Printable Self-Adhesive Vinyl Films Market Size, Overview, and Growth Outlook (2025–2034)

Printable Self-Adhesive Vinyl Films Market Set to Grow to $5.4 Billion by 2034 on Rising Demand for Fleet Graphics and Sustainable Materials

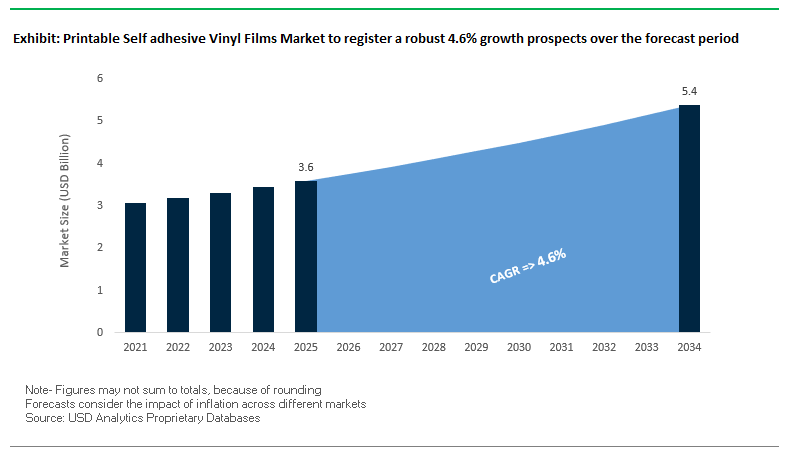

The global printable self-adhesive vinyl films market is projected to increase from $3.6 billion in 2025 to $5.4 billion by 2034, at a CAGR of 4.6%, driven by the rising adoption of fleet graphics, outdoor signage, and promotional applications in developed economies. Fleet branding on commercial vehicles offers a highly visible advertising medium, making durable, vibrant vinyl films an essential choice for marketers. The dominance of calendered films is underpinned by their cost-effectiveness, durability, and ease of handling, while high-performance films with UV resistance and advanced pigments are gaining traction for long-lasting indoor and outdoor graphics.

Key Insights for industry professionals and buyers:

- Fleet Graphics Fuel Demand: High visibility and brand promotion drive volume consumption in the U.S. and Europe.

- Calendered Vinyl Films Remain Dominant: Cost-effective, durable, and ideal for mass-produced signage.

- Shift Toward High-Performance Solutions: Superior color, durability, and UV resistance enhance aesthetic impact.

- Sustainability and Non-PVC Innovation: Growing focus on recyclable, biodegradable, and eco-friendly materials.

- Digital Transformation in Printing: Integration with digital printing technologies supports high customization and faster production.

- Durability and Installation Efficiency: Advanced adhesives and overlaminates ensure longer lifespan and easier application.

Market Analysis: Strategic Acquisitions and Product Innovations Highlight Growth in Printable Self-Adhesive Vinyl Films

The printable self-adhesive vinyl films industry has witnessed several strategic developments to enhance market share and address evolving consumer needs. In August 2025, Avery Dennison Corporation acquired Meridian Adhesives Group's U.S. flooring adhesives business for $390 million, reinforcing its specialty adhesives portfolio and presence in high-value categories. That same month, a Nano Letters study introduced a new ALD-based ultrathin film strategy, potentially improving future nanocoating formulations for high-performance printable films.

Innovation and sustainability have become major focus areas. In March 2025, Arlon Graphics launched its VITAL non-PVC product range, a cast polyurethane film for vehicle wraps, reflecting the industry’s shift toward eco-friendly, high-performance solutions. Earlier, in February 2025, Avery Dennison introduced the AD Stretch accelerator program, partnering with startups to tackle challenges in sustainability, customer experience, and circular material usage. Additionally, companies are increasingly leveraging digital tools to improve business outcomes. In July 2025, 3M published a white paper on Wrap Business Growth, guiding installers on profitability and digital marketing strategies.

Vehicle wrap innovations continue to drive competitive differentiation. In November 2024, 3M launched its Print Wrap Film IJ280, designed for faster installation and minimal lifting, improving efficiency for professional installers. Parallel to this, partnerships like Covestro and PolySource’s June 2025 distribution deal expand material availability for high-performance film production, demonstrating the industry’s focus on supply chain optimization, sustainability, and innovation.

