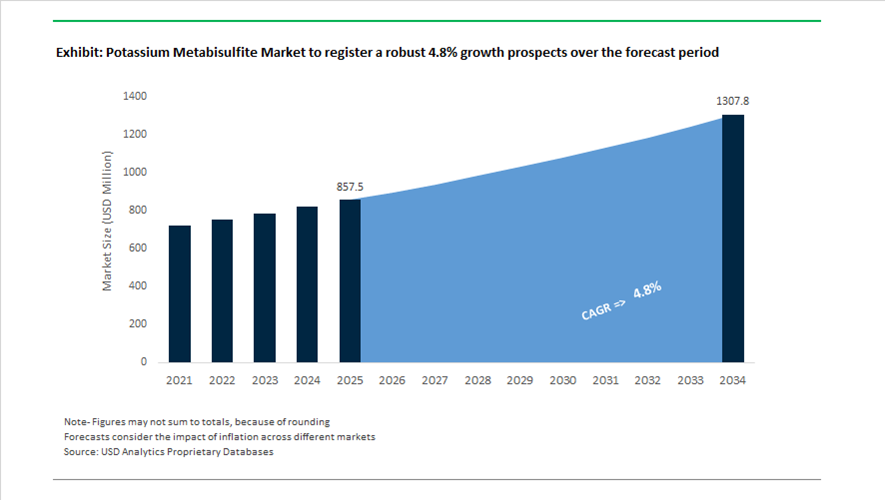

Potassium Metabisulfite Market Valued at $857.5 Million in 2025, Forecast to Reach $1,307.6 Million by 2034 at 4.8% CAGR

The global potassium metabisulfite market is valued at $857.5 million in 2025 and is projected to reach $1,307.6 million by 2034, expanding at a CAGR of 4.8%. Growth is supported by rising demand for food-grade preservatives, wine stabilizers, water treatment chemicals, pharmaceutical antioxidants, and specialty reducing agents across food processing, beverage exports, API stabilization, and industrial cleaning applications. A structural shift toward sodium-reduced food formulations between 2024 and 2026 has accelerated substitution of sodium bisulfite with potassium metabisulfite, enabling manufacturers to maintain antimicrobial and antioxidant efficacy while meeting low-sodium labeling requirements in juices, dried fruits, and winemaking.

Market consolidation remains pronounced. As of 2025, the five largest producers, including BASF, Esseco Srl, and Aditya Birla Group, collectively account for approximately 65% of global market share. Rather than pursuing large-scale mergers, leading players have emphasized contract manufacturing collaborations and portfolio integration to manage input cost volatility in sulfur derivatives. In 2025, Grasim Industries, the chemical arm of Aditya Birla Group, deepened integration of potassium metabisulfite production with its chlor-alkali and sulfur-derivative operations, optimizing internal supply chains for APAC food and beverage customers. Throughout 2025, Latin America emerged as a high-growth region, with Brazil and Mexico reporting strong demand driven by municipal water-cleaning programs and a surge in craft beverage exports. Brazilian imports increased by more than 8% in 2024, signaling tightening domestic supply.

Regulatory refinement is shaping application standards. In August 2025, China’s National Health Commission issued updated notifications refining permitted usage levels for sodium and potassium metabisulfite in food additives to align with international safety benchmarks. This development enhances clarity for exporters targeting Chinese markets. In early 2025, several European suppliers introduced eco-optimized packaging formats designed to reduce moisture absorption and extend shelf stability for small-scale wineries, addressing spoilage losses during storage. In 2025, manufacturers such as Shakti Chemicals and Jay Dinesh Chemicals launched high-purity crystalline grades tailored for pharmaceutical use, particularly for API stabilization and vaccine production, where sulfite-based antioxidants protect sensitive compounds from oxidative degradation.

Sustainability and digital transformation initiatives are influencing production economics. In late 2025 and early 2026, BASF advanced its “Winning Ways” strategy, positioning sulfiting agents within its broader green transformation agenda and increasing renewable energy usage at sites such as Ludwigshafen. In January 2026, BASF opened a global Digital Hub in Hyderabad to enhance supply chain transparency and standardized digital services across its specialty chemicals portfolio, including preservative distribution. At Plastindia 2026 in February, producers highlighted refinements in sulfite-based stabilizers to extend the service life of agricultural plastics while minimizing soil leaching. By early 2026, research expanded into electronic cleaning fluids leveraging potassium metabisulfite’s reducing properties without metallic residue formation, opening niche opportunities in high-precision circuit board manufacturing.

