Tab Leads and Tab Seal Film Market Size, Overview, and Growth Outlook (2025–2034)

Global Tab Leads and Tab Seal Film Market Set to Triple by 2034 Amid Surging EV and Energy Storage Demand

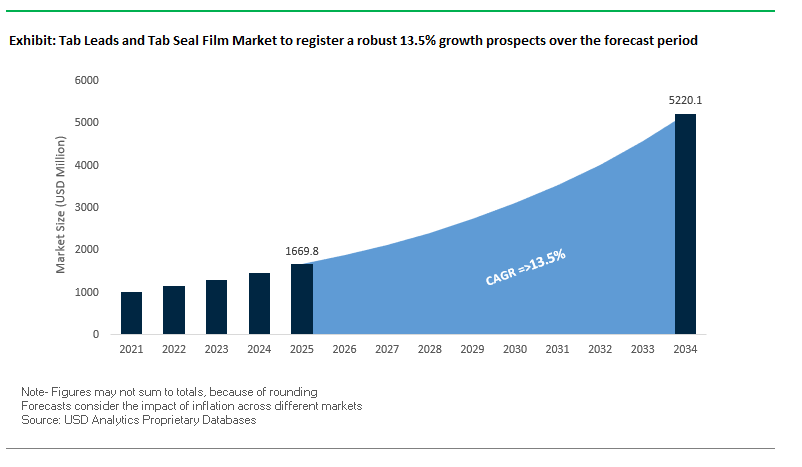

The global tab leads and tab seal film market is projected to grow from $1,669.8 million in 2025 to $5,219.5 million by 2034, at a robust CAGR of 13.5%. These components are critical for the safety, longevity, and performance of lithium-ion pouch cells, widely used in electric vehicles (EVs), consumer electronics, and energy storage systems.

Key Insights for battery manufacturers and investors:

- Electrification trends in automotive and renewable energy sectors are driving unprecedented demand for high-quality tab leads and seal films.

- Material innovation is at the forefront, with lightweight, high-conductivity alloys and multi-layer seal films enhancing battery efficiency.

- Enhanced safety and thermal management are critical, as robust seals prevent electrolyte leakage and thermal runaway under extreme conditions.

- Integrated design and manufacturing collaboration between film/tab suppliers and cell producers streamline production and improve battery reliability.

- The market offers opportunities for differentiation through durability, thermal resilience, and conductive performance.

The market is positioned at the nexus of battery performance, safety innovation, and electrification, providing lucrative opportunities for companies investing in advanced materials, lightweighting, and process integration.

Market Analysis: Strategic Developments and Material Innovations Are Driving Growth in Tab Leads and Seal Films

The tab leads and tab seal film market is rapidly evolving, propelled by technological innovation, sustainability initiatives, and strategic partnerships. In August 2025, research highlighted the increasing use of advanced additives to enhance mechanical and antimicrobial properties of sustainable films. Meanwhile, in April 2025, LINDAL Group introduced the FlipStraw dual spray actuator with foldable straw, emphasizing functionality improvement and waste reduction in technical applications.

Investment in circular economy and sustainable materials continues to influence market direction. Ball Corporation (February 2025) invested in Meadow, a Swedish startup, to develop aluminum refill solutions, reflecting a commitment to recycling and sustainability. Similarly, CJ Biomaterials (November 2024) achieved BPI certification for its PHACT™ PHA masterbatches, enabling compostable coatings.

Expansion of manufacturing capabilities underscores the demand for high-performance solutions. In June 2024, Nefab Group opened a new facility in Mexico to meet growing packaging and ESD requirements, while Conductive Containers (November 2023) acquired Crestline Plastics, enhancing its static control packaging offerings.

Trends and Opportunities in the Tab Leads and Tab Seal Film Market

Adoption of High-Barrier, Multi-Layer Coextruded Films

The tab leads and tab seal film market is being reshaped by the introduction of advanced coextruded structures that deliver superior barrier performance. Jindal Films’ Metallyte™ ultra-high-barrier films exemplify this trend, providing excellent resistance to moisture, oxygen, and light while reducing overall packaging weight by up to 30% compared to aluminum foil alternatives. This innovation not only supports sustainability targets but also ensures increased puncture resistance, making it a strong alternative for sensitive applications in pharmaceuticals, food preservation, and electronics.

