Automotive NVH Materials Market Overview- EV Cabin Acoustics, Lightweight Damping Technologies & Sustainable Absorbers Shaping Next-Gen Vehicle Design

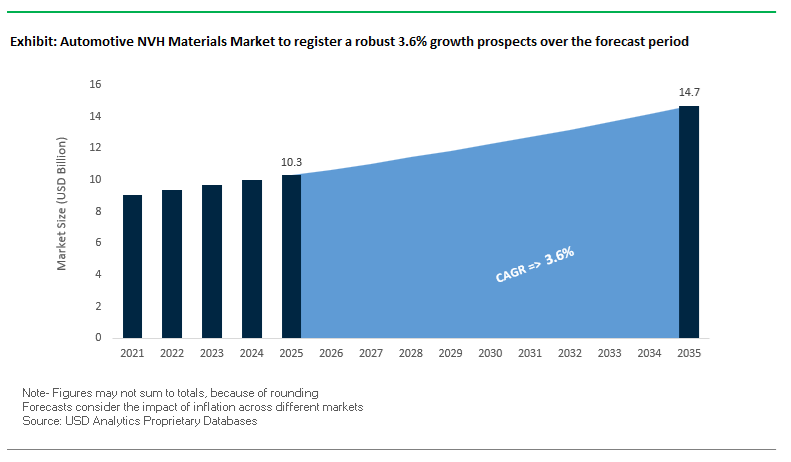

The Automotive NVH (Noise, Vibration & Harshness) Materials Market, valued at USD 10.3 billion in 2025 and projected to reach USD 14.7 billion by 2035 at a steady 3.6% CAGR, is undergoing a structural transformation driven by the rapid shift toward electric vehicles (EVs), increasingly stringent noise regulations, and the global push for lightweight and sustainable material systems. As the traditional internal combustion engine fades from the acoustic profile of modern vehicles, NVH engineering is dominated by road, tire, wind, and high-frequency cabin noise in the 500 Hz–4,000 Hz range, requiring advanced materials tailored specifically for EV-class acoustic challenges.

To meet these evolving requirements, OEMs and Tier-1 suppliers are accelerating adoption of lightweight acoustic composites, micro-perforated films, high-damping viscoelastic sheets, and recycled-content sound absorbers engineered to deliver equal or superior NVH performance at significantly lower mass—supporting both regulatory compliance and EV range optimization. With global sustainability mandates tightening, NVH material selection increasingly incorporates bio-based foams, recycled PET fibers, circular textile blends, and low-VOC binders, especially in non-visible, high-volume components such as carpet underlays, wheel-arch liners, trunk liners, dash insulators, and roof absorbers.

The convergence of lightweighting, electrification, and environmental regulation is repositioning NVH materials as a core enabler of premium cabin comfort, vehicle efficiency, and sustainability reporting (Scope 3 emissions). For OEMs competing on quietness, ride quality, and eco-friendly interiors, next-generation NVH systems are a strategic requirement for achieving acoustic differentiation and regulatory alignment through 2035.

Market Analysis: Recent Product Launches, Sustainability Recognitions & EV-Focused NVH Solutions

The Automotive NVH sector recorded a concentrated set of developments that underline its pivot to EV-specific acoustic solutions and sustainability. In November 2025, Vibracoustic announced a dedicated battery pack isolation system for body-on-chassis EVs (large SUVs and LCVs) incorporating multiple mounts and elastomer dampers to mitigate torsional bending forces - a move that combines structural protection with targeted NVH attenuation for the powertrain and chassis interface. Also in November 2025, Sika achieved an EcoVadis Silver Medal, a supplier sustainability recognition that strengthens its standing with OEMs prioritizing ESG performance when selecting damping sheets, sealants and liquid applied sound deadeners.