The potassium metabisulfite market is increasingly defined by low-sodium food preservation, pharmaceutical-grade sulfite stabilization, regulatory alignment in China, Latin American water-treatment demand, sustainable production initiatives, and emerging electronics cleaning applications. Consolidated supply structures, sulfur-derivative integration strategies, and application diversification are shaping competitive positioning across food, pharma, water treatment, and specialty industrial segments.

Trends and Opportunities in the Potassium Metabisulfite (KMS) Market

Mandated Transparency and Regulatory Risk Mitigation in Enology

The global wine industry remains the single largest demand center for potassium metabisulfite, accounting for close to 55% of total consumption, but its usage profile is undergoing a fundamental transformation. Regulatory scrutiny around sulfites has shifted KMS from a routine preservative to a precision-managed processing aid. The emphasis is no longer on volume usage but on dosing accuracy, residue control, and traceable compliance to meet evolving consumer expectations for low-sulfite and clean-label wines.

A major inflection point occurred with the full enforcement of the European Union Regulation 2024/1143 in January 2025. All wines produced from the 2024 harvest onward must now disclose a complete ingredient list and nutritional information, typically through digital QR-code labeling. This regulatory shift has materially increased demand for high-purity, low-residue potassium metabisulfite grades, as winemakers seek to minimize declared sulfite levels while preserving microbial stability and oxidative protection. Industry benchmarks indicate that producers are increasingly targeting optimized sulfite concentrations in the 50–150 ppm range, driving tighter quality specifications for KMS suppliers.

At the same time, the maturation of the natural wine segment has created a clear bifurcation in demand. While sulfite-free wines have gained visibility in boutique and local markets, export-oriented and mass-market producers continue to rely on potassium metabisulfite as a non-negotiable stabilizer to ensure product integrity during long-haul transportation. This divergence has strengthened demand for standardized, export-grade KMS in high-volume wine-producing regions, reinforcing its role as a compliance-critical input rather than a discretionary additive.

Strategic Adoption in Hydrometallurgy and Mineral Processing

Beyond food and beverage applications, potassium metabisulfite is gaining strategic importance in hydrometallurgy and mineral processing, particularly in gold and copper extraction. In these applications, KMS is increasingly favored over sodium-based reducing agents due to its ability to control redox reactions without introducing excess sodium ions that can disrupt downstream processing circuits.

Industrial data from mid-2025 shows rising adoption of potassium metabisulfite in secondary gold refining, especially within e-waste recycling operations across Southeast Asia and India. In aqua regia refinement, KMS is being used as a safer and more controllable alternative to sulfur dioxide gas for gold precipitation. This shift reduces handling risks, improves dosing accuracy, and aligns with tighter workplace safety standards in small-to-mid-scale refining facilities.

In copper leaching, potassium metabisulfite is being integrated into modern hydrometallurgical circuits to manage oxidation states in increasingly complex ore bodies. Operational reports following production disruptions at major global mines in 2025 highlighted the need for flexible reducing agents capable of maintaining recovery rates despite declining ore grades. KMS has emerged as a valuable process stabilizer in these systems, supporting efficient metal recovery while improving control over leach chemistry.

Stabilizer for High-Purity Pharmaceutical and Vitamin Synthesis

The pharmaceutical and nutraceutical sectors represent a structurally attractive growth opportunity for potassium metabisulfite, driven by rising demand for oxidation-sensitive APIs and liquid formulations. In these applications, KMS functions as a reductive stabilizer, protecting active ingredients from degradation and extending shelf life under stringent regulatory oversight.

In April 2025, pharmaceutical ingredient manufacturers in Gujarat, India, reported a measurable increase in demand for pharma-grade potassium metabisulfite. It is now widely used at concentrations ranging from 0.1% to 0.5% in liquid formulations containing ascorbic acid and other oxidation-prone compounds. This application is particularly critical in vitamin syrups, injectables, and oral solutions, where KMS enables consistent product stability exceeding 24 months without compromising safety or efficacy.