The industry is also witnessing a shift from complex multi-material laminates to simplified, high-performance single structures. ExxonMobil has reported success in barrier coextrusion projects where one optimized film replaces multiple laminated layers, streamlining the manufacturing process, lowering costs, and enhancing recyclability. Moreover, technical advancements in coextrusion now allow for multi-layer structures with EVOH cores, which drastically improve oxygen barrier properties while ensuring durability against puncture and tearing. This makes them particularly valuable for modified atmosphere packaging and other high-value applications where packaging integrity directly impacts shelf life and product safety.

Integration of PCR Content into Non-Contact Layers

Sustainability pressures and regulatory mandates are pushing manufacturers to integrate post-consumer recycled (PCR) content into their products. In the case of tab seal films, PCR is primarily used in non-food contact layers, ensuring that critical performance and safety standards remain uncompromised. For instance, recycled HDPE and PP recompounds with anti-static properties are being used in ESD-safe packaging for electronics, demonstrating how PCR materials can deliver both sustainability and functionality.

Overcoming the technical and aesthetic challenges of PCR integration is also a core focus. Companies like ePac Flexibles have developed advanced sorting and processing methods to produce PCR-based films with barrier performance, strength, and appearance comparable to virgin materials. This enables brand owners to leverage circular materials without trade-offs, aligning with their carbon reduction targets and consumer-facing sustainability commitments.

Development of Compatible, Conductive Tab Leads for Smaller Electronics

The miniaturization of medical and electronic devices is creating a strong opportunity for conductive tab leads engineered for precision. Companies like Henkel are pioneering high-reliability conductive inks for medical electrodes, enabling flexible, fine-gauge solutions used in ECG electrodes and continuous glucose monitors (CGMs). By leveraging flexographic printing processes, these solutions can be scaled for mass production, addressing the rising global demand for wearable health monitoring devices.

Similarly, TE Connectivity is developing injection-moldable conductive plastics, which combine durability, flexibility, and EMI shielding in a lightweight design. These innovations support the production of wearable electronics, medical sensors, and connected health devices, where traditional metal components would be bulky or cost-intensive. With the healthcare and consumer electronics industries expanding rapidly, the development of fine-gauge, conductive tab leads represents a long-term growth segment for packaging-integrated electronics.

Engineering Films for Advanced Recycling Compatibility

A second major opportunity is the design of tab seal films compatible with chemical recycling technologies. Multi-layer structures, while critical for performance, often pose recycling challenges due to the incompatibility of their layers in mechanical systems. Companies like Dow are actively advancing pyrolysis and depolymerization technologies, which break down these complex plastics into virgin-quality feedstock. This allows even hard-to-recycle barrier films to be reintegrated into the packaging value chain.

The investment in this space is substantial. According to Plastics Europe, more than $8 billion has already been invested in chemical recycling facilities worldwide, underlining the industry’s commitment to scaling circular solutions. By engineering tab seal films with chemical recycling compatibility in mind, manufacturers can create packaging that retains high-barrier performance while also being future-proofed for circular economies. This not only creates value from plastic waste but also helps brands meet stringent Extended Producer Responsibility (EPR) and EU PPWR targets.

Competitive Landscape: Leading Global Players Are Advancing Tab Leads and Seal Film Technology Through Innovation and Sustainability

The tab leads and tab seal film market is dominated by companies leveraging materials science, manufacturing expertise, and sustainability initiatives to meet the growing demands of EVs, energy storage, and electronics.

Sumitomo Electric Industries, Ltd.: Innovating Materials and Technologies to Enhance Battery Safety and Performance

Sumitomo Electric provides high-conductivity tab leads and seal films for lithium-ion batteries. Its Vision 2025 plan focuses on advancing materials for automotive and energy storage applications, with significant investments in R&D. Sumitomo Electric’s vertically integrated model and global expertise ensure high-quality, compliant solutions that enhance battery performance and reliability.

