Market Overview: Battery Metal Demand Concentration and Refining Vulnerability Shape Strategic Mineral Materials Market Outlook

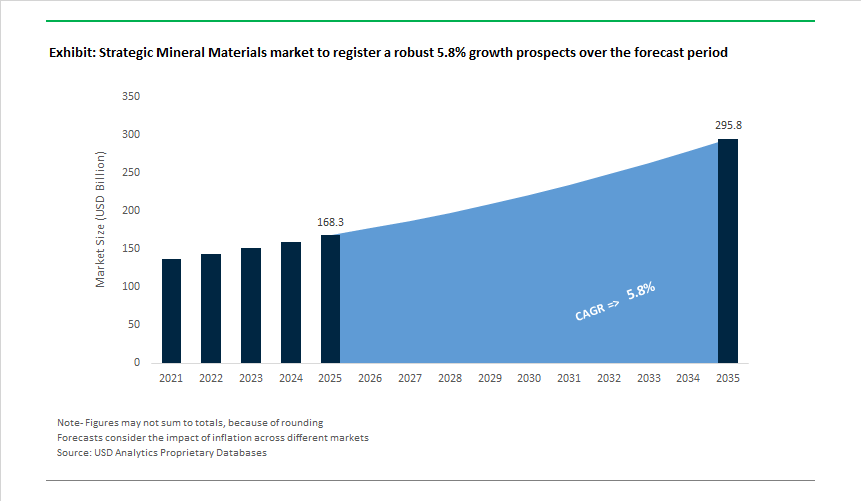

The Global Strategic Mineral Materials Market is valued at USD 168.3 billion in 2025 and is projected to reach USD 295.8 billion by 2035, expanding at a 5.8% CAGR as strategic minerals move from commodity inputs to nationally significant industrial assets. Today, market momentum is being shaped less by price cycles and more by demand concentration, refining bottlenecks, and geopolitical exposure, making strategic minerals central to both corporate strategy and public policy.

The defining force is the energy transition’s unprecedented material intensity. Electric vehicles, grid-scale storage, renewable power systems, and defense technologies are collectively driving structural demand for lithium, nickel, cobalt, graphite, and rare earths. Between 2020 and 2024, approximately 85% of incremental demand growth for key battery metals originated from energy-transition applications, fundamentally changing how these materials are sourced, financed, and secured. For OEMs and governments alike, access to strategic minerals is now a prerequisite for industrial competitiveness, not a procurement detail.

The demand surge is colliding with highly concentrated refining capacity, creating a systemic vulnerability. In several critical minerals, the top three refining nations control more than 80% of global processing output, giving downstream manufacturers limited flexibility in the event of trade disruptions, export controls, or geopolitical escalation. As a result, companies are increasingly assessing supply chains through a risk-adjusted lens, factoring in country exposure, refining chokepoints, and the resilience of midstream capacity rather than focusing solely on upstream reserves.

At the same time, defense-sector procurement is emerging as a parallel demand anchor, tightening availability for civilian markets. Strategic stockpiling programs-particularly for cobalt and rare earths-are competing directly with EV battery and electronics manufacturers for the same material streams. This overlap reinforces the strategic nature of these minerals: demand is not purely commercial and cannot be assumed to soften during economic slowdowns.

Despite these constraints, the market’s long-term upside remains compelling. A substantial share of global reserves-around 44% of rare earths and more than one-third of lithium resources-lies outside the current dominant supply countries. This creates a clear investment runway for new extraction, refining, and processing capacity in alternative jurisdictions, provided projects can clear permitting, financing, and ESG thresholds. Governments are increasingly supporting this shift through incentives, strategic partnerships, and offtake agreements aimed at accelerating diversification.

Market Analysis: Regulatory Shifts, M&A Consolidation, and National Critical Mineral Missions Reshape the Global Supply Chain

Recent developments show rapid restructuring across the Strategic Mineral Materials landscape, driven by government policy activation, consolidation among mining majors, and accelerated domestic supply chain initiatives. In December 2025, the US Department of Interior finalized its updated 2025 Critical Minerals List, elevating Rare Earth Elements and Tantalum as essential to national defense programs and signaling deeper federal investment into extraction and refining capacity. Also in December 2025, the Ontario Chamber of Commerce advocated for fast-tracked permitting and enhanced Indigenous partnerships to unlock Canada’s role in the North American Critical Minerals Supply Chain. These reforms are critical as OEMs seek stable feedstock for EV batteries, permanent magnets, and high-performance alloys.

