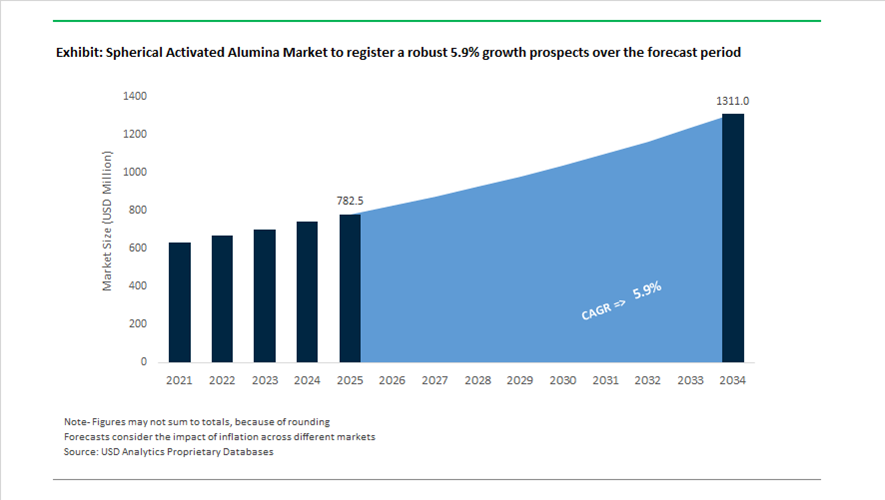

Spherical Activated Alumina Market Valuation 2025–2034: $782.5 Million to $1,310.8 Million at 5.9% CAGR Powered by Battery Thermal Management and Catalyst Lifecycle Integration

The global spherical activated alumina market is valued at $782.5 million in 2025 and is projected to reach $1,310.8 million by 2034, expanding at a CAGR of 5.9%. Demand is accelerating across catalyst supports, desiccants, adsorbents, battery separator coatings, thermal interface materials, and sustainable fuel processing catalysts. High-purity spherical alumina beads are increasingly used in lithium-ion battery separators, solid-state battery architectures, ethanol-to-jet catalysts, and advanced semiconductor packaging due to their controlled porosity, thermal conductivity, mechanical strength, and moisture adsorption efficiency. Market growth is reinforced by decarbonization initiatives in aviation fuels, electrification of mobility, and tighter performance standards in gas dehydration and petrochemical catalyst systems.

Technology diversification intensified in 2024. In March 2024, SiAT and CSAC introduced carbon nanotube-coated aluminum foil integrating specialty alumina treatments to enhance charging speeds and lifecycle stability in lithium-ion and sodium-ion batteries. In July 2024, Resonac Corporation launched the US-JOINT R&D consortium in Union City, California, focusing on semiconductor back-end innovation where spherical alumina functions as a high-performance thermal filler in advanced packaging. In November 2024, PQ completed the expansion of its Pasuruan, Indonesia facility, strengthening its position as a regional hub for spherical activated alumina beads used in liquid and gas dehydration applications in Southeast Asia’s energy sector. Throughout 2024, Tata Chemicals scaled production of rice husk-derived TREADSIL™ silica and alumina grades, introducing bio-based spherical materials for sustainable tire and industrial adsorbent markets. In late 2024, PPG finalized the divestiture of its precipitated silica and related specialty materials business to Qemetica, reflecting broader raw-material portfolio rationalization across coatings and advanced materials suppliers.

Strategic restructuring and clean energy alignment accelerated in 2025 and 2026. In October 2025, Honeywell completed the spin-off of its Advanced Materials division into Solstice Advanced Materials, creating a focused platform for specialty alumina and adsorbent R&D targeting carbon capture and clean energy systems. In November 2025, Sumitomo Chemical restructured its lithium-ion battery separator business to prioritize high-purity spherical alumina coatings engineered for improved thermal stability in high-nickel battery chemistries. In January 2026, Syensqo and Axens launched Argylium, a joint venture dedicated to scaling advanced materials for solid-state batteries in Europe, incorporating spherical alumina into separator and thermal management systems. During the same month, Praj Industries and Axens demonstrated the Jetanol™ Ethanol-to-Jet pathway utilizing specialized spherical alumina catalysts for sustainable aviation fuel production. In February 2026, Axens completed the full acquisition of Eurecat, strengthening catalyst lifecycle management, ex situ activation services, and metals reuse capabilities for alumina-based catalyst systems. These battery-driven innovations, catalyst service integrations, bio-derived feedstock expansions, and energy transition applications are redefining competitive intensity in the spherical activated alumina market through 2034.

Structural Trends and Strategic Opportunities in the Spherical Activated Alumina Market

Standardization of Spherical Activated Alumina for EV Battery Humidity Management

The Spherical Activated Alumina Market is experiencing a specification-driven inflection point as electric vehicle manufacturers harden requirements around moisture control inside high-energy-density battery packs. With Lithium-ion and emerging solid-state architectures operating under tighter electrochemical tolerances, internal humidity is now treated as a safety-critical variable rather than a secondary design consideration. Automotive OEMs are increasingly standardizing spherical activated alumina within integrated desiccant breather systems to consistently maintain moisture levels below 100 ppm, directly mitigating hydrofluoric acid formation that accelerates electrolyte breakdown and cathode degradation.

A decisive shift away from silica gel has occurred across European and North American EV platforms. In 2025, OEM validation programs increasingly favored spherical activated alumina due to its superior crush strength, commonly exceeding 15 kg per bead, and its ability to withstand repeated thermal shock and vibration cycles encountered across an automotive chassis. This mechanical robustness is particularly relevant for battery enclosures certified to IP67 and IP69K standards, where desiccant failure can compromise long-term sealing performance. Industrial test data confirms that alumina’s attrition loss, often below 0.1%, significantly reduces the risk of desiccant dusting, a failure mode that can interfere with battery management system sensors and high-voltage electrical contacts. As EV warranties extend beyond eight years, durability and stability metrics are becoming as important as adsorption capacity, firmly embedding spherical activated alumina into next-generation battery pack design specifications.

Mandatory Dehydration in Renewable Natural Gas and Green Hydrogen Upgrading

Decarbonization mandates are driving large-scale deployment of dehydration systems across renewable gas value chains, creating structurally anchored demand for spherical activated alumina. Renewable Natural Gas and Green Hydrogen both require aggressive moisture removal to meet pipeline, storage, and end-use purity standards. Activated alumina has emerged as the preferred desiccant due to its high water uptake capacity, thermal regenerability, and mechanical resilience under pressure cycling.

In India, the SATAT initiative and 2025 guidelines issued by the Ministry of Petroleum and Natural Gas have accelerated the mandatory blending of Compressed Bio-Gas into the national gas grid. By late 2025, more than 130 CBG plants had been commissioned, each requiring dehydration skids capable of achieving water dew points of minus 40 degrees Celsius or lower. These operating conditions favor spherical activated alumina over polymeric or gel-based alternatives, particularly in regions with wide ambient temperature fluctuations.

Hydrogen upgrading is reinforcing this trend globally. For Fuel Cell Electric Vehicles, hydrogen must comply with ISO 14687 purity standards, where even trace moisture can irreversibly poison platinum-based catalysts. Industrial gas leaders such as Air Liquide and Linde have highlighted the deployment of alumina-based Pressure Swing Adsorption units to ensure ultra-dry hydrogen streams. As hydrogen infrastructure scales, dehydration is no longer an optional process step but a regulated requirement, anchoring long-term demand for high-performance spherical alumina adsorbents.

High-Purity Alumina for Pharmaceutical Chromatography and Biologics Processing

The rapid expansion of mRNA therapeutics, viral vector vaccines, and advanced biologics manufacturing is opening a premium opportunity for High-Purity Activated Alumina. In downstream purification, spherical alumina is gaining traction as a robust and cost-efficient alternative to polymeric chromatography resins for pre-filtration and buffer stabilization steps. Its chemical inertness, thermal stability, and consistent bead geometry enable reliable operation under high flow rates and repeated sterilization cycles.

Strategic investments underline the significance of this opportunity. In June 2025, Hindalco Industries completed the acquisition of AluChem Companies, Inc., explicitly strengthening its specialty alumina portfolio for semiconductor and pharmaceutical applications. Low-soda, high-purity alumina grades are increasingly specified in biologics manufacturing, where ionic contamination can compromise yield and regulatory compliance.

Recent 2025 studies on pharmaceutical-grade chromatography indicate that spherical alumina with controlled pore architectures and surface areas in the 200 to 350 square meter per gram range can stabilize pH during protein separation. This reduces reliance on complex buffer systems, lowers consumable costs, and improves process robustness, positioning high-purity spherical alumina as a value-enhancing material rather than a commodity adsorbent.

Selective Adsorbents for PFAS Removal and Water Remediation

Water treatment regulations are creating one of the most compelling long-term opportunities for spherical activated alumina. The U.S. Environmental Protection Agency’s National Primary Drinking Water Regulation has established enforceable maximum contaminant levels for six PFAS compounds, with compliance entering a critical phase in 2025. This regulatory shift is forcing utilities and industrial operators to adopt treatment technologies capable of removing contaminants at parts-per-trillion concentrations.

While granular activated carbon remains widely deployed, surface-modified spherical activated alumina is increasingly being evaluated for its selectivity toward short-chain PFAS species that often evade traditional carbon filters. Federal funding of one billion dollars under the Infrastructure Investment and Jobs Act is accelerating pilot programs and full-scale deployments, particularly in regions with complex water chemistries.

Mid-2025 pilot projects in the U.S. Midwest demonstrated that modified activated alumina maintained higher adsorption capacity for compounds such as PFHxS and GenX in the presence of competing natural organic matter. These systems extended filter bed life by up to 30% compared to standard GAC installations, materially improving lifecycle economics. As PFAS compliance moves from monitoring to enforcement, selective alumina-based adsorbents are positioned to capture a durable, regulation-driven growth corridor within the Spherical Activated Alumina Market.

Spherical Activated Alumina Market Share and Segmentation Insights

Spherical Alumina Beads Dominate the Market for Adsorption and Catalyst Support Applications

Spherical alumina beads accounted for 48.60% of the spherical activated alumina market in 2025, reflecting their widespread use in industrial adsorption and catalytic processing systems. Their spherical geometry provides high surface area, strong mechanical strength, and excellent flow characteristics, which minimize pressure drop and abrasion in packed-bed reactor systems. These properties make spherical alumina beads ideal for applications such as gas dehydration, water purification, catalyst support structures, and adsorption processes. A major 2025 demand driver is the increasing use of natural gas processing and LNG production, where activated alumina desiccants are widely used for gas dehydration to remove moisture and protect downstream processing equipment.

Catalyst and Catalyst Support Applications Drive Demand for Spherical Activated Alumina

Catalyst and catalyst support applications represent the largest segment in the spherical activated alumina market, accounting for 38.60% of global demand in 2025 due to the extensive use of alumina materials in catalytic processes. Activated alumina serves as a high-surface-area support for metal catalysts used in petrochemical refining, chemical synthesis, and environmental emission control systems. Its stability under high temperatures and reactive chemical environments makes it suitable for demanding industrial operations. A key 2025 industry trend is the continued expansion of petrochemical processing and environmental catalytic technologies, where advanced catalyst formulations require optimized alumina supports to improve catalytic efficiency, extend catalyst lifespan, and enhance reaction selectivity in refining and chemical manufacturing operations.

Spherical Activated Alumina Market Competitive Landscape

The spherical activated alumina market in 2026 is transitioning toward precision-engineered adsorbents with tailored pore structures, high crush strength, and circular production models. Demand is accelerating across semiconductor processing, CCUS, hydrogen purification, and sustainable fuels, driving innovation in high-surface-area alumina and advanced gas drying technologies.