Mitsubishi Materials Corporation: Driving Sustainable and High-Performance Materials for Advanced Battery Applications

Mitsubishi Materials produces foils and films with high conductivity and durability, essential for lithium-ion batteries. Its Sustainability Management strategy emphasizes reduced environmental impact and circular economy solutions. With global brand recognition and materials expertise, Mitsubishi delivers innovative, compliant, and high-performance components for a variety of industries.

Furukawa Electric Co., Ltd.: Combining Expertise in Electronics and Automotive to Advance Pouch Cell Technology

Furukawa Electric manufactures high-performance tab leads and seal films with a focus on conductivity, durability, and safety. The Furukawa G.R.E.E.N. 2025 plan highlights initiatives for environmental sustainability and advanced material development. Furukawa’s integrated operations and global footprint support the production of innovative solutions for energy storage and EV applications.

DOWA Holdings Co., Ltd.: Enhancing Battery Safety and Performance Through Advanced Non-Ferrous Materials

DOWA Holdings provides high-conductivity foils and films for lithium-ion batteries. Its Vision for 2030 outlines sustainability commitments and development of materials supporting the circular economy. DOWA’s materials expertise and vertically integrated model enable delivery of high-quality, durable, and compliant components to global customers.

Nitto Denko Corporation: Pioneering Advanced Seal Films and Adhesive Solutions for High-Performance Batteries

Nitto Denko specializes in high-quality films and sealants for lithium-ion batteries. The Mid-Term Management Plan 2025 focuses on sustainability, material innovation, and circular economy solutions. Nitto Denko’s brand strength and materials expertise provide reliable, durable, and high-performance tab leads and seal films for global battery manufacturers.

Tab Leads and Tab Seal Film Market Share Insights, 2025-2034

Electric Vehicles Dominate Market Share by Application in Tab Leads and Tab Seal Film Industry

Electric vehicles (EVs) account for 65% of the tab leads and tab seal film market, making automotive applications the overwhelming demand driver for this niche but high-value segment. Each EV battery pack contains hundreds of pouch cells, and the integrity of the tab lead and seal film is critical to prevent moisture ingress, oxygen exposure, and thermal failure. The rapid acceleration of EV adoption, supported by government incentives, net-zero targets, and OEM investments in gigafactories, has created unprecedented demand for tab seal films with superior durability, thermal resistance, and compatibility with advanced chemistries such as high-nickel cathodes and solid-state prototypes. Unlike consumer electronics, where cost efficiency and miniaturization dominate, the EV sector demands ultra-high performance to deliver cycle lives exceeding 1,000 charges and warranties extending up to 10 years. This segment’s dominance is expected to continue as EV penetration climbs globally, making automotive innovation the primary engine for material and design advancements in tab leads and seal films.

Lithium-Ion Pouch Cells Define Market Share by Battery Type in Tab Leads and Tab Seal Film Industry

Lithium-ion pouch cells account for an overwhelming 98% of the tab leads and tab seal film market, underscoring the fact that this industry is intrinsically tied to this specific battery format. Unlike cylindrical and prismatic cells, which use crimped metal lids, pouch cells require a flexible aluminum laminate casing sealed with a polymer-based film to ensure hermetic integrity at the point where the conductive tab exits the cell. This technical necessity means that the entire tab seal film market is a derivative of pouch cell adoption, which has become the preferred format in both EVs and certain consumer electronics due to its lightweight design, energy density advantages, and shape flexibility. The small “other” category primarily refers to experimental chemistries such as solid-state pouch cells, which would still require similar sealing technology. Thus, the dominance of pouch cells not only defines the demand for tab seal films but also dictates the pace of innovation in materials engineered for cycle life, mechanical robustness, and long-term reliability under demanding conditions.

China: Government Support and Battery Giants Driving Market Growth

The China tab leads and tab seal film market is rapidly expanding due to the country’s aggressive push for electric vehicle (EV) adoption under its subsidy and infrastructure programs. The reliance of pouch lithium-ion batteries on advanced sealing films and tab leads for structural integrity has made these components critical to China’s battery ecosystem. Major manufacturers like CATL are spearheading innovation by developing new cell designs that demand high-performance aluminum-plastic composite films (APCs) and next-generation tab seal technologies to enhance energy density and safety.