M&A activity intensified in October 2025, when Rio Tinto completed its USD 6.7 billion acquisition of Arcadium Lithium, consolidating key hard-rock and brine resources and lifting its planned production capacity to over 200,000 MT LCE by 2028. On the other hand, market volatility surfaced when the DRC government implemented a four-month cobalt export ban in May 2025, aiming to correct oversupply dynamics. This elevated spot price uncertainty and underscored the sector’s geopolitical vulnerability. During the same month, Rio Tinto entered a major joint venture with Codelco in Chile to advance the Salar de Maricunga Lithium project, backed by a staged USD 900 million investment, strengthening future South American brine output.

National-level strategies further accelerated global supply chain diversification. India’s launch of the National Critical Mineral Mission (NCMM) in April 2025, with plans to auction 100+ exploration blocks, positions the country as an emerging supplier of REEs and Cobalt. In March 2025, MP Materials reported record NdPr production of 563 MT, a 36% sequential increase, illustrating rapid scaling of domestic REE refining crucial for EV traction motors and wind turbines. Earlier, in November 2024, Rio Tinto’s Rincon pilot plant in Argentina achieved first production of 3,000 MT of battery-grade lithium carbonate, advancing its Direct Lithium Extraction (DLE) roadmap. Collectively, these moves reflect strengthening national security strategies, industry consolidation, and accelerated investment in diversified supply streams.

Strategic Mineral Materials Market Trends and Opportunities

Trend 1: Onshoring of Mid-Stream Processing for Magnet Rare Earths

The strategic mineral materials market is undergoing a structural reset as governments move aggressively to onshore mid-stream rare earth processing, long considered the weakest link in Western supply chains. While upstream mining capacity has expanded modestly over the past decade, the conversion of rare earth oxides into high-performance neodymium-iron-boron (NdFeB) magnets has remained overwhelmingly concentrated in adversary-controlled regions. This imbalance is now being directly addressed through defense-led industrial policy. In July 2025, the U.S. Department of Defense initiated a landmark intervention by awarding multi-year funding to establish a fully sovereign NdFeB magnet ecosystem, targeting domestic output of roughly 10,000 tonnes per annum by 2028. This shift is not symbolic; it reflects recognition that permanent magnets are foundational to precision-guided munitions, advanced radar systems, electric propulsion, and next-generation aerospace platforms. Parallel investments are reinforcing the entire value chain. A $150 million, 12-year loan facility has been deployed to expand heavy rare earth separation circuits at Mountain Pass, enabling domestic processing of dysprosium, terbium, and samarium—elements essential for high-temperature, demagnetization-resistant magnets used in fighter aircraft and hypersonic systems. Allied integration further strengthens resilience: the DoD-backed Gulf Coast separation facility under the Lynas 2025 framework is designed to process Australian feedstock entirely outside traditional refined material routes. Collectively, these moves signal a decisive shift from market-optimized sourcing toward security-optimized industrial capacity, with long-term implications for pricing power, qualification cycles, and supplier consolidation in strategic mineral materials.

Trend 2: Strategic Stockpiling of High-Purity Defense Minerals

In parallel with onshoring, national stockpiling strategies are expanding at a pace not seen since the Cold War, fundamentally altering demand dynamics for high-purity strategic minerals. Rather than relying on just-in-time procurement, defense agencies are transitioning to state-directed accumulation to hedge against geopolitical disruption and supply weaponization. In October 2025, the U.S. Defense Logistics Agency confirmed plans to procure up to $1 billion in critical minerals under authorities expanded by the OBBA legislation, which allocates $7.5 billion to critical materials security, including $2 billion for the National Defense Stockpile. Unlike earlier stockpiling programs that focused on bulk materials, the current cycle is highly targeted toward purity-constrained metals with limited substitution pathways. Procurement priorities include cobalt for superalloys, antimony for flame retardant and ballistic applications, tantalum for advanced electronics, and indium for optoelectronic and sensing systems. The scale is disruptive: planned acquisition of 222 tonnes of indium alone equates to nearly 90% of total U.S. annual consumption, effectively crowding out commercial demand and tightening availability across civilian supply chains. Similar dynamics are emerging in bismuth and specialty alloying metals, where defense-grade specifications further restrict usable supply. This stockpiling wave is transforming strategic minerals from cyclical commodities into quasi-sovereign assets, where pricing, availability, and contract structures are increasingly shaped by national security priorities rather than industrial consumption alone.

