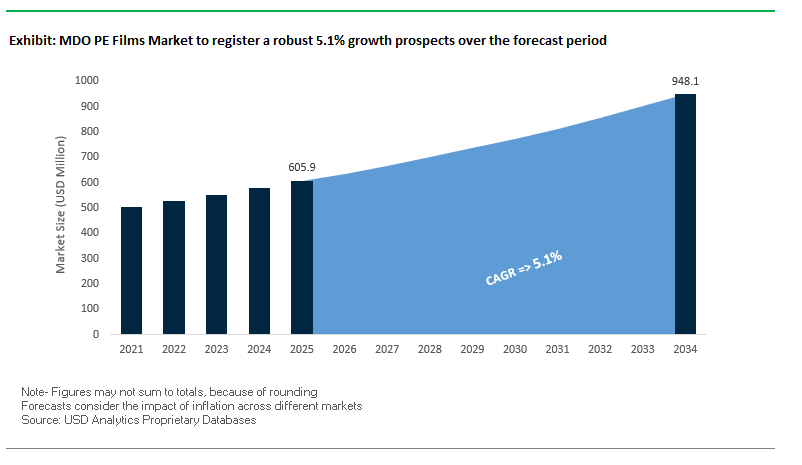

The MDO PE Films Market is projected to reach $605.9 million in 2025 and grow steadily to $948 million by 2034, reflecting a CAGR of 5.1%

This growth trajectory is underpinned by the rising demand for recyclable and downgauged films that balance cost efficiency with sustainability. MDO (Machine Direction Orientation) technology significantly enhances the mechanical properties of polyethylene films, making them competitive alternatives to multi-material laminates in packaging.

Industry professionals are increasingly turning to mono-material packaging solutions as global regulations push for reduced carbon footprints and higher recyclability. With the ability to cut emissions by nearly 30%, according to European trials, MDO PE films present both an environmental and economic advantage. Furthermore, new technology enabling stable production of 18 µm films instead of conventional 20–25 µm thickness highlights the sector’s emphasis on resource efficiency.

Key Insights for Industry Buyers and Investors

- Mechanical superiority: MDO PE films achieve modulus values above 1,000,000 psi, doubling PET film performance.

- Carbon footprint reduction: Mono-material MDO PE films cut emissions by ~30%.

- Downgauging potential: Latest processes enable stable production of ultra-thin 18 µm films.

- Recyclability advantage: Compatible with existing PE recycling streams, unlike multi-material laminates.

Market Analysis: Recent Developments Strengthening Competitive Edge

The global MDO PE Films market is witnessing transformative momentum with innovations, partnerships, and strategic expansions by leading players. A notable trend is the integration of recyclability with performance improvements, aligning with the sustainability commitments of global packaging leaders.

In August 2025, Amcor and Flügger launched a paint container with 50% recycled material, reinforcing circularity in packaging applications. Around the same time, Mondi ramped up production of its FunctionalBarrier Paper Ultimate, a direct competitive technology to MDO PE films, emphasizing the market’s broader shift toward sustainable packaging alternatives. Also in July 2025, Borouge Group International acquired Nova Chemicals for $13.4 billion, marking one of the largest consolidations in the plastics materials sector, with implications for MDO PE value chains.

On the technology front, June 2025 saw Reifenhäuser Blown Film and Cast Sheet Coating introduce new MDO technologies that enable process-stable 18 µm mono-material films. These advances are accelerating recyclability adoption in food and non-food packaging. In March 2025, LG Chem entered the cosmetics sector with UNIQABLE™, a fully recyclable mono-material barrier solution for beauty packaging, demonstrating how MDO-compatible innovation is spreading into adjacent industries.

Earlier developments also continue to shape the market. In July 2024, Mondi debuted its FlexiBag Reinforced for pet food packaging with customizable PCR content, while in November 2023, Berry Global launched Omni® Xtra+ cling film with 25% downgauging versus PVC. The RKW Group, in May 2023, expanded its ECORE® portfolio with RKW Horizon® MDO PE films, underscoring the competitive dynamism of the market.

Key Trends and Growth Opportunities in the MDO PE Films Market

Rapid Adoption Driven by Demand for Plastic Reduction and Lightweighting

The MDO PE (Machine Direction Oriented Polyethylene) films market is rapidly expanding as brand owners and converters embrace the technology to meet ambitious plastic reduction targets and regulatory mandates. This transition is being driven by both consumer pressure for sustainable packaging and legally binding commitments around recyclability. Nestlé’s pledge to achieve 95% recyclable packaging by 2024 underscores the central role MDO PE films play in delivering mono-material solutions that can replace hard-to-recycle laminates. Lightweighting is another key factor: MDO technology enables film thickness reduction of 20–30% without compromising performance, translating into direct cost savings and a reduced environmental footprint. Furthermore, regulations such as Japan’s Plastic Resource Circulation Act, mandating 60% recyclable or reusable plastic packaging by 2030, are accelerating adoption across high-volume categories such as snack foods and detergent sachets. This combination of sustainability pledges, cost optimization, and regulatory enforcement firmly positions MDO PE films as a cornerstone of next-generation packaging.

Technological Advancements in High-Barrier and Functional MDO PE Films

Innovation in material science is elevating MDO PE films from simple recyclable alternatives to high-performance substrates capable of competing with BOPP, BOPET, and metallized films. Companies are investing heavily in barrier coatings, resin engineering, and mono-material structures to ensure that MDO PE films can deliver the oxygen and moisture resistance required for sensitive food and consumer applications. Henkel and ExxonMobil’s collaboration has yielded a recyclable mono-material PE pouch with advanced oxygen barrier coatings, achieving both functionality and recyclability. Similarly, NOVA Chemicals’ SURPASS® HPs267-AB resin has enhanced water-vapor transmission performance by 20%, enabling the replacement of metallized laminates in moisture-sensitive applications. Innovations extend to recycled content integration, with INEOS successfully producing an MDO film containing over 50% recycled waste, demonstrating scalability for circular economy objectives. These technological leaps are solidifying MDO PE films as versatile, high-barrier packaging materials that can balance performance with recyclability.

Expansion into the Fresh and Chilled Food Packaging Segment

The growing demand for sustainable fresh and chilled food packaging presents one of the largest opportunities for MDO PE films. Retailers are under increasing pressure to reduce their environmental footprint, with scorecards that prioritize recyclability and sustainability, creating a strong market pull for alternatives to PVC and PS trays. High-barrier MDO PE films extend shelf life by offering superior oxygen and moisture protection, thereby reducing spoilage and food waste. For perishable goods such as meat, poultry, and dairy, these films provide a reliable barrier that preserves quality and enhances product safety. In Brazil, moisture-retentive PE films have even been shown to improve soybean yields by 15%, showcasing their functional effectiveness in agricultural applications as well. With their clarity, toughness, and barrier performance, MDO PE films are increasingly positioned as the go-to solution for retailers and food brands transitioning away from less sustainable substrates in chilled and fresh food markets.

Capitalizing on E-commerce and Industrial Packaging Demands

E-commerce and industrial packaging are emerging as high-growth frontiers for MDO PE films due to their combination of strength, durability, and lightweighting benefits. The e-commerce sector, with its demanding logistics and higher risk of product damage, requires packaging materials that offer puncture resistance and tear strength. Amazon’s 2022 adoption of moisture-resistant MDO PE mailers resulted in a 25% reduction in damaged shipments, highlighting the material’s value in high-volume operations. Beyond durability, MDO PE’s lightweight properties reduce shipping costs and fuel consumption, enabling companies to achieve both cost savings and carbon reduction. These films are also gaining traction in protective applications such as bubble wraps and water-resistant packaging for sensitive electronics, offering additional resilience in global supply chains. With rising pressure on e-commerce and industrial players to minimize plastic waste, MDO PE films offer a scalable solution that combines performance with circular economy compliance.

Competitive Landscape: Leading Global Players in MDO PE Films Market

The global MDO PE Films industry is dominated by packaging and material science leaders who are innovating to enhance recyclability, downgauging, and performance characteristics. Their strategies converge on sustainability, circular economy integration, and material substitution to reduce dependency on non-recyclable laminates.

Amcor plc: Driving Sustainability with AmSky Blister System

Amcor stands at the forefront of recyclable packaging innovation. Its AmSky Blister System, a mono-material PE blister solution, eliminates aluminum and PVC while remaining compatible with existing recycling streams. The company is deeply focused on meeting its 2025 commitment to make all packaging recyclable or reusable. By leveraging global sustainability teams and designing recycle-ready films compatible with customer machinery, Amcor eases transitions to circular packaging.

Jindal Films: Expanding BOPE Innovation with Ethy-Lyte™

Jindal Films is advancing sustainable solutions with its Ethy-Lyte™ BOPE films, engineered for mono-material recyclable structures. Its strategy is to replace mixed-plastic laminates with PE-based films aligned with CEFLEX guidelines. The company is also expanding manufacturing capacity, including a new BOPE line in Brindisi, reinforcing its commitment to innovation and supply growth in sustainable flexible packaging.

Mondi Group: Scaling Sustainable PE-Based Packaging Solutions

Mondi has positioned itself as a leader in recyclable mono-PE solutions, with its FlexiBag Reinforced addressing pet food packaging challenges by combining PCR content with puncture resistance. The company’s strategy emphasizes sustainable-by-design solutions under its re/cycle and re/loop portfolios. Its films are engineered for compliance with recyclability standards and can serve a wide variety of applications, from lamination to pouch converting.

SABIC: Enabling Circularity with TRUCIRCLE™ Portfolio

SABIC, while not directly manufacturing films, plays a critical role as a polyethylene supplier to converters. Its TRUCIRCLE™ portfolio, offering recycled and bio-based materials, directly supports MDO PE films manufacturers in reducing carbon footprints. Through collaborations across the packaging value chain, SABIC enables lightweighting, cost savings, and recyclability while leveraging its six innovation centers to accelerate new product development.

Berry Global Inc.: Pioneering Recyclable and Downgauged Cling Films

Berry Global’s innovations, such as Omni® Xtra+ cling film, demonstrate its focus on downgauging and recyclability. By reducing weight by 25% compared to PVC while enhancing elasticity and durability, Berry Global is setting benchmarks in sustainable packaging. Its broader portfolio spans pharmaceutical and healthcare packaging, and the company remains committed to advancing circular plastics through partnerships and R&D in recyclable flexible films.

MDO PE Films Market Share Insights

Cast Films Dominate Market Share by Manufacturing Process

Cast films hold the majority share in the MDO PE films market, capturing 65% of industry volume in 2025. This dominance stems from the process’s ability to deliver superior optical clarity, uniform thickness control, and faster line speeds — features that directly support the high-volume packaging demands of food, beverages, and healthcare sectors. Cast film lines are not only more efficient but also better aligned with downgauging strategies, enabling converters to reduce resin consumption while maintaining stiffness and barrier performance. This positions cast films at the center of sustainability-driven packaging transformation, where brand owners seek scalable, mono-material solutions compatible with recycling streams. Their entrenched infrastructure advantage further widens the adoption gap, as cast technology integrates seamlessly into existing global packaging supply chains.

Food & Beverages Secure Leading Market Share by End-Use Industry

The food and beverages sector commands the largest market share for MDO PE films, accounting for over half of total demand. Its dominance is tied to the global push for recyclable mono-material pouches, bags, and wraps, where MDO PE replaces complex multilayer laminates. Beyond recyclability, the material’s mechanical strength, moisture resistance, and transparency make it indispensable for retail-ready packaging, stand-up pouches, and frozen food formats. Regulatory frameworks such as the EU’s PPWR and the U.S. state-level plastics legislation amplify this transition, forcing FMCG leaders to redesign packaging portfolios around MDO-based structures. With multinational brands prioritizing shelf appeal, speed-to-market, and compliance simultaneously, the food industry is consolidating its position as the undisputed driver of MDO PE film demand through 2025 and beyond.

United States: Rising Sustainability and Technological Innovation Driving MDO PE Films Demand

The U.S. MDO PE films market is experiencing accelerated growth, fueled by consumer and corporate demand for sustainable, high-performance, and recyclable films. Rising awareness of environmental responsibility is creating a strong preference for mono-material packaging, particularly across food, pharmaceutical, and packaging industries. Companies are increasingly adopting cost-effective solutions that maintain packaging integrity while enhancing recyclability.

Technological advancements are reshaping production processes, with advanced film stretching technologies at the forefront. In June 2025, RKW Group launched new MDO-PE films with an integrated EVOH barrier under its RKW Horizon range, optimized for sustainable packaging applications. Additionally, major brand owners, including Mars Wrigley Europe, are transitioning to recyclable candy wrappers made from MDO PE films, stimulating converter investments and capacity expansion. Retailers and e-commerce giants are further driving the trend toward downgauging—reducing film thickness—to meet sustainability targets, highlighting MDO PE films as a critical enabler of corporate ESG (Environmental, Social, and Governance) goals.

Germany: Regulatory Stringency and Circular Economy Leadership Propel MDO PE Films

Germany’s MDO PE films industry is strongly influenced by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates eco-friendly, fully recyclable packaging solutions. The country’s leadership in the circular economy drives close collaboration between manufacturers and end-users, ensuring innovations align with sustainability targets.

Technological breakthroughs are a key market driver. In June 2024, ExxonMobil partnered with Hosokawa Alpine, Henkel, Nordmeccanica Group, and Univel to develop a high-barrier, recyclable MDO-PE/PE laminate suitable for diverse food products. Additionally, in May 2024, Reifenhäuser Blown Film introduced the world’s first 18-micrometre MDO-PE film, reducing material usage by 25% while enabling fully recyclable mono-material flexible packaging. These innovations, combined with government mandates for waste reduction and enhanced recyclability, position Germany as a global leader in sustainable MDO PE films.

China: Carbon Neutral Goals and Technological Integration Accelerate MDO PE Films Market

China’s MDO PE films market is being shaped by governmental initiatives aimed at achieving dual carbon goals—carbon peak and carbon neutrality. These policies are driving a green transformation across the packaging sector, promoting eco-friendly, reduced, and reusable materials. Additionally, the ban on unsorted solid waste imports has encouraged domestic manufacturers to source raw materials locally, boosting domestic production capacity and sustainability efforts.

Technological advancement is a significant growth driver. Chinese manufacturers are heavily investing in automation, AI, and “5G plus industrial internet” integration, enhancing production efficiency and enabling flexible MDO PE film manufacturing. Policy enforcement to limit non-degradable plastics in the express delivery sector by 2025 is expected to further stimulate demand for high-quality, recyclable MDO PE films, positioning China as a key contributor to global sustainable packaging growth.

India: E-commerce Expansion and Government Sustainability Drives MDO PE Films Adoption

India’s MDO PE films market is witnessing rapid expansion, driven by growth in food processing and e-commerce sectors. The demand for affordable, protective, and eco-friendly packaging, particularly for ready-to-consume and liquid products, has surged. Indian dairy firms, for instance, have begun commercially using MDO laminates for liquid pouches, highlighting the adoption of advanced packaging solutions in domestic supply chains.

Government initiatives such as the Plastic Waste Management (Amendment) Rules are phasing out single-use plastics and encouraging the use of eco-friendly, reusable alternatives, directly benefiting the MDO PE films industry. Technological advancements, including blown film technologies, are enabling manufacturers to produce films with low gauge and superior mechanical properties, improving efficiency and product performance. Furthermore, the India Plastics Pact promotes a circular plastics economy, aiming for 100% of plastic packaging to be reusable, recyclable, or compostable by 2030, reinforcing the long-term sustainability prospects for the MDO PE films market in India.

