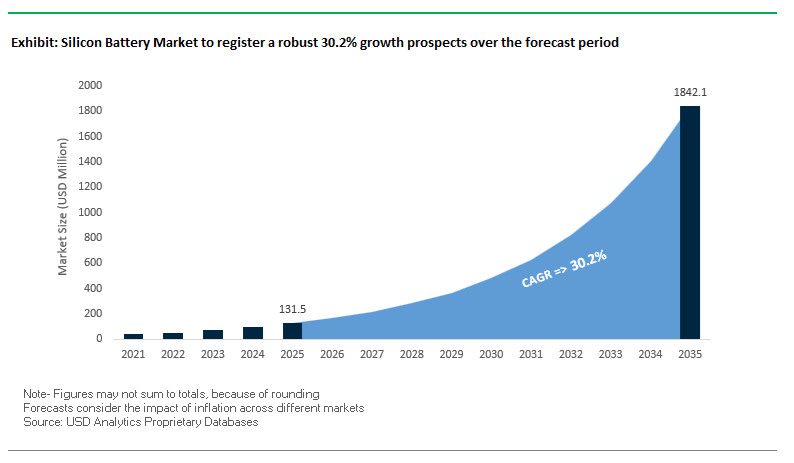

The Silicon Battery Market is projected to grow from USD 131.5 million in 2025 to USD 1,840.9 million by 2035, registering an exceptional CAGR of 30.2% as OEMs shift from conventional graphite to silicon-rich anode architectures in next-generation lithium-ion cells.

From a market analysis perspective, the Silicon Battery Market is scaling into vehicle and stationary applications Further as the global carbon fiber and advanced composite ecosystem reorganizes around sustainability, hydrogen mobility, and high-rate manufacturing. The launch of the Carbon Fiber Europe sector alliance by EuCIA in November 2025 is strategically relevant for silicon battery stakeholders because it formalizes a European industrial platform focused on resilience and circularity. As European OEMs look to combine high-energy silicon batteries with lightweight body structures, a stable continental composite supply base will be vital to meeting CO₂ targets while maintaining pack safety and stiffness.

Technology developments in high-performance fibers and thermoplastic composites also shape the design space for silicon battery integration. In November 2025, Teijin Carbon and A&P Technology launched high-performance BIMAX TPUD thermoplastic braided fabric, enabling faster cycle times and automated manufacturing of structural parts – precisely the kind of under-body trays, cross-members, and pack enclosures where next-generation silicon cells will be housed. Earlier, in October 2025, Toray Industries announced a chemical recycling breakthrough capable of decomposing CFRP waste from aircraft and wind turbines while retaining over 95% of the original fiber strength, signaling that future EV and storage products using silicon batteries can be embedded in circular composite value chains without compromising mechanical performance.

On the cost and scale front, several 2025 moves directly impact the economic feasibility of silicon battery-equipped platforms. Toray’s March 2025 decision to expand its French carbon fiber facility by 20% to 6,000 tons/year strengthens the supply of medium- and high-modulus grades for aerospace and high-end automotive, both of which are early adopters of silicon-anode cells. In parallel, Brembo and SGL’s September 2025 expansion of carbon-ceramic brake disc capacity by 50% illustrates how high-performance automotive segments are redesigning full vehicle systems—brakes, chassis, and energy storage—around lightweight, thermally robust materials, creating a natural beachhead for silicon batteries in premium models.

Sustainability-driven product launches also influence the strategic positioning of silicon batteries within broader electrification ecosystems. Teijin’s March 2025 release of Tenax Next HTS45 E23 24K, offering a 35% CO₂ reduction compared to conventional carbon fiber, aligns with OEMs trying to offset the embedded emissions of high-silicon anode production. Hexcel’s February 2025 launch of HexPly M949 cosmetic prepreg for high-quality automotive carbon parts and its January 2025 R&D collaboration with FIDAMC highlight how advanced composites are moving toward high-volume, defect-free surfaces suitable for mass-market EV exteriors, while still leveraging high-energy battery packs underneath. Finally, Asahi Kasei’s planned CFRP recycling technology for continuous fibers from pressure vessels (announced September 2025) reinforces the long-term vision where hydrogen storage cylinders, composite structures, and next-generation batteries (including silicon) all participate in closed-loop material systems rather than linear, wasteful lifecycles.

For industry professionals, the core question is no longer whether silicon batteries will commercialize, but how fast they will reach cost parity, what form factors (pouch, cylindrical, prismatic) will dominate, and which ecosystem partners will enable safe, high-energy battery packs for EVs, stationary storage, and premium consumer electronics. A critical insight for buyers is that silicon battery adoption is tightly coupled to parallel advances in carbon-based structural materials and lightweight composites for EV platforms and pressure vessels, since system-level energy density depends on both cell chemistry and pack architecture.

The underlying performance benchmarks cited for the broader advanced materials ecosystem illustrate the type of engineering envelope silicon batteries must live in. For example, PAN-based carbon fibers have already demonstrated a tensile strength ceiling of 7.677 GPa with a 362 GPa modulus in Toray’s R&D programs, defining the reference for ultra-lightweight structural components around high-energy silicon packs in aerospace and defense. Toray’s plan to raise medium- and high-modulus capacity in Europe from 5,000 to 6,000 metric tons/year by 2025 underpins the supply of composite housings and crash structures used in EVs that will increasingly integrate silicon batteries. Further, chemical recycling technology recovering >95% of virgin carbon fiber strength points to a future where high-energy silicon battery systems can be embedded in circular composite architectures, particularly for wind blades and aircraft structures approaching end of life. Sharp carbon fiber price reductions in China from USD 33/kg (2022) to USD 18/kg (2023) alter the economics of lightweighting for mass-market platforms, making it more attractive to pair silicon battery modules with affordable composite frames. Finally, the projected 42% annual growth in carbon fiber demand for Type IV hydrogen storage tanks (toward 40,000 tons by 2025) confirms the broader shift to high-pressure, lightweight energy systems – a trend that directly complements the use of silicon-based high-energy traction batteries in fuel-cell trucks and hybrid architectures.

- System-level energy density: Ultra-strong PAN-CF structures around silicon battery packs enable higher kWh per vehicle without exceeding mass targets.

- Cost and scalability: The rapid USD/kg cost decline in carbon fiber supports economically viable lightweight platforms that justify investing in premium silicon-anode cells.

- Sustainability & recycling: >95% strength retention in recycled CFRP aligns with OEM circularity roadmaps, where silicon batteries must also plug into recycled enclosures and components.

- Hydrogen and EV convergence: Carbon fiber growth in Type IV hydrogen tanks mirrors the electrification trend, creating integrated opportunities where silicon batteries and hydrogen storage co-exist on heavy-duty trucks and buses.

Trends & Opportunities: Silicon-Dominant Anode Systems, Pre-Lithiation Scaling, Binder/Additive Innovation & Precision Electrode Engineering Redefine the Silicon Battery Market

The Silicon Battery Market is entering a pivotal technology transition as global EV manufacturers, battery chemists, and equipment suppliers move toward high-content silicon anodes, industrial pre-lithiation, next-generation polymeric binders and electrolyte additives, and precision electrode manufacturing systems. These advancements aim to unlock the long-envisioned pathway to 500 Wh/kg-class batteries, marking a new era for the energy storage industry. The following section provides a fact-rich, SEO-optimized, and industry-targeted analysis of the defining trends and opportunities shaping high-silicon battery architectures.

Trend 1: Shift from Silicon-Blends to High-Content and 100% Silicon Anode Architectures in Automotive Electrification Plans

The most disruptive structural change in the Silicon Battery Market is the rapid transition from low-SiOx blends toward high-content silicon anodes, aggressively pursued to achieve >500 Wh/kg battery packs required for next-generation long-range EVs. Silicon’s unmatched theoretical specific capacity of ≈4200 mAh/g, which is over 10× higher than graphite, provides the fundamental material advantage driving this shift.

Key data-backed factors accelerating this transition include:

- Historic automotive investment cycles, as companies like Group14 Technologies secure massive capital injections such as a $463 million Series D round, aimed at scaling Si-C composite production across North America and South Korea.

- Breakthrough volumetric energy density projections, with high-silicon anode batteries positioned to surpass 1000 Wh/L at the cell level-significantly higher than the ≈800 Wh/L plateau reached by state-of-the-art lithium-ion systems.

- Superior cycle life performance, with advanced Si-C anode cells demonstrating 80%–95% capacity retention across extended testing scenarios-far exceeding the degradation seen in graphite-based electrodes under identical current density conditions.

- Material-science fundamentals confirming silicon's capacity dominance, as the lithium-rich phase (Li₄.₄Si) reaches ≈4200 mAh/g, compared to graphite’s 372 mAh/g, illustrating the exponential energy density potential driving automotive adoption.

This trend reflects a decisive industry pivot as major EV OEMs incorporate silicon-dominant anodes into their long-term platform strategies, setting the stage for a new era of ultra-high-energy EV batteries.

Trend 2: Emergence of Pre-Lithiation as an Industrial-Scale Enabler for Silicon-Based Battery Systems

The commercialization of high-silicon anodes is fundamentally linked to pre-lithiation, now emerging as the most critical scalable process for compensating silicon’s substantial initial lithium losses (ICE loss). Pre-lithiation methods aim to restore usable lithium capacity lost to SEI formation, volume expansion, and irreversible Li consumption, which otherwise limit practical energy density.

Important industry-backed achievements include:

- ICE transformation metrics, where chemical pre-lithiation (e.g., Li-Naph) increased ICE from ≈74.8% to 97.2%, enabling near-full utilization of cathode lithium.

- High-cycle stability verification, with prelithiated amorphous silicon achieving 90.1% capacity retention after 800 cycles at 1C in 27 mAh pouch cells-excellent stability for EV-grade requirements.

- Commercial adoption of scalable materials, such as Stabilized Lithium Metal Powder (SLMP), engineered to embed lithium directly into the silicon anode structure and counteract the 400% volume expansion experienced during initial lithiation.

- Patent momentum, including US20200395593A1, detailing multiple pre-lithiation manufacturing approaches-proof of accelerating industrial readiness and process integration.

This trend underscores that pre-lithiation is no longer experimental; it is becoming the defining industrial process required to unlock silicon’s full potential.

Opportunity 1: High-Value Supply of Specialized Binders and Electrolyte Additives for Silicon-Dominant Anodes

The severe >300% volumetric expansion of silicon creates a non-commodity materials market for next-generation binders and SEI-enhancing additives capable of maintaining electrode cohesion under extreme mechanical strain. These materials are essential to maintaining cycle life and safety as silicon loading increases.

Key performance benchmarks include:

- Exceptional retention with cross-linked polymer binders, such as PR-PAA, delivering 91% capacity retention after 150 cycles with micron-sized silicon.

- High-rate stability achieved through water-soluble binders, where PAA-SS allowed silicon anodes to retain 1559 mAh/g after 150 cycles at an extraordinarily high 4200 mA/g, supporting environmentally friendly electrode processing.

- Electrolyte additive advantages, with 1 wt% Vinylene Carbonate (VC) enabling silicon electrodes to sustain ≈2000 mAh/g for 200 cycles and maintain >500 mAh/g even after 500 cycles, highlighting the additive’s impact on SEI stabilization.

- Functional group engineering, as modern binders incorporate ionic, covalent, and hydrogen bonding sites to create durable adhesion with SiOH and SiOx surfaces, crucial for mitigating particle isolation and current collector delamination.

This opportunity positions chemical suppliers, specialty polymer manufacturers, and electrolyte additive innovators at the center of silicon battery commercialization.

