Stilbene Market Valuation 2025–2034: $914.6 Million to $1,598.5 Million at 6.4% CAGR Driven by Optical Brighteners, Nutraceutical Stilbenoids, and Advanced Electronic Emitters

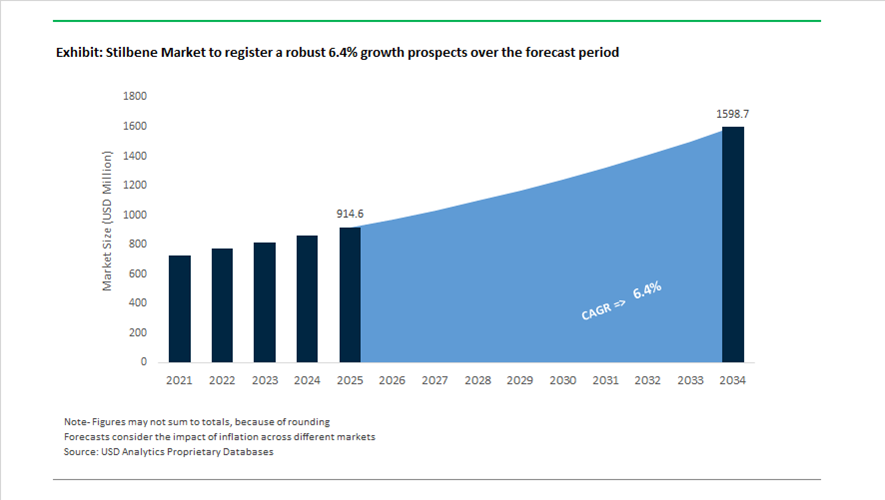

The global stilbene market is valued at $914.6 million in 2025 and is projected to reach $1,598.5 million by 2034, expanding at a CAGR of 6.4%. Demand spans stilbene-based optical brightening agents (OBAs), natural stilbenoids such as resveratrol and pterostilbene, high-purity stilbene crystals for scintillation, OLED emitter materials, and pharmaceutical chiral catalysts. Growth is supported by rising consumption of detergent brighteners, premium textile whitening agents, clean-label nutraceutical supplements, radiation detection systems, and next-generation display technologies. Manufacturers are restructuring portfolios toward high-margin specialty stilbene derivatives, sustainable synthesis routes, and regionally integrated production assets to improve supply resilience and regulatory compliance.

Industrial consolidation and green chemistry initiatives shaped 2024. In early 2024, Sunthetics secured $4 million in seed funding to commercialize an AI-driven electrochemical platform aimed at reducing waste-intensive petrochemical synthesis of stilbene compounds. In mid-2024, Clariant divested legacy intermediate lines, including standard stilbene-based dyes, to concentrate capital on higher-value care chemicals and specialty segments. In Q3 2024, Sigma-Aldrich expanded its portfolio with new stilbene-based chiral catalysts designed for asymmetric pharmaceutical synthesis, strengthening its position in advanced medicinal chemistry. In November 2024, PQ operationalized its expanded Indonesian facility, reinforcing its role as a regional hub for stilbene-derived optical brighteners serving textile and detergent markets across Southeast Asia. In late 2024, Kensing LLC finalized the acquisition of Advanced Organic Materials, enhancing its extraction capabilities for non-GMO resveratrol and pterostilbene targeting clean-label nutraceutical formulations.

Capacity expansion and application diversification accelerated through 2025. In February 2025, Denka commenced new production lines at its Omuta Plant in Japan, including high-purity stilbene crystals engineered for radiation detection and medical imaging scintillators. Throughout 2024 and 2025, Archroma integrated production assets in Ankleshwar, India following its acquisition of BASF’s stilbene-based OBA business, consolidating its position as a dominant supplier to the global paper and detergent sectors. In late 2025, collaborative research funded by leading nutraceutical companies launched an enhanced bioavailability formulation of pterostilbene, offering improved metabolic stability compared to conventional resveratrol. During 2025 Display Week, a consortium including Sumitomo Chemical showcased advanced stilbene-derived fluorescent emitters delivering improved blue-light purity and operational lifespan for OLED panels used in foldable smartphones and high-resolution displays.

Advanced materials innovation intensified entering 2026. In January 2026, Luxium Solutions introduced a new generation of organic stilbene scintillators optimized for fast-neutron detection in security screening and industrial non-destructive testing, providing superior gamma-ray rejection characteristics. In February 2026, Shin-Etsu opened its Pinghu City specialty facility in China, producing functionalized stilbene emulsions used in high-contrast electronic display films. These integrations, clean synthesis breakthroughs, OBA capacity expansions, nutraceutical formulation advancements, and optoelectronic innovations are reinforcing structural growth in the stilbene market through 2034.

Structural Market Trends and Monetizable Opportunities in the Stilbene Market

OBA-Led Recycled Fiber Upgrading for Premium and E-Commerce Packaging

The Stilbene Market is structurally anchored to the global shift toward recycled and sustainably sourced paper packaging, where visual performance has become a non-negotiable commercial parameter. As brand owners commit to 100% recyclable or recycled packaging targets between 2025 and 2030, paper mills face a persistent challenge linked to recycled fiber discoloration, including graying and yellowing caused by lignin residues and fiber aging. Stilbene-based Optical Brightening Agents, particularly triazine-stilbene derivatives, have emerged as the dominant chemical solution to offset this aesthetic penalty while maintaining process compatibility with high-speed paper machines.

By 2024–2025, stilbene chemistries accounted for approximately 57.3% of the global OBA market, reflecting their superior affinity for cellulose and their ability to deliver ISO brightness levels above 90 even at high recycled fiber inclusion rates. This performance advantage is especially critical for e-commerce packaging, luxury retail boxes, and folding cartons, where shelf appeal and brand perception directly influence consumer behavior. Strategic sustainability-driven partnerships are reinforcing this trend. In October 2024, BASF expanded collaborations across Southeast Asia to scale low-impact and sustainable OBA portfolios for recycled paper grades. This initiative followed the March 2024 launch of Luminous by Novonesis, an enzyme-based biodegradable brightener platform. Collectively, these developments signal a clear market pivot toward stilbene-based OBAs that meet UN Sustainable Development Goals while preserving high visual performance benchmarks required by premium packaging customers.

Regulatory Elimination of Halogenated Flame Retardants in Electronics

A second structural trend supporting the Stilbene Market is the accelerated transition toward halogen-free flame retardant systems in electronics, driven by tightening regulatory frameworks under REACH and RoHS. Brominated flame retardants, long used in polyamides, epoxy laminates, and electronic housings, are being systematically phased out due to toxicity and persistence concerns. This regulatory pressure has created a substitution-driven demand for phosphorus-based halogen-free flame retardants, where stilbene-linked intermediates play a critical synthesis role.

Regulatory momentum intensified in late 2025 when the European Chemicals Agency classified Decabromodiphenyl Ethane as a Substance of Very High Concern. This designation triggered immediate reformulation efforts across electronics, EV components, and insulation materials to maintain UL94 V-0 fire ratings without halogenated additives. In response, chemical innovators are advancing DOPO-based and stilbene-integrated phosphorus systems that deliver thermal stability, low smoke density, and enhanced char formation. In December 2025, Clariant and LANXESS, through the pinfa industry association, highlighted next-generation phosphinate solutions engineered for e-mobility components and high-performance insulation foams. These systems are increasingly specified for EV battery housings and semiconductor enclosures, reinforcing stilbene’s relevance in safety-critical electronics applications.

Stilbene-Based Photoinitiators for LED-Driven Additive Manufacturing

The rapid evolution of vat photopolymerization technologies, including SLA and DLP 3D printing, is unlocking a high-margin opportunity for stilbene-based photoinitiators. As the industry migrates toward LED light sources operating at 365–405 nm, conventional photoinitiators face limitations related to poor absorption efficiency and post-cure yellowing. Stilbene derivatives are emerging as a differentiated one-component solution that aligns precisely with these wavelength requirements.

