Market Overview: Global Self-Adhesive Labels Industry Growth Driven by E-commerce and Sustainability

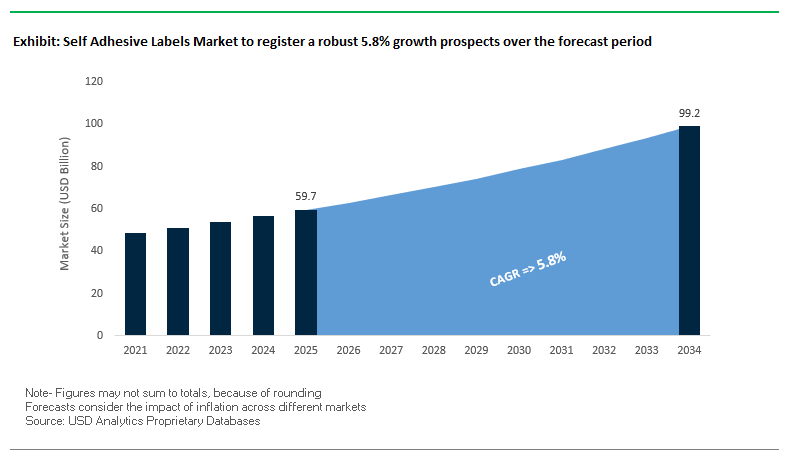

The Self-Adhesive Labels Market is projected to reach $59.7 billion in 2025 and expand to $99.2 billion by 2034, reflecting a healthy CAGR of 5.8%. This growth is primarily fueled by the expanding e-commerce sector, rising demand for sustainable packaging, and increasing use of pressure-sensitive labels across industries such as food, beverages, pharmaceuticals, and consumer goods. For buyers and industry professionals, self-adhesive labels provide versatile, cost-effective, and high-performance solutions for branding, compliance, and logistics.

Paper-based labels dominate the market, accounting for nearly 63% of demand due to their versatility and affordability. Emulsion acrylic adhesives continue to lead, given their excellent bond strength and suitability for diverse applications. Meanwhile, flexographic printing technology remains the most widely adopted method thanks to its speed, cost-efficiency, and ability to print on varied substrates.

The growth of e-commerce is reshaping demand, with shipping, tracking, and logistics labels becoming indispensable for smooth supply chain operations. Additionally, sustainability is at the forefront, with recyclability, downgauging, and carbon footprint reduction shaping product innovation.

Key Insights for Professionals and Buyers

- Paper-based labels lead: Around 63% of the global market share is attributed to paper due to affordability and versatility.

- Emulsion acrylic adhesives dominate: Widely used in food, beverage, and pharma sectors for reliable bonding.

- Flexographic printing prevails: High-volume label production driven by cost-efficiency and adaptability.

- E-commerce surge boosts demand: Strong growth in shipping, logistics, and package tracking labels globally.

Market Analysis: Strategic Developments Shaping the Self-Adhesive Labels Market

The global self-adhesive labels market is undergoing rapid transformation driven by strategic acquisitions, sustainability initiatives, and technological innovation. Companies are expanding their portfolios while strengthening capabilities to meet evolving regulatory and consumer expectations.

In August 2025, Constantia Flexibles won two WorldStar Global Packaging Awards for sustainable solutions, reinforcing its leadership in eco-friendly labels. During the same month, Avery Dennison announced a $390 million acquisition of Meridian Adhesives Group’s U.S. flooring adhesives business, enhancing its specialty adhesives portfolio. Also in August, Mondi scaled up its sustainability efforts with new recycling collaborations, while Borouge Group International’s $13.4 billion acquisition of Nova Chemicals (July 2025) signaled consolidation across the plastics and labeling supply chain.

Other milestones highlight the market’s innovation focus. In May 2025, Avery Dennison and Shenzhou Group launched a joint venture in Vietnam, boosting capacity for apparel labeling and RFID solutions. In April 2025, UPM Raflatac introduced its Carbon Action Plastic Films portfolio to support carbon reduction across packaging. Earlier, in March 2025, Constantia Flexibles and Aluflexpack formed a joint venture emphasizing innovation and sustainability in flexible packaging.