Opportunity 1: U.S. Supply Chain Buildout for Battery-Grade Graphite Anodes

The battery materials segment presents one of the most capital-intensive opportunities within strategic mineral materials, driven by regulatory mandates that explicitly favor domestic and allied supply chains. Graphite, despite its abundance, has emerged as a critical bottleneck because over 90% of spherical purified graphite processing remains concentrated in China, creating compliance risk under the U.S. Inflation Reduction Act. This has catalyzed a rapid investment cycle in North American anode material production. A defining milestone occurred in November 2025 when Canada designated the Matawinie Mine–Bécancour Battery Material Plant complex as a Major Project of National Interest. The vertically integrated project, representing approximately $1.8 billion in capital investment, is engineered to deliver battery-grade spherical purified graphite using hydroelectric power, aligning both carbon intensity and traceability requirements. Commercial momentum has followed policy clarity: binding offtake agreements secured in late 2025 with Panasonic Energy and Traxys cover up to 20,000 tonnes per annum, providing the revenue certainty required for Final Investment Decisions. The strategic importance is amplified by downstream demand pull—planned U.S. battery cell capacity exceeding 1,100 GWh creates a captive market where IRA compliance determines eligibility for the full $7,500 EV consumer credit. As a result, domestic graphite is no longer competing on cost alone but on regulatory access, making this segment one of the most defensible and strategically insulated growth avenues in the mineral materials landscape.

Opportunity 2: Scandium Recovery from Industrial Waste Streams

Scandium represents a high-leverage opportunity where circular extraction models are redefining supply economics for advanced materials. Historically constrained by scarcity and price volatility, scandium’s commercial adoption has lagged despite its transformative impact on aluminum alloys and electrochemical systems. This dynamic is now shifting as producers unlock scandium from existing titanium and iron waste streams, bypassing the need for new greenfield mines. In November 2025, Rio Tinto and the Canada Growth Fund advanced a C$25 million transaction to expand scandium oxide production at the Sorel-Tracy complex in Quebec, increasing output from 4 tonnes to 12 tonnes per year through byproduct recovery. This model directly addresses the “scandium paradox” by stabilizing supply without escalating extraction costs. The implications span multiple strategic sectors. In clean energy, high-purity scandium oxide is a critical dopant for solid oxide fuel cells, where it enhances ionic conductivity and lowers operating temperatures, materially extending system lifetimes. In aerospace and defense, scandium-aluminum alloys deliver 10–15% strength improvements and superior weldability compared to conventional 7000-series alloys, enabling lighter airframes and improved fatigue resistance. The royalty-based structure of public funding ensures that this recovered supply remains prioritized for North American advanced manufacturing through 2030, positioning scandium as a rare example of a strategic mineral where sustainability, security, and performance advantages align into a durable, high-margin opportunity.

Market Share Analysis: Strategic Mineral Materials Market

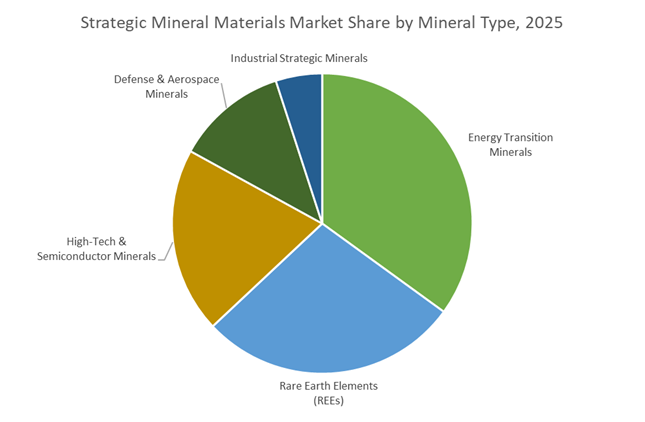

Market Share by Mineral Type: Energy Transition Minerals Anchor Policy-Driven Demand

Energy transition minerals—lithium, copper, nickel, and cobalt—command approximately 35% of the Strategic Mineral Materials Market because they sit at the intersection of industrial policy, capital allocation, and irreversible electrification trends. In 2025, this segment is no longer demand-led by cyclical manufacturing but by sovereign-backed capacity build-outs. Lithium illustrates this structural shift most clearly: forecasts from Albemarle and Ganfeng Lithium place global demand between 1.55 and 1.8 million metric tons LCE, a near-30% year-over-year expansion that effectively hard-codes lithium into national energy strategies. Copper reinforces the same dynamic at scale—Chinese producers such as Zijin Mining and Jiangxi Copper are on track to deliver ~10 million metric tons in 2025, underlining copper’s role as the physical backbone of electrification. Critically, price stabilization has restored investment confidence: lithium carbonate’s ~$21,000/ton floor marks a return to viable project economics after the 2023–24 correction. With Albemarle alone targeting >20% of global lithium supply, market share is increasingly concentrated among strategic majors—turning this segment into a policy-protected, capital-intensive core of the broader minerals market.