Axens Expands Circular Adsorbent Ecosystem with CCUS Integration and High-Surface-Area Alumina Solutions

Axens is reinforcing its leadership in spherical activated alumina through strategic acquisitions and decarbonization-focused innovation. The 100% acquisition of Eurecat in 2026 strengthens catalyst recycling and metals recovery, enhancing lifecycle management of alumina adsorbents. Its DMX™ CCUS technology, developed with Samsung C&T, utilizes advanced alumina-based adsorbents for high-efficiency CO2 capture and purification. The AxSorb A and D series are engineered for high-performance air and gas drying, increasingly deployed in SAF pathways such as Jetanol™. Axens leverages its Salindres facility to produce high-surface-area alumina spheres (350 m²/g) optimized for arsine and mercury removal. The company’s "Decarbonization-as-a-Service" model positions it strongly in energy transition applications.

Honeywell UOP Integrates Advanced Alumina Adsorbents with Process Technologies for High-Purity Gas Systems

Honeywell UOP is advancing spherical activated alumina through integrated purification platforms combining MOLSIV™ and Versal™ technologies. Its Versal™ alumina portfolio includes customizable phases such as pseudoboehmite and gamma alumina, engineered for optimized porosity and mechanical strength. The expansion of AZ and CLR product lines in 2025 enhances trace contaminant removal in cryogenic air separation units. These high-capacity alumina spheres improve process efficiency by reducing regeneration frequency under thermal swing adsorption systems. Honeywell’s solutions support production of ultra-high purity oxygen, nitrogen, and hydrogen for industrial and semiconductor applications. Integration with digital monitoring tools ensures corrosion prevention and operational reliability in gas processing environments.

Evonik Strengthens Specialty Alumina Portfolio with Chloride Adsorbents and EV-Focused Manufacturing Expansion

Evonik is scaling its specialty adsorbent capabilities following the integration of Porocel into its catalyst division. The launch of Chlorocel™ 909 in 2026 enhances chloride removal efficiency, protecting downstream systems from corrosion in refining and petrochemical operations. Its Alu5 plant in Yokkaichi, Japan produces advanced alumina solutions for EV battery thermal management and high-purity applications. The company reported €1.87 billion adjusted EBITDA in 2025, with stable pricing in its Inorganics segment supported by resilient demand. Evonik is optimizing production under its "Tailor Made" program to achieve higher ROCE through specialty adsorbents. Its focus on green transformation and high-margin alumina solutions strengthens its competitive position.

Sumitomo Chemical Advances High-Purity Alumina for Semiconductor and Lithium Processing Applications

Sumitomo Chemical is leveraging its innovation-driven strategy to expand its specialty activated alumina portfolio for high-purity applications. Recognized as a Clarivate Top 100 Global Innovator in 2026, the company excels in integrating catalyst design with advanced material science. Its spherical alumina products feature controlled pore distribution and mechanical strength, supporting lithium purification and desulfurization processes. The company is aligning its Essential & Green Materials segment toward semiconductor and ICT applications where ultra-high purity is critical. Strong patent activity reinforces its leadership in advanced alumina structures. Sumitomo’s solutions are increasingly adopted in natural gas treatment and battery material value chains.

BASF Expands Environmental Adsorbents Portfolio for Water Treatment and Gas Processing Applications

BASF is leveraging its Verbund integration to supply high-performance spherical activated alumina for environmental and industrial applications. The company is scaling fluoride and arsenic removal media to meet tightening water purification regulations in Asia-Pacific markets. Its high-thermal-stability alumina spheres are designed for Claus process applications, supporting efficient sulfur recovery in refining operations. BASF generated €1.3 billion in free cash flow in 2025, enabling reinvestment into bio-based adsorbent development. Its integrated production model ensures cost efficiency and consistent supply across petrochemical and air treatment sectors. BASF continues to expand its role in sustainable water and gas purification technologies.

Huber Engineered Materials Focuses on Abrasion-Resistant Alumina for Industrial Drying and Flame Retardant Applications

Huber Engineered Materials is targeting niche high-performance applications for spherical activated alumina, particularly in industrial drying and flame retardancy. The company expanded its ATH and specialty alumina production to meet demand for halogen-free flame retardants in automotive and construction sectors. Its spherical alumina grades offer superior abrasion resistance, minimizing dust generation in vacuum systems and air dryers. Huber is implementing sustainable bauxite sourcing strategies to deliver carbon-transparent alumina products for European OEMs. The company’s focus on durability and environmental compliance aligns with evolving industrial standards. Its specialized product portfolio supports high-reliability applications in sensitive mechanical systems.