Peer-reviewed research published during 2024–2025 in Macromolecules demonstrated that newly engineered stilbene-based iodonium salts achieve absorption efficiencies between 62% and 64% at 365 nm, materially outperforming legacy initiator systems. This performance enables faster curing, higher resolution, and improved surface finish without discoloration. The most commercially attractive applications are in dentistry and medical devices, where precision and biocompatibility are mandatory. Experimental data indicate cell viability rates exceeding 90% when using stilbene-based photoinitiators, making them well suited for dental crowns, surgical guides, and patient-specific implants. As regulatory scrutiny over medical polymers intensifies, this segment represents a structurally defensible growth avenue for the Stilbene Market.

Fluorescent Stilbene Taggants for Anti-Counterfeiting and Brand Security

Global counterfeiting has evolved into a technologically sophisticated threat, pushing brand owners toward covert authentication systems rather than overt visual markers. Stilbene compounds are increasingly being engineered as fluorescent molecular taggants that provide a unique optical signature detectable only under specific UV wavelengths. This capability positions stilbenes as a core material in next-generation brand protection strategies.

The UV fluorescent anti-counterfeit label segment reached an estimated value of $3.4 billion in 2024, with pharmaceuticals and luxury goods representing the fastest-growing end users. Regulatory frameworks such as the U.S. Drug Supply Chain Security Act and EU serialization mandates are accelerating adoption of multi-layer authentication that includes invisible fluorescent markers embedded in inks, coatings, adhesives, and even liquid formulations. In 2025, security material innovators such as Angstrom Technologies advanced stilbene-based pigments responsive to UV-A wavelengths around 365 nm. These covert taggants enable rapid, non-destructive verification across global supply chains, significantly raising the barrier for counterfeiters. As brand owners prioritize both regulatory compliance and revenue protection, this opportunity strengthens the long-term strategic relevance of stilbene chemistries beyond traditional OBAs.

Stilbene Market Share and Segmentation Insights

Trans-Stilbene Leads the Stilbene Market Due to Dominance in Optical Brightener Production

Trans-stilbene accounted for 48.60% of the stilbene market in 2025, making it the leading stilbene type used across industrial chemical manufacturing. Its molecular structure provides the stability and fluorescence required for producing optical brighteners used in paper, textile, and detergent industries. These brighteners enhance material whiteness by absorbing ultraviolet light and re-emitting visible blue light, creating the perception of higher brightness in finished products. Trans-stilbene also serves as the foundational intermediate for several stilbene-based derivatives used in chemical synthesis and specialty materials. The 2025 industry trend shows strong linkage between trans-stilbene demand and global optical brightener consumption, particularly in premium paper grades and high-performance textile finishing applications.

Optical Brighteners Drive Global Stilbene Consumption Across Paper and Textile Manufacturing

Optical brighteners accounted for 48.60% of stilbene market demand in 2025, representing the largest application segment due to their critical role in paper whitening, textile finishing, and detergent formulation. Stilbene-derived fluorescent whitening agents improve visual brightness and product appearance in industries where whiteness is a key quality parameter. Paper manufacturers use optical brighteners to achieve high-brightness printing papers and premium packaging materials, while textile producers rely on them for whitening synthetic and natural fibers. The 2025 development focus is the advancement of environmentally improved stilbene-based brighteners, where manufacturers are developing formulations with enhanced biodegradability and reduced aquatic toxicity to meet environmental regulations while maintaining high whitening performance.

Stilbene Market Competitive Landscape Driven

The stilbene market in 2026 is evolving toward high-purity derivatives, scintillation-grade materials, and low-PCF optical brighteners. Demand is driven by OLED dopants, nuclear detection, and sustainable textiles, with industry leaders focusing on backward integration, spectral precision, and regulatory-compliant chemistries.

Merck KGaA Expands High-Purity Stilbene Portfolio for OLED Research and Semiconductor Applications

Merck KGaA is reinforcing its leadership in high-purity stilbene derivatives through its Life Science and Electronics segments. The company reported €21.1 billion in 2025 sales, with its Electronics business expected to grow 3%–7% in 2026, driven by semiconductor recovery. Merck is prioritizing >99% purity stilbenes for OLED dopants, display R&D, and laboratory reagents. Its integrated Science & Lab Solutions platform enables seamless scaling from research-grade synthesis to industrial production. The company also supplies stilbene-based antioxidants like resveratrol for pharmaceutical and cosmetic applications. Strategic trade alignment with the U.S. market enhances supply chain efficiency for specialty chemical intermediates.

TCI Chemicals Strengthens Custom Synthesis and High-Purity Stilbene Supply for Advanced Materials Research

TCI Chemicals is a global leader in high-purity stilbene isomers, catering to precision applications in materials science and analytical chemistry. Its portfolio includes specialized derivatives such as 1,4-Bis(2-methylstyryl)benzene for liquid scintillation counting and brominated stilbenes for organic semiconductor synthesis. The company’s custom synthesis capabilities support rapid production of niche stilbene derivatives for pharmaceutical and optoelectronic R&D. TCI’s AI-powered digital tools enable researchers to select compounds based on photophysical properties and emission wavelengths. Its extensive catalog of over 30,000 compounds enhances responsiveness to emerging demand. TCI remains a critical supplier for non-linear optical materials and high-performance fluorescent systems.

Sudarshan Chemical Expands Low-PCF Stilbene-Based Optical Brighteners Through Heubach Integration

Sudarshan Chemical is scaling its stilbene-based optical brightener portfolio following the integration of the Heubach Group. The company is focusing on low Product Carbon Footprint (PCF) solutions aligned with global sustainability mandates. Its stilbene chemistry is widely used in enhancing brightness of recycled plastics and coatings, particularly in automotive OEM applications. The company showcased NIR-detectable and recycling-friendly pigment solutions at PlastIndia 2026. Sudarshan is transitioning toward application-ready systems, offering integrated shade-matching solutions for global coatings manufacturers. Its expanded global footprint strengthens its position in high-performance pigment and optical brightener markets.

Inrad Optics Leads Scintillation-Grade Stilbene Crystal Production for Radiation Detection and Defense Applications

Inrad Optics is the benchmark provider of scintillation-grade trans-stilbene crystals for radiation detection and nuclear security. Its solution-grown stilbene crystals offer superior pulse shape discrimination, enabling precise differentiation between neutron and gamma radiation. The company has scaled production of large-format crystals exceeding 100 mm diameter to meet rising demand in border security and spectroscopic systems. Its products are widely used in medical imaging technologies such as PET/CT scanners. Inrad’s vertically integrated manufacturing combines crystal growth, precision machining, and coating technologies. Its focus on high-performance optical components supports defense, aerospace, and homeland security sectors.

Archroma Advances Sustainable Stilbene Optical Brighteners for Textile and Paper Applications

Archroma is leading the shift toward sustainable stilbene-based optical brighteners with a strong focus on PFAS-free and biodegradable chemistries. Its Leucophor® range is being reformulated to meet stringent EU REACH and environmental compliance standards. The company plays a key role in the paper and packaging sector, enhancing brightness and opacity of recycled fibers for circular economy applications. Archroma’s local-for-local production strategy reduces supply chain emissions across major textile hubs. Its integrated system solutions combine optical brighteners with dyes and finishing agents to ensure consistent performance. The company is targeting high-durability textile applications requiring resistance to repeated washing and high-temperature processing.

China Stilbene Market Anchored by Textile Brighteners and Functional Materials

China remains the structural center of gravity for the global stilbene industry, driven primarily by its dominance in textile manufacturing and downstream chemical processing. Demand for stilbene-based Optical Brightening Agents continues to be concentrated in Zhejiang and Jiangsu, where textile clusters reported a marked transition in late 2025 toward low-toxicity stilbene derivatives. This shift reflects tighter domestic ecological labeling requirements and growing scrutiny on aromatic whitening agents used in export-oriented fabrics. Parallel to this, China’s Green Manufacturing Initiative, reinforced through the 2025 updates to the Green Bond Endorsed Project Catalogue, has redirected capital toward solvent-free and low-emission synthesis routes for trans-stilbene, improving compliance across large-volume intermediate plants.