MDO PE Films Market Report Scope

MDO PE Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$605.9 Million

|

|

Market Size (2034)

|

$948 Million

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Material Type (HDPE, LDPE, LLDPE, PP, PA, EVOH, Other Materials), By Manufacturing Process (Blown Films, Cast Films), By Application (Bags & Pouches, Shrink Labels, Wraps & Liners, Tapes, Other Applications), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Homecare, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Group, Inc., Dow Inc., Jindal Poly Films Limited, Mondi Group, Tekni-Plex, Inc., Avery Dennison Corporation, Alpla-Werke Alwin Lehner GmbH & Co KG, Rani Plast Oy, Taghleef Industries, Toray Plastics (America), Inc., Innovia Films (CCL Industries Inc.), ExxonMobil Chemical Company, Mitsui Chemicals, Inc., Polyplex Corporation Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

MDO PE Films Market Segmentation

By Material Type

- HDPE

- LDPE

- LLDPE

- PP

- PA

- EVOH

- Other Materials

By Manufacturing Process

By Application

- Bags & Pouches

- Shrink Labels

- Wraps & Liners

- Tapes

- Other Applications

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Homecare

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in MDO PE Films Market

- Amcor plc

- Berry Global Group, Inc.

- Dow Inc.

- Jindal Poly Films Limited

- Mondi Group

- Tekni-Plex, Inc.

- Avery Dennison Corporation

- Alpla-Werke Alwin Lehner GmbH & Co KG

- Rani Plast Oy

- Taghleef Industries

- Toray Plastics (America), Inc.

- Innovia Films (CCL Industries Inc.)

- ExxonMobil Chemical Company

- Mitsui Chemicals, Inc.

- Polyplex Corporation Ltd.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global MDO PE Films market, analyzing breakthroughs in mono-material film technologies, downgauging capabilities, high-barrier functional solutions, and sustainability-driven innovations. The analysis reviews historical trends from 2021 to 2024 and projects market developments from 2025 to 2034, highlighting how regulatory pressures, circular economy adoption, and consumer demand for recyclable packaging are shaping industry strategies. This report is an essential resource for industry professionals seeking insights into technological advancements such as 18 µm film production, oxygen and moisture barrier enhancements, and recycled content integration. It emphasizes competitive developments, including strategic partnerships, acquisitions, and capacity expansions, while examining end-use sectors like food & beverages, pharmaceuticals, cosmetics, and industrial packaging. USDAnalytics provides in-depth profiles of 15+ leading companies, including Amcor, Berry Global, Jindal Films, Mondi Group, and ExxonMobil Chemical, evaluating their innovations, sustainability initiatives, and market positioning. The study further explores regional dynamics across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, offering actionable intelligence for investors, converters, brand owners, and procurement specialists navigating the evolving MDO PE films landscape.

Scope Highlights:

- Segmentation: By Material Type (HDPE, LDPE, LLDPE, PP, PA, EVOH, Other Materials), By Manufacturing Process (Blown Films, Cast Films), By Application (Bags & Pouches, Shrink Labels, Wraps & Liners, Tapes, Other Applications), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Homecare, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Historic data from 2021 to 2024; forecast data from 2025 to 2034

- Companies: Analysis/profiles of 15+ major players, including Amcor plc, Berry Global, Dow Inc., Jindal Poly Films, Mondi Group, Tekni-Plex, Avery Dennison, Alpla-Werke, Rani Plast Oy, Taghleef Industries, Toray Plastics, Innovia Films, ExxonMobil Chemical, Mitsui Chemicals, Polyplex Corporation

Methodology

The research methodology combines primary interviews with industry stakeholders, company disclosures, trade associations, and regulatory sources, alongside secondary data from market reports, press releases, and sustainability publications to ensure data reliability. USDAnalytics applies a mix of quantitative and qualitative approaches, including CAGR estimation, market share analysis, and end-use segmentation evaluation, complemented by trend analysis of technological innovations and regulatory impacts. A bottom-up approach estimates production capacity and regional supply contributions, validated by top-down market projections for global demand. Advanced modeling techniques assess recyclability adoption, downgauging potential, and high-barrier film development, while scenario planning considers policy shifts, sustainability mandates, and supply chain disruptions. This methodology ensures accurate, actionable insights for investors, converters, and packaging professionals seeking a strategic understanding of the MDO PE Films market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.