Earlier in June 2025, Hutchinson showcased integrated NVH and thermal management solutions at Battery Show Europe, emphasizing acoustic encapsulation and lightweight, recyclable materials for e-motors and battery packs. That same month, FORVIA/MATERI’ACT launched NAFILean Vision, a bio-composite family aimed at visible engine and under-hood trims that can also serve acoustic shielding functions - signaling material convergence between sustainability and NVH performance. In April 2025, Vibracoustic engineered air springs, jounce bumpers and hydro bushings for a premium electric pickup truck, reinforcing the need for integrated NVH subsystems in high-load EV platforms. Notable product and regulatory work across 2024–2025 - including PFAS-free surface treatments (Hutchinson, April 2025) and high-volume recyclable encapsulation validated for 600,000 vehicles per year (Hutchinson, July 2024) - collectively demonstrate suppliers’ dual focus on acoustic performance and eco-compliance, aligning NVH material roadmaps with OEM electrification and sustainability strategies.

Key Trends Redefining the Automotive NVH Materials Market

Trend 1: Re-Engineering NVH Material Profiles to Target EV-Specific Acoustic Signatures and High-Frequency Noise Sources

Electric Vehicle architectures fundamentally alter the acoustic environment inside the cabin. The absence of combustion masking noise makes electric motor whine, inverter harmonics, tire impact noise, and aerodynamic disturbances disproportionately prominent, forcing material suppliers to redesign NVH products around precision-mapped frequency responses. EV traction motors generate a characteristic high-frequency whine between 800 Hz and 3000 Hz, well outside the low-frequency range where traditional mass dampers are effective. This shift requires multilayer absorbers with tailored pore structures, engineered flow resistivity, and composite laminates that target specific high-frequency tonalities.

OEMs are establishing aggressive refinement targets, with leading manufacturers aiming for 3–5 dBA cabin noise reduction at highway speeds compared to best-in-class ICE vehicles. Achieving this requires applying advanced constrained-layer damping (CLD) materials on floorpans and body-in-white structures to address structural-borne vibration paths. Above 80 km/h, tire and road noise account for 70–80% of total in-cabin noise in EVs, intensifying the focus on fender liners, wheelhouse absorbers, and underbody shields manufactured using engineered textiles and lightweight acoustic foams. This precise acoustic rebalancing represents a major shift from generic NVH solutions toward scientifically tuned, application-specific NVH material architectures.

Trend 2: Regulatory and OEM Sustainability Mandates Drive Adoption of Recycled, Bio-Based, and Low-Carbon NVH Materials

Alongside acoustic re-engineering, NVH suppliers face strong downward pressure on carbon footprint metrics as OEMs commit to circularity and regulators impose lifecycle emission limits. One of the most visible transitions is the replacement of heavy, VOC-emitting bitumen sound deadeners with recyclable thermoplastic elastomers (TPEs), polyurethane foams, and advanced lightweight composites. These materials not only reduce embodied carbon but also eliminate the volatile emissions associated with petroleum-derived damping materials.

Recycled fiber content is becoming a foundational requirement. Leading European suppliers now produce acoustic nonwoven pads containing up to 70% recycled PET fibers derived from textile waste, demonstrating that circularity can coexist with OEM-level acoustic performance. Parallel R&D programs—often supported by government bodies—are validating bio-based polyurethane foams made from natural oils, achieving noise reduction coefficients comparable to conventional foams while cutting carbon footprints by more than 50%.

As sustainability expectations escalate across EV and premium vehicle lines, suppliers capable of delivering traceable, recycled, and bio-based acoustic materials without compromising noise absorption performance will gain substantial competitive advantage.

High-Value Opportunities Emerging in the Automotive NVH Materials Market

Opportunity 1: Lightweight, High-Performance Meta-Materials and Multifunctional NVH Systems for EV Range Optimization

The critical importance of EV driving range places acute pressure on every kilogram of material used, opening major opportunities for high-performance NVH meta-materials that maximize absorption efficiency per unit mass. Engineered meta-materials leveraging Helmholtz resonators, acoustic black holes, and microstructured geometries are achieving absorption coefficients above 0.8 while weighing up to 10× less than traditional heavy acoustic barriers. Substituting conventional mass-loading NVH solutions with these ultra-efficient materials directly contributes to range extension and reduces overall material cost.

The underbody shield is becoming a pivotal multifunctional NVH integration zone. Today’s advanced underbody systems combine aerodynamic drag reduction, acoustic absorption, and thermal protection into a single lightweight component. Multifunctional implementations already demonstrate 3–4 dB noise reduction while improving the vehicle’s coefficient of drag (Cd) by up to 0.01, supporting both efficiency and refinement targets. Another area gaining traction is aerogel composite blankets, which offer thermal resistances 2–8× higher than glass wool while simultaneously delivering robust acoustic absorption capabilities. These ultra-light, high-performance composites are increasingly being qualified for thermally stressed EV regions such as battery enclosures and electric motor housings.

The convergence of lightweighting, acoustic performance, and multi-functionality positions engineered meta-materials as one of the most commercially attractive segments in the NVH materials market.

Opportunity 2: Active Noise Cancellation (ANC) Expansion Requires Complementary Passive NVH Material Optimization

As more EVs integrate cabin-wide Active Noise Cancellation (ANC) systems, a significant opportunity emerges for NVH suppliers to redesign passive materials that complement digital noise-reduction algorithms. ANC systems excel at cancelling low-frequency noises (<500 Hz) such as road booming and structural resonance, but require carefully tuned passive materials to manage mid-to-high frequency noise components.

Industry evaluations show that a hybrid strategy—ANC for low frequencies combined with frequency-targeted passive insulation—delivers up to 40% greater Net Sound Reduction (NSR) than either approach alone. This synergy requires passive materials to be acoustically stable and non-interfering with ANC microphones and speakers. Consequently, headliners, pillars, door trims, and roof structures are being re-engineered to incorporate acoustically neutral mounting points, optimized porosity close to sensor interfaces, and low-reflection surfaces to prevent standing waves that degrade ANC performance.

As ANC adoption grows across mid-range and premium EVs, NVH suppliers that provide integrated passive–active NVH architectures—rather than standalone materials—will be positioned at the forefront of OEM sourcing strategies.

Automotive NVH Materials Market Share Analysis

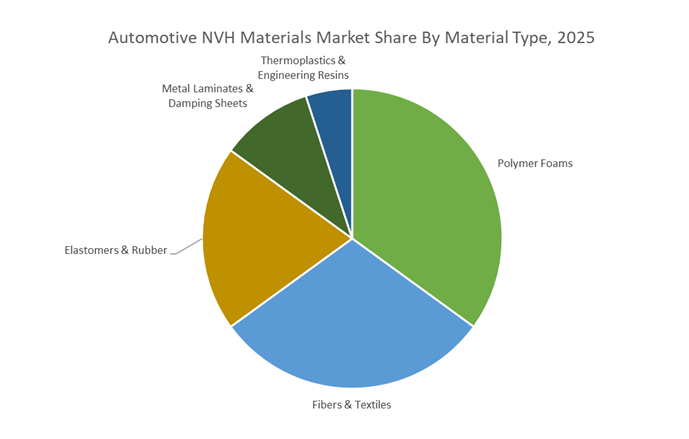

Market Share by Material Type: Polymer Foams Lead with 36.8% Share

Polymer Foams hold the largest share of the Automotive NVH Materials Market at 36.8% in 2025, underscoring their essential role in absorbing and dissipating airborne noise across cabin surfaces, floor structures, dashboards, and door panels. Their dominance is driven by a compelling combination of lightweighting, low cost, high acoustic absorption efficiency, and ease of molding into complex geometries, making them the material of choice for mass-produced NVH solutions in both ICE and EV platforms. With the electrification of vehicles eliminating engine masking noise, OEMs face heightened acoustic challenges—amplified tire, wind, and road noise—which further strengthens demand for polyurethane, polyester, and melamine foam systems. Supporting material categories shape a multi-functional NVH landscape: fibers and textiles, many containing high recycled content (rPET, recycled cotton), meet sustainability requirements while enhancing mid–high frequency sound absorption; elastomers and rubber components address structure-borne vibration at its source; metal laminates and damping sheets deliver rigid-panel damping and resonance control; and thermoplastics and engineering resins provide barrier insulation and structural integration.