Beyond textiles, China is expanding the functional scope of stilbenes. Research institutes in Suzhou successfully commercialized stilbene-functionalized OLED materials in 2025, delivering a documented 12% improvement in blue-light emission efficiency for domestic display panels. Regulatory developments are equally influential. New safety assessment rules introduced by the National Medical Products Administration in 2025 have formalized the use of oxyresveratrol as a regulated cosmeceutical ingredient, enabling its adoption in premium skin-brightening formulations. At the industrial level, wastewater monitoring mandates across the Yangtze River Economic Belt have increased demand for stilbene-based fluorescent tracers, while pharmaceutical producers in Hubei expanded output of stilbene-Z and stilbene-E isomers for oncology and estrogen-modulating drug intermediates.

United States Stilbene Market Defined by Advanced Materials and Bioavailability

The United States stilbene market is increasingly innovation-driven, with emphasis on green synthesis, electronic-grade purity, and high-value health applications. In 2025, Sunthetics demonstrated the commercial feasibility of AI-optimized electrochemical stilbene production, reporting a 20% reduction in process waste versus conventional thermal pathways. This aligns with broader federal support under the CHIPS and Science Act, which has incentivized domestic development of high-purity trans-stilbene for lithography-adjacent photoresponsive materials and niche semiconductor uses.

Scientific validation continues to expand application depth. Data published by the National Renewable Energy Laboratory in late 2025 showed record timing resolution from stilbene-doped scintillators, accelerating interest from nuclear medical imaging and radiation detection sectors. In parallel, nutraceutical demand has shifted decisively toward pterostilbene, driven by its superior bioavailability under the DSHEA compliance framework. Security applications are also emerging, with exploratory work by the U.S. Bureau of Engraving and Printing on fluorous (E)-stilbene derivatives for advanced anti-counterfeiting substrates.

France Stilbene Market Shaped by Circular Bio-Extraction and Clinical Research

France occupies a differentiated position in the stilbene value chain through bio-based sourcing and pharmaceutical research. The StilNov joint laboratory initiative between ACTICHEM and GESVAB, expanded in 2025, has focused on extracting high-purity resveratrol derivatives from vine and wine by-products, reinforcing France’s leadership in agro-industrial upcycling. This approach is tightly aligned with the EU Circular Economy Action Plan, transforming grapevine bark and winery waste into high-margin cosmetic and nutraceutical actives.

Research funding has further strengthened demand fundamentals. New grants issued in late 2025 by the French National Research Agency have supported clinical investigations into stilbenoids as neuroprotective agents, particularly for aging populations. These programs are driving sustained regional demand for pharmaceutical-grade stilbenes with consistent purity and traceability, positioning France as a center for medically validated stilbene applications rather than volume-driven production.

Japan Stilbene Market Focused on Electronic Purity and Molecular Engineering

Japan’s stilbene industry is anchored in advanced materials and electronics rather than traditional OBAs. In 2025, companies such as Tokyo Chemical Industry implemented ultra-high-purity filtration systems exceeding 99% purity to supply stilbene-based LED phosphors for emerging 6G infrastructure. These requirements reflect Japan’s stringent contamination thresholds for optoelectronic components.

Under the METI Green Innovation Fund, Japanese researchers achieved a breakthrough in rhodium-catalyzed ortho-olefination, significantly reducing the activation energy required for stilbene synthesis. This has opened pathways for cost-efficient production of highly specialized derivatives. Additionally, Japan’s electronics R&D centers debuted stilbene-based molecular switches in late 2025, exploiting cis-trans isomerization for experimental high-density data storage, underscoring the compound’s strategic relevance in next-generation information technologies.