Transformative Trends and Emerging Opportunities in the Printable Self-Adhesive Vinyl Films Market

Accelerated Adoption of Phthalate-Free and Low-VOC Bio-Based Plasticizers

The printable self-adhesive vinyl films market is undergoing a structural shift as regulations and consumer preferences converge toward safer, more sustainable materials. The European Union’s REACH regulation and the U.S. EPA’s VOC standards are driving rapid innovation in alternative plasticizers. A study in ACS Sustainable Chemistry & Engineering showcased bio-based oligoesters with strong compatibility and plasticizing performance, proving viable replacements for ortho-phthalates. This transition is not just regulatory-driven but also demand-led: certifications like the WELL Building Standard prioritize indoor air quality, making phthalate-free, low-VOC vinyl films the preferred choice for interior applications such as wall graphics, murals, and architectural coverings. Brands seeking wellness-focused building certifications are increasingly specifying phthalate-free vinyl products, positioning sustainable formulations as both a compliance necessity and a market differentiator.

Proliferation of Durable, Removable Films for Short-Term Promotional Use

Retailers, event organizers, and advertisers are accelerating adoption of removable vinyl films designed for short-term campaigns. Traditional graphics often leave adhesive residues, requiring costly surface restoration. In contrast, modern acrylic-based adhesive systems, highlighted in an industry guide from Jessup Manufacturing, are engineered with controlled molecular weights that prevent deep surface penetration while maintaining secure adhesion. These films can remain in place for up to 90 days and be removed without residue, aligning perfectly with the fast-paced nature of promotional campaigns. A technical guide on wall graphics emphasized that reduced removal time translates directly into lower labor costs and operational efficiency. As retailers and entertainment venues pivot toward frequent seasonal promotions, removable films provide flexibility, brand consistency, and cost-effectiveness, cementing their role in short-lifecycle applications.

Development of Films for Direct-to-Film (DTF) and Durable Direct-to-Garment (DTG) Transfer Printing

The growth of digital textile printing is opening opportunities for printable vinyl film suppliers, particularly through the rise of Direct-to-Film (DTF) transfer printing. Unlike traditional Direct-to-Garment (DTG) methods that require fabric pretreatment and struggle with dark fabrics, DTF allows vibrant, durable prints on a wide variety of textiles by transferring designs from PET-based films using heat-press technology. A technical review of DTF processes underscores the critical role of the PET film, which requires specialized coatings to ensure smooth ink release and strong powder adhesive bonding. Manufacturers who can engineer films with optimized release, adhesion, and durability characteristics are poised to become key enablers in this fast-expanding textile printing market. This shift elevates printable self-adhesive vinyl films beyond signage and into high-growth apparel and fashion segments.

Expansion of Conformable and Paint-Replacement Films for Automotive and Industrial Applications

The automotive industry is driving demand for self-adhesive films as replacements for traditional paint, unlocking new opportunities for vinyl film manufacturers. For instance, 3M’s Body Contrast Film demonstrates how polyurethane-based vinyl can streamline production by eliminating additional paint booth processes while enabling multi-tone styling. Beyond OEM applications, advanced cast vinyl films are proving their value in the aftermarket by offering extreme conformability. According to TeckWrap, these films are engineered with reduced internal stress, allowing them to stretch and adhere seamlessly to complex curves and recessed areas of vehicles without peeling. This innovation supports high-end vehicle wraps that deliver long-lasting aesthetics, UV protection, and paint preservation. As sustainability mandates push automotive and industrial sectors to explore alternatives to paint, conformable self-adhesive vinyl films are emerging as a cost-efficient, lightweight, and environmentally superior solution.

Competitive Landscape: Leading Companies in Printable Self-Adhesive Vinyl Films are Driving Innovation and Sustainability Across Fleet Graphics and High-Performance Applications

The global printable self-adhesive vinyl films market is led by players focusing on innovative materials, sustainability, and efficiency. Companies differentiate through high-performance products, strategic acquisitions, and digital integration, catering to fleet graphics, architectural signage, and promotional markets.