Market Share by Application: Clean Energy Consumption Redefines Mineral Intensity

Clean energy applications account for around 40% of total strategic mineral demand, overtaking traditional industrial uses as the dominant value sink in 2025. The driver is not unit growth alone but mineral intensity: benchmarks referenced by the IEA and industrial suppliers show that an electric vehicle requires 6–8× more copper than an internal combustion vehicle, fundamentally altering long-term demand curves. This effect compounds at the system level—grid-scale storage has surpassed 90 GWh of deployed capacity, and stationary batteries are now the second structural growth engine after EVs, with lithium-based storage demand expanding at ~30% CAGR toward 2030. The result is near-total sector dependence: by late 2025, 94% of global lithium consumption is tied directly to batteries, compared with 64% in 2020. Forward-looking supply gaps amplify the segment’s dominance—long-range modeling highlights a potential 19 million-ton copper shortfall against clean-energy demand by mid-century, a figure that has become a central risk metric for utilities, automakers, and governments alike. These dynamics explain why clean energy now absorbs the largest share of strategic minerals: it is not merely a high-growth end market, but the structural determinant of future supply security, pricing power, and geopolitical relevance.

Competitive Landscape: Integrated Miners, Refining Leaders, and National Supply Chain Champions Drive Strategic Mineral Material Competitiveness

The competitive environment in the Strategic Mineral Materials market is characterized by vertically integrated miners, government-backed refining assets, and companies expanding aggressively into battery-grade chemical processing. The strategic focus across leading firms includes upstream resource control, downstream refining, DLE technology adoption, cobalt and rare earth supply chain stabilization, and long-term contracting with EV battery manufacturers and defense agencies.

Rio Tinto - Aggressive Lithium Expansion and Multi-Mineral Integration Strengthen Global Strategic Materials Leadership

Rio Tinto has rapidly scaled its position through major acquisitions and technology investments, including the USD 6.7 billion acquisition of Arcadium Lithium in 2025, which immediately boosted its brine and hard-rock lithium portfolio. The company plans to expand its Rincon project to 60,000 MT LCE by 2028, deploying Direct Lithium Extraction to improve recovery and sustainability metrics. Beyond lithium, Rio Tinto leverages strong multi-mineral assets-including copper and borates-that underpin renewable energy infrastructure. Its strong financial capability and project development expertise enable it to progress major initiatives such as the Jadar borate-lithium project in Serbia.

CMOC Group Limited - The World’s Largest Cobalt Miner Anchors Global EV Battery Precursor Supply

CMOC Group remains the dominant force in global cobalt mining, having produced 114,000 tonnes from its DRC operations (TFM and KFM) in 2024-well above capacity expectations. The company has rapidly scaled copper and cobalt output, supporting global cathode precursor manufacturing and EV Battery Materials demand. Its downstream processing facilities in China ensure tight supply chain integration from mine to refined cobalt chemicals. CMOC’s aggressive expansion has reshaped global cobalt availability and positioned the company as a critical supplier for the lithium-ion battery ecosystem.

MP Materials - North America’s Rare Earth Refining and Permanent Magnet Revival Accelerates

MP Materials has emerged as the United States’ cornerstone REE supplier, reporting record NdPr oxide output of 563 MT in Q1 2025, driven by expanded refining capacity at Mountain Pass. The company maintains a strong national strategic role, supported by US government investment, including a 15% equity stake secured in 2024. MP Materials is restoring the full domestic REE supply chain by building magnet manufacturing capabilities to serve EV traction motors and wind turbine OEMs. It remains the only significant North American producer of rare earth concentrate.

Albemarle Corporation - Global Lithium Leader Advances High-Purity Hydroxide Capacity For Battery-Grade Materials

Albemarle maintains leadership in lithium through diversified Tier-1 assets, including the Greenbushes joint venture in Australia and brine operations in Chile’s Salar de Atacama. Its strategic focus centers on scaled production of high-purity lithium hydroxide optimized for nickel-rich NMC cathodes used in next-generation EV batteries. Albemarle supplies battery-grade materials with impurity levels often below 10 ppm, meeting stringent OEM quality thresholds. The company continues expanding hydroxide conversion facilities in the US and Europe, aligning with regional gigafactory supply chain development.