Opportunity 2: High-Precision Coating and Calendering Equipment for Silicon Composite Electrode Manufacturing

Silicon composite electrodes exhibit low packing density, high viscosity, and structural sensitivity, creating a significant equipment opportunity for precision slot-die coaters, intelligent calendering systems, and high-throughput web handling solutions. This segment is rapidly emerging as a critical enabling technology for Gigafactory-scale silicon battery production.

Key technical requirements driving demand include:

- Micron-level calendering precision, with industry-leading systems providing ±1 μm gap accuracy, essential for uniform density and preventing localized electrochemical stress.

- High-throughput manufacturing performance, with calendering units supporting 1,500 mm web widths and 150 m/min line speeds while maintaining full accuracy-critical for EV-scale volumes.

- Electrode uniformity as a performance determinant, as silicon slurry non-uniformity impairs lithium transport and accelerates degradation, making slot-die pre-metered coating indispensable.

- Controlled densification demands, requiring calendering pressures up to 300 tons, alongside temperature-controlled rolls (10°C–200°C), to balance porosity, mechanical stability, and electrolyte accessibility without fracturing silicon domains.

This opportunity fuels demand for advanced equipment manufacturers specializing in precision electrode engineering, metrology, and continuous roll-to-roll processing.

Silicon Battery Market Share Analysis

Market Share by End-Use Application: Electric Vehicles Lead Due to Silicon’s Energy-Density Advantage and Fast-Charging Capabilities

The Electric Vehicle (EV) segment commands a dominant 65% share of the Silicon Battery Market because EV manufacturers face relentless pressure to improve driving range, charging speed, and cost efficiency, and silicon-anode batteries are the most direct technological pathway to achieving all three simultaneously. Silicon’s extraordinary theoretical specific capacity—≈3,570 mAh/g, nearly 10× greater than graphite—translates into a practical, system-level energy density boost of 20–50%, enabling automakers to increase driving range by 10–20% without altering pack size or vehicle architecture. This capacity advantage is central to overcoming the industry’s core bottleneck: maximizing energy storage per unit mass while maintaining pack safety and manufacturability. Moreover, silicon is emerging as the key enabler for Extreme Fast Charging (XFC), a non-negotiable requirement for mainstream EV adoption. Leading silicon-anode developers report charging speeds approaching 80% state-of-charge in ≤10 minutes, with next-generation cells targeting sub-5-minute recharge cycles, placing battery refill times on par with combustion refueling. Silicon also supports volumetric optimization, freeing internal volume within the cell and allowing for a larger cathode fraction—an essential characteristic for long-range EVs that depend heavily on high cathode loading. As EV battery demand accelerates toward multi-terawatt-hour scale, silicon-anode technologies provide the highest-value performance uplift per manufacturing dollar, solidifying the EV segment as the market’s primary growth engine.

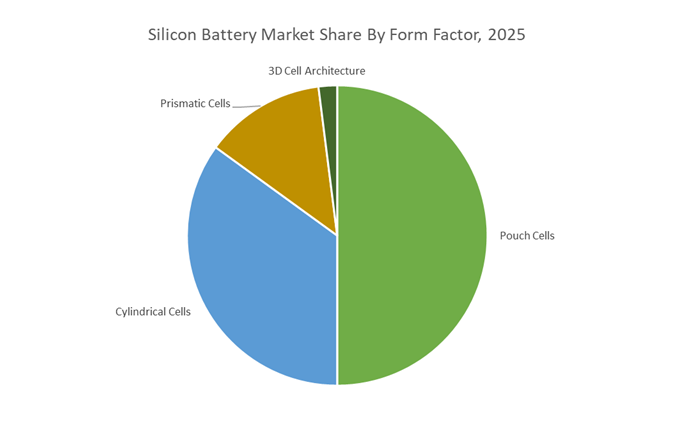

Market Share by Form Factor: Pouch Cells Dominate by Enabling Maximum Energy Density and Superior Compatibility with Silicon Anode Expansion

Pouch cells hold a 50% share of the form-factor segment because their structural architecture uniquely supports both the high-energy-density requirements and the mechanical expansion characteristics inherent to silicon anodes. Unlike cylindrical and prismatic formats, pouch cells employ a lightweight polymer-laminate casing, eliminating the rigid metal enclosure and enabling 90–95% packaging efficiency, the highest among lithium-based cell formats. This efficiency directly translates into industry-leading gravimetric and volumetric energy density (Wh/kg and Wh/L)—a decisive advantage for EV manufacturers striving to extend vehicle range without increasing battery pack size. The flexible casing of pouch cells is especially important for silicon-dominant chemistries, which undergo significant anode swelling—often up to 300% during lithiation. The pouch architecture accommodates this expansion more effectively than rigid housings, reducing electrode stress, mitigating particle fracture, and extending cycle life—an essential requirement for commercial viability of silicon-rich cells.

Furthermore, pouch cells provide a large, planar surface area, which enhances thermal dissipation during high-rate charging and discharging, a critical performance attribute for Extreme Fast Charging (XFC) systems. Their stackable, customizable form factor also gives EV OEMs substantial design freedom, enabling ultra-thin modules, curved pack geometries, and space-optimized layouts tailored to modern vehicle chassis constraints. As leading battery suppliers—such as LG Energy Solution, SK On, and Chinese innovators—scale silicon-enabled pouch cells for next-generation EVs, this form factor remains the most compatible, efficient, and strategically aligned with the performance demands driving the silicon battery market.

Country Analysis: Global Silicon Battery Technology Commercialization

United States – Silicon Anode Manufacturing Scale-Up and Defense-Grade Energy Storage Integration

The United States remains the most strategically significant hub in the global silicon battery market, driven by federal initiatives targeting domestic battery supply chain security, high-performance silicon anode production, and next-generation defense energy systems. The U.S. Department of Energy’s award of up to $100 million to Sila Nanotechnologies (2024) underscores a national commitment to securing leadership in silicon anode mass production, directly supporting the construction of the Moses Lake, Washington facility. Designed to deliver 2,300 tons/year of silicon anode material, this facility will supply enough high-capacity anode material to power hundreds of thousands of electric vehicles annually, marking a transformative shift in U.S. EV battery independence.

Commercialization momentum is equally strong across performance-driven segments. Enovix Corporation’s AI-1™ platform, unveiled in July 2025, represents a breakthrough in volumetric energy density—surpassing 900 Wh/L, now under qualification by a major global smartphone OEM. The aerospace and defense sectors are adopting silicon-anode technologies rapidly: Amprius Technologies’ 370 Wh/kg SiCore 21700 cell (2025) targets drones and light EVs requiring extreme gravimetric energy density, while Enovix continues scaling production of 3D Silicon™ Li-ion cells for U.S. Army wearable systems that demand nearly double the runtime of standard lithium-ion devices. The U.S. remains a critical technology incubator for hybrid solutions, highlighted by QuantumScape’s anode-free solid-state architecture, which achieved over 1,000 cycles with >95% retention and fast charging from 10–80% in under 15 minutes. Collectively, U.S. advancements cement the country’s role as a powerhouse for silicon-anode manufacturing, defense-grade storage systems, and next-generation battery commercialization.

China – Cost-Parity Silicon-Graphite Composites and EV Market Acceleration

China is rapidly scaling its position in the global silicon battery ecosystem by driving adoption of silicon-graphite composite anodes that achieve enhanced performance while maintaining cost parity with conventional synthetic graphite. This value-driven strategy aligns with China’s mass-market EV production environment, where cost efficiency and scalable integration are essential. NanoGraf’s Onyx EV-ready material (2024) serves as a pivotal product for this transition, specifically engineered to deliver improved cycle efficiency and performance at a price point equivalent to synthetic graphite—removing one of the biggest barriers to mass deployment of silicon-based anodes.

Material innovation across China is accelerating to position the country as a dominant supplier for EVs and consumer electronics. Sunrise New Energy’s silicon-carbon anode materials, designed with a high theoretical capacity of 1800 mAh/g and an initial coulombic efficiency exceeding 91%, demonstrate China’s capability to develop high-performance composites suited for both electric vehicle platforms and premium 3C digital devices. As China continues enhancing its silicon-graphite product portfolio and streamlining high-volume production, it solidifies its role as the world’s fastest-scaling market for cost-effective silicon battery technologies.

South Korea – High-Content Silicon Integration for Premium EVs and High-End Consumer Electronics

South Korea leverages decades of advanced battery engineering expertise to drive the integration of high-content silicon anodes into premium EV cells and high-end portable electronics. Key manufacturers such as Samsung SDI are actively collaborating with specialized anode development partners while advancing their internal R&D to enhance energy density in both prismatic and pouch cell formats. These innovations complement South Korea's market strategy of serving luxury EV platforms that prioritize extended driving range, superior cycle life, and fast-charging capabilities.

A major competitive advantage for South Korean companies is their mastery of precision manufacturing and cell engineering, enabling them to effectively manage the volumetric expansion challenges inherent to silicon anodes. By implementing optimized electrode architectures and refined thermal management strategies, South Korea maintains leadership in delivering automotive-grade reliability and consumer-electronics-grade durability. This strong technological foundation positions South Korea as a global leader in commercializing high-performance silicon battery systems.

Japan – Silicon Battery Innovation for Next-Generation Miniaturized Electronics

Japan is focusing its silicon battery commercialization efforts on next-generation miniaturized electronics, where longer runtimes, rapid charging, and compact form factors are mission-critical. TDK Corporation, one of Japan’s most influential electronics component manufacturers, announced its next-generation silicon-anode batteries in January 2025, with mass production of third-generation cells scheduled to begin by late summer. These advanced cells are engineered specifically for AI-driven mobile devices, IoT ecosystems, and industrial sensors, sectors where silicon’s high volumetric energy density offers significant performance advantages.

Japan’s emphasis on material science precision, miniaturization expertise, and reliability testing ensures that its silicon-anode technologies remain highly attractive for premium electronics manufacturers. The country continues to expand its role in supplying ultra-compact, high-energy-density silicon cells to global brands seeking breakthroughs in device runtime and battery efficiency.

Germany / Europe – Automotive-Grade Silicon Materials and Scalable Anode Manufacturing

Europe is strengthening its leadership in the automotive battery materials market by investing in specialized silicon anode chemistries tailored for the region’s electrification strategy. In May 2025, BASF and Group14 Technologies introduced a market-ready silicon anode solution engineered for extreme durability, capable of operating under high-stress automotive thermal environments up to 113°F while enabling faster charging performance. This solution directly supports European automotive OEMs transitioning to high-power EV architectures that require long cycle life and consistent thermal stability.

Complementing this materials push, Europe is scaling proprietary silicon-anode manufacturing technologies through advanced chemical deposition processes. LeydenJar Technologies (Netherlands) is expanding production of its PECVD-based 100% silicon anode film, a highly porous structure deposited directly onto copper foil. This breakthrough technology enhances energy density significantly and positions LeydenJar as a key enabler for European EV battery supply chain independence. Europe’s combined focus on materials innovation, manufacturing scalability, and supply chain sovereignty continues to accelerate its role in the global silicon battery landscape.

Competitive Landscape: Advanced Material Leaders Shaping Silicon Battery Platform Design

The competitive landscape for the Silicon Battery Market is still dominated by emerging cell specialists and established lithium-ion incumbents, but the platform economics and pack engineering are heavily influenced by a small group of advanced carbon fiber and composite suppliers. Companies including Toray, Hexcel, Teijin, SGL Carbon, and Mitsubishi Chemical Group provide the structural backbone for battery enclosures, crash structures, pressure vessels, and lightweight body components, which ultimately determine how much of the silicon battery’s intrinsic energy density can be translated into usable range and payload. For industry professionals, understanding these players is critical to assessing the real-world deployability of high-energy silicon-anode solutions in EVs, aerospace, hydrogen mobility, and high-performance industrial systems.

