Battery Packaging Market Overview: Enabling EV Growth and Circular Economy

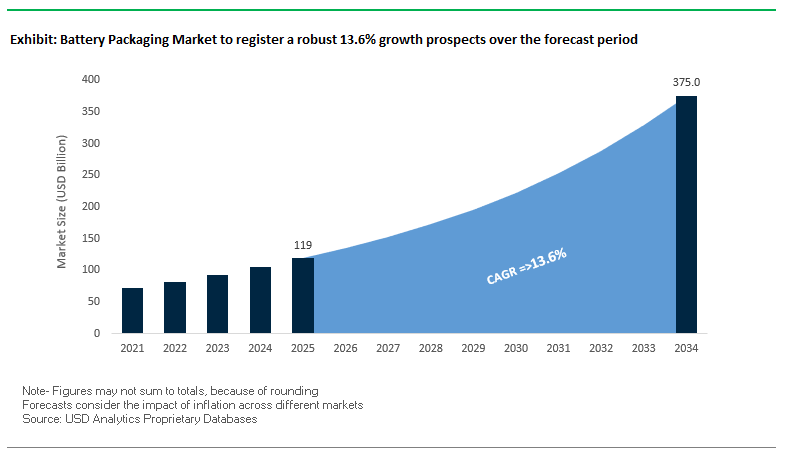

The global battery packaging market is projected to grow from USD 119 billion in 2025 to USD 374.9 billion by 2034, expanding at an impressive CAGR of 13.6%. This industry is no longer confined to the safe transport of cells it now underpins the entire electric vehicle (EV) revolution, renewable energy adoption, and the circular economy transition. For industry professionals, the key challenge is balancing safety, regulatory compliance, sustainability, and innovation while supporting unprecedented demand from EVs and stationary energy storage systems.

Key Insights Driving the Battery Packaging Market

- Regulatory Stringency Defines the Market: Lithium-ion batteries must pass UN 38.3 tests covering altitude, thermal stress, vibration, and impact, making compliant packaging a non-negotiable industry standard.

- EV Adoption is the Prime Growth Driver: With 2.3 million EVs sold in Q1 2023 alone (IEA), packaging demand for safe assembly, shipping, and integration of battery modules is expanding rapidly.

- Circular Economy in Focus: Over 95% of aluminum battery packs are recyclable, making design for disassembly and recycling a core priority for manufacturers.

- Thermal Safety at the Forefront: High-energy-density cells have accelerated demand for fire-retardant foams, thermal barriers, and vented enclosures to contain and mitigate thermal runaway events.

Market Analysis: Strategic Moves and Technological Innovations

The past year has been characterized by capacity expansions, research breakthroughs, and regulatory tailwinds that are reshaping the global battery packaging sector. In August 2025, a pivotal academic study highlighted the use of advanced composites in battery enclosures, emphasizing their lightweight structure and fire resistance critical for next-generation EVs. That same month, Orora completed the expansion of its Australian facility to scale up aluminum-based packaging, a material increasingly adopted for battery modules.

In July 2025, researchers published findings on a smart battery passport system, proposing digital traceability for chemistry, origin, and lifecycle data. This development would necessitate packaging capable of housing integrated chips and sensors. Regulatory frameworks are also accelerating innovation. In June 2025, the EU launched an initiative promoting renewable materials in industrial packaging, directly encouraging the shift toward bio-based enclosures. Meanwhile, in May 2025, Crown Holdings added a new aluminum production line in Brazil to address surging regional demand.

Sustainability continues to dominate strategic moves. In March 2025, Ball Corporation announced a joint venture to scale its Ball Aluminum Cup, reinforcing its role in sustainable packaging innovation. By February 2025, logistics companies unveiled IoT-enabled battery containers with real-time temperature and location tracking, meeting compliance and enhancing transport safety. Finally, in January 2025, the EU confirmed aluminum’s 95% recyclability, strengthening its role as a cornerstone material for battery casings. These developments underscore a clear direction: lighter, smarter, and safer packaging solutions will define the next decade of battery logistics and integration.

Emerging Trends and Opportunities Shaping the Battery Packaging Market

Strategic Shift Towards Flame-Retardant and Non-Combustible Materials for Cell Containment

The battery packaging market is undergoing a fundamental transformation as manufacturers prioritize safety through the development of advanced, flame-retardant, and non-combustible materials. Preventing thermal runaway a chain reaction caused by overheating or internal short circuits has become the most pressing challenge in EV and energy storage applications. Research in advanced materials highlights the promise of composite phase change materials (CPCMs), which combine polymers with additives like expanded graphite or ammonium polyphosphate to withstand temperatures of up to 1000°C while absorbing and dissipating heat. Corporate R&D efforts are intensifying in this direction. Saint-Gobain, for instance, is engineering proprietary silicone foams layered with mica, designed as compressible pads that act as both thermal barriers and fire containment systems inside battery packs. Meanwhile, battery leaders such as LG Energy Solution are investing in fire suppression systems compliant with UL9540A standards, alongside advanced thermal management strategies that embed these high-performance materials. By integrating such innovations, manufacturers are building safer, more reliable battery packs that meet the increasingly stringent safety standards demanded by regulators, automakers, and consumers worldwide.