The United States has decisively shifted from critical minerals policy formulation to large-scale capital execution, embedding strategic mineral materials at the core of national economic security. The U.S. Geological Survey (USGS) finalized its 2025 Critical Minerals List, expanding coverage to 60 minerals, including copper, silver, lead, and silicon—materials now classified as indispensable for grid-scale electrification, defense electronics, and semiconductor manufacturing. This expansion has unlocked accelerated permitting, Defense Production Act (DPA) financing, and priority federal procurement access for domestic extractive and refining projects.

A defining milestone is the near-completion of E-Vac’s sintered NdFeB magnet facility in South Carolina, marking the first serious attempt to establish a fully domestic rare-earth magnet supply chain independent of Chinese refining. Complementing this, the U.S. secured a friend-shoring alliance with Malaysia, granting access to over 16 million tonnes of strategic reserves in exchange for processing technology and tariff relief. Collectively, these moves position the U.S. as a demand anchor and downstream integrator, with strategic minerals increasingly treated as defense infrastructure rather than commodities.

China – Tactical Export Leverage and Resource Preservation

China continues to dominate global strategic mineral refining, but its 2025 strategy reflects a shift from blunt export restrictions to surgical trade management. In November 2025, Ministry of Commerce of the People's Republic of China (MOFCOM) issued Announcement No. 70, temporarily suspending several export controls on rare earths, lithium-battery materials, and gallium/germanium until November 2026. This pause is widely viewed as a geopolitical bargaining instrument, offering supply stability while retaining the option to reimpose controls if negotiations deteriorate.

However, China has maintained tight controls on antimony and indium, essential for infrared optics and advanced semiconductor applications, resulting in ex-China price premiums of up to 40% by late 2025. Simultaneously, customs data shows a 150% surge in imports of raw molybdenum ores, signaling a deliberate policy of preserving domestic high-grade deposits while leveraging imported feedstock for value-added refining. China’s role is thus evolving from volume exporter to strategic gatekeeper of refined materials.

Australia – Billion-Dollar Buildouts and Defense Alignment

Australia has emerged as the primary Western alternative to Chinese strategic mineral supply, leveraging its low-ESG-risk jurisdiction and mature mining governance. In October 2025, Canberra and Washington formalized a $1 billion U.S.–Australia critical minerals financing framework, explicitly aligned with the AUKUS defense industrial base. This agreement accelerates mining, separation, and downstream processing approvals, transforming Australia into a strategic minerals security partner rather than a raw-material exporter.

At the project level, Tivan Ltd’s acquisition of the Molyhil tungsten–molybdenum project underscores Australia’s push toward vertically integrated critical minerals hubs. By December 2025, mining contributed over 12% of national GDP, with lithium, cobalt, nickel, and tungsten projects increasingly adopting transparent, standard-based pricing to counter non-market distortions. Australia’s strategic value now lies as much in reliability and governance as in resource abundance.

European Union – CRMA Execution and Processing Independence

The European Union has entered the implementation phase of the Critical Raw Materials Act (CRMA), translating policy into tangible project pipelines. In April 2025, the European Commission approved 47 strategic projects across 13 member states, spanning 25 extraction sites and 24 processing facilities, with lithium and graphite dominating the portfolio. The explicit objective is to achieve 40% domestic processing capacity by 2030, sharply reducing dependence on external refiners.

Regulatory acceleration is a cornerstone of this strategy: extraction permits are now capped at 27 months, while processing and recycling facilities are fast-tracked to 15 months. Among the most geopolitically significant initiatives is Verde Magnesium, identified as the EU’s sole strategic project to establish sustainable magnesium metal production, addressing near-total reliance on Chinese imports for automotive aluminum alloys. The EU is positioning itself as a rules-driven, processing-focused market, prioritizing resilience over cost arbitrage.

Brazil – Lithium Valley and Resource-Led Industrialization

Brazil’s strategic minerals profile has transformed rapidly, driven by its emergence as a hard-rock lithium powerhouse. In late 2025, national lithium resource estimates were upgraded by 350%, propelling Brazil to 7th globally. The Neves Project, led by Atlas Lithium, is on track to reach 150,000 tonnes per year of spodumene concentrate, positioning Brazil as a sustainable alternative to brine-based lithium producers.