Avery Dennison Corporation: Driving Innovation and Sustainability Through Strategic Acquisitions and Startup Collaboration

Avery Dennison’s Graphics Solutions portfolio includes brands such as Fasson, Monarch, and Mactac, serving applications from vehicle wraps to architectural graphics. In August 2025, the acquisition of Meridian Adhesives Group’s U.S. flooring adhesives business strengthened its specialty adhesives segment. The AD Stretch accelerator program (February 2025) partners with startups to advance sustainability, circularity, and digital solutions. Avery Dennison’s atma.io connected product cloud provides digital product passports, enabling enhanced transparency and supply chain management for brands.

3M Company: Enhancing Professional Wrap Efficiency Through Advanced Materials and Global Film Solutions

3M offers a broad range of vinyl and non-vinyl printable films for vehicles, wall graphics, and illuminated signage. In November 2024, it launched Print Wrap Film IJ280, reducing installation time and film lift for vehicle wraps. Leveraging its materials science expertise, 3M provides overlaminates, reflective films, and technical training, ensuring durability and professional-grade results across diverse applications.

Orafol Europe GmbH: Delivering Premium High-Performance Vinyl Films for Fleet and Specialty Applications

ORAFOL manufactures high-performance graphic films and adhesive solutions, including ORAJET and ORACAL brands for vehicle wraps, transit graphics, and floor graphics. The introduction of ORAJET 3951RA+ ProSlide™ reflects the company’s focus on premium vehicle wrap solutions. ORAFOL’s products serve fleet graphics, reflective safety films, and specialty applications such as photoluminescent and screen-printing films, catering to both aesthetic and functional requirements.

Hexis S.A.S.: Innovating with Antimicrobial and PVC-Free Solutions for a Growing Variety of Applications

Hexis specializes in printable adhesive films, including the SKINTAC range for vehicle wraps and PURE ZONE antimicrobial films. Its PVC-free water-based production technology reduces solvents and chemicals while maintaining performance. Hexis invests around 2.5% of turnover in R&D, focusing on high-quality, durable, and environmentally responsible films for visual communication, healthcare, and public transportation markets.

Arlon Graphics, LLC: Expanding Sustainable High-Performance Film Offerings Through Strategic Growth Initiatives

Arlon Graphics offers cast vinyl and high-performance graphic materials for fleet, wall, and promotional applications. In March 2024, it launched VITAL non-PVC films, emphasizing sustainability and durability. Strategic acquisitions, including Alamotape in July 2022, expanded its capabilities through Arlon Innovations, supporting enhanced customer service and continuous product development. The company’s focus on workplace culture and talent development ensures ongoing innovation and market leadership.

Printable Self-adhesive Vinyl Films Market Share Insights, 2025-2034

Permanent Adhesives Dominate Market Share by Adhesive Type in the Printable Self-Adhesive Vinyl Films Industry

Permanent adhesives account for 72% of the printable self-adhesive vinyl films market, cementing their leadership in long-term, durability-critical applications such as vehicle wraps, industrial labeling, and outdoor signage. Their superior bond strength ensures branding consistency across campaigns that must withstand harsh weather conditions, frequent washing, and prolonged exposure to UV radiation. By contrast, removable films have carved out a growing role in temporary applications, particularly in retail pop-ups, exhibitions, and leased commercial spaces, where ease of removal without surface damage is essential. Repositionable adhesives, while niche, play a premium role in large-format installations where error-free application is vital, reducing both material waste and installation costs. This segmentation underscores how adhesive performance requirements align with evolving application needs, with permanent adhesives remaining the market’s backbone while removable and repositionable options expand in specialized, high-value niches.

Labels & Decals Lead Market Share by Application in the Printable Self-Adhesive Vinyl Films Industry

Labels and decals represent 26% of total market share, making them the largest application segment within the printable self-adhesive vinyl films industry. Their dominance is driven by sheer volume across industrial and commercial uses—ranging from safety warnings and compliance labels to durable decals for electronics, appliances, and sporting goods. The cost-effectiveness of vinyl-based decals, compared to direct printing, has accelerated their adoption in high-volume sectors. Indoor and outdoor signage remains a close second, powered by retail marketing campaigns, event branding, and the resilience of cast PVC films in long-term outdoor installations. Vehicle wraps and fleet graphics, although slightly smaller in share, are the fastest-growing application as brands increasingly treat vehicles as mobile billboards, supported by innovations in film conformability and removability. Window graphics, wall graphics, floor graphics, and exhibition panels make up smaller but strategically important segments, serving retail, experiential marketing, and trade shows where visual impact, ease of installation, and reuse are key differentiators.