Integration of Smart and Connected Packaging for Supply Chain Visibility and Lifecycle Management

Battery packaging is evolving from a passive protective shell to an active, data-enabled ecosystem that supports logistics, safety, and lifecycle optimization. Smart packaging solutions embed sensors, RFID tags, and data loggers into containers, transforming them into data-rich assets that monitor real-time parameters such as temperature, shock, and humidity. Companies like CakeBoxx Technologies are pioneering this approach by equipping lithium-ion battery shipping containers with advanced monitoring devices that validate warranties and ensure safe handling across global supply chains. Beyond transport, smart packaging facilitates digital lifecycle management, enabling manufacturers and users to track state-of-charge (SOC), storage conditions, and usage history from production through deployment. This data enables the creation of digital twins that extend into second-life applications, improving efficiency in reuse and recycling. Automated data capture also supports large-scale manufacturing and recycling by enabling error-free inventory management and robotic sorting. Together, these developments underscore how connected packaging is becoming indispensable for risk management, compliance, and value chain optimization in the battery industry.

Development of Standardized, Returnable, and Reusable Packaging Ecosystems for OEMs

The transition to electric mobility is driving the need for circular logistics systems, where packaging plays a pivotal role. Single-use shipping containers for EV batteries are costly and environmentally unsustainable, creating an urgent opportunity for standardized, returnable packaging ecosystems. Automakers such as Volvo Group are actively developing closed-loop logistics models that align with second-life applications for EV batteries, ensuring containers can be reused multiple times across their lifecycle. Durable, standardized containers and pallets lower the total cost of ownership (TCO) by eliminating the recurring expenses of disposable packaging while supporting ESG goals by reducing carbon emissions and waste. This opportunity is further reinforced by regulatory mandates, such as the EU’s Circular Economy Action Plan and India’s Battery Waste Management Rules (2022), which emphasize Extended Producer Responsibility (EPR). By adopting reusable packaging, OEMs not only ensure compliance but also build a logistics infrastructure that is both cost-efficient and environmentally responsible, positioning themselves at the forefront of sustainable battery value chains.

Innovation in Packaging Design to Facilitate Automated Disassembly and Recycling

As millions of EV batteries approach end-of-life, recycling efficiency has become a critical challenge and packaging design is central to enabling it. Current battery packs are difficult to dismantle, making recycling labor-intensive and costly. A major opportunity exists in developing design-for-disassembly packaging, where enclosures use fasteners or adhesives that can be easily removed by robotic systems. Such designs improve worker safety, accelerate throughput, and enhance the economic viability of recycling facilities. Another innovation area is the use of mono-material packaging structures, which eliminate the need for costly sorting and ensure that enclosures can be reprocessed directly into new products. To support automation, packaging can also integrate machine-readable labels, QR codes, or embedded identifiers that allow robotic systems to instantly recognize a battery’s chemical composition and optimal recycling pathway. This combination of automated disassembly, mono-materials, and intelligent labeling is set to revolutionize end-of-life management, turning packaging from a disposal challenge into an enabler of circular economy solutions for the battery sector.

Competitive Landscape: Global Leaders Driving Safety and Sustainability

The battery packaging market is highly specialized, with a mix of packaging innovators, material science leaders, and logistics providers shaping its trajectory. Their strategies revolve around compliance, safety, sustainability, and integration capabilities.

Nefab AB advances modular battery packaging with thermal safety

Nefab AB is a global specialist in custom-engineered packaging for EVs and energy storage systems. In 2025, it launched a modular packaging system with integrated thermal barriers, enhancing compliance and safety across supply chains. Its expertise in UN 38.3 compliance and its ability to reduce total supply chain costs while minimizing environmental impact give it a strong market edge.

Smurfit Kappa Group develops fiber-based battery packaging alternatives

Smurfit Kappa, best known for paper-based packaging, has expanded into corrugated and fiber-based inserts for battery modules. Its engineers are developing recyclable cushioning with thermal resistance, providing a sustainable alternative to plastics and foams. Its integrated supply model ensures security of materials, while its commitment to reducing environmental impact aligns with the EV industry’s sustainability goals.

Zarges GmbH strengthens reusable aluminum battery containers

Zarges GmbH specializes in reusable aluminum containers for hazardous goods. Its K 470 series is an industry standard for transporting lithium-ion batteries, particularly damaged or defective ones. The lightweight durability of its containers makes them ideal for closed-loop logistics, while its focus on compliance with UN and IATA regulations ensures global shipment safety.

Sealed Air Corporation innovates with sustainable protective foams

Sealed Air brings expertise in specialty foams, cushions, and void fill solutions tailored for lithium-ion transport. It is developing next-generation recyclable foams with superior cushioning and vibration protection. With deep material science expertise and integration with automated lines, Sealed Air is positioned as a critical supplier for shock-sensitive, high-value battery shipments.

FedEx Corporation integrates IoT-enabled logistics for battery safety

FedEx plays a vital role as a global logistics and compliance enabler. In 2025, it launched IoT-enabled packaging solutions with real-time tracking, GPS location data, and thermal monitoring to enhance lithium-ion shipping safety. With its global network and compliance expertise, FedEx collaborates with OEMs and packaging providers to design tailored transport solutions spanning from consumer electronics to EV battery packs.

Battery Packaging Market Share Insights

Market Share by Packaging Type in the Battery Packaