Market Overview: Sphericity, Thermal Conductivity Gains and Purity Demands Underpin the Spherical Silicon Carbide Market

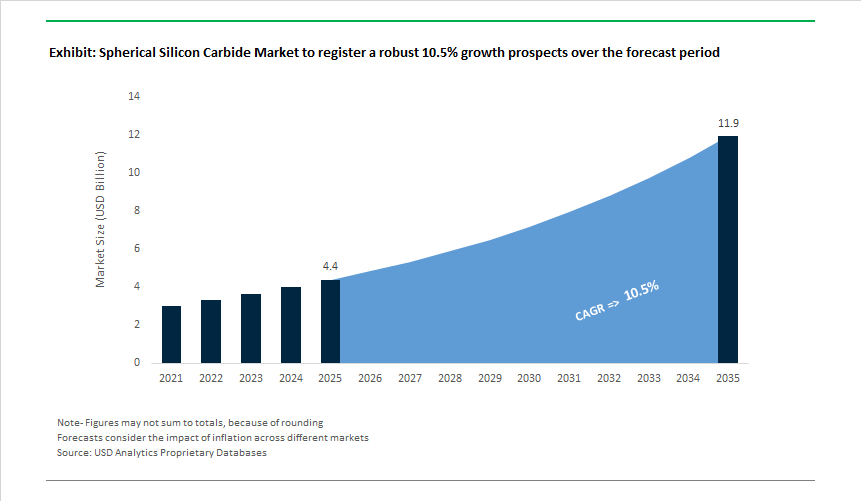

The Global Spherical Silicon Carbide (SiC) Market is valued at USD 4.4 billion in 2025 and is projected to reach USD 11.9 billion by 2035, expanding at a 10.5% CAGR as SiC becomes a core enabling material for electrification, high-power electronics, and advanced manufacturing. The market’s momentum is not being driven by incremental materials substitution, but by system-level redesigns in electric vehicles, power infrastructure, and semiconductor packaging where thermal performance, reliability, and miniaturization are becoming binding constraints.

Spherical SiC is benefiting from the structural shift toward wide-bandgap power electronics. As EV architectures move to higher voltages and faster switching frequencies, thermal management has emerged as a decisive bottleneck for power modules and inverters. OEMs are increasingly designing systems around materials that can dissipate more heat in less space, rather than compensating with larger housings or more complex cooling. In this context, spherical SiC has moved from a specialty filler to a design-critical input, particularly in thermal interface materials, encapsulation compounds, and high-density packaging.

The market’s value uplift is also linked to manufacturability and yield economics. Compared with irregular or angular powders, spherical SiC enables better flow, more uniform packing, and higher consistency in molding and coating processes. For electronics manufacturers, these attributes translate into higher production yields, fewer defects, and improved thermal reliability over product life cycles. As device makers scale volumes-especially in automotive and industrial power electronics-such yield and reliability gains have a direct impact on total cost of ownership, reinforcing long-term material lock-in.

Beyond electronics, precision abrasives and advanced ceramics provide a second, stabilizing demand pillar. Spherical SiC’s durability and consistency support longer tool life and tighter tolerances in polishing, lapping, and surface finishing applications used in semiconductor wafers, optical components, and high-performance mechanical parts. These industrial segments are less cyclical than consumer markets and benefit from ongoing investment in digital infrastructure, automation, and advanced manufacturing.

From a supply-side perspective, the market is entering a scale-and-integration phase. Downstream demand growth is increasingly predictable, but value creation is shifting toward suppliers that can guarantee consistent quality, secure supply, and proximity to OEM production hubs. This is driving closer coordination between powder producers, compound formulators, and device manufacturers, as well as selective vertical integration across the SiC value chain. Suppliers that can align material development with customer roadmaps are moving upstream in strategic importance.

Geopolitically, spherical SiC is also gaining attention as part of a broader semiconductor and EV supply-chain localization agenda. As governments and OEMs seek to reduce dependence on concentrated materials ecosystems, regional sourcing of critical powders and fillers is becoming a competitive differentiator rather than a cost penalty. This trend favors established producers with global footprints or the ability to scale localized capacity near automotive and semiconductor clusters.