Toray Industries stands out as the benchmark supplier for ultra-high-performance carbon fibers that underpin the most advanced silicon battery platforms. Its flagship T1100G fiber guarantees 7.0 GPa tensile strength, with R&D records reaching 7.677 GPa, enabling extremely lightweight yet robust frames and battery enclosures for aerospace and performance EVs. Strategically, Toray is betting on hydrogen mobility and has forecast that carbon fiber demand for Type IV hydrogen tanks will grow 42% annually, reaching roughly 40,000 tons by 2025, which dovetails with the adoption of silicon batteries in fuel-cell hybrid vehicles. The company is also expanding European capacity—raising medium- and high-modulus output in France to 6,000 tons/year by 2025—giving regional EV and aircraft OEMs a secure source of high-grade structural materials to pair with next-generation high-energy cells. Its chemical recycling innovation, retaining >95% of original fiber strength, is particularly synergistic with silicon battery sustainability narratives, allowing pack structures to be recycled without major mechanical compromises.

Hexcel is a dominant name in aerospace composites, and its strategic posture has direct implications for the deployment of silicon batteries in aviation and defense platforms. The company estimates that its backlog with Airbus and Boeing programs (A350, 787, etc.) represents roughly USD 10 billion in future commercial aerospace sales, reflecting the long-term integration of lightweight composite structures where high-energy storage (including silicon-based systems) will increasingly be required for hybrid-electric aircraft concepts. Hexcel’s Defense, Space & Other segment grew 7.6% year over year in Q2 2025, demonstrating diversified demand across more than 100 defense programs—many of which are exploring high-specific-energy power sources. On the product side, HexPly M949 cosmetic prepreg, launched in February 2025, achieves Class A automotive surfaces at 150°C Tg, ideal for visible composite parts on EVs that may house silicon battery modules below. Hexcel’s commitment that 75% of its R&T projects will deliver sustainability benefits by 2030 aligns tightly with OEM expectations that new battery chemistries must fit within low-carbon, recyclable vehicle architectures.

Teijin is a key integrated supplier of high-tensile (HTS) and intermediate-modulus (IMS) carbon fibers, including Tenax HTS40 (4.0 GPa) and Tenax IMS (5.5 GPa), widely used in aircraft and utility-scale wind blades that are increasingly co-deployed with large battery systems. For the silicon battery ecosystem, Teijin’s impact is strongest where sustainable lightweight structures are needed at automotive scale. The Tenax Next HTS45 filament yarn, launched in March 2025, provides a 35% CO₂ reduction versus incumbent fibers, supporting OEMs that must offset the higher embodied energy of silicon-rich anode production. Teijin also moves aggressively into thermoplastic composites, partnering to release BIMAX TPUD braided fabric in November 2025, designed for high-volume, automation-friendly composite components around battery packs and crash structures. Its Nadcap certification (July 2025) for carbon fiber production confirms aerospace-grade process control, making Teijin a trusted partner for future hybrid-electric aircraft platforms that may require light, stiff mounting structures for silicon batteries.

SGL Carbon delivers tangible proof that carbon composite parts can be manufactured at high automotive volumes, which is critical for mainstream adoption of silicon batteries in passenger vehicles. The company manufactures around 500,000 composite leaf springs annually for Volvo 60 and 90 series, demonstrating a 65% weight reduction versus steel and showcasing how structural mass savings can be redeployed into larger kWh silicon packs without exceeding axle load limits. In performance applications, the BSCCB joint venture expanded carbon-ceramic brake disc capacity by 50% in September 2025, matching the braking needs of heavier, high-power EVs that might use silicon-anode batteries for extended range. SGL is also diversifying into energy storage, launching a carbon fiber battery felt for Redox Flow Batteries in June 2025, extending its expertise beyond structural composites. The company’s recognition via the Ford Q1 award in May 2025 underscores its reliability as a Tier-1 supplier—an important signal for automakers planning to combine its lightweight structures with new generations of high-energy silicon cells.