The trend extends back to 2024, when Mondi developed recycling initiatives for release liner waste and Fuji Seal International set a new expansion plan for labels in home personal care, dairy, and pharmaceuticals. By November 2023, Berry Global had launched its downgauged recyclable cling film Omni® Xtra+, while May 2023 saw RKW Group expand its RKW ECORE® range with MDO PE films suitable for packaging and labeling.

Emerging Trends and Opportunities Transforming the Self-Adhesive Labels Market

Accelerated Adoption of Digital Printing Presses for Short-Run and Versioning

The self-adhesive labels market is undergoing a rapid transformation as brand owners demand shorter run lengths, faster turnaround times, and highly customized versioning to address micro-trends, seasonal launches, and regional promotions. This shift is driving widespread investment in digital printing technologies, moving beyond the traditional dominance of flexography. HP Indigo presses, for instance, are being rapidly adopted by converters to meet demand for agility and cost efficiency in short-run production. Digital printing eliminates the high setup costs associated with conventional presses and allows converters to deliver jobs profitably even at low volumes. By enabling “just-in-time” label production, brand owners are significantly reducing inventory waste and mitigating the risk of obsolete stock from outdated campaigns. For fast-moving consumer goods (FMCG), this agility translates into a competitive advantage, with brands now able to launch limited-edition designs or seasonal promotions in days rather than weeks. As digital printing adoption accelerates, it is reshaping both the economics and the creative potential of the self-adhesive labels market.

Integration of RFID and NFC Technology into Mainstream Label Applications

Self-adhesive labels are no longer limited to product identification; they are evolving into active data carriers through the integration of RFID (Radio Frequency Identification) and NFC (Near Field Communication) technology. Once considered niche or premium, smart labels are now entering mainstream applications in retail, pharmaceuticals, and luxury goods. Retailers such as Kroger are partnering with Avery Dennison to deploy RFID-enabled labels for real-time inventory visibility, improving both efficiency and customer experience. At the same time, RFID and NFC technologies are proving instrumental in brand protection, helping companies assign unique digital identities to products and combat counterfeit goods. A French fragrance brand, for instance, integrates RFID and QR code labels to ensure authenticity while enhancing supply chain transparency. On the consumer side, NFC-enabled labels transform everyday packaging into interactive experiences consumers can tap their smartphones to access sustainability information, promotional offers, or loyalty rewards. This combination of supply chain efficiency, anti-counterfeiting, and engagement is driving rapid adoption across diverse industries.

Development of Functional and Sustainable Adhesive Technologies

The push toward circular economy models is creating a high-value opportunity for functional adhesives that enable recyclability without compromising performance in demanding conditions. Wash-off adhesives, already deployed by brands such as Heineken and Fever-Tree, allow labels to detach cleanly during PET bottle recycling, preventing adhesive contamination and ensuring high-quality recycled PET flakes. Industry innovation is also converging sustainability with digital transformation Avery Dennison has launched the first RFID-enabled self-adhesive label recognized by the Association of Plastic Recyclers (APR) for its compatibility with PET recycling streams. This breakthrough allows brands to meet both traceability and sustainability goals in a single solution. In parallel, adhesives capable of withstanding extreme environments, such as Henkel’s cold- and oil-resistant formulations, ensure label integrity across diverse use cases from frozen food packaging to industrial chemicals. As brands face tightening regulations and growing consumer expectations, the ability to offer recyclable, durable, and functional adhesive technologies represents a critical growth frontier for label manufacturers.

Expansion into Primary Pharmaceutical Labeling and Serialization

The pharmaceutical industry is emerging as one of the most lucrative growth segments for self-adhesive labels, fueled by strict global regulations mandating serialization and track-and-trace capabilities. Under the EU’s Falsified Medicines Directive (FMD), all prescription medicine packs must feature unique identifiers and anti-tampering devices, making serialized self-adhesive labels indispensable. Similarly, the U.S. FDA’s Drug Supply Chain Security Act (DSCSA) is accelerating adoption of serialized labels as a tool to ensure patient safety and prevent counterfeit drugs. Beyond compliance, the pharmaceutical labeling segment is characterized by high-value requirements, including tamper-evidence, durability, and compatibility with automated packaging lines. These factors create barriers to entry and reward manufacturers capable of delivering highly specialized solutions. For label producers, this segment offers both regulatory-driven volume growth and premium pricing potential, positioning pharmaceutical serialization as a transformative opportunity within the self-adhesive labels market.

Competitive Landscape: Leading Companies in Global Self-Adhesive Labels Market

The Self-Adhesive Labels Market is competitive, with leading companies investing in acquisitions, eco-friendly innovations, and global expansion. Industry leaders are differentiating through sustainability portfolios, digital technologies such as RFID, and vertical integration to ensure supply chain resilience.

Avery Dennison: Expanding Global Reach with RFID and Specialty Adhesives

Avery Dennison leads in pressure-sensitive labels and digital identification technologies. In August 2025, it announced the $390 million acquisition of Meridian Adhesives Group’s U.S. flooring adhesives business, strengthening its specialty adhesives portfolio. Earlier in May 2025, the company partnered with Shenzhou Group to open a joint venture facility in Vietnam, producing apparel labels and RFID solutions under its Embelex brand. With innovations connecting physical products to the digital ecosystem, Avery Dennison is positioning itself as a pioneer in smart labeling and supply chain transparency.

CCL Industries: Driving Label Sustainability with EcoStream® and EcoFloat®

CCL Industries offers a broad portfolio of specialty labels, with strong positions in healthcare and consumer goods. Its EcoStream® and EcoFloat® technologies are designed to support PET recycling, enabling bottle-to-bottle recovery. Strategically, CCL emphasizes both organic growth and acquisitions, while expanding digital printing capabilities to meet customization trends. Its vertically integrated operations, from film extrusion to label converting, provide a competitive edge in serving multinational clients with consistent global supply.

UPM Raflatac: Advancing Low-Carbon Label Solutions with Carbon Action Films

UPM Raflatac is recognized for its sustainability leadership. In April 2025, it launched the Carbon Action Plastic Films portfolio, offering solutions to lower carbon footprints in packaging and labeling. The company’s commitment to net-zero targets and membership in the UN Global Compact underline its ESG focus. Through tools such as the UPM Label Life service, which conducts life cycle assessments, the company empowers clients to evaluate environmental impacts and make data-driven sustainable label choices.

LINTEC Corporation: Leveraging Adhesive and Surface Technologies for Expansion

LINTEC specializes in adhesive papers, films, and specialty materials. With strengths in adhesive applications, surface improvements, and release materials, the company delivers highly differentiated self-adhesive solutions. Its portfolio also extends into barcode printers and labeling equipment, creating synergies across materials and machinery. LINTEC’s strategy emphasizes global expansion, particularly in the Americas, Europe, and Asia Pacific, positioning it as a comprehensive solutions provider in labeling.

Constantia Flexibles: Award-Winning Leadership in Sustainable Labeling

Constantia Flexibles has a strong presence in food, beverage, and pharmaceutical labeling. In August 2025, the company earned two WorldStar Global Packaging Awards for sustainable innovations such as EcoPeelCover and EcoLamHighPlus. Its portfolio spans self-adhesive labels, flexible packaging, and digital services including augmented reality packaging. Constantia’s strategy centers on eco-friendly solutions and strategic partnerships to strengthen its leadership in sustainable and innovative labeling.

Self Adhesive Labels Market Share Insights

Release-Liner Labels Command Market Share by Product Type

Release-liner labels dominate the self-adhesive labels industry, accounting for more than 90% of total demand in 2025. Their leadership is deeply entrenched due to decades of investment in high-speed conversion infrastructure, global applicator compatibility, and proven versatility across industries ranging from FMCG to pharmaceuticals. Unlike linerless alternatives, release-liner labels integrate seamlessly into existing packaging lines, minimizing downtime and avoiding costly retooling, which remains a significant barrier for brand owners operating at global scale. For manufacturers, this stability offers predictable supply chains, material performance consistency, and broad substrate adaptability, making release-liner formats the default standard. Even as sustainability pressures mount, the inertia of installed equipment and the breadth of use cases ensures that release-liner labels remain the backbone of product identification and branding worldwide.

Food & Beverages Hold the Largest Market Share by End-Use Industry

The food and beverages sector leads self-adhesive label consumption, representing nearly one-third of global demand. This share is underpinned by the sheer volume of packaged goods requiring compliant, visually appealing, and durable labeling solutions. Beyond basic branding, food labels must deliver high legibility for regulatory compliance (ingredient disclosures, nutritional facts, and traceability codes) while maintaining adhesion and print quality under cold-chain conditions and high-moisture environments. The sector’s influence is amplified by its role in driving material innovation, with brand owners demanding recyclable substrates, low-migration inks, and liner reduction strategies to align with circular economy goals. As FMCG giants shift to sustainable packaging roadmaps, food and beverage applications will continue to anchor the market, not only through scale but by setting the direction for next-generation self-adhesive label technologies.

United States: Smart and Sustainable Self-Adhesive Labels Driving Market Growth

The U.S. self-adhesive labels market is witnessing significant growth, driven by rising consumer and corporate awareness of sustainability. Demand for high-performance, cost-effective, and recyclable labels is particularly strong across food, pharmaceutical, and e-commerce industries. Companies are increasingly adopting eco-friendly solutions, including linerless labels, which eliminate backing paper, reduce waste, and lower transportation costs.

Technological innovations are transforming the sector, with smart label technologies like QR codes and RFID tags gaining traction for enhanced product tracking, consumer engagement, and supply chain visibility. Leading firms, such as Avery Dennison, have introduced new lines of sustainable self-adhesive labels, reflecting the industry’s shift toward eco-conscious packaging solutions. The rapid growth of e-commerce further fuels demand for durable, print-ready, and tamper-evident labels, reinforcing the strategic importance of self-adhesive labels in the logistics and packaging ecosystem.

Germany: Circular Economy and Regulatory Framework Accelerate Sustainable Label Adoption

Germany’s self-adhesive labels industry is strongly influenced by the stringent EU Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates eco-friendly and fully recyclable labels. The market benefits from the country’s leadership in the circular economy, fostering collaboration between manufacturers and end-users to create labels with high recycled content and designed for recyclability.

Technological innovation is central to Germany’s market growth. For instance, Herma launched a wash-off label adhesive for PET bottles, facilitating recycling and aligning with sustainability goals. Additionally, Avery Dennison’s €45 million expansion of its European facilities in Champs-sur-Drac aims to enhance production efficiency and incorporate a high-speed hotmelt adhesive coater, meeting increasing demand for sustainable, high-speed labeling solutions. Governmental mandates and new waste reduction targets under PPWR continue to stimulate investment and innovation in the German self-adhesive labels market.

China: Green Initiatives and Technological Advancements Propel Self-Adhesive Labels

China’s self-adhesive labels market is being shaped by the government’s dual carbon goals of achieving carbon peak and carbon neutrality, prompting a green transformation of the packaging industry. New regulations are encouraging eco-friendly, reduced, and reusable label materials, while policies restricting non-degradable plastics in e-commerce packaging by 2025 further strengthen sustainability efforts.

Technological adoption is a key growth driver. Chinese manufacturers are investing in automation, AI, and “5G plus industrial internet” solutions to optimize production efficiency and enable flexible label manufacturing. The rapid expansion of e-commerce, especially in Tier 2 and 3 cities, is increasing demand for secure, tamper-evident, and high-quality self-adhesive labels, creating opportunities for innovative labeling solutions that align with both consumer convenience and environmental standards.

India: E-commerce Growth and Government Policies Accelerate Sustainable Label Market

India’s self-adhesive labels industry is expanding rapidly, propelled by Make in India initiatives that encourage local manufacturing and innovation in packaging. The growing demand for labels across food, beverage, and pharmaceutical sectors highlights the increasing adoption of efficient labeling solutions to improve product visibility and consumer trust.

E-commerce growth is a major catalyst, driving the need for reliable shipping and logistics labels that support accurate package tracking and identification. Sustainability initiatives, such as the Plastic Waste Management (Amendment) Rules, are creating strong demand for eco-friendly and reusable labels. Indian companies are also investing in technological advancements, with firms like UFlex introducing new eco-friendly self-adhesive label solutions, and dairy companies implementing MDO laminates for liquid pouches, reinforcing the market’s focus on high-quality, sustainable labeling innovations.

Self-Adhesive Labels Market Report Scope

Self Adhesive Labels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$59.7 Billion

|

|

Market Size (2034)

|

$99.2 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (Release-Liner Labels, Linerless Labels), By Material Type (Paper-based, Plastic-based, Foil-based), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Consumer Durables, Retail & Logistics, Other Industries), By Printing Technology (Flexography, Digital Printing, Screen Printing, Letterpress, Gravure)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, CCL Industries Inc., Multi-Color Corporation, Fuji Seal International, Inc., UPM Raflatac, Lintec Corporation, SATO Holdings Corporation, 3M Company, R.R. Donnelley & Sons Company, All4Labels Global Packaging Group GmbH, Toray Industries, Inc., Labelmakers Group, Herma, Mondi Group, Quad/Graphics, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Self Adhesive Labels Market Segmentation

By Product Type

- Release-Liner Labels

- Linerless Labels

By Material Type

- Paper-based

- Plastic-based

- Foil-based

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Consumer Durables

- Retail & Logistics

- Other Industries

By Printing Technology

- Flexography

- Digital Printing

- Screen Printing

- Letterpress

- Gravure

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Self Adhesive Labels Market

- Avery Dennison Corporation

- CCL Industries Inc.

- Multi-Color Corporation

- Fuji Seal International, Inc.

- UPM Raflatac

- Lintec Corporation

- SATO Holdings Corporation

- 3M Company

- R.R. Donnelley & Sons Company

- All4Labels Global Packaging Group GmbH

- Toray Industries, Inc.

- Labelmakers Group

- Herma

- Mondi Group

- Quad/Graphics, Inc.

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global Self-Adhesive Labels market, highlighting breakthroughs in digital printing, smart label integration, functional adhesives, and sustainability-driven innovations. The analysis reviews historical trends from 2021 to 2024 and forecasts developments from 2025 to 2034, examining how e-commerce growth, regulatory mandates, and environmental initiatives are shaping market dynamics. This report is an essential resource for industry professionals seeking insights into high-performance label materials, adhesive technologies, and digital solutions, while evaluating the competitive landscape of leading players. Analysis reviews the impact of RFID and NFC integration, wash-off adhesives, linerless technologies, and short-run printing on market growth. Key trends such as circular economy adoption, carbon footprint reduction, and packaging compliance are explored alongside sector-specific developments in food & beverages, pharmaceuticals, cosmetics, and retail logistics. The report also highlights strategic developments, including acquisitions, joint ventures, and sustainability initiatives undertaken by major companies. USDAnalytics provides detailed profiles and competitive analyses of 15+ companies, including Avery Dennison, CCL Industries, Multi-Color Corporation, UPM Raflatac, Lintec Corporation, and Fuji Seal, offering actionable intelligence for investors, converters, and brand owners navigating the evolving self-adhesive labels market.

Scope Highlights:

- Segmentation: By Product Type (Release-Liner Labels, Linerless Labels), By Material Type (Paper-based, Plastic-based, Foil-based), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Consumer Durables, Retail & Logistics, Other Industries), By Printing Technology (Flexography, Digital Printing, Screen Printing, Letterpress, Gravure)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Historic data from 2021 to 2024; forecast data from 2025 to 2034

- Companies: Analysis/profiles of 15+ major players, including Avery Dennison Corporation, CCL Industries Inc., Multi-Color Corporation, Fuji Seal International, UPM Raflatac, Lintec Corporation, SATO Holdings, 3M Company, R.R. Donnelley, All4Labels Global Packaging, Toray Industries, Labelmakers Group, Herma, Mondi Group, Quad/Graphics

Methodology

The research methodology integrates primary data collection from industry experts, converters, and brand owners with secondary research from company filings, trade associations, sustainability reports, and regulatory documents to ensure robust insights. USDAnalytics applies both quantitative and qualitative analyses, including market sizing, CAGR estimation, end-use segmentation, and technology adoption assessment. A bottom-up approach evaluates production capacities, material utilization, and regional supply contributions, cross-verified with top-down forecasts for global demand. Technological trends such as digital printing, RFID/NFC integration, functional adhesive performance, and sustainability initiatives are modeled for impact on growth and adoption. The methodology also incorporates scenario planning, regulatory compliance evaluation, and competitive benchmarking to provide actionable intelligence for strategic decision-making in the self-adhesive labels market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.