Market Overview: Rare Earth Metals Recycling is Shifting from Environmental Option to Strategic Supply Infrastructure

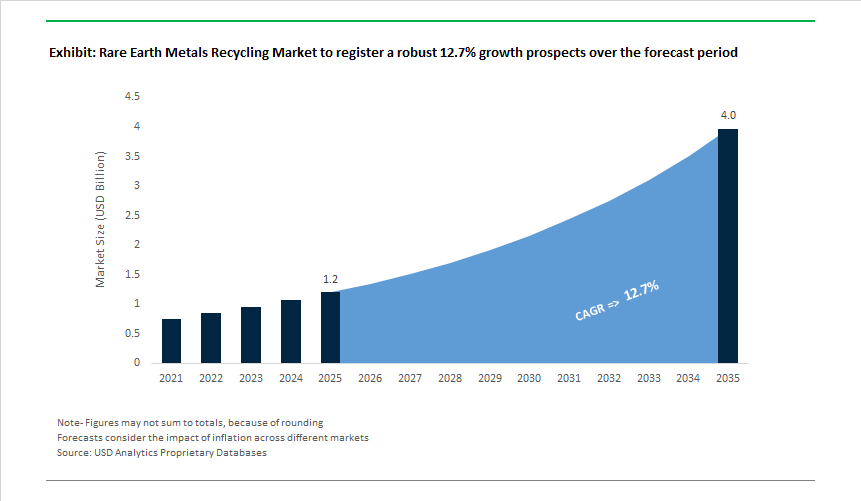

The Rare Earth Metals Recycling Market is valued at USD 1,237.1 million in 2025 and is projected to reach USD 4,089.3 million by 2035, growing at a 12.7% CAGR as recycling moves decisively into the realm of supply-chain security, industrial policy, and strategic risk management. This market is no longer driven primarily by sustainability narratives; it is being pulled by the hard reality that access to rare earth elements-particularly heavy rare earths-has become a constraint on electrification, defense readiness, and advanced manufacturing.

The strategic inflection point lies in geographic concentration and exposure risk. Major consuming economies remain structurally dependent on external supply for rare earths, with downstream manufacturers in electric vehicles, wind turbines, defense electronics, and robotics facing growing uncertainty around pricing, availability, and export controls. Recycling directly addresses this vulnerability by converting end-of-life magnets, production scrap, and electronic waste into domestic secondary supply, reducing dependence on newly mined material and shortening supply chains. As a result, recycling capacity is increasingly viewed as strategic infrastructure, comparable to refining and processing assets.

Policy frameworks are now actively shaping market demand rather than merely supporting it. Regulatory mandates in advanced economies are establishing minimum recycled-content and recovery targets for critical raw materials, effectively creating a guaranteed offtake baseline for rare earth recycling output. These policies are accelerating investment into magnet-to-magnet recycling, industrial scrap reclamation, and urban mining systems, while also de-risking capital deployment for technology developers and processors. Unlike primary mining, recycling benefits from faster permitting, lower environmental opposition, and proximity to end-use manufacturing clusters-factors that materially improve project timelines and capital efficiency.

From the materials perspective, the market’s value density is concentrated in permanent magnets, which represent the single most attractive recycling stream. Magnets combine high rare-earth intensity, predictable composition, and growing end-of-life volumes driven by EV motors, wind turbines, and industrial automation equipment. Critically, heavy rare earths such as dysprosium and terbium-essential for high-temperature magnetic performance-remain structurally scarce, making their recovery disproportionately valuable. Recycling these elements is less about cost parity with mining and more about ensuring availability for applications where substitution is not feasible.

Looking ahead, competitive advantage in the rare earth metals recycling market will be defined by integration and traceability. OEMs are increasingly exploring closed-loop agreements, recycled-content qualification, and material traceability to meet regulatory, customer, and defense procurement requirements. Recycling players that can align with motor designers, magnet manufacturers, and policymakers-offering consistent quality, transparent provenance, and scalable capacity-will move upstream in strategic importance. As electrification and automation deepen, rare earth recycling is evolving into a core pillar of industrial resilience, anchoring long-term demand well beyond cyclical commodity dynamics.