Market Analysis: Sic Supply-Chain Shifts, Wafer Roadmap Advances and Vertical Integration Accelerating Commercialization

The Spherical SiC market has seen a rapid sequence of strategic moves and technology milestones that are reshaping supply chains and end-market economics. India moved to localize SiC device manufacturing with a major investment to establish its first domestic SiC semiconductor fab (March 2025), signalling new regional demand for spherical SiC powders for packaging and module assembly. Parallel wafer-scale technology progress (February 2025) by a leading power semiconductor vendor announced commercial 200 mm SiC product rollouts that will expand usable wafer area and reduce per-wafer cost, thereby materially increasing the volumes of thermal management fillers and substrate materials required by power module OEMs. Consolidation in device supply occurred with a strategic acquisition that strengthened an integrated vendor’s access to SiC JFET IP and device platforms (January 2025), improving vertical coordination across precursor to powder to device value chains.

Earlier milestones established the trend: onsemi’s introduction of SiC power-integrated modules for utility PV in December 2024 and Wolfspeed’s substrate capacity expansion in North Carolina (October 2024) emphasized continued investment upstream in wafers and substrates. Materials innovation is progressing on cost and scale too: academic work demonstrated a lower-cost synthesis route to spherical nano-SiC (≤1 µm) (September 2024), potentially cutting TIM material costs by up to 40%, while major device makers expanded fabrication lines (July 2024) and multi-year supply agreements with automotive OEMs (April 2024) locked in long-term, large-volume downstream demand.

Spherical Silicon Carbide Market Trends and Opportunities

Trend 1: Adoption in Precision Slurries for Wafer Backside Thinning

As advanced semiconductor packaging shifts toward heterogeneous integration, chiplet architectures, and 3D stacking, wafer thinning has become a yield-critical step rather than a back-end commodity process. In this context, spherical silicon carbide (SiC) is gaining rapid adoption in precision CMP and back-grinding slurries because particle morphology now directly determines device reliability. Technical studies published through 2025 show that spherical SiC particles with tightly controlled size distributions below 30 μm significantly reduce subsurface damage compared to angular abrasives, enabling surface roughness to be pushed into the sub-nanometer Ra range. This is essential as logic, memory, and wide-bandgap power devices are routinely thinned to below 100 μm, where microcracks or stress concentrations can propagate into catastrophic wafer breakage. Beyond surface finish, spherical SiC also lowers internal stress accumulation during high material-removal-rate operations, reducing rupture risk in SiC and silicon wafers used for advanced power electronics. The same morphology advantage is now extending into thermal interface and encapsulation materials. Patent activity in late 2025 highlights how high-sphericity SiC fillers, when blended in multi-modal particle systems, achieve tighter packing density and lower interfacial thermal resistance. This creates continuous 3D heat-conduction pathways that are increasingly specified in AI accelerators, advanced memory modules, and high-power smartphone processors, where thermal margins are shrinking faster than transistor geometries.

Trend 2: Spherical SiC-Reinforced Metal Matrix Composites for Extreme Environments

Aerospace and defense programs are accelerating the transition from traditional aluminum alloys to spherical SiC-reinforced metal matrix composites (MMCs) as mass reduction and dimensional stability become mission-critical. Powder-metallurgy-based SiC/Al composites containing roughly 15–20% spherical SiC are now being qualified for satellite structures, optical benches, and thermal control components because they combine high stiffness with low coefficients of thermal expansion. Compared to whisker or angular reinforcements, spherical SiC delivers more uniform particle dispersion, isotropic mechanical behavior, and predictable thermal conductivity across complex geometries—key advantages for spaceborne platforms exposed to rapid thermal cycling. Manufacturing data published in 2025 confirms that spherical particles also improve powder flowability during compaction and casting, reducing tool wear and machining defects that historically limited MMC adoption. These material benefits are being reinforced by policy-driven investment. Strategic funding allocated in late 2025 to unconventional mineral processing and advanced ceramics is explicitly supporting domestic production of high-purity spherical SiC powders for armor systems, satellite electronics, and next-generation defense communication infrastructure. As military platforms push further into hypersonic, orbital, and electronic-warfare domains, spherical SiC-reinforced MMCs are moving from niche materials into standardized structural solutions.

Opportunity 1: Feedstock for Binder Jetting Additive Manufacturing

The industrialization of binder jetting is opening a structurally new demand channel for spherical silicon carbide as a high-performance ceramic feedstock. Unlike laser-based additive processes, binder jetting depends heavily on powder flowability, packing density, and uniformity to achieve dimensional accuracy and mechanical integrity in printed parts. Spherical SiC powders offer clear advantages here, delivering higher bulk density and smoother layer deposition that enable near-net-shape fabrication of complex geometries with internal channels. Research conducted between 2024 and 2025 demonstrates that green-part strength in binder-jetted ceramics correlates strongly with particle sphericity, as uniform packing reduces stress gradients during debinding and sintering. This is particularly valuable as manufacturers shift from solid printing to shell-based architectures, which shorten debinding cycles and reduce binder-related defects. Industrial users are now qualifying spherical SiC for high-temperature heat exchangers, catalyst supports, and reaction hardware where conventional machining is cost-prohibitive or geometrically impossible. As chemical processing, energy, and aerospace industries increasingly demand customized ceramic components with short lead times, spherical SiC is emerging as an enabling material for scalable ceramic additive manufacturing.

Opportunity 2: Abrasive Media for Infrastructure Refurbishment and Surface Preparation

Tightening occupational health standards and environmental regulations are reshaping the abrasive blasting market, creating a durable opportunity for spherical SiC as a high-performance, recyclable alternative to silica sand. With regulators intensifying controls on crystalline silica exposure due to silicosis risk, industrial maintenance operators are shifting toward abrasives that generate less dust and degrade more slowly. Spherical SiC meets these requirements while offering superior hardness and durability, allowing multiple reuse cycles without significant loss of cutting efficiency. In large-scale marine, pipeline, and bridge refurbishment projects, the spherical morphology produces a controlled peening effect that efficiently removes corrosion while minimizing substrate damage—an increasingly important requirement for extending asset life rather than replacing infrastructure. This performance profile aligns closely with the surge in government-funded refurbishment programs, where coating longevity targets of 30 years or more are now common. As infrastructure owners prioritize lifecycle cost reduction and worker safety alongside performance, spherical SiC is becoming a preferred abrasive medium for heavy-duty surface preparation in corrosive and high-risk environments.

Market Share Analysis: Spherical Silicon Carbide Market

Market Share by Particle Size: 30–50 μm Spherical SiC as the Thermal Filler Sweet Spot

The 30–50 μm particle size segment, commanding around 45% of global spherical silicon carbide demand in 2025, has become the market’s structural core because it uniquely balances maximum thermal conductivity, ultra-high filler loading, and automated processability—three criteria that define commercial success in advanced thermal management. Within this band, materials such as Shinano-SiC’s SSC-A40 grades deliver thermal conductivity approaching 270 W/m·K, enabling TIM formulations that outperform conventional silicon fillers by more than 2.5× at the system level. Equally decisive is particle geometry: manufacturers including Denka now guarantee >0.95 sphericity, allowing compounders to push SiC loadings to ~80 wt% without triggering viscosity spikes that would otherwise disrupt high-speed dispensing and injection molding. This size range also aligns precisely with modern bond-line thickness requirements in miniaturized power modules, where system footprints have shrunk by up to 300% through SiC-based thermal architectures. Beyond performance, the segment delivers a tangible manufacturing advantage—spherical particles act as micro-bearings, cutting abrasive wear on pumps and nozzles by ~50%, a cost-of-ownership lever that procurement teams increasingly prioritize. These combined performance-economics dynamics explain why 30–50 μm spherical SiC has consolidated its lead as the default industrial specification.

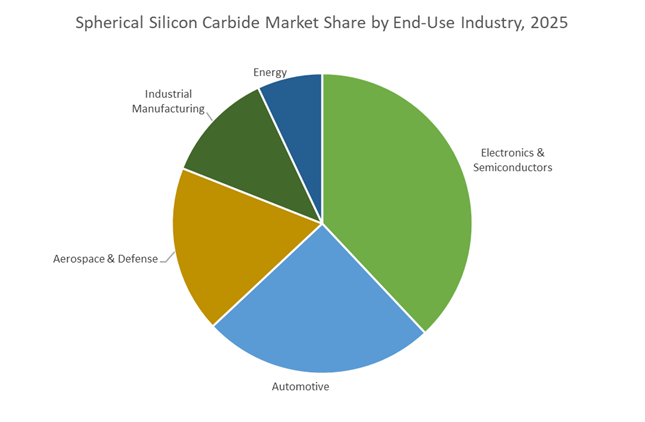

Market Share by Application: Electronics & Semiconductors Driving High-Value Adoption