Finland Stilbene Market Leveraging Forestry-Based Bioeconomy

Finland represents an emerging bio-based frontier for stilbenes, leveraging its forestry ecosystem. In 2025, Finnish industrial players successfully extracted stilbenoids from spruce bark at commercial scale, replacing petroleum-derived intermediates with renewable alternatives. This development aligns with Nordic bioeconomy strategies and positions stilbenes as value-added outputs of the pulp and paper sector.

Further downstream, Finnish research hubs validated a bolt-on valorization process that converts bark-press effluents into bio-based UV-filter ingredients. This innovation not only improves resource efficiency but also creates new revenue streams for forest operators, embedding stilbenes into integrated biorefinery models rather than standalone chemical production.

Indonesia Stilbene Market Driven by Textile Exports and Regulatory Alignment

Indonesia’s role in the stilbene industry is primarily consumption-led. Under the Indonesia 4.0 roadmap, textile manufacturers increased imports of stilbene-based whitening agents in 2025 to meet tightening quality expectations from European buyers. Export competitiveness has become closely linked to chemical compliance.

Regulatory convergence is accelerating this transition. In late 2025, Indonesia initiated harmonization of its chemical safety framework with EU REACH standards, compelling domestic OBA formulators to migrate toward more biodegradable stilbene derivatives. This alignment is reshaping supplier selection and favoring producers with proven environmental performance.

Comparative Snapshot: Stilbene Industry by Country

Stilbene Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Key Applications

|

Strategic Differentiator

|

|

China

|

Textile scale and policy mandates

|

OBAs, OLEDs, pharma intermediates

|

Integrated manufacturing and regulatory leverage

|

|

United States

|

Advanced materials and health

|

Scintillators, nutraceuticals, security

|

AI-driven synthesis and purity innovation

|

|

France

|

Circular bio-sourcing

|

Cosmetics, neuropharma

|

Vine by-product valorization

|

|

Japan

|

Electronics and photonics

|

LED phosphors, molecular switches

|

Ultra-high-purity and catalytic efficiency

|

|

Finland

|

Forestry bioeconomy

|

Bio-UV filters, stilbenoids

|

Bark-based renewable extraction

|

|

Indonesia

|

Export-oriented textiles

|

OBAs

|

EU-aligned regulatory transition

|

Stilbene Market Report Scope

Stilbene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$914.6 Million

|

|

Market Size (2034)

|

$1598.5 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Type (Trans-Stilbene, Cis-Stilbene, Stilbenoids), By Source (Synthetic, Natural and Bio-based), By Application (Optical Brighteners, Electronics and Photonics, Pharmaceuticals and Nutraceuticals, Cosmetics and Personal Care, Chemical Intermediates)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huntsman International LLC, BASF SE, Archroma, Eastman Chemical Company, Tokyo Chemical Industry Co., Ltd., Inrad Optics, Inc., Clariant AG, DayGlo Color Corp., Merck KGaA, Zhejiang Transfar Whyyon Chemical Co., Ltd., Rudolf GmbH, Milliken Chemical, Paramount Minerals and Chemicals, Actichem, Siansonic Technology

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Stilbene Market Segmentation

By Type

- Trans-Stilbene

- Cis-Stilbene

- Stilbenoids

By Source

- Synthetic

- Natural and Bio-based

By Application

- Optical Brighteners

- Electronics and Photonics

- Pharmaceuticals and Nutraceuticals

- Cosmetics and Personal Care

- Chemical Intermediates

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Stilbene Industry

- Huntsman International LLC

- BASF SE

- Archroma

- Eastman Chemical Company

- Tokyo Chemical Industry Co., Ltd.

- Inrad Optics, Inc.

- Clariant AG

- DayGlo Color Corp.

- Merck KGaA

- Zhejiang Transfar Whyyon Chemical Co., Ltd.

- Rudolf GmbH

- Milliken Chemical

- Paramount Minerals and Chemicals

- Actichem

- Siansonic Technology

*- List not Exhaustive