Market Share by Product Function: Sound Absorption Materials Lead with 38.9% Share

Sound Absorption Materials dominate the product-function landscape with a 38.9% share in 2025, affirming their position as the highest-volume NVH category due to their widespread deployment across virtually every interior surface of modern vehicles. This segment leads because effective absorption is the first and most critical step in managing cabin acoustics, capturing airborne sound energy across a broad frequency range and ensuring a quiet, comfort-optimized driving environment. The shift toward electric vehicles amplifies the importance of absorption materials, as EV cabins expose more high-frequency tire and wind noise that must be mitigated using foams, fiber mats, acoustic pads, and porous composites. Complementing absorption functions, sound insulation (barrier) materials block external noise intrusion; vibration damping materials suppress resonance and panel vibrations that radiate secondary noise; and sealing materials prevent air leaks that can undermine the entire NVH system. The strong share of sound absorption reflects the industry’s move toward holistic acoustic engineering, where OEMs deploy layered solutions that combine absorption, insulation, damping, and sealing to meet stricter NVH targets across vehicle segments.

Country Analysis: Global Automotive NVH Materials Market Innovation Hubs

China: NEV-Driven Acoustic Lightweighting and High-Volume NVH Material Integration

China has become the fastest-scaling global hub for automotive NVH materials, propelled by record-setting New Energy Vehicle (NEV) production and intense competition among domestic EV brands. The transition to electric powertrains—where motor whine, inverter switching noise, and tire/road interaction dominate cabin acoustics—has amplified demand for ultra-lightweight acoustic foams, fiber-based insulators, and polyolefin NVH solutions. NEV leaders like BYD are prioritizing every gram of weight savings to improve EV range, accelerating adoption of lightweight acoustic pads, PU foams, and EV-specific damping laminates designed to offset battery mass while enhancing cabin quietness.

Chinese material suppliers are rapidly expanding production capacity for PU foams, polyolefin blends, and thermal-acoustic insulation materials optimized for battery pack isolation systems. These NVH materials are engineered not only for vibration damping but also for thermal stability and flame resistance, aligning with recent industry emphasis on battery safety. China’s new generation of fully automated NEV super factories—exemplified by BAIC’s intelligent EV facility in Beijing—enables immediate integration of next-generation NVH components into large-scale automotive production. Sustainability has also become a competitive differentiator, with Chinese OEMs increasingly sourcing recyclable, low-VOC, and bio-based insulation materials, accelerating China’s transition toward globally aligned, high-performance NVH material ecosystems.

Germany (Europe): Premium Cabin Acoustics and Active NVH Systems Anchored in High R&D Investment

Germany remains a premium automotive acoustics leader due to its engineering-intensive OEM ecosystem and strict compliance with EU noise regulations. In 2023, German OEMs invested €30.3 billion in R&D, a sizable share of which supported advancements in acoustic engineering, e-drive NVH mitigation, and structural noise optimization. As EV adoption redefines vehicle noise signatures, suppliers such as Vibracoustic are developing specialized EV motor mounts, battery mounts, and frequency-optimized bushings that address high-frequency inverter noise and low-frequency structural vibrations in both passenger and commercial EVs.

European NVH strategies increasingly require multi-layer acoustic barriers, hybrid composites, and lightweight underbody shields to counter wind, road, and tire noise—now more perceptible in quiet electric cabins. EU regulatory pressure on external vehicle noise also compels manufacturers to deploy high-performance damping films, acoustic dash insulators, and BIW (body-in-white) NVH reinforcement materials. Germany’s commitment to Industry 4.0 and advanced manufacturing further accelerates the refinement of NVH materials, integrating digital simulations, robotic lamination, and automated cutting processes for precision acoustic engineering. This positions Europe as a global frontrunner in premium NVH systems and advanced acoustic materials for electric mobility.