Electronics and semiconductors, accounting for approximately 38% of total market value, represent the most influential demand center for spherical silicon carbide because thermal management has become a first-order constraint on chip performance, yield, and energy efficiency. As the broader SiC materials ecosystem scales beyond $10 billion in 2025, the spherical niche has emerged as the highest-value sub-segment, tightly linked to the industry’s transition from 150 mm to 200 mm wafer platforms at leaders such as Wolfspeed. In advanced packaging, spherical SiC fillers embedded in epoxy molding compounds and TIMs have demonstrated up to 60% reductions in junction temperature, translating directly into 5–10% system-level energy efficiency gains for data centers and power electronics OEMs. This performance threshold has become non-negotiable for AI and high-performance computing workloads, where heat densities routinely exceed 200°C operating limits and alternative fillers fail. Purity standards further reinforce the segment’s dominance: semiconductor-grade spherical SiC now requires 99.9995% ultra-high purity, as supplied by players such as CoorsTek, ensuring zero metallic contamination in 2 nm and 3 nm fabrication environments. With AI server racks, EV power modules, and advanced logic devices all converging on extreme thermal loads, electronics and semiconductors remain the primary value engine anchoring spherical silicon carbide demand.

Spherical Silicon Carbide Market Share by End-Use Industry

Competitive Landscape: Specialized Sic Powder Producers and Integrated Materials Players Capture Value Across Tims, Abrasives and Electronic Substrates

The Spherical SiC competitive field blends specialist powder producers that focus on ultra-high purity and sphericity with global materials conglomerates that leverage integration to serve large industrial customers. Competitive differentiation centers on particle-size control, surface treatments for resin compatibility, impurity management, and localized supply to major semiconductor and EV OEM clusters.

Fujimi Corporation - Specialist Supplier Of Ultra-Fine Spherical Sic Powders Optimized For Thermal Management

Fujimi offers a focused product line of ultra-high-purity spherical SiC powders (1-30 µm PSD) tailored for TIMs and electronic packaging. Its technical capability in particle surface treatment and functionalization ensures excellent dispersion and resin wetting, critical for epoxy molding compounds and silicone TIMs. Fujimi’s strategy centers on direct supply relationships with semiconductor packaging houses and EV battery module manufacturers, leveraging tight PSD control and sphericity (>0.95) to maximise packing density and thermal performance.

Shin-Etsu Chemical Co., Ltd. - Chemical Process Leader Producing Semiconductor-Grade Sic Powders and Integrated Resin Systems

Shin-Etsu combines advanced chemical synthesis with resin expertise to deliver spherical SiC fillers integrated into EMC and compound systems for high-reliability electronics. The firm prioritizes impurity reduction (aiming below 5 ppm metals) to serve RF power and wide-bandgap device manufacturers. Its R&D pipeline focuses on lowering metallic contaminants and improving compatibility with miniaturized, high-temperature packaging trends in ADAS and consumer electronics.

Saint-Gobain - Global Advanced Materials Supplier With Scale For Abrasive and Structural Sic Markets

Saint-Gobain supplies spherical SiC grains and advanced ceramics for high-precision lapping, polishing and structural components across aerospace and refractory applications. Its global manufacturing footprint provides supply resilience for large-volume industrial customers and enables Saint-Gobain to bundle SiC with complementary ceramic and abrasive product portfolios. The company leverages SiC’s extreme hardness and thermal stability for wear-resistant coatings and demanding high-temperature uses.

ESK-SIC Gmbh - European Specialist Focusing On Ultrafine Morphologies and Batch Consistency

ESK-SIC produces high-quality spherical and ultrafine SiC grades for Europe’s precision ceramics and automotive supply chains, emphasizing rigorous quality control and PSD optimization. Its product range supports sintering aids, advanced technical ceramics and brake system components, where material consistency and low defect rates are critical to downstream performance. Strong domestic production positions ESK-SIC as a preferred partner for European OEM localization strategies.

Tokai Carbon Co., Ltd. - Vertically Integrated Carbon/Sic Producer Enabling Composite and Refractory Innovations

Tokai Carbon leverages vertical integration across carbon and SiC product lines to develop composite materials and advanced heat-sink solutions incorporating spherical SiC fillers. Their R&D targets niche high-dissipation applications-advanced heat sinks, refractory linings and hot-pressed structural ceramics-benefitting from Tokai’s process expertise in sintering and hot-press manufacturing. Integration capabilities allow tailored feedstock specification for specialized ceramic manufacturing processes.