The 14th Five-Year Plan places significant emphasis on advanced material development for new energy technologies, prompting large-scale R&D investments in pouch packaging materials. In addition, the government’s support for remanufacturing and green technology adoption through tax incentives is accelerating domestic innovation. As a result, China has become a global hub for both battery production and material development, ensuring strong demand for tab leads and seal films across EV and stationary energy storage applications.

South Korea: Technological Leadership and Advanced Research in Pouch Batteries

The South Korea tab leads and tab seal film market benefits from the country’s leadership in battery innovation through companies like LG Energy Solution and Samsung SDI, which are global pioneers in pouch-type lithium-ion batteries. These firms rely on high-quality tab leads and seal films to achieve higher performance and safety standards in both consumer electronics and EVs. The government has committed significant funding to advanced industries including semiconductors, AI, and rechargeable batteries, directly supporting the development of materials critical to flexible and pouch batteries.

Academic research plays a vital role, with KAIST developing advanced sealing materials and flexible battery components that integrate innovative tab technologies. Domestic companies such as NEPES and SAMA are strengthening supply chains by providing critical conductive and sealing materials for high-performance applications. Additionally, South Korea’s investment in next-generation OLED and display technology—industries that rely heavily on flexible batteries—further boosts demand for advanced tab seal films, reinforcing the country’s position as a leader in battery materials R&D and commercialization.

Japan: Innovation in Conductive Materials and Government R&D Support

The Japan tab leads and tab seal film market is anchored by its strong foundation in battery innovation and advanced materials manufacturing. Leading companies such as Panasonic and Nitto Denko are continuously enhancing battery safety, conductivity, and durability through more robust tab seal films. A notable example is Toray’s 2021 joint venture with LG Chem in Hungary to increase separator film production, a complementary technology that underscores Japan’s collaborative approach to scaling lithium-ion battery supply chains.

The Japanese government, through METI subsidies and the Plastic Resource Circulation Strategy, is actively promoting sustainable and recyclable material development within battery packaging. At the same time, advancements in conductive materials for tab leads—with improved heat dissipation and electrical conductivity—are being developed to meet the high-performance needs of the automotive and industrial sectors. This strong blend of corporate innovation, government support, and sustainability mandates positions Japan as a frontrunner in safe and high-performance battery component development.

United States: Federal Funding and Growing Domestic Battery Supply Chains

The United States tab leads and tab seal film market is being shaped by substantial federal support through the Department of Energy (DOE) under the Bipartisan Infrastructure Law and Inflation Reduction Act, which are channeling billions into domestic battery supply chains. These initiatives are designed to reduce reliance on imports and build resilient pouch battery manufacturing capacity, directly driving demand for tab leads and seal films.

A notable trend in the U.S. is the focus on sustainable and recyclable packaging solutions, with companies like Berry Global and startups innovating in bio-based materials that could extend to the battery industry. The e-commerce boom also underscores the importance of lightweight and durable packaging systems, driving innovation in space-efficient designs. Additionally, the U.S. research ecosystem—funded by institutions like the NSF and DoD—is exploring advanced ESD protection and flexible electronic materials, further enhancing opportunities for tab seal film innovation in both defense and consumer electronics applications.

European Union: Semiconductor Expansion and Circular Economy Regulations

The European Union tab leads and tab seal film market is benefiting from the European Chips Act and Chips Joint Undertaking (Chips JU), which are mobilizing over €80 billion to strengthen semiconductor and advanced material supply chains. These programs are bridging the gap between research and commercialization, creating opportunities for new conductive films and tab lead materials in electronics and battery manufacturing.

At the same time, EU-wide regulations such as the Packaging and Packaging Waste Regulation (PPWR, 2025) and the Ecodesign for Sustainable Products Regulation (ESPR) are pushing companies toward recyclable, durable, and circular material use. Firms like Mondi are investing in flexible laminates and sustainable films that could be adapted for battery packaging, while the EU’s aggressive decarbonization targets are fostering demand for advanced EV battery technologies. Together, these measures place Europe at the forefront of sustainable and high-tech packaging innovations for the tab leads and seal films sector.