United States: Next-Generation Lightweight Foam Technology and Thermal-Acoustic EV Battery Protection

The United States is shaping the NVH materials market through its strong polymer chemistry ecosystem and the dominance of large vehicle categories such as SUVs and pickup trucks, now rapidly transitioning to electric powertrains. U.S.-based innovators like 3M have introduced cutting-edge products including 3M™ Thinsulate™ Acoustic Insulation 40A, engineered specifically for EV motor noise, road noise, and cabin whispering-level environments. This ultra-thin, lightweight acoustic mat addresses EV-specific challenges such as high-frequency motor harmonics and reduced masking noise.

A major U.S. trend is the convergence of thermal management and NVH engineering, driven by EV battery safety requirements. Companies such as 3M are integrating Glass Bubbles, advanced adhesives, and ceramic-enhanced thermal-acoustic composites to create materials that simultaneously insulate sound and act as protective heat barriers around battery modules and e-powertrain components. Production efficiency innovation is also emerging—3M’s collaboration with Halco to laminate high-performance adhesive tapes onto fastening materials streamlines acoustic component assembly for high-volume vehicle manufacturing. With CAFE standards pressuring OEMs to cut vehicle mass, U.S. manufacturers are adopting lightweight foams, engineered polymers, and multi-function NVH solutions, reinforcing the U.S. as a leader in high-performance, regulation-driven NVH material development.

Japan: Acoustic Meta-Materials and Precision Damping Compounds for High-Fidelity Automotive NVH Control

Japan continues to lead in advanced acoustic materials, meta-material sound insulation, and precision damping technologies, supported by its long-standing expertise in materials science and automotive engineering. A notable breakthrough is Nissan’s development of an acoustic meta-material, offering the same sound isolation performance as traditional rubber mats at only 25% of the weight. This innovation is strategically aligned with Japan’s focus on improving EV energy efficiency and cabin refinement without compromising environmental sustainability or material recyclability.

Japanese Tier 1 suppliers such as Sumitomo Riko are deepening investments in precision-molded elastomers, rubber-metal bonding technologies, and structural damping components designed to minimize low-frequency harshness and high-frequency vibrations across combustion, hybrid, and electric platforms. Their precision-engineered damping systems optimize engine mounts, bushings, suspension components, and subframe isolators, addressing the evolving vibration signatures of EVs, including torsional motor ripple and inverter-induced oscillations. With expertise spanning functional materials, advanced elastomers, and next-generation acoustic science, Japan remains a pivotal innovation hub for lightweight NVH materials and high-reliability vibration control solutions.

Competitive Landscape: Material Science Leaders Delivering Lightweight, Sustainable & High-Frequency NVH Solutions

The competitive field for Automotive NVH Materials is defined by suppliers that combine elastomer chemistry, engineered foams, recycled textile platforms, acoustic simulation expertise and high-volume validation. Leaders differentiate through EV-specific product portfolios (battery isolation, e-motor encapsulation), sustainability credentials, and the ability to deliver lightweight, recyclable NVH subsystems at automotive scale.

Vibracoustic (Freudenberg Group) - EV-specialized vibration control, battery isolation and hydro-bushing systems

Vibracoustic is a global NVH specialist whose portfolio spans engine mounts, chassis mounts, air springs and mass dampers. The company has recently prioritized EV-specific NVH (battery pack isolation systems and hydro bushings) that address torsional bending and high-frequency excitations in body-on-chassis platforms. Vibracoustic’s integrated approach combines elastomer formulation with structural mounts and advanced NVH modelling, positioning it as a systems OEM partner for premium and commercial EV programs.

Autoneum Holding AG - Lightweight acoustic absorbers and textile-based NVH systems at scale

Autoneum leads in vehicle acoustic and thermal management, focusing on lightweight absorbers (including r-PET solutions), floor and headliner systems. Its acquisition of Borgers Automotive expanded textile integration and vertical capability, enabling Autoneum to deliver low-mass, high-NRC NVH modules that meet OEM weight and sustainability targets. The company’s expertise in textile laminates and engineered foam stacks makes it a preferred tier-1 for global OEM NVH programs.