Market Analysis: Policy Acceleration, Export Controls, Strategic Partnerships

The Rare Earth Metals Recycling Market experienced significant geopolitical, regulatory, and commercial shifts, reshaping supply reliability and investment priorities. December 2025 marked a decisive step for North America as REalloys and SRC initiated a US$21 million expansion to boost HREE processing capacity by ~300%. This initiative effectively positions North America’s first commercial-scale HREE supply chain with zero dependency on China, in direct response to U.S. defense procurement requirements for domestic sourcing. Parallel to this, the U.S. Department of Energy (DOE) launched a $134 million funding opportunity (Dec 2025) targeting recycling innovation for unconventional feedstocks such as mine tailings and E-waste, a strong signal of federal commitment to scaling competitive REE recycling infrastructure.

Europe experienced a landmark regulatory update in December 2025 with the REsourceEU Action Plan, reinforcing the EU’s 2030 recycling target and creating multi-year incentives for environmentally optimized recycling processes, closed-loop NdFeB magnet recovery, and secondary refining technologies. At the same time, policy risks intensified globally as China expanded export controls in October 2025, extending restrictions beyond raw REEs to downstream magnet compounds, components, and technical know-how-particularly NdFeB magnets containing Tb and Dy. This directly heightened global supply chain vulnerability, reflected by a 29% month-on-month drop in U.S. magnet imports from China in September 2025, signalling the urgency for domestic Permanent Magnet recycling and secondary refining.

Earlier policy actions established the foundation for today’s accelerated investment. The U.S. DOE’s October 2024 allocation of $19.5 million supported domestic REE recovery programs, while Iluka Resources (Australia) advanced its Eneabba rare earth refinery in August 2024, strengthening non-Chinese downstream separation capabilities. In the defense sector, the 2022 activation of the Defense Production Act (DPA) formally recognized REEs-and by extension REE recycling-as strategically critical to national security. Collectively, the developments show that the market is shifting from pilot programs to industrial-scale deployment, with recycling moving from optional value-add to mandatory supply chain infrastructure.

Rare Earth Metals Recycling Market Trends and Opportunities

Trend 1: Commercial-Scale Hydrometallurgical Recycling of NdFeB Magnet Swarf

Rare earth recycling has crossed a critical threshold with the commercialization of hydrometallurgical and short-loop processes capable of producing magnet-grade rare earth oxides (REOs) from manufacturing waste and end-of-life (EOL) magnets. NdFeB magnet production is inherently inefficient, with 20–30 wt.% of material lost as swarf during cutting, grinding, and finishing—historically treated as low-value waste.

In April 2025, Solvay inaugurated its permanent magnet rare earth production line in La Rochelle, France, marking one of Europe’s most strategically important recycling milestones. The facility integrates recycled feedstocks with primary materials, targeting a 40% reduction in CO₂ emissions and 50% lower water consumption by 2030, while aiming to supply around 30% of European magnet-grade REE demand by the end of the decade. This signals a shift from laboratory separation chemistry to industrial reliability and scale.

Process optimization is delivering tangible efficiency gains. Advanced hydrometallurgical routes validated in 2025 are achieving ~95% recovery rates from magnet swarf, returning high-purity Nd and Pr back into the magnet supply chain without degrading coercivity or remanence. These closed-loop flows are particularly attractive for EV motor and wind turbine OEMs seeking to stabilize input quality while reducing lifecycle emissions.

Hybrid process architectures are accelerating adoption. European demonstration programs such as LIFE INSPIREE have proven that mechanical pre-sorting combined with selective chemical leaching can recover up to 90% of Nd and Dy from complex e-waste streams. Compared with primary mining, these processes operate at significantly lower temperatures and reagent intensity, positioning recycled magnets as a structurally lower-cost and lower-risk alternative.

Trend 2: Direct Electrolytic and Chemical Recovery from Red Mud and Phosphate By-Products

Beyond magnets, the industry is unlocking rare earth value from industrial residues that were historically considered environmental liabilities. Red mud from bauxite refining and phosphogypsum from fertilizer production are now being reclassified as secondary rare earth resources, particularly for scandium (Sc) and yttrium (Y)—elements critical for aerospace alloys, SOFCs, and next-generation aluminum applications.

In October 2025, Rio Tinto and Geomega Resources announced a landmark collaboration to commercialize rare earth extraction from bauxite residue at a Quebec facility. The process employs a three-circuit recovery system capable of producing 6–7 commercial byproducts, while reducing overall waste volumes by 80–85%. This transforms red mud from a long-term storage risk into a revenue-generating feedstock.

Selective leaching benchmarks are particularly compelling. Pilot data released in 2025 shows that optimized phosphoric acid leaching can selectively extract ~40% of scandium from Greek bauxite residue under ambient conditions—without the gelation issues that plague conventional acid treatments. This “nose-to-tail” resource utilization model bypasses energy-intensive smelting and materially improves project economics.

A parallel opportunity is emerging in fertilizer-linked waste streams. Phosphogypsum, once stockpiled at scale, is now being processed via selective precipitation techniques to recover lanthanides. These developments diversify rare earth supply away from mined concentrates and reduce exposure to price shocks in primary markets, reinforcing recycling as a strategic buffer rather than a marginal supplement.

Opportunity 1: Recovery of Magnets from Decommissioned Wind Turbines Under EU ESPR

Europe’s wind repowering cycle is creating one of the largest secondary rare earth feedstocks globally. The Ecodesign for Sustainable Products Regulation (ESPR), in force since July 2024, is transforming this technical reality into a regulatory obligation.

Under ESPR implementation phases in 2025–2026, the European Commission is introducing Digital Product Passports for permanent magnets, embedding data on material composition, origin, and recyclability. By 2030, at least 25% of critical raw materials consumed in the EU must originate from recycling, effectively mandating magnet recovery at end of life.

The material scale is significant. Direct-drive wind turbines above 3 MW contain 1–2 tons of NdFeB magnets per unit, representing a concentrated, high-purity feedstock. The EU’s RESourceEU Action Plan (December 2025) explicitly prioritizes keeping this material within Europe to reduce single-country dependency by 30–50% by 2029.

Environmental performance further strengthens the case. ISO-aligned lifecycle assessments published in March 2025 confirm that recycled NdFeB magnets produced via short-loop processes carry a carbon footprint of ~2.35 kg CO₂ eq./kg, compared with >10 kg CO₂ eq./kg for magnets derived from primary mining and refining. This delta is increasingly decisive for OEMs operating under Scope 3 emissions pressure.

Opportunity 2: Onshoring Magnet-to-Magnet Recycling for U.S. Supply Chains

In the United States, rare earth recycling is becoming a national security and industrial policy priority, particularly for EVs, defense systems, and grid infrastructure. The emphasis is shifting toward magnet-to-magnet recycling, where recovered material is reintroduced directly into new magnet production without reverting to oxide intermediates.

In December 2025, the U.S. Department of Energy announced a $134 million funding program to accelerate domestic rare earth supply chains. The initiative targets demonstration-scale facilities capable of processing unconventional feedstocks, including e-waste and EOL magnets, to reduce reliance on imported materials.

Commercial deployment is already underway. HyProMag USA, a subsidiary of Mkango Resources, finalized a lease in late 2025 for a 128,000 sq. ft. recycling and manufacturing hub in the Dallas–Fort Worth region. Scheduled for commissioning by mid-2027, the facility will produce ~750 metric tons of recycled NdFeB magnets annually using patented Hydrogen Processing of Magnet Scrap (HPMS) technology—one of the most material-efficient recycling routes available.

Feedstock security is being addressed through upstream integration. In August 2025, HyProMag USA partnered with Intelligent Lifecycle Solutions to begin systematic stockpiling of magnet-bearing e-waste, supported by planned pre-processing sites in South Carolina and Nevada. This hub-and-spoke model establishes the first fully integrated U.S.-based magnet-to-magnet recycling network, with a strategic focus on high-coercivity grades (>20 kOe) required for EV traction motors.

Market Share Analysis: Rare Earth Metals Recycling Market

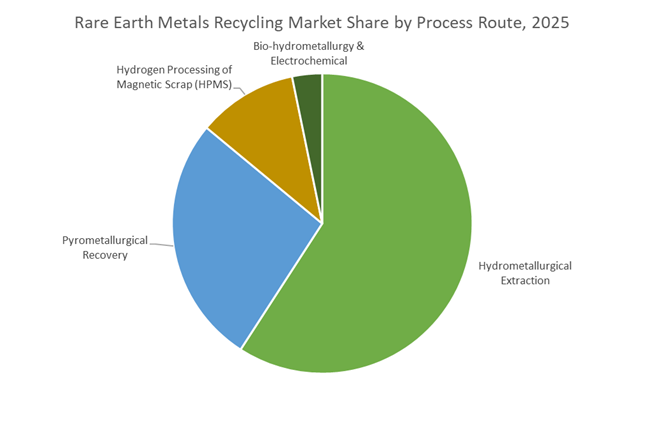

Market Share by Process Route: Hydrometallurgical Extraction Anchors Commercial-Scale Rare Earth Circularity

Hydrometallurgical extraction commands approximately 55% of the Rare Earth Metals Recycling Market because it is currently the only process route capable of delivering magnet-grade purity, high recovery yields, and regulatory-aligned carbon performance at scale. Unlike pyrometallurgical smelting—which struggles with selective separation and permanently loses heavy rare earths into slag—hydrometallurgy enables element-by-element recovery, a decisive advantage as demand shifts toward dysprosium- and terbium-rich formulations for high-temperature EV motors. Commercial validation has moved well beyond pilot status: facilities in the U.S. and Europe are now consistently achieving ≥99.5% NdPr oxide purity, a threshold that allows recycled oxides to be directly reintroduced into sintered NdFeB magnet supply chains without reformulation risk. Just as critical for procurement teams, optimized solvent extraction flowsheets are now delivering 95%+ neodymium and near-total dysprosium recovery, materially improving unit economics versus mining while avoiding the geopolitical exposure of primary supply. The segment’s dominance is further reinforced by lifecycle metrics—carbon footprint reductions exceeding 60% versus virgin mining—which directly align with the EU Critical Raw Materials Act and OEM Scope 3 decarbonization mandates. As recycling shifts from “sustainability add-on” to strategic feedstock, hydrometallurgy has become the default process route underpinning the rare earth circular economy.

Market Share by Application: Automotive & E-Mobility Drives Closed-Loop Demand at Industrial Scale

Automotive and e-mobility represent the largest application segment at around 45% market share, reflecting the structural convergence of EV adoption, magnet-intensive drivetrain design, and end-of-life material recovery. A single battery electric vehicle contains 2–3 kg of rare earth magnets, and the first large wave of EVs sold between 2015 and 2020 is now entering retirement—creating a predictable, high-quality scrap stream ideally suited for hydrometallurgical recycling. What differentiates automotive demand is scale and value density: recycled material from traction motors can now support capacity equivalent to 1 million EVs per year, with confirmed expansion plans targeting multi-million-vehicle throughput within this decade. The economics are amplified by the 250–400% price premium commanded by heavy rare earth oxides, making recycling the most profitable and reliable Western source of dysprosium and terbium for high-efficiency motors. OEM design strategies are also reinforcing this dominance, with next-generation motors engineered for rapid disassembly and magnet extraction, reducing recycling energy intensity by up to 80% versus primary ore processing. Finally, provenance matters: certified non-Chinese, recycled rare earth supply has emerged as a procurement differentiator, allowing automotive and defense buyers to justify 15–20% pricing premiums in exchange for supply security. Together, these factors firmly position automotive and e-mobility as the demand anchor shaping market share dynamics in rare earth metals recycling.

Competitive Landscape: Integrated Producers & Closed-Loop Innovators Reshaping Global Supply

The competitive landscape is defined by companies that combine refining expertise, recycling technology, magnet manufacturing, and supply chain integration. Players who can secure reliable secondary feedstock and establish non-Chinese refining pathways will benefit the most from tightening policies and magnet-centric demand.

MP Materials - Building a U.S. end-to-end NdPr to magnet ecosystem

MP Materials is moving beyond oxide production at Mountain Pass toward full domestic magnet production: the company is converting NdPr oxide to NdFeB precursor and ramping trial sintered magnet output, while bringing a vertically integrated Independence (Fort Worth) magnet facility online to produce finished magnets and incorporate magnet-recycling feedstock. The Independence roadmap targets commercial precursor output already online and a progressive ramp to finished magnets by late-2025 / 2026 - positioning MP to supply OEMs (notably GM as an anchor customer) and reduce U.S. dependence on overseas magnet supply. Strategic implication: buyers seeking nearshore magnet supply and traceable NdPr content should prioritize MP as a primary offtake partner.

Lynas Rare Earths - Largest non-Chinese separation scale + Kalgoorlie cracking & leaching buildout

Lynas combines Mt Weld mining with multi-site processing (Malaysia separation and the newer Kalgoorlie cracking & leaching hub) to shorten the chain from concentrate to separated REE. Recent moves show Lynas expanding Kalgoorlie to perform upstream cracking/leaching (reducing radioactive waste footprint in Malaysia) and negotiating heavy-REE separation routes (including new Malaysian heavy-REE facilities). Lynas is also pursuing capital raises and potential offtake/dialogue with defence customers, making it a cornerstone non-Chinese LREE+HREE supplier - relevant for buyers needing scale, regulatory traceability and third-party feedstock intake. Note: Kalgoorlie has seen operational sensitivity (power disruptions) in late-2025, which buyers should monitor as a near-term supply risk.

Umicore - Closed-loop metallurgical capability and industrial recycling scale

Umicore operates advanced pyrometallurgical + hydrometallurgical flowsheets that recover precious & critical metals from production scrap and end-of-life streams. The company publishes detailed recycling roadmaps and investor materials showing integrated recovery for complex residues and battery/industrial waste, positioning Umicore as a partner for OEMs that require verifiable, low-carbon, circular sourcing of REEs and associated critical metals. For companies prioritizing sustainability claims and chain-of-custody, Umicore’s closed-loop offerings (and scale) are a primary avenue to secure recycled metal feedstock.

Neo Performance Materials - European magnet capacity and direct-magnet recovery ambitions

Neo has moved aggressively into Europe: in 2025 it opened a state-of-the-art permanent-magnet facility in Narva, Estonia, signaling a strategic push to localize magnet supply for EU EV and wind OEMs and align with the EU Critical Raw Materials agenda. Neo’s Magnequench heritage in melt-spun magnetic powders and pilot lines for direct NdFeB recovery from scrap give it a specialist edge in supplying both primary magnet powders and recycled magnet feedstreams - attractive for OEMs seeking managed supply in Europe with shorter lead times.

Energy Fuels - Fast path to U.S. REE oxides via White Mesa and monazite processing

Energy Fuels repurposed the White Mesa Mill and commissioned Phase-1 REE separation capability, and publicly reports pilot heavy REE oxide production (Dy/Tb) with plans to scale HREE oxide output if a production decision is taken. Their strategy leverages existing licensed infrastructure to accelerate U.S. REE oxide capability (including monazite processing and hydrometallurgical routes), making Energy Fuels an expedient partner for buyers who need domestic HREE supply windows and government-aligned sourcing. Recent financing activity also strengthens their near-term scale potential.

The United States has moved decisively from pilot-scale recycling to commercial closed-loop rare earth recovery, positioning recycling as a core pillar of national resource security. The most consequential milestone came in July 2025, when Apple and MP Materials announced a $500 million partnership to establish a dedicated recycling facility at Mountain Pass, California. The plant is engineered to process end-of-life electronics and convert recovered neodymium (Nd) and praseodymium (Pr) into magnet-grade feedstock for Apple’s Taptic Engine and other precision components—marking one of the world’s first large-scale consumer-electronics-to-magnet loops.

Federal funding has accelerated scale-up. In December 2025, the U.S. Department of Energy committed $134 million to demonstrate commercial recovery of rare earth elements (REEs) from secondary sources such as coal fly ash and acid mine drainage, materially de-risking supply for EVs, wind turbines, and defense platforms. Parallel progress on heavy rare earths strengthens resilience: Energy Fuels produced 99.9% purity dysprosium oxide at its White Mesa Mill in August 2025, with commercial capacity planned by Q4 2026, enabling high-temperature magnet performance for EV traction motors.

European Union: RESourceEU and Binding 25% Recycling Mandate

The European Union has enacted the most stringent circularity framework globally, reframing rare earth recycling from sustainability to industrial competitiveness. The RESourceEU Action Plan, adopted in December 2025 by the European Commission, mobilizes €3 billion for priority projects within 12 months, directly targeting urban mining and magnet-to-magnet recovery to cut dependence on imports exceeding 90% for some materials.

Implementation of the Critical Raw Materials Act (CRMA) in 2025 sets a binding 2030 target: 25% of annual strategic material consumption must come from recycling. This mandate is reshaping investment decisions across automotive, wind, and electronics supply chains. To secure feedstock, the Commission is preparing export restrictions on permanent magnet scrap by Q2 2026, ensuring NdFeB waste remains within the EU for domestic processors—an explicit move to anchor recycling capacity and stabilize long-term supply.

China: Extraterritorial Controls and the 0.1% De Minimis Rule

China continues to leverage its unparalleled processing base to exert extraterritorial control over recycled rare earth flows. In October 2025, the Ministry of Commerce of the People's Republic of China (MOFCOM) implemented export controls that apply even to foreign-made items containing Chinese-origin rare earths. Central to this regime is the “0.1% de minimis rule” (Announcement 61): if the value share of Chinese-origin rare earth metals in a foreign magnet reaches ≥0.1%, exports require Chinese licensing.

Crucially, the policy extends beyond materials to recycling and separation technologies, effectively freezing the transfer of advanced Chinese recovery know-how. This has elevated compliance risk for global recyclers and OEMs while reinforcing China’s leverage over heavy rare earths (Dy, Tb)—materials indispensable for high-temperature EV and aerospace magnets.

India: ₹7,280 Crore National Magnet Mission Anchored in Recycling

India is building a domestic rare earth permanent magnet (REPM) ecosystem with recycling embedded as a strategic pillar of its 2047 self-reliance vision. In November 2025, the Union Cabinet approved a ₹7,280 crore ($870 million) Sintered REPM Scheme to establish 6,000 MTPA of integrated magnet manufacturing capacity, explicitly linking production incentives to secondary material recovery.

The National Critical Mineral Mission (NCMM), launched in 2025, prioritizes recovery from discarded products and industrial waste, while Indian Rare Earths Limited (IREL) is collaborating with private partners to deploy NdPr separation circuits. These efforts aim to reduce India’s import dependence from 100% to ~60% by 2030, aligning EV growth with domestic material security.

Japan: Economic Security, ¥400 Billion Stimulus, and Allied Frameworks

Japan is reinforcing economic security legislation to reshore advanced recycling capabilities for automotive, robotics, and electronics. Under the US–Japan Critical Minerals Framework signed in October 2025, Japan secured allied support for diversified sourcing and recycling, while committing financing to stabilize downstream manufacturing.

Tokyo has earmarked ~¥400 billion ($2.7 billion) through 2027 for rare earth and battery material projects, accelerating deployment of high-efficiency solvent extraction and magnet recycling technologies. In December 2025, collaborative research involving Japanese partners demonstrated improved recovery yields from used EV motors, reducing energy intensity and enabling higher-purity outputs for next-generation traction systems.

Australia: From Mining Powerhouse to Mid-Stream Recycling Hub

Australia is transitioning from a primary miner to a mid-stream processing and recycling anchor for Western supply chains. A US–Australia framework signed in October 2025 outlines an $8.5 billion pipeline of projects, including Pentagon-backed investment in gallium refining and $2.2 billion in EXIM financing for critical mineral processing.

Operational milestones underpin this shift. In May 2025, Lynas Rare Earths produced commercial dysprosium oxide outside China for the first time, increasingly incorporating post-industrial scrap. The Kalgoorlie cracking and leaching hub, expected fully operational by late 2025, will process 84,000 tonnes/year of concentrate—creating a robust base for future recycling integration across Nd, Pr, and Dy streams.

2025 Strategic Matrix: Rare Earth Metals Recycling Developments

Rare Earth Metals Recycling Developments Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Recycled Elements

|

|

United States

|

Closed-loop consumer tech

|

$500M Apple–MP Materials facility

|

Nd, Dy, Pr

|

|

European Union

|

Binding circularity mandates

|

25% recycling target by 2030 (CRMA)

|

NdFeB magnet scrap

|

|

China

|

Resource diplomacy

|

MOFCOM 0.1% de minimis rule

|

Heavy REEs (Dy, Tb)

|

|

India

|

EV growth & self-reliance

|

₹7,280 Cr REPM scheme

|

Sintered magnets (NdPr)

|

|

Japan

|

Economic security

|

¥400B stimulus & US–Japan framework

|

Nd, Tb

|

|

Australia

|

Mid-stream integration

|

$8.5B US–Australia alliance

|

Pr, Dy

|

Rare Earth Metals Recycling Market Report Scope

Rare Earth Metals Recycling Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1237.1 Million

|

|

Market Size (2035)

|

$4089.3 Million

|

|

Market Growth Rate

|

12.7%

|

|

Segments

|

By Process Route (Hydrometallurgical, Pyrometallurgical, HPMS, Bio-hydrometallurgy, Electrochemical Recovery), By Feedstock Type (End-of-Life Magnets, Industrial Scrap, Secondary Sources, Industrial Tailings), By Recovered Element (LREE, HREE, Specialty Elements), By End-User Industry (Automotive, Energy, Consumer Electronics, Aerospace & Defense, Medical Devices)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hitachi Metals, Solvay S.A., TDK Corporation, MP Materials Corp., ReElement Technologies, Umicore N.V., Neo Performance Materials, HyProMag Ltd., Carester, Urban Mining Co., Mitsubishi Materials Corporation, China Southern Rare Earth Group, Geomega Resources Inc., Cyclic Materials, Heraeus Remloy

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rare Earth Metals Recycling Market Segmentation

By Process Route

- Hydrometallurgical Extraction

- Pyrometallurgical Recovery

- Hydrogen Processing of Magnetic Scrap (HPMS)

- Bio-hydrometallurgy

- Electrochemical Recovery

By Feedstock Type

- End-of-Life Magnets

- Industrial Scrap

- Secondary Sources

- Industrial Tailings

By Recovered Element

- Light Rare Earths (LREE)

- Heavy Rare Earths (HREE)

- Specialty Elements

By End-User Industry

- Automotive

- Energy

- Consumer Electronics

- Aerospace & Defense

- Medical Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Rare Earth Metals Recycling Market

- Hitachi Metals, Ltd.

- Solvay S.A.

- TDK Corporation

- MP Materials Corp.

- ReElement Technologies

- Umicore N.V.

- Neo Performance Materials

- HyProMag Ltd.

- Carester

- Urban Mining Co.

- Mitsubishi Materials Corporation

- China Southern Rare Earth Group

- Geomega Resources Inc.

- Cyclic Materials

- Heraeus Remloy

*- List not Exhaustive