Specialty Nitriles Market Valuation 2025–2034: $2.8 Billion to $4.8 Billion at 6.1% CAGR Amid ADN Overcapacity, Bio-Acrylonitrile Innovation, and High-Purity Electronics Shift

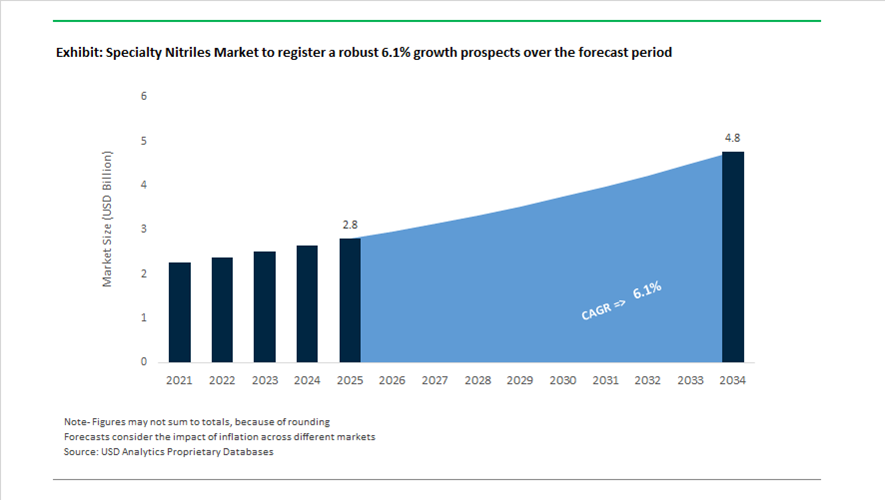

The global specialty nitriles market is valued at $2.8 billion in 2025 and is projected to reach $4.8 billion by 2034, expanding at a CAGR of 6.1%. Growth is driven by demand for high-purity acrylonitrile, adiponitrile (ADN), acetonitrile, hydrogenated nitrile intermediates, and specialty nitrile elastomers used in carbon fiber production, EV components, pharmaceuticals, agrochemicals, and animal nutrition. Specialty nitriles command premium pricing due to strict purity thresholds, controlled polymerization behavior, and performance requirements in electronics, battery systems, and high-strength composite materials. The market is undergoing structural transformation as sustainability mandates, Chinese production overcapacity, and vertical integration reshape supply chains.

In April 2024, INEOS Nitriles launched commercial sales of Invireo™ bio-based acrylonitrile and acetonitrile, reporting up to 90% lower carbon footprint compared to fossil-based equivalents, with qualification in carbon fiber and pharmaceutical applications. In April 2024, LG Chem secured ISCC PLUS certification across its bio-circular balanced NBR latex value chain, accelerating adoption of sustainable nitrile elastomers in industrial and medical sectors. In December 2024, Ascend Performance Materials produced bio-circular acrylonitrile and nylon 6,6 using used cooking oil feedstocks. During 2024–2025, Adisseo completed its 30KT European specialty optimization project and achieved mechanical completion of its 37KT specialty blending facility in Nanjing, strengthening production of nitrile-based intermediates for animal nutrition. In March 2024, construction began on a new HNBR plant in Changzhou, targeting 2,500 tons of initial production by Q3 2025.

Market volatility intensified in 2025. In March 2025, Sumitomo Chemical launched its 2025–2027 “V-Shaped Recovery” plan, divesting non-core petrochemical assets to concentrate on ICT and mobility segments, including specialty nitrile elastomers for EV platforms. In April 2025, Ascend Performance Materials filed for Chapter 11 bankruptcy protection, citing Chinese overcapacity in ADN and HMD along with operational disruptions. In May 2025, shortly after the filing, Ascend commenced high-purity acrylonitrile production at its Alvin, Texas facility, pivoting toward electronics and specialty chemical markets rather than commodity nylon. In May 2025, Arlanxeo and TSRC opened their expanded Nantong nitrile rubber plant, increasing capacity by 33% to support high-performance Perbunan® specialty nitriles.

Biotechnology integration and decarbonization are influencing long-term innovation pathways. The January 2024 formation of Novonesis through the merger of Novozymes and Chr. Hansen strengthens enzymatic R&D capabilities, including potential biocatalytic routes for nitrile-based intermediates. Expansion of bio-acrylonitrile platforms, ISCC PLUS-certified nitrile latex, HNBR capacity growth in China, and restructuring among ADN producers are redefining competitive positioning. These shifts toward high-purity electronics-grade nitriles, sustainable feedstocks, EV-driven elastomer demand, and carbon-reduced production routes are shaping the specialty nitriles market trajectory toward $4.8 billion by 2034.

Strategic Trends and High-Impact Opportunities in the Specialty Nitriles Market

Blockbuster GLP-1 Drug Manufacturing Drives Structural Demand for High-Purity Nitrile Intermediates

The explosive global uptake of GLP-1 receptor agonists for diabetes and obesity management has fundamentally reshaped demand patterns in the specialty nitriles market. Advanced peptide therapeutics such as semaglutide, tirzepatide, and emerging oral candidates rely on highly engineered nitrile intermediates, including protected aminoacetonitriles and heterocyclic nitriles, to construct unnatural amino acids and lipid-linker side chains. These molecular components are essential for achieving prolonged half-life and once-weekly dosing profiles, making nitriles a non-substitutable input in next-generation metabolic drugs.

This demand surge is directly reflected in upstream capacity investments. In November 2025, Eli Lilly reported a 54% year-on-year revenue increase in Q3, largely attributed to its GLP-1 portfolio. To support both injectable and oral pipelines such as orforglipron, the company is executing a $3 billion manufacturing expansion that includes secured sourcing of high-purity chemical intermediates. Within this expansion, specialty nitriles are critical for multi-step condensation and coupling reactions that define peptide scaffold construction.

Contract Development and Manufacturing Organizations are similarly recalibrating capital priorities. By late 2025, leading CDMOs such as Piramal Pharma indicated that GLP-1 programs had become the single largest driver of investment in dedicated nitrile-handling reactor suites. These facilities emphasize ultra-low impurity profiles, controlled cyanation steps, and GMP-compliant purification, signaling a durable, long-cycle growth trend for pharmaceutical-grade specialty nitriles.

Low-VOC Regulations Accelerate Adoption of Nitrile-Derived Acrylates in Coatings

Environmental compliance has become a decisive force in coatings chemistry, pushing specialty nitriles into the spotlight as enablers of low-VOC and high-solids formulations. The U.S. EPA’s January 2025 updates to the National VOC Emission Standards and the subsequent July 2025 Interim Final Rule have established a firm compliance deadline of January 17, 2027. This regulatory timeline has created a mandatory reformulation window for automotive and industrial coating manufacturers.

To meet reactivity-based VOC limits without sacrificing durability, formulators are increasingly turning to nitrile-derived acrylic monomers. These materials enable higher crosslink density, superior adhesion, and enhanced chemical resistance at significantly reduced solvent volumes. The influence of California’s SCAQMD Rule 1113, which caps VOC content below 50 g/L, has effectively become the global benchmark, shaping reformulation strategies well beyond North America.

Major coatings players such as Sherwin-Williams and PPG are increasingly specifying specialty nitrile-based acrylates to maintain film integrity in harsh industrial environments. This trend embeds nitriles deeper into performance coatings supply chains, transforming them from optional additives into compliance-critical building blocks.

High-Voltage Nitrile Electrolytes Enable Next-Generation Lithium-Ion Batteries

Electrification trends are opening a high-margin opportunity for specialty nitriles in advanced battery electrolytes. As lithium-ion batteries evolve toward high-nickel cathodes and silicon-dominant anodes, traditional carbonate solvents are approaching their oxidative and thermal limits. Dinitriles such as adiponitrile are emerging as enabling solvents due to their high flash points, wide electrochemical stability windows above 4.5V, and intrinsic resistance to thermal runaway.

In September 2025, research updates referenced by the U.S. Department of Energy highlighted a strategic pivot toward non-carbonate electrolyte systems for both grid-scale storage and high-performance EV batteries. Nitrile-based electrolytes are now central to improving Solid Electrolyte Interface stability, particularly in high-voltage and lithium-metal cell architectures.

Battery material developers have also reported that nitrile additives materially increase thermal runaway thresholds, directly enhancing safety metrics for next-generation cells. This positions electronic-grade, ppt-purity nitriles as a premium input for gigafactories across North America and Europe, where safety validation and regulatory scrutiny are most intense.

Commercialization of Bio-Based Acrylonitrile Unlocks Scope 3 Decarbonization

Sustainability mandates are creating a parallel growth pathway for renewable nitriles, particularly bio-based acrylonitrile. Driven by Scope 3 emissions reduction targets, polymer producers and OEMs are actively seeking drop-in solutions that lower carbon footprints without disrupting existing processing infrastructure.

A major milestone was reached in April 2024 when INEOS Nitriles launched its INVIREO brand, representing the first commercial-scale bio-based acrylonitrile produced via a certified mass-balance approach. This product delivers an estimated 90% reduction in carbon footprint compared to conventional petroleum-derived ACN, immediately positioning it as a strategic lever for downstream sustainability goals.

By October 2025, bio-based Acrylonitrile Butadiene Styrene accounted for more than 46% of global bio-nitrile consumption. Demand is being led by consumer electronics and automotive applications, where manufacturers require sustainable materials without retooling injection-molding lines. This drop-in compatibility gives bio-ACN a structural advantage, allowing specialty nitrile producers to capture a green premium while aligning with long-term decarbonization frameworks across multiple end-use industries.

Specialty Nitriles Market Share and Segmentation Insights

Nitrile Butadiene Rubber Dominates the Specialty Nitriles Market Through Automotive and Industrial Applications

Nitrile butadiene rubber accounted for 38.60% of the specialty nitriles market in 2025, making it the largest product category across nitrile-based materials. NBR offers excellent oil resistance, fuel compatibility, mechanical strength, and durability, which supports its extensive use in automotive components, industrial equipment, protective gear, and sealing products. The large-scale production of vehicles and industrial machinery continues to sustain strong global demand for NBR materials. A key 2025 industry development is the influence of automotive electrification, where NBR remains relevant in new vehicle architectures through its use in thermal management systems, battery cooling circuits, and electric drivetrain sealing applications, ensuring reliable performance in evolving automotive platforms.

Automotive Sector Drives Global Demand for Specialty Nitriles

Automotive applications represent the largest segment in the specialty nitriles market, accounting for 34.80% of global consumption in 2025 due to the extensive use of nitrile-based materials in vehicle systems. Components such as fuel hoses, transmission seals, gaskets, O-rings, and vibration dampers rely on nitrile materials for their resistance to oils, fuels, and mechanical stress. The scale of global vehicle production supports sustained consumption of specialty nitrile materials. A major 2025 industry trend is the growing focus on electric vehicle thermal management systems, where NBR and hydrogenated NBR are increasingly used in coolant hoses, sealing systems, and battery thermal control components that require compatibility with glycol-based coolants and elevated operating temperatures.

Specialty Nitriles Market Competitive Landscape

The global specialty nitriles market in 2026 is driven by bio-based acrylonitrile, high-purity acetonitrile for pharmaceuticals, and HNBR demand for EV batteries. Tier-1 players are optimizing ammoxidation efficiency, scaling integrated production, and advancing sustainable nitrile chemistries to strengthen supply security and performance applications.

INEOS Nitriles Leads Bio-Based Acrylonitrile Transition with Invireo™ and Global UHP Supply Chain Integration

INEOS Nitriles maintains global leadership in specialty nitriles through its large-scale acrylonitrile and acetonitrile production network. The Invireo™ bio-based acrylonitrile platform delivers up to 90% lower greenhouse gas emissions, targeting sustainable automotive and electronics applications. Its Jubail world-scale plant ensures cost-efficient feedstock access and stable supply for downstream derivatives. INEOS supplies ultra-high purity acetonitrile for pharmaceutical applications, including DNA/RNA synthesis and HPLC analysis. Proprietary ammoxidation catalysts introduced in 2025 improve carbon efficiency by 3%–5% across operations. Its vertically integrated logistics and production network reinforce resilience in a volatile global nitriles market.

Alzchem Expands High-Purity Nitrile Intermediates with NITRALZ® Innovation and Record €562 Million Revenue Performance

Alzchem Group AG is strengthening its position in specialty nitriles through high-purity intermediates for pharmaceuticals and defense applications. The company reported €562.1 million in 2025 sales with EBITDA rising 11% to €116.5 million, driven by its Specialty Chemicals segment. Its NITRALZ® platform utilizes advanced gas-phase synthesis to produce aromatic and aliphatic nitriles for API manufacturing. Expansion of guanidine nitrate and related derivatives in 2026 targets aerospace and defense demand growth. Its solvent-efficient production technology reduces emissions and aligns with green chemistry standards. Alzchem’s focus on precision nitrile synthesis supports high-value life science applications.

Zeon Advances HNBR and Battery Binder Applications Through Capacity Expansion and Molecular Engineering Leadership

Zeon Corporation is driving innovation in specialty nitriles through its Zetpol® HNBR portfolio and advanced polymer design capabilities. Capacity expansion in the U.S. supports increasing demand from the North American EV battery market. Its nitrile elastomers are widely used as lithium-ion battery binders, particularly for silicon-based anodes requiring enhanced mechanical strength. Under its STAGE30 strategy, Zeon is shifting toward specialty chemical ecosystems and targeting a 25% carbon footprint reduction by 2030. With over 200 patents, the company delivers customized nitrile polymers with high thermal and chemical resistance. Its R&D leadership strengthens its role in high-performance nitrile applications.

Adisseo Integrates Nitrile Chemistry into Methionine Production with 40,000-Ton Expansion and Double-Digit Specialty Growth

Adisseo is leveraging specialty nitrile chemistry as a core intermediate in amino acid production, particularly for methionine. Its 40,000-ton debottlenecking project at the Burgos plant enhances integration of nitrile processing for Rhodimet® AT88 production. The company reported double-digit growth in its specialty segment, including 13% growth in Q3 2025 revenues. Internalization of nitrile and esterification processes reduces dependence on external suppliers and improves cost efficiency. Its One-China strategy aims to localize production and optimize the nitrile-to-methionine value chain. Adisseo’s integrated approach strengthens its competitiveness in nutritional and feed additive markets.

Ascend Performance Materials Expands High-Purity Acrylonitrile and ADN Integration for EV and Advanced Material Applications

Ascend Performance Materials is strengthening its specialty nitriles portfolio through high-purity acrylonitrile production at its Gulf Coast facilities. This enables domestic supply of pharmaceutical-grade intermediates and reduces reliance on imports. The company is leveraging its adiponitrile technology to expand into high-growth applications such as 3D printing resins and specialty adhesives. Its Trinohex® Ultra additive is gaining traction in EV battery electrolytes for improving safety and longevity. Ascend’s full value chain integration from ammonia and propylene to nitrile derivatives enhances cost control and supply stability. Its focus on performance chemicals supports expansion into advanced industrial and energy applications.

United States Specialty Nitriles Market Reinforced by Domestic Capacity and Bio-Based Innovation

The United States specialty nitriles industry is undergoing a decisive shift toward domestic capacity expansion and regulatory-aligned reformulation. In late 2024, INEOS announced plans to construct a world-scale nitrile butadiene rubber facility in the U.S., aimed at strengthening local supply for high-performance automotive sealing systems and military-grade protective equipment. This investment reflects a broader national strategy to reduce reliance on imported elastomers and specialty nitrile intermediates, particularly in defense, transportation, and critical infrastructure applications. Parallel consolidation is visible downstream, with Ascend Performance Materials acquiring a majority stake in a nitrile latex producer in early 2025, integrating polymer science capabilities with glove and industrial safety applications.

Advanced grades are increasingly central to U.S. competitiveness. Zeon Chemicals expanded its Texas operations in late 2025 to boost output of Zetpol HNBR, targeting hybrid vehicle timing belts and high-temperature seals. Sustainability and regulation are reinforcing innovation pathways, as bio-acrylonitrile programs tied to sustainable aviation fuel and bio-economy mandates aim to reduce carbon intensity by 20% by 2027. At the same time, updated TSCA requirements in 2025 are accelerating the transition toward low-extractable nitrile formulations for food-contact and sensitive industrial uses, reshaping formulation priorities across the U.S. specialty nitriles value chain.

India Specialty Nitriles Market Shaped by Policy Support and Technical Textiles Demand

India’s specialty nitriles industry is being structurally enabled by industrial policy, infrastructure development, and defense-linked demand. Under the Make in India and Aatmanirbhar Bharat frameworks, four Petroleum, Chemicals and Petrochemical Investment Regions have been designated as focal points for specialty chemical manufacturing. In 2025, NITI Aayog proposed an empowered committee to manage a dedicated chemical infrastructure fund, improving shared utilities and logistics for nitrile intermediates and downstream specialty fibers. Complementing this, the Production-Linked Incentive scheme has been extended through 2026, directly incentivizing incremental production of specialty nitriles to curb import dependence on East Asia.

Demand-side momentum is being driven by technical textiles. The extension of the National Technical Textiles Mission through March 2026, with a ₹1,480 crore outlay, is supporting R&D in nitrile-coated protective fabrics for defense, healthcare, and industrial safety. By late 2025, 168 government-approved R&D projects were actively developing specialty fiber and nitrile-based composite systems for high-stress applications. Sustainability is also emerging as a differentiator, with domestic producers such as Apcotex Industries transitioning roughly 30% of power consumption to renewable sources, aligning India’s specialty nitriles sector with global green manufacturing expectations.

South Korea Specialty Nitriles Market Anchored in Semiconductors and EV Materials

South Korea’s specialty nitriles industry is tightly integrated with its semiconductor and electric vehicle ecosystems. A major structural enabler emerged in August 2025 when Air Liquide acquired DIG Airgas for $2.9 billion, strengthening domestic supply chains for specialty gases essential to electronic-grade nitrile synthesis. This integration supports the production of ultra-high-purity nitriles used as precursors in thin-film deposition processes for next-generation high bandwidth memory chips, a segment where purity tolerances are measured in parts per billion.

Automotive electrification is reinforcing nitrile demand beyond electronics. LG Chem commissioned new production lines in 2025 for carboxylated nitriles optimized for EV battery pack gaskets and thermal management systems. These materials are designed to withstand continuous thermal cycling, dielectric exposure, and chemical stress, positioning South Korea as a critical supplier of application-specific nitriles for advanced mobility platforms.

Germany Specialty Nitriles Market Defined by Green Deal Alignment and Pharmaceutical Purity

Germany continues to occupy a premium position in specialty nitriles through process innovation and pharmaceutical-grade production. In 2025, AlzChem Group successfully piloted a low-emission production route for specialty nitrile rubber, significantly reducing wastewater contaminants while aligning operations with EU Green Deal 2030 targets. This technology-driven approach reflects Germany’s emphasis on compliance-led innovation rather than volume expansion.

Pharmaceutical intermediates remain a core strength. German producers expanded capacity in 2025 for high-purity cyanide-based nitriles used in cardiovascular and oncology drug synthesis, reinforcing the country’s role as a reliable supplier to regulated pharma markets. At an ecosystem level, chemical parks across Germany are integrating carbon capture and utilization infrastructure to synthesize nitriles from captured industrial CO2, embedding circular economy principles directly into specialty nitrile production.

Malaysia Specialty Nitriles Market Positioned as a Sustainable Export Hub

Malaysia has consolidated its position as a global export hub for sustainable nitrile latex, particularly for the medical glove industry. In late 2024, Synthomer established an ISCC PLUS certified value chain at its Pasir Gudang facility, enabling the production of bio-based nitrile latex using responsibly sourced feedstock. The site applies a mass balance methodology, linking at least 20% bio-feedstock to final NBR grades, meeting stringent sustainability criteria set by multinational medical brands.