China has formally entered what industry stakeholders describe as “Year One of 8-Inch Silicon Carbide”, marking a structural shift from laboratory-scale SiC development to mass industrialization of wide-bandgap power semiconductors. According to disclosures from the Ministry of Industry and Information Technology (MIIT), multiple domestic 200 mm (8-inch) SiC wafer lines moved into ramp-up mode in Q1 2025. This transition is strategically aimed at reducing per-device costs by 20–30%, which directly amplifies demand for 99.9%+ purity spherical SiC powders used in sintering aids, CMP slurries, and high-performance thermal coatings.

At the ecosystem level, provincial governments in Jiangsu and Shaanxi have launched “New Materials Funds” to accelerate purity upgrades and morphology control, explicitly targeting replacement of Japanese and U.S. imported spherical SiC powders. Downstream pull is intensifying as well: by 2025, more than 45% of premium Chinese EV models integrate SiC-based traction inverters, sharply increasing consumption of spherical SiC fillers in gap fillers, potting compounds, and encapsulants. China’s strategy is therefore not just capacity expansion, but full domestic substitution across the SiC value chain.

India – Semicon India CapEx and Atmanirbhar SiC Ecosystem

India has emerged as one of the fastest-growing strategic markets for spherical SiC, underpinned by sovereign semiconductor policy and aggressive capital incentives. A defining milestone came in November 2025 with the groundbreaking of SiCSem’s integrated SiC semiconductor facility in Odisha, following a ₹2,000 crore cabinet approval earlier in the year. Designed for 60,000 wafers per year, the plant instantly establishes domestic demand for high-grade SiC powders used in wafer preparation, polishing, and advanced packaging.

Parallel momentum is visible at RIR Power Electronics Limited, which received state backing for a SiC power electronics facility focused on high-voltage renewable and grid applications. Under the updated 2025 Semicon India Programme of the Ministry of Electronics and Information Technology (MeitY), ten approved projects now represent ₹1.6 lakh crore in cumulative investment, explicitly targeting a closed-loop SiC ecosystem. Within this framework, spherical SiC has become a strategic consumable, not a specialty additive.

Japan – Precision Spherical SiC and Thermal Interface Leadership

Japan continues to define the global quality benchmark for spherical SiC powders, particularly in thermal management systems for EVs and AI infrastructure. In January 2025, Wacker Chemie AG and Asahi Kasei jointly expanded their Wacker-Asahikasei Silicone (WAS) facility in Tsukuba, commissioning a new Thermal Interface Material (TIM) line. This line leverages high-fluidity spherical SiC fillers to achieve thermal conductivities approaching 270 W/m·K, while maintaining low viscosity at extreme filler loadings.

At CERAMIC JAPAN 2025, firms such as Fujimi Corporation showcased rounded silicon carbide fillers that dramatically reduce resin shear stress compared with angular SiC. Meanwhile, SEMICON Japan 2025 emphasized a national “Step 1-2-3” strategy, positioning SiC as essential for AI data-center cooling and next-generation GPU clusters. Japan’s leadership is therefore rooted in morphology control, dispersion science, and reliability, rather than volume alone.

United States – Re-Shoring and 200 mm SiC Vertical Integration

The United States has anchored its spherical SiC strategy around vertical integration and domestic security of 8-inch substrates, particularly for defense and EV supply chains. Wolfspeed’s Mohawk Valley Fab—the world’s first large-scale 200 mm SiC wafer facility—reached critical utilization milestones in 2025, driving a sharp increase in demand for high-purity SiC source powders and processing materials.

Following its acquisition of II-VI Incorporated, Coherent Corp. expanded domestic 200 mm SiC substrate production, reinforcing the importance of polycrystalline SiC feedstock quality. Policy tailwinds further amplify demand: the U.S. Department of Energy (DOE) projects EV sales reaching 6.8 million units annually in high-growth scenarios, triggering OEM mandates for SiC-based power electronics. As a result, spherical SiC has become a strategic upstream material, tightly linked to U.S. re-industrialization goals.

Germany – Green SiC Manufacturing and EU Semiconductor Autonomy

Germany occupies a central role in Europe’s SiC roadmap under the European Chips Act, combining semiconductor autonomy with energy efficiency mandates. Infineon Technologies highlighted in its 2024/2025 Annual Report a strategic pivot toward energy-efficient SiC power devices, scaling production across Dresden and Kulim while integrating spherical SiC-based thermal coatings to enhance module reliability.