India: Domestic Battery Manufacturing Incentives and Regulatory Drivers

The India tab leads and tab seal film market is gaining momentum with the government’s National Programme on Advanced Chemistry Cell (ACC) Battery Storage, which incentivizes domestic and foreign companies to establish battery manufacturing facilities. This directly boosts demand for tab leads and seal films as India scales up EV and renewable energy storage solutions.

The regulatory environment is also a critical driver. The Plastic Waste Management (Amendment) Rules, 2024, effective April 1, 2025, emphasize Extended Producer Responsibility (EPR), making manufacturers accountable for recycling and disposal. Additionally, as of July 1, 2025, all plastic packaging in India must carry traceability features like barcodes or QR codes, compelling companies to upgrade packaging technologies. While MSMEs are exempt, large manufacturers are required to adopt advanced sustainable and traceable materials, including those used in battery components and flexible films. With rising e-commerce and retail activity, India is poised to become a fast-growing market for advanced tab sealing materials.

Tab Leads and Tab Seal Film Market Report Scope

Tab Leads and Tab Seal Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1669.8 Million

|

|

Market Size (2034)

|

$5219.5 Million

|

|

Market Growth Rate

|

13.5%

|

|

Segments

|

By Material (Aluminum, Nickel, Copper, Polyamide, Polypropylene, Other Polyolefins, Composites), By Application (Electric Vehicles, Consumer Electronics, Energy Storage Systems, Military & Aerospace, Industrial Equipment), By Battery Type (Lithium-Ion Pouch Cells, Other Battery Types)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sumitomo Electric Industries, Ltd., Nitto Denko Corporation, Zacros (Shenzhen) Co., Ltd., MISUZU Holding, NEPES Corporation, SAMA, Yujin Technology Co., Ltd., T&T Enertechno Co., Ltd., Avocet Steel, Daest Coating India Pvt Ltd., Clavis Corporation, Okura Industrial Co., Ltd., Soulbrain Co., Ltd., Toray Industries, Inc., DuPont de Nemours, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tab Leads and Tab Seal Film Market Segmentation

By Material

- Aluminum

- Nickel

- Copper

- Polyamide

- Polypropylene

- Other Polyolefins

- Composites

By Application

- Electric Vehicles

- Consumer Electronics

- Energy Storage Systems

- Military & Aerospace

- Industrial Equipment

By Battery Type

- Lithium-Ion Pouch Cells

- Other Battery Types

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Tab Leads and Tab Seal Film Market

- Sumitomo Electric Industries, Ltd.

- Nitto Denko Corporation

- Zacros (Shenzhen) Co., Ltd.

- MISUZU Holding

- NEPES Corporation

- SAMA

- Yujin Technology Co., Ltd.

- T&T Enertechno Co., Ltd.

- Avocet Steel

- Daest Coating India Pvt Ltd.

- Clavis Corporation

- Okura Industrial Co., Ltd.

- Soulbrain Co., Ltd.

- Toray Industries, Inc.

- DuPont de Nemours, Inc.

* List Not Exhaustive

Methodology

USDAnalytics utilizes a robust, multi-faceted research methodology to provide industry professionals with actionable insights into the global tab leads and tab seal film market. Our approach combines primary research—including interviews with battery manufacturers, material suppliers, and technology experts—with extensive secondary research from corporate reports, patent filings, regulatory documents, and trade publications. Quantitative modeling and market forecasting are applied to analyze historical trends, competitive landscapes, and regional growth dynamics, particularly in EV, consumer electronics, and energy storage sectors. USDAnalytics emphasizes technological innovation, materials science, and sustainability, tracking advancements in high-conductivity tab leads, multi-layer coextruded films, and recycling-compatible solutions. Country-specific regulations, government incentives, and market expansions in the U.S., EU, China, Japan, South Korea, and India are incorporated to assess regional adoption and growth opportunities. All findings are validated through triangulation and expert consultations, ensuring accurate, reliable, and strategic insights for investors, manufacturers, and stakeholders seeking to capitalize on electrification-driven growth, material innovation, and high-performance battery component demand.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.