Mitsubishi Chemical Group brings a unique pitch-based carbon fiber portfolio under its DIALEAD brand, offering ultra-high modulus (>500 GPa) and high thermal conductivity grades that are particularly relevant for thermal management around high-energy silicon batteries. Such fibers can be used in heat spreaders, busbar reinforcement, and structural components that manage the higher heat flux associated with silicon-dominant anodes. On the processing side, the group has been showcasing Kyron ULTRA thermoplastic CF prepregs (December 2025) designed for high-speed manufacturing of e-mobility structures, allowing OEMs to integrate structural and protective layers around silicon battery modules in mass production. Mitsubishi’s Fusion Core Molding (FCM) technology enables complex 3D hollow CF parts, ideal for stiff yet lightweight frames, cross-members, and battery protection beams. At the SAMPE Japan 2025 exhibition, the company also emphasized plant-derived epoxy resin/CF composites and CFRP recycling technology, underscoring that advanced silicon battery platforms will be deployed in vehicles and aircraft that are themselves built from low-carbon, recyclable composite materials.

Silicon Battery Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$131.5 Million

|

|

Market Size (2035)

|

$1840.9 Million

|

|

Market Growth Rate

|

30.2%

|

|

Segments

|

By Anode Type (Silicon-Graphite Composite Anodes, Pure Silicon Anodes, Silicon Oxide Anodes, Nanostructured Silicon Anodes, Graphene-Silicon Composites), By Electrolyte (Liquid Electrolyte Batteries, Solid-State Silicon Batteries, Quasi-Solid-State Batteries), By Capacity (Low Capacity, Medium Capacity, High Capacity), By End-Use Application (Electric Vehicles, Consumer Electronics, Aerospace & Drones, Medical Devices, Industrial & Grid Energy Storage), By Form Factor (Pouch Cells, Cylindrical Cells, Prismatic Cells, 3D Cell Architecture)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sila Nanotechnologies Inc., Enovix Corporation, Group14 Technologies, Amprius Technologies Inc., Enevate Corporation, Nexeon Ltd., QuantumScape Corporation, TDK Corporation, LG Energy Solution, Samsung SDI Co. Ltd., LeydenJar Technologies BV, NanoGraf Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicon Battery Market Segmentation

By Anode Type

- Silicon-Graphite Composite Anodes

- Pure Silicon Anodes

- Silicon Oxide (SiOx) Anodes

- Nanostructured Silicon Anodes (Nanowires, Nanoparticles)

- Graphene-Silicon Composites

By Electrolyte

- Liquid Electrolyte Batteries

- Solid-State Silicon Batteries

- Quasi-Solid-State Batteries

By Capacity

- Low Capacity (< 3,000 mAh)

- Medium Capacity (3,000–10,000 mAh)

- High Capacity (> 10,000 mAh)

By End-Use Application

- Electric Vehicles (EV)

- Consumer Electronics (Smartphones, Laptops, Wearables)

- Aerospace & Drones

- Medical Devices

- Industrial/Grid Energy Storage (ESS)

By Form Factor

- Pouch Cells

- Cylindrical Cells (21700, 4680)

- Prismatic Cells

- 3D Cell Architecture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Silicon Battery Developers and Suppliers

- Sila Nanotechnologies, Inc.

- Enovix Corporation

- Group14 Technologies

- Amprius Technologies, Inc.

- Enevate Corporation

- Nexeon Ltd.

- QuantumScape Corporation

- TDK Corporation

- LG Energy Solution (LGES)

- Samsung SDI Co., Ltd.

- LeydenJar Technologies BV

- NanoGraf Corporation

*- List not Exhaustive