Hutchinson SA - Elastomer expertise and validated high-volume e-motor acoustic encapsulation

Hutchinson specializes in rubber and elastomer technologies for sealing, mounts and encapsulation. It developed a lightweight, recyclable e-motor acoustic encapsulation validated for >600,000 vehicles annually, and continues to introduce PFAS-free surface treatments and thermally optimized NVH solutions showcased at battery and mobility events. Hutchinson’s strengths lie in elastomer compound development and scalable production for both thermal management and acoustic isolation.

Sika AG - Sealants, damping sheets and sustainability-driven NVH chemistries

Sika is a major supplier of damping sheets, acoustic sealants and liquid applied sound deadeners (LASD). Its EcoVadis Silver Medal in November 2025 highlights its progress in low-VOC formulations and circular product development. Sika’s materials are commonly robotically applied in Body-in-White (BiW) processes, enabling precise, repeatable NVH damping while meeting stringent OEM sustainability and indoor-air quality requirements.

3M Company - Advanced polymers, Thinsulate™ acoustic materials and lightweight NVH innovations

3M brings broad materials science to NVH through vibration damping tapes, acoustic foams and Thinsulate™ lightweight acoustic insulation. The company’s portfolio of glass bubbles and specialty polymers supports density reduction strategies without compromising acoustic or mechanical integrity, enabling NVH weight targets to be met while maintaining high performance in the 500–4,000 Hz band critical to EV cabins.

BASF SE - PU systems and bio-based elastomers for sustainable acoustic foams and absorbers

BASF supplies key polyurethane chemistries and polymer resins used in molded acoustic foams and decoupling components. Its strategic focus on bio-based and circular PU systems enables NVH manufacturers to incorporate high recycled content while retaining foam performance and acoustic damping characteristics. BASF’s materials underpin many lightweight NVH modules and advanced absorber formulations used across passenger and commercial vehicle classes.

Automotive NVH Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.3 Billion

|

|

Market Size (2035)

|

$14.7 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material Type (Elastomers & Rubber, Polymer Foams, Fibers & Textiles, Thermoplastic Polymers, Metal Laminates, Engineering Resins), By Product Function (Sound Absorption Materials, Sound Insulation Materials, Vibration Damping Materials, Sealing Materials), By Application/Location (Interior, Exterior, Engine/Powertrain, Body-in-White, Chassis), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, Autonomous Vehicles)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Autoneum Holding AG, Vibracoustic GmbH, BASF SE, The Dow Chemical Company, 3M Company, Sumitomo Riko Company Limited, Henkel AG & Co. KGaA, Huntsman Corporation, Auria Solutions, DuPont de Nemours Inc., Saint-Gobain S.A., ElringKlinger AG, Trelleborg AB, Janesville Acoustics, Wolverine Advanced Materials LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive NVH Materials Market Segmentation

By Material Type

- Elastomers & Rubber

- Polymer Foams

- Fibers & Textiles

- Thermoplastic Polymers

- Metal Laminates

- Engineering Resins

By Product Function

- Sound Absorption Materials

- Sound Insulation Materials

- Vibration Damping Materials

- Sealing Materials

By Application / Location

- Interior

- Exterior

- Engine / Powertrain

- Body-in-White

- Chassis

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (BEV, PHEV)

- Autonomous Vehicles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Automotive NVH Materials Market

- Autoneum Holding AG

- Vibracoustic GmbH

- BASF SE

- The Dow Chemical Company

- 3M Company

- Sumitomo Riko Company Limited

- Henkel AG & Co. KGaA

- Huntsman Corporation

- Auria Solutions

- DuPont de Nemours, Inc.

- Saint-Gobain S.A.

- ElringKlinger AG

- Trelleborg AB

- Janesville Acoustics

- Wolverine Advanced Materials, LLC

*- List not Exhaustive