the Indian government allocated ₹3,000 crore during 2024 to 2025 to promote domestic production of critical chemical intermediates, directly benefiting local sorbitol and mannitol manufacturers. Export competitiveness is strengthening, with Indian producers reporting a 15% year-on-year increase in sorbitol shipments to Middle East and Africa markets in the 2024 to 2025 fiscal year. Environmental compliance is now non-negotiable, as all new polyol facilities in Gujarat and Maharashtra are required to operate under Zero Liquid Discharge norms introduced in 2025, positioning India as a cost-competitive yet regulation-aligned production base.

China: Scale Leadership, Health Campaigns, and Digital Traceability

China remains the largest and most systemically influential market in the global polyols sweeteners industry, with 2025 marked by regulatory streamlining, health policy alignment, and digital oversight. Under Announcement No. 3 of 2025, the National Health Commission approved eleven new food items, simplifying regulatory pathways for specialty sweetener blends incorporating rare polyols. Despite tariff barriers in certain export destinations, China continues to dominate global erythritol supply. Leading producers such as Baolingbao Biology upgraded facilities in 2025 to manufacture Non-GMO Project Verified crystalline erythritol, targeting premium export markets.

Domestic demand is being reinforced by national health initiatives. The government’s Three Reductions campaign mandates a 15% sugar reduction in school-targeted snacks by 2026, directly accelerating polyol adoption in mass-market food categories. Sustainability and compliance requirements are also tightening. Under the 2025 Green Packaging roadmap, polyol manufacturers are transitioning away from plastic drums toward fully recyclable IBCs and paper-based bulk packaging for crystalline exports. Since May 2025, mandatory QR-code batch traceability has been enforced across major sweetener producers, requiring disclosure of corn or wheat feedstock origin and enzyme safety data. These measures underscore China’s evolution toward transparent, health-aligned, and export-oriented polyol production at scale.

Iran and West Asia: Emerging Regional Self-Sufficiency in Sorbitol

Iran and the broader West Asian region are entering a new phase of polyols production focused on import substitution and pharmaceutical integration. In January 2025, the first world-scale sorbitol production facility in West Asia was commissioned in Tehran, with an annual capacity of 7,500 tons of 70% liquid sorbitol. This facility is strategically aligned with national objectives to localize excipient supply and reduce dependence on imported pharmaceutical ingredients.

The project supports the Iranian Ministry of Health’s stated goal of cutting pharmaceutical-grade excipient imports by 40% by 2027. By anchoring sorbitol production domestically, the region is laying the foundation for broader polyol adoption across pharmaceuticals, oral care, and food processing. Although still at an early stage compared to mature markets, Iran’s entry into large-scale sorbitol manufacturing signals a gradual shift toward regional self-sufficiency in polyol sweeteners.

Comparative Overview of Country-Level Dynamics in the Polyols Sweeteners Industry

Polyols Sweeteners Market County Level Snapshot

|

Country / Region

|

Core 2024–2025 Focus Areas

|

Implications for Polyols Sweeteners

|

|

France

|

Confectionery reformulation, Nutri-Score optimization, low-carbon sorbitol

|

Premium demand for maltitol, xylitol, and erythritol

|

|

United States

|

FDA labeling reform, trade protection, pharma excipients

|

Strong growth in erythritol, allulose, and mannitol

|

|

India

|

Oral care dominance, domestic hydrogenation, export growth

|

Rising sorbitol and maltitol production and exports

|

|

China

|

Health campaigns, digital traceability, export scale

|

Sustained leadership in erythritol and specialty polyols

|

|

Iran & West Asia

|

Import substitution, pharma integration

|

Emerging regional demand for pharmaceutical-grade sorbitol

|

Polyols Sweeteners Market Report Scope

Polyols Sweeteners Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.6 Billion

|

|

Market Size (2034)

|

$12.2 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Sorbitol, Erythritol, Xylitol, Maltitol, Mannitol, Isomalt, Lactitol & Other Polyols), By Form (Powder & Crystalline, Liquid & Syrup), By Function (Sweetening Agents, Bulking Agents, Humectants & Stabilizers, Pharmaceutical Excipients), By Application (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Roquette Frères SA, Cargill Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, BENEO GmbH, Tereos Starch & Sweeteners Europe, Gulshan Polyols Ltd., Südzucker AG, Baolingbao Biology Co. Ltd., Jungbunzlauer Suisse AG, B Food Science Co. Ltd., CSPC Shengxue Glucose Co. Ltd., Mitsubishi Corporation Life Sciences Ltd., Hebei Huaxu Pharmaceutical Co. Ltd., DHW Deutsche Hydrierwerke GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyols Sweeteners Market Segmentation

By Product Type

- Sorbitol

- Erythritol

- Xylitol

- Maltitol

- Mannitol

- Isomalt

- Lactitol & Other Polyols

By Form

- Powder & Crystalline

- Liquid & Syrup

By Function

- Sweetening Agents

- Bulking Agents

- Humectants & Stabilizers

- Pharmaceutical Excipients

By Application

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyols Sweeteners Industry

- Roquette Frères SA

- Cargill Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- BENEO GmbH

- Tereos Starch & Sweeteners Europe

- Gulshan Polyols Ltd.

- Südzucker AG

- Baolingbao Biology Co. Ltd.

- Jungbunzlauer Suisse AG

- B Food Science Co. Ltd.

- CSPC Shengxue Glucose Co. Ltd.

- Mitsubishi Corporation Life Sciences Ltd.

- Hebei Huaxu Pharmaceutical Co. Ltd.

- DHW Deutsche Hydrierwerke GmbH

*- List not Exhaustive