United States: Tariff Policies and Premiumization Drive Localized Manufacturing Growth

The United States printable self-adhesive vinyl films market is undergoing a structural shift due to the government’s revised tariff framework on imported vinyl films, which is designed to protect domestic resin and substrate manufacturers. This policy has accelerated investment in local production facilities, with companies expanding extrusion lines and acquiring regional players to reduce reliance on imports. Alongside trade regulations, the U.S. market is witnessing rapid adoption of advanced digital printing platforms, especially those utilizing UV-curable and eco-solvent inks, which produce fade-resistant, high-definition graphics suitable for automotive wraps, retail branding, and outdoor advertising. Manufacturers are responding to sustainability requirements by innovating eco-friendly films that incorporate reclaimed PVC and bio-based plasticizers. A notable trend is the premiumization of products, with a rising focus on high-margin cast films for luxury automotive applications and architectural graphics, signaling that U.S. buyers are prioritizing both performance and sustainability.

European Union: Circular Economy and PVC-Free Innovations Reshape the Market

The European Union market for self-adhesive vinyl films is deeply shaped by regulatory policies, particularly the Packaging and Packaging Waste Regulation (PPWR) of 2025, which has set new benchmarks for recyclability and reusable materials. In response, manufacturers are heavily investing in PVC-free alternatives, solvent-free adhesives, and water-based formulations to minimize environmental impact. Companies like UPM Raflatac are not only innovating but also expanding their market share through acquisitions such as Metamark, signaling a wave of consolidation across the region. The EU’s push for a circular economy is driving demand for films that are both high-performance and recyclable, with significant traction in packaging, retail displays, and promotional graphics. This regulatory and sustainability-driven environment makes Europe a global leader in eco-conscious printable film innovations.

China: Domestic Manufacturing and Automation Power Market Expansion

China’s printable self-adhesive vinyl films market is defined by scale, efficiency, and government-backed manufacturing initiatives aimed at reducing reliance on imports. Local producers dominate with automation-ready facilities capable of mass-producing films in diverse formats—transparent, black, and grey adhesives—catering to applications ranging from vehicle advertising to large-scale public signage. The country is also witnessing rapid investment in paint protection films (PPF) and high-end automotive wraps, driven by the booming aftermarket automotive sector. A growing trend is the versatility of printable films, with products tailored for eco-solvent, solvent, and UV-compatible inks, ensuring compatibility with diverse printing technologies. With e-commerce and consumer electronics accelerating demand, China remains one of the fastest-growing hubs for durable, customizable, and cost-effective printable vinyl films.

India: Make in India and MSME Demand Drive Cost-Effective Vinyl Solutions

India’s printable self-adhesive vinyl films market is strongly supported by the government’s Make in India and PLI (Production Linked Incentive) programs, which encourage domestic manufacturing across packaging and graphic materials. Companies such as Shiva Polymers are scaling production capacity and introducing PVC lamination films tailored for a wide range of printing applications. Industry showcases like PrintPack 2025 have highlighted innovations in chemical-free manufacturing and sustainable vinyl solutions, reflecting India’s increasing alignment with eco-friendly practices. The demand is largely driven by MSMEs and small-scale printers, which seek affordable solutions for promotional graphics, vehicle wraps, and retail advertising. The rise of e-commerce and branding initiatives across consumer goods is further fueling demand, making India a promising growth market for cost-effective, high-utility printable films.

Germany: High-Performance Films and Automotive Applications Lead Growth

Germany remains one of the most advanced markets for printable self-adhesive vinyl films, thanks to its focus on high-quality materials, advanced adhesives, and superior performance standards. The automotive and fleet graphics sectors are the largest demand drivers, with films widely used for wraps, branding, and promotional campaigns. German manufacturers are actively innovating with new formulations that improve durability, weather resistance, and adhesive performance, ensuring films withstand extreme environmental conditions. With a mature printing infrastructure and well-structured distribution networks, Germany sets a benchmark for adoption and scalability, reinforcing its leadership position within Europe’s printable vinyl films market.

Japan: Premium Quality and Design-Focused Applications Define Market Growth

Japan’s market for printable self-adhesive vinyl films is heavily influenced by consumer demand for high-quality, aesthetically refined graphics. Regulatory oversight by the Japan Vinyl Industry Association (JVIA) ensures strict quality and safety standards, influencing the raw materials and adhesives used. The country is at the forefront of premium applications, with films widely used in vehicle wraps, architectural decoration, retail signage, and indoor promotional materials. Japanese manufacturers are also developing advanced films that are highly compatible with eco-solvent and UV inkjet systems, reflecting the nation’s emphasis on both design excellence and technology integration. The market is further shaped by consumer preference for durability and visual appeal, making Japan a leader in premium-grade printable self-adhesive vinyl solutions

Printable Self-adhesive Vinyl Films Market Report Scope

Printable Self adhesive Vinyl Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.6 Billion

|

|

Market Size (2034)

|

$5.4 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Film Type (Cast, Calendered), By Thickness (Thin, Thick), By Finish/Type (Opaque, Transparent, Translucent), By Adhesive Type (Permanent, Removable, Repositionable), By Application (Vehicle Wraps & Fleet Graphics, Labels & Decals, Indoor & Outdoor Signage, Window Graphics, Wall Graphics, Floor Graphics, Exhibition & Trade Show Panels)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, 3M Company, Orafol Europe GmbH, Arlon Graphics, LLC, Hexis S.A., Ritrama S.p.A. (Fedrigoni Self-Adhesives), Mactac LLC, UPM Raflatac, Drytac Corporation, General Formulations, Lintec Corporation, Grafityp Self-adhesive Products N.V., APA S.p.A., Poli-Tape Group, Ricoh Company, Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Printable Self-adhesive Vinyl Films Market Segmentation

By Film Type

By Thickness

By Finish/Type

- Opaque

- Transparent

- Translucent

By Adhesive Type

- Permanent

- Removable

- Repositionable

By Application

- Vehicle Wraps & Fleet Graphics

- Labels & Decals

- Indoor & Outdoor Signage

- Window Graphics

- Wall Graphics

- Floor Graphics

- Exhibition & Trade Show Panels

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Printable Self-adhesive Vinyl Films Market

- Avery Dennison Corporation

- 3M Company

- Orafol Europe GmbH

- Arlon Graphics, LLC

- Hexis S.A.

- Ritrama S.p.A. (Fedrigoni Self-Adhesives)

- Mactac LLC

- UPM Raflatac

- Drytac Corporation

- General Formulations

- Lintec Corporation

- Grafityp Self-adhesive Products N.V.

- APA S.p.A.

- Poli-Tape Group

- Ricoh Company, Ltd.

* List Not Exhaustive

Methodology

The research methodology for the Printable Self-Adhesive Vinyl Films Market leverages a combination of primary and secondary research techniques to provide accurate, actionable insights for industry professionals. Primary research included interviews with key stakeholders such as industry executives, production engineers, material scientists, sustainability experts, and supply chain managers across major regions including North America, Europe, Asia-Pacific, and the Middle East. Secondary research involved the detailed analysis of company annual reports, patents, regulatory frameworks, sustainability disclosures, industry journals, and verified market publications, with particular focus on trends in fleet graphics, eco-friendly materials, cast versus calendered films, adhesive types, and digital printing integration. Advanced data triangulation was employed to validate market sizing, growth projections, and segmentation insights, incorporating macroeconomic indicators, raw material pricing trends, technological adoption, and regulatory compliance. Forecasting combined both top-down and bottom-up approaches, while regional analysis was contextualized against local manufacturing initiatives, sustainability mandates, and sector-specific demand trends. This comprehensive methodology by USDAnalytics ensures the report provides reliable, fact-based intelligence aligned with real-world industry developments and decision-making requirements.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.