Germany Spherical Activated Alumina Market Anchored in Catalyst Geometry and Hydrogen Desiccation

Germany has emerged as the global reference point for high-precision spherical activated alumina, driven by process innovation, hydrogen infrastructure, and digitalized manufacturing control. In late 2025, BASF completed its commercial-scale X3D® production facility in Ludwigshafen, enabling the industrial manufacture of 3D-printed spherical alumina catalysts and supports. These engineered geometries reduce reactor pressure drop by up to 30%, directly improving throughput and energy efficiency in refining and petrochemical applications. This marks a structural shift away from commodity alumina beads toward application-optimized catalyst architectures.

Hydrogen economy integration is reinforcing this trajectory. Under Germany’s National Hydrogen Strategy, spherical activated alumina has been selected as the preferred desiccant for low-carbon hydrogen purification, including methane pyrolysis pathways jointly developed by BASF and ExxonMobil, with pilot demonstrations scheduled for 2026. The Ludwigshafen methane pyrolysis test unit relies on alumina-based reactors capable of splitting natural gas into hydrogen and solid carbon with substantially lower energy intensity than water electrolysis. Alongside this, Evonik expanded its Catalyst Lifecycle Management program in mid-2025, focusing on regeneration and reuse of spherical alumina adsorbents for olefin purification. German manufacturers have also eliminated PFAS-based processing aids following ECHA’s 2025 updates, reinforcing compliance in food-contact and pharmaceutical drying applications.

United States Spherical Activated Alumina Market Driven by Energy, Semiconductors, and CCS

The United States market is defined by demand from energy processing, advanced polymers, and semiconductor fabrication. In early 2025, Evonik completed strategic consolidation of its North American assets, concentrating high-performance spherical alumina production at integrated hubs serving green tire compounds and biofuel dehydration systems. This rationalization reflects rising demand for consistency in bead strength, attrition resistance, and moisture adsorption efficiency.

Process-specific innovation remains a key differentiator. Honeywell UOP introduced the P-310 spherical promoted alumina adsorbent in 2025 for its Oleflex™ technology, delivering higher regenerative stability in sulfur and moisture removal. Federal incentives linked to the CHIPS Act in late 2025 further accelerated domestic scaling of ultra-high-purity spherical alumina for CMP slurries supporting 2nm semiconductor fabrication. Beyond electronics, the U.S. Department of Energy reported a 15% increase in spherical alumina demand for shale gas desulfurization and Claus tail-gas treatment in the Permian Basin. Carbon capture infrastructure is also emerging as a demand vector, with Axens deploying AxSorb® spherical adsorbents across new Gulf Coast CCS projects in 2025.

China Spherical Activated Alumina Market Shaped by Circularity and Energy Policy

China’s spherical activated alumina industry is undergoing structural realignment under energy efficiency mandates and circular economy objectives. The Ministry of Industry and Information Technology’s 2025–2027 Aluminium Action Plan enforces stricter energy thresholds for high-purity alumina refineries while mandating higher utilization of red mud byproducts. These policies are accelerating investment in high-efficiency spherical alumina routes over conventional irregular powders.

Circular chemistry has emerged as a defining theme. In early 2025, BASF commissioned its first commercial loopamid facility in Caojing, Shanghai, using alumina-based catalysts to chemically recycle nylon 6 for textile-grade feedstocks. In parallel, BASF’s Nanjing site brought a new CFRP-enabled dispersant line online in late 2025 to stabilize nano-spherical alumina for advanced coatings and electronics. Export controls on rare earths in 2025 further strengthened alumina’s role as a cost-effective catalyst alternative in automotive emission control systems. At the same time, alumina production capacity is relocating toward clean-energy provinces such as Inner Mongolia, with new facilities capped below 13,000 kWh per ton to comply with national decarbonization targets.

India Spherical Activated Alumina Market Accelerated by Electronics and Water Treatment

India’s spherical activated alumina demand profile is increasingly shaped by electronics manufacturing and public infrastructure programs. The $6.65 billion Production Linked Incentive scheme for electronics has materially increased domestic consumption of spherical alumina as a thermal filler in semiconductor packaging, LEDs, and thermal interface materials. By September 2025, more than 32 major electronics manufacturers had been approved under the scheme, anchoring long-term demand for controlled-sphericity alumina grades.