From a systems perspective, the Federal Ministry for Economic Affairs and Climate Action (BMWK) has embedded SiC power converters into national SuperLink grid modernization projects, citing energy-loss reductions of up to 50% versus silicon. Concurrently, institutes such as Fraunhofer Society are advancing plasma-synthesized monodisperse spherical SiC nanoparticles, addressing agglomeration issues that limit filler performance. Germany’s focus is thus on reliability, sustainability, and EU-level supply security.

South Korea – Battery, Semiconductor, and Fusion Synergies

South Korea is rapidly integrating spherical SiC into a closed-loop ecosystem spanning specialty chemicals, batteries, semiconductors, and even fusion research. In January 2025, Wacker Chemie AG commissioned a new specialty silicone line in Jincheon, producing spherical-SiC-modified sealants and encapsulants tailored for the K-Battery industry’s thermal protection needs.

Beyond commercial electronics, the Korea Institute of Fusion Energy (KFE) continues to evaluate SiC-based composites for extreme thermal environments, validating material stability under fusion-relevant heat flux. South Korea also hosted ICSCRM 2025 in Busan, where its national semiconductor strategy emphasized the global transition toward SiC-based electricity infrastructure. This multi-sector integration positions South Korea as a high-growth, high-reliability market for spherical SiC.

National Strategic Development Matrix – Spherical Silicon Carbide Market

Spherical Silicon Carbide Market Matrix

|

Country

|

Key Driver

|

2025 Milestone

|

Primary Application

|

|

China

|

8-Inch Ramp-Up

|

“Year One” of 200 mm SiC lines

|

EV inverters, domestic substitution

|

|

India

|

CapEx Incentives

|

₹2,000 Cr SiCSem plant groundbreaking

|

Power electronics, Atmanirbhar Bharat

|

|

Japan

|

Thermal Precision

|

Wacker Tsukuba TIM line startup

|

AI cooling, high-loading fillers

|

|

United States

|

Vertical Integration

|

Wolfspeed 200 mm fab utilization

|

Defense, EV power modules

|

|

Germany

|

Energy Efficiency

|

Infineon green SiC module scaling

|

Grid modernization, renewables

|

|

South Korea

|

Battery Synergy

|

Wacker Jincheon specialty line

|

EV encapsulants, fusion research

|

Spherical Silicon Carbide Market Report Scope

Spherical Silicon Carbide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.4 Billion

|

|

Market Size (2035)

|

$11.9 Billion

|

|

Market Growth Rate

|

10.5%

|

|

Segments

|

By Particle Size (Below 30 µm, 30–50 µm, Above 50 µm), By Type (Black Spherical SiC, Green Spherical SiC), By Application (Filler Material, Ceramic Material, Coatings, Abrasives), By End-Use Industry (Electronics & Semiconductors, Automotive, Aerospace & Defense, Energy, Industrial Manufacturing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Fujimi Incorporated, Saint-Gobain Ceramics (Hexoloy), CoorsTek Inc., Washington Mills, AGC Inc., Advanced Abrasives Corporation, Infineon Technologies AG, STMicroelectronics, Wolfspeed Inc., ROHM Co. Ltd., Fuji Electric Co. Ltd., Mitsubishi Electric Corporation, Ningxia Darshan Silicon Industry Co. Ltd., Tokamak Energy / TE Magnetics, Microchip Technology Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Spherical Silicon Carbide Market Segmentation

By Particle Size

- Below 30 μm

- 30–50 μm

- Above 50 μm

By Type

- Black Spherical Silicon Carbide

- Green Spherical Silicon Carbide

By Application

- Filler Material

- Ceramic Material

- Coating

- Abrasives

By End-Use Industry

- Electronics & Semiconductors

- Automotive

- Aerospace & Defense

- Energy

- Industrial Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Spherical Silicon Carbide Market

- Fujimi Incorporated

- Saint-Gobain Ceramics - Hexoloy

- CoorsTek, Inc.

- Washington Mills

- AGC Inc.

- Advanced Abrasives Corporation

- Infineon Technologies AG

- STMicroelectronics

- Wolfspeed, Inc.

- ROHM Co., Ltd.

- Fuji Electric Co., Ltd.

- Mitsubishi Electric Corporation

- Ningxia Darshan Silicon Industry Co., Ltd.

- Tokamak Energy / TE Magnetics

- Microchip Technology Inc.

*- List not Exhaustive