This certification has strategic trade implications. Malaysia’s 2025 trade policy continues to favor exports of sustainable-certified nitrile products to Europe and North America, where procurement standards increasingly mandate traceable and lower-carbon materials. As a result, Malaysian producers are transitioning from volume-driven glove supply toward higher-margin, certified specialty nitrile offerings.

China Specialty Nitriles Market Reoriented by Trade Barriers and Feedstock Leadership

China remains structurally dominant in upstream nitrile chemistry, particularly ammoxidation processes. In 2025, multiple state-owned enterprises completed retrofitting projects to improve the efficiency and environmental performance of adiponitrile production, reinforcing China’s leadership in key nylon and specialty nitrile feedstocks. However, external trade dynamics are reshaping export strategies. Tariff modifications implemented by the U.S. Trade Representative from September 2024 onward, with further escalations planned through 2026, have constrained Chinese access to U.S. markets for nitrile-based chemicals and protective equipment.

In response, Chinese specialty nitrile producers are pivoting toward Belt and Road markets across Southeast Asia, Africa, and the Middle East, while upgrading product quality to meet diverse regulatory regimes. This shift is accelerating differentiation within China’s nitrile sector, separating commodity-grade output from export-oriented specialty nitriles with enhanced purity and application specificity.

Comparative Snapshot: Specialty Nitriles Industry by Country

Specialty Nitriles Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Drivers

|

Competitive Position

|

|

United States

|

Domestic capacity and bio-based nitriles

|

TSCA compliance, HNBR demand

|

High-performance, regulated markets

|

|

India

|

Policy-backed localization

|

PLI, NTTM, PCPIR infrastructure

|

Emerging specialty manufacturing hub

|

|

South Korea

|

Electronics and EV integration

|

UHP purity, battery sealing

|

Technology-intensive supplier

|

|

Germany

|

Green chemistry and pharma

|

EU Green Deal, CCU

|

Premium, compliance-led producer

|

|

Malaysia

|

Sustainable nitrile latex exports

|

ISCC PLUS, mass balance

|

Certified global export base

|

|

China

|

Feedstock leadership, market pivot

|

Ammoxidation scale, tariffs

|

Scale-driven with specialty upgrades

|

Specialty Nitriles Market Report Scope

Specialty Nitriles Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$4.8 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Product Type (Nitrile Butadiene Rubber, Hydrogenated Nitrile Butadiene Rubber, Carboxylated Nitrile Butadiene Rubber, Electronic-Grade Nitriles, Aromatic Nitriles, Acetonitrile and Adiponitrile), By Manufacturing Process (Ammoxidation, Hydrocyanation, Biological Synthesis), By Form (Liquid Latex, Powder, Solid), By End-Use Application (Protective Gear, Automotive, Electronics, Pharmaceuticals, Agrochemicals, Oilfield, Aerospace)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, INEOS Group, Zeon Chemicals L.P., Synthomer plc, ARLANXEO, LG Chem, Ascend Performance Materials, AlzChem Group AG, Kumho Petrochemical, Sinopec, Mitsubishi Chemical Group, Evonik Industries AG, Emerald Performance Materials, Apcotex Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Nitriles Market Segmentation

By Product Type

- Nitrile Butadiene Rubber

- Hydrogenated Nitrile Butadiene Rubber

- Carboxylated Nitrile Butadiene Rubber

- Electronic-Grade Nitriles

- Aromatic Nitriles

- Acetonitrile and Adiponitrile

By Manufacturing Process

- Ammoxidation

- Hydrocyanation

- Biological Synthesis

By Form

- Liquid Latex

- Powder

- Solid

By End-Use Application

- Protective Gear

- Automotive

- Electronics

- Pharmaceuticals

- Agrochemicals

- Oilfield

- Aerospace

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Nitriles Industry

- BASF SE

- INEOS Group

- Zeon Chemicals L.P.

- Synthomer plc

- ARLANXEO

- LG Chem

- Ascend Performance Materials

- AlzChem Group AG

- Kumho Petrochemical

- Sinopec

- Mitsubishi Chemical Group

- Evonik Industries AG

- Emerald Performance Materials

- Apcotex Industries Limited

*- List not Exhaustive