Policy support under PlanGeo 2025–2034 prioritizes minerals tied to food security (phosphates, potash) and the energy transition (lithium, rare earths, nickel). Financially, Brazil launched a $200 million SME-focused strategic minerals fund, alongside an €820 million BNDES call targeting battery and magnet technologies. Brazil’s competitive edge lies in combining resource scale with downstream ambition, reshaping it into Latin America’s strategic minerals anchor.

Democratic Republic of Congo – Cobalt Quotas and Resource Nationalism

The Democratic Republic of Congo has fundamentally reasserted state control over cobalt, the backbone of global EV battery chemistry. In December 2025, the regulator ARECOMS granted a one-time carryover of unused Q4 cobalt export quotas, safeguarding 18,125 tonnes of delayed shipments and preventing market dislocation. This move stabilized logistics while reinforcing the legitimacy of the quota regime.

More structurally, the DRC has signaled a permanent annual export cap of 96,600 tonnes, with excess production redirected into a state-controlled strategic stockpile. This supply discipline triggered a dramatic cobalt price rebound, with cobalt hydroxide prices quadrupling to $24/lb by December 2025. The DRC is no longer a passive supplier—it is actively managing cobalt as a strategic macroeconomic lever.

2025 Strategic Mineral Policy Matrix

Strategic Mineral Policy Matrix

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Investment / Figure

|

|

United States

|

Defense & supply security

|

60 minerals on USGS list; NdFeB magnet reshoring

|

Federal DPA-backed financing

|

|

China

|

Tactical trade leverage

|

MOFCOM Announcement No. 70 export pause

|

150% surge in raw ore imports

|

|

Australia

|

Allied supply diversification

|

$1B U.S.–Australia minerals framework

|

Mining >12% of GDP

|

|

European Union

|

Processing independence

|

47 CRMA strategic projects approved

|

€22.5B initial investments

|

|

Brazil

|

Hard-rock lithium scale

|

350% lithium resource upgrade

|

$5.8B required by 2030

|

|

DRC

|

Resource nationalism

|

96,600t permanent cobalt export cap

|

$24/lb cobalt price (Dec 2025)

|

Strategic Mineral Materials Market Report Scope

Strategic Mineral Materials market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$168.3 Billion

|

|

Market Size (2035)

|

$295.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Mineral Type (Energy Transition Minerals, Rare Earth Elements, High-Tech & Semiconductor Minerals, Defense & Aerospace Minerals, Industrial Strategic Minerals), By Extraction & Source (Primary Mining, Secondary Recovery, Urban Mining/Recycling, Deep-Sea Exploration), By Processing Level (Ores & Concentrates, Refined Oxides & Salts, High-Purity Metals & Alloys, Specialty Precursors), By Application (Clean Energy, Defense & Aerospace, Digital Infrastructure, Healthcare, Industrial Manufacturing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Rio Tinto Group, BHP Group, Glencore plc, Freeport-McMoRan Inc., Albemarle Corporation, China Molybdenum Co. Ltd., Zijin Mining Group Co. Ltd., Anglo American plc, Vale S.A., ICL Group, SQM, MP Materials Corp., Lynas Rare Earths Ltd., Hindustan Zinc (Vedanta Limited), Eti Maden

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Strategic Mineral Materials Market Segmentation

By Mineral Type

- Energy Transition Minerals

- Rare Earth Elements (REEs)

- High-Tech & Semiconductor Minerals

- Defense & Aerospace Minerals

- Industrial Strategic Minerals

By Extraction & Source

- Primary Mining

- Secondary Recovery

- Urban Mining / Recycling

- Deep-sea Mineral Exploration

By Processing Level

- Ores & Concentrates

- Refined Oxides & Salts

- High-Purity Metals & Alloys

- Specialty Precursors

By Application

- Clean Energy

- Defense & Aerospace

- Digital Infrastructure

- Healthcare

- Industrial Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Strategic Mineral Materials Market

- Rio Tinto Group

- BHP Group

- Glencore plc

- Freeport-McMoRan Inc.

- Albemarle Corporation

- China Molybdenum Co., Ltd.

- Zijin Mining Group Co., Ltd.

- Anglo American plc

- Vale S.A.

- ICL Group

- Sociedad Química y Minera de Chile

- MP Materials Corp.

- Lynas Rare Earths Ltd

- Hindustan Zinc / Vedanta Limited

- Eti Maden

*- List not Exhaustive