Public water treatment initiatives provide a parallel growth channel. Under the Jal Jeevan Mission, spherical activated alumina was widely deployed in 2025 for rural defluoridation projects, particularly in Rajasthan and Andhra Pradesh. Domestic producers such as NALCO and Hindalco invested a combined ₹850 crore between 2024 and 2025 to improve particle size distribution and bead sphericity to ISO-aligned standards. The rapid expansion of EV manufacturing has further increased demand for spherical alumina-filled thermally conductive plastics, now representing a significant share of specialty material consumption in India’s automotive clusters.

South Korea Spherical Activated Alumina Market Focused on Batteries and Semiconductors

South Korea’s market is closely integrated with its battery and semiconductor ecosystems. In October 2024, Momentive Technologies completed the acquisition of multiple spherical alumina and silica operations in South Korea, strengthening its position in high-purity thermal fillers for EV battery modules. This consolidation supports localized supply of materials critical for thermal runaway mitigation.

Semiconductor applications represent the second major pillar. Korean mineral processors, including Imerys operations in Korea, pivoted toward fused and spherical alumina optimized for CMP and abrasive processes supporting the 2025–2026 chip production cycle. In parallel, manufacturers of copper-clad laminates transitioned to spherical alumina fillers by late 2025 to enhance heat dissipation in high-power 5G infrastructure, reinforcing alumina’s role in next-generation electronics reliability.

Comparative Snapshot: Spherical Activated Alumina Industry by Country

Spherical Activated Alumina Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Application Focus

|

Structural Direction

|

|

Germany

|

Hydrogen economy and catalyst design

|

3D-printed catalysts, hydrogen drying

|

Geometry optimization and digital synthesis

|

|

United States

|

Energy processing and semiconductors

|

Oleflex adsorbents, CMP-grade alumina

|

Asset consolidation and purity scaling

|

|

China

|

Circular economy and energy policy

|

Chemical recycling catalysts, nano-alumina

|

Energy-efficient relocation and circular use

|

|

India

|

Electronics PLI and water treatment

|

TIM fillers, defluoridation media

|

Domestic standardization and capacity build-out

|

|

South Korea

|

EV batteries and chip fabrication

|

Thermal fillers, CMP abrasives

|

Consolidation around high-purity grades

|

Spherical Activated Alumina Market Report Scope

Spherical Activated Alumina Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$782.5 Million

|

|

Market Size (2034)

|

$1310.8 Million

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Product Type (Spherical Alumina Beads, Micronized Spherical Alumina, High-Purity Spherical Alumina, Promoted Spherical Alumina), By Application (Adsorption and Desiccants, Catalyst and Catalyst Supports, Thermal Management, Electronics and Semiconductors, Environmental Protection)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Honeywell International Inc., Axens SA, Evonik Industries AG, Sumitomo Chemical Co., Ltd., W. R. Grace and Company, Momentive Technologies, Shin-Etsu Chemical Co., Ltd., Almatis GmbH, Sasol Limited, Resonac Holdings Corporation, Aluminum Corporation of China, National Aluminium Company Limited, Imerys S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Spherical Activated Alumina Market Segmentation

By Product Type

- Spherical Alumina Beads

- Micronized Spherical Alumina

- High-Purity Spherical Alumina

- Promoted Spherical Alumina

By Application

- Adsorption and Desiccants

- Catalyst and Catalyst Supports

- Thermal Management

- Electronics and Semiconductors

- Environmental Protection

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Spherical Activated Alumina Industry

- BASF SE

- Honeywell International Inc.

- Axens SA

- Evonik Industries AG

- Sumitomo Chemical Co., Ltd.

- W. R. Grace and Company

- Momentive Technologies

- Shin-Etsu Chemical Co., Ltd.

- Almatis GmbH

- Sasol Limited

- Resonac Holdings Corporation

- Aluminum Corporation of China

- National Aluminium Company Limited

- Imerys S.A.

*- List not Exhaustive