Further reinforcing this opportunity, late-2024 research highlighted potassium metabisulfite’s role as a mild and controllable reducing agent in complex organic synthesis. Its ability to release sulfur dioxide in a predictable, pH-dependent manner allows manufacturers to stabilize oxygen-sensitive intermediates during critical reaction stages. This precision makes KMS well suited for specialty pharmaceutical manufacturing, where batch-to-batch consistency and impurity control are essential for regulatory approval.

Scaling of Emergency and Mobile Water Purification Systems

Climate-driven disasters, geopolitical instability, and infrastructure stress are creating a growing readiness-driven market for potassium metabisulfite in emergency water treatment. Its dual functionality as an oxygen scavenger and dechlorinating agent positions KMS as a key chemical in portable and mobile purification systems.

During severe flooding events in Sumatra in December 2025, the deployment of mobile reverse osmosis units highlighted the operational importance of potassium metabisulfite in water treatment workflows. KMS was used to neutralize residual chlorine following disinfection, preventing off-tastes in drinking water while protecting RO membranes from oxidative damage. This application has gained traction among disaster-response agencies seeking rapid, scalable water purification solutions.

Military and humanitarian logistics further underscore this opportunity. In 2025, defense forces and non-governmental organizations in Southeast Asia reported increased use of KMS-based dechlorination tablets in emergency response kits. These systems allow for high-dose chlorination to eliminate pathogens, followed by rapid neutralization with potassium metabisulfite, enabling the production of potable water within 30 minutes from contaminated sources. As disaster preparedness budgets expand globally, demand for compact, chemically robust water treatment solutions is expected to remain a durable growth driver for the KMS market.

Potassium Metabisulfite Market Share and Segmentation Insights

Food Grade Potassium Metabisulfite Leads Global Demand in Food Preservation and Winemaking

Food grade potassium metabisulfite accounted for 52.80% of the Potassium Metabisulfite Market by grade in 2025, driven by its critical role in food preservation and beverage processing applications that require strict purity and safety standards. The compound is widely used as an antimicrobial preservative and antioxidant in winemaking, dried fruits, fruit juices, and processed foods where oxidation control and microbial stability are essential. Regulatory approvals such as GRAS status in major markets support widespread adoption across the food industry. In 2025, growing consumer awareness of sulfite sensitivity has influenced labeling regulations, prompting food manufacturers to ensure transparent labeling while continuing to rely on potassium metabisulfite in applications where its preservation efficiency and oxidation control remain essential for product stability.

Winemaking Industry Drives Potassium Metabisulfite Consumption in Global Beverage Production

Winemaking represented 42.80% of the Potassium Metabisulfite Market by application in 2025, reflecting the compound’s essential role in modern enology practices. Potassium metabisulfite is used throughout the winemaking process to inhibit unwanted microbial activity, prevent oxidation, and stabilize finished wine products during storage and distribution. The global scale of wine production and the need for consistent product quality continue to support strong demand for sulfite-based preservation systems. In 2025, precision sulfite management technologies are increasingly adopted in wineries, with automated dosing systems and real time monitoring of free sulfur dioxide enabling winemakers to optimize sulfite levels while maintaining microbial stability and preserving wine aroma and color characteristics.

Potassium Metabisulfite Market Competitive Landscape

The global potassium metabisulfite market in 2026 is evolving toward high-purity, low-dust, and microencapsulated formulations. Growth is driven by food-grade preservatives, pharmaceutical stabilizers, and premium wine production, with manufacturers focusing on Verbund integration, SO₂ stability control, and regulatory-compliant clean label solutions.

BASF Strengthens High-Purity Sulfur Integration with Zhanjiang Verbund Expansion

BASF maintains a dominant position in the potassium metabisulfite market through its fully integrated Verbund production model, ensuring consistent quality and cost efficiency. The company reported €59.7 billion in 2025 sales and is targeting €6.2–€7.0 billion EBITDA in 2026 under its “Winning Ways” strategy. The Zhanjiang Verbund site startup in 2026 significantly enhances regional supply of high-purity inorganic sulfur chemicals across Asia-Pacific. BASF’s control over SO₂ synthesis and downstream potassium absorption ensures ultra-low impurity levels, making it a preferred supplier for pharmaceutical-grade stabilizers and food preservatives. Its strategic reorganization of catalysts and chemicals improves supply chain resilience for potassium derivatives. The company’s scale, integration, and regulatory compliance position it as a benchmark in precision sulfur chemistry.

Esseco Drives Circular Sulfur Chemistry with ECOChem Innovations and Oenology Leadership

Esseco Group is a specialized leader in potassium metabisulfite, focusing on circular economy integration and energy-efficient sulfur processing. Its ECOChem Innovations initiative captures CO₂ emissions and converts them into bicarbonates, reducing environmental impact while enhancing process efficiency. Through its Enartis division, Esseco dominates the wine additives market with advanced granular potassium metabisulfite that minimizes dust exposure and improves solubility. The company serves over 15 industrial applications, including textiles, mining, and water treatment, with a diversified sulfur derivative portfolio. Its 2030 sustainability roadmap targets a 30% reduction in energy intensity across production sites. Esseco’s focus on oenology-grade purity and sustainable manufacturing strengthens its competitive positioning in premium applications.

Aditya Birla Chemicals Leads Global Sulfite Supply with Export-Driven Scale and Raw Material Integration

Aditya Birla Chemicals (Thailand) is the world’s largest producer of powdered sulfites, playing a critical role in the global potassium metabisulfite supply chain. Its Thailand-based facility supports over 70% export output, serving more than 90 countries across food, mining, and water treatment industries. The company benefits from strong backward integration through its chlor-alkali operations, ensuring stable access to key raw materials. Its product portfolio spans sodium and potassium metabisulfites tailored for high-volume industrial and preservative applications. Expansion into advanced materials and sustainable technologies enhances its ESG positioning and global reach. Its scale, cost efficiency, and supply reliability make it a key exporter in the Asia-Pacific market.

IOCL Expands Industrial and Oilfield Applications with Customized Sulfite Blending Capabilities

Imperial Oilfield Chemicals (IOCL) is strengthening its niche in industrial-grade potassium metabisulfite, particularly for oilfield and water treatment applications. The company focuses on oxygen scavenging solutions for boiler systems and drilling fluids, preventing corrosion in high-pressure environments. Its 2026 strategy emphasizes digital logistics and enhanced track-and-trace capabilities to improve supply chain transparency. IOCL has expanded custom blending services to cater to specialized applications in textile dyeing and photographic chemicals requiring precise pH control. The company maintained stable utilization rates in 2025 despite volatile commodity markets, demonstrating operational resilience. Its targeted approach to industrial applications supports steady growth in high-demand sectors.

Brenntag Enhances Global Distribution with Regulatory Compliance and Value-Added Specialty Services

Brenntag plays a pivotal role in the potassium metabisulfite market as a leading global distributor, focusing on specialty chemicals and life sciences applications. Its dual-division model supports tailored solutions for food, beverage, and pharmaceutical customers requiring high-purity preservatives. The company expanded its footprint through strategic acquisitions in Latin America and Southeast Asia, strengthening last-mile delivery capabilities. Brenntag provides micro-packaging and dosing solutions for SMEs, particularly in wine and beer production, improving handling safety and efficiency. Its leadership in regulatory compliance ensures adherence to REACH and FDA standards across global markets. By combining logistics expertise with technical services, Brenntag enhances accessibility and quality assurance for specialty sulfite products.

Kertis Chemicals Targets Clean Label and Pharma-Grade Growth with Advanced Crystallization Technology

Kertis Chemicals is emerging as a competitive mid-tier player by focusing on high-purity, clean label potassium metabisulfite formulations. The company introduced a stabilized solution in 2025 that reduces SO₂ odor, improving usability in consumer-facing food and beverage applications. Its strategic emphasis on pharma-grade (BP/USP/EP) products aligns with growing demand for stable antioxidants in drug manufacturing. Kertis expanded its regional presence in Eastern Europe and South Africa to support emerging wine production markets. Its proprietary crystallization process improves particle uniformity and extends shelf-life stability by 20% in dry food applications. This focus on purity, stability, and niche innovation enables Kertis to compete effectively in specialized segments.

Germany: Supply Chain Realignment and Compliance-Driven Grade Upgrading

Germany’s potassium metabisulfite landscape in 2025 is defined by a structural supply reset and tighter regulatory oversight. In September 2025, BASF announced its strategic exit from hydrosulfites and related sulfur-based reducing agents, including the closure of dedicated assets in Ludwigshafen. This decision has triggered immediate supply chain realignment for European wine, food processing, and textile buyers, with procurement shifting toward imports amid reduced domestic availability. Despite the exit, BASF continues to invest in adjacent innovation. Its 2025 Research Press Briefing highlighted ongoing work on X3D catalyst shaping, which improves efficiency for sulfur-based intermediates used downstream, indirectly supporting process optimization across the value chain.

Regulatory and cost pressures are simultaneously reshaping demand. The German Federal Environment Agency updated effluent guidelines in 2025, mandating lower residual sulfite levels in neutralized industrial discharge, increasing compliance costs for technical-grade usage. Pharmaceutical demand is moving the market up the value curve, with specialty chemical suppliers prioritizing Ph. Eur. grade potassium metabisulfite to support injectable formulations requiring high stability antioxidants ahead of 2026. Elevated natural gas prices during 2024–2025 introduced a temporary surcharge on domestic sulfur derivatives, further favoring imports from North America and Asia. Exporters also implemented the EU 2025/973 Implementing Regulation in May 2025, updating authorization constraints for sulfur-based preservatives in organic production. Collectively, Germany is transitioning toward a smaller, higher-specification market anchored in compliance and pharma-grade quality.

India: Integrated Feedstocks and Expansion into Pharma-Grade Applications

India’s potassium metabisulfite industry in 2025 is characterized by consolidation, feedstock security, and a rapid pivot toward regulated end uses. In February 2025, Gujarat Alkalies and Chemicals Limited completed acquisitions of domestic production assets, consolidating its footprint in the food-grade segment and improving scale economics. Feedstock resilience has strengthened as producers such as Aditya Birla Chemicals integrated sulfur dioxide sourcing directly with regional oil refineries, stabilizing supply quality and reducing volatility for high-purity outputs.

Demand diversification is accelerating. The mining sector recorded a 12% increase in technical-grade potassium metabisulfite usage in 2025 as a reducing agent for cyanide detoxification in precious metals extraction. Food safety regulation is also tightening. The Food Safety and Standards Authority of India introduced clearer sulfite labeling mandates in late 2025 for export-bound preserved fruits and coconut creams, increasing scrutiny on dosage control and traceability. Pharmaceutical demand is rising in parallel, with Jay Dinesh Chemicals and Shakti Chemicals expanding clean-room packaging to serve USP-grade stabilizer requirements in domestic vaccine manufacturing. Environmental compliance is now a baseline expectation, as major Gujarat producers transitioned to Zero Liquid Discharge operations following 2025 audits, reinforcing India’s positioning as a compliant, export-capable supplier.

China: Smart Manufacturing, Market Rebalancing, and Grade Segmentation

China’s potassium metabisulfite market is advancing through smart manufacturing upgrades and strategic export rebalancing. In May 2025, producers in Shandong, including Shandong Minde Chemical, implemented automated smart kiln systems to curb sulfur trioxide emissions during crystallization, improving yield consistency and emissions performance. Pricing dynamics reflected logistical and market shifts, with the domestic price index rising modestly in Q3 2025 as suppliers prioritized higher-margin sales to China’s premium winemaking regions such as Ningxia.

Export conditions are tightening. Increased EU scrutiny and anti-dumping monitoring in 2025 prompted Chinese exporters to redirect volumes toward Southeast Asia and Latin America. At the same time, R&D is opening new value tiers. Late-2024 pilots achieved electronic-grade potassium metabisulfite exceeding 99.9% purity for use as a reducing agent in high-definition display manufacturing. Sustainability frameworks are formalizing. In January 2025, the Ministry of Industry and Information Technology added sulfur-based intermediates to its Green Factory roadmap for 2025–2030, setting benchmarks that favor energy-efficient, low-emission producers. China’s market is thus segmenting by grade, with compliance and specialty applications driving differentiation.

United States: Seasonal Demand Cycles and Emerging Circular Applications

The United States potassium metabisulfite market in 2025 reflects seasonal agricultural demand alongside emerging industrial applications. Price firmness was observed in Q3 2025 due to precautionary restocking by West Coast wineries ahead of harvest, reinforcing the role of viticulture cycles in short-term demand patterns. Supply chains experienced friction early in 2025, leading to a temporary premium on spot-market drums relative to long-term contracts, underscoring the value of contracted procurement for food and beverage processors.

Application breadth is expanding beyond food and wine. The U.S. Department of Energy highlighted the use of metabisulfites as reducing agents in hydrometallurgical lithium-ion battery recycling, where they facilitate cobalt and nickel leaching, positioning potassium metabisulfite within circular economy workflows. Regulatory signaling is also influencing formulation strategies. The FDA’s proposed 2025 revisions to “Healthy” labeling are prompting food processors to optimize sulfite dosages to balance shelf-life performance with clean-label perceptions. These factors position the U.S. as a market where cyclical agricultural demand intersects with technology-driven industrial use.

Italy: Enological Innovation and Precision Sulfite Management

Italy’s potassium metabisulfite market is closely aligned with wine industry innovation and worker safety. In 2025, ESSECO launched a low-dust granular potassium metabisulfite designed to reduce inhalation risks during tank sterilization, addressing occupational health concerns in wineries while maintaining efficacy. This product innovation aligns with broader sector efforts to modernize cellar operations.

Sustainability practices are gaining traction across viticulture. Italian wine associations reported a 20% increase in adoption of integrated sulfite management systems during 2025, using precision dosing to comply with forthcoming EU organic wine standards effective in 2026. These systems reduce total sulfite usage while preserving microbial control and sensory quality. Italy’s market profile is therefore defined by application-specific innovation and compliance-led optimization rather than volume expansion.

Comparative Overview of Country-Level Dynamics in the Potassium Metabisulfite Industry

Potassium Metabisulfite Market County Level Snapshot

|

Country

|

Primary 2025 Focus Areas

|

Implications for Potassium Metabisulfite

|

|

Germany

|

Supply exit, effluent limits, pharma-grade shift

|

Reduced availability, higher-specification demand

|

|

India

|

Consolidation, refinery integration, ZLD compliance

|

Scaled, compliant supply with pharma growth

|

|

China

|

Smart kilns, export rebalancing, electronic grade

|

Grade segmentation and sustainability benchmarking

|

|

United States

|

Seasonal winery demand, battery recycling

|

Cyclical pricing with new circular applications

|

|

Italy

|

Winery safety innovation, precision dosing

|

Value-added products aligned with organic standards

|

Potassium Metabisulfite Market Report Scope

Potassium Metabisulfite Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$857.5 Million

|

|

Market Size (2034)

|

$1307.6 Million

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Grade (Food Grade, Pharmaceutical Grade, Technical Grade, Photo Grade), By Form (Solid, Liquid), By Function (Preservative & Antimicrobial Agent, Antioxidant & Color Stabilizer, Reducing Agent, Bleaching Agent, Sterilizing Agent), By Application (Winemaking, Food Processing, Pharmaceuticals, Water Treatment, Textile Processing, Chemical Synthesis)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ESSECO Srl, Aditya Birla Chemicals, BASF SE, Laffort SA, Imperial Chemical Incorporation, Murphy and Son Ltd., Jay Dinesh Chemicals, Shandong Minde Chemical Co. Ltd., Alkaloid AD Skopje, Triveni Chemicals, Shakti Chemicals, Zibo Baida Chemical Co. Ltd., VWR International, Ever SRL, Advance Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Potassium Metabisulfite Market Segmentation

By Grade

- Food Grade

- Pharmaceutical Grade

- Technical Grade

- Photo Grade

By Form

By Function

- Preservative & Antimicrobial Agent

- Antioxidant & Color Stabilizer

- Reducing Agent

- Bleaching Agent

- Sterilizing Agent

By Application

- Winemaking

- Food Processing

- Pharmaceuticals

- Water Treatment

- Textile Processing

- Chemical Synthesis

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Potassium Metabisulfite Industry

- ESSECO Srl

- Aditya Birla Chemicals

- BASF SE

- Laffort SA

- Imperial Chemical Incorporation

- Murphy and Son Ltd.

- Jay Dinesh Chemicals

- Shandong Minde Chemical Co. Ltd.

- Alkaloid AD Skopje

- Triveni Chemicals

- Shakti Chemicals

- Zibo Baida Chemical Co. Ltd.

- VWR International

- Ever SRL

- Advance Chemical

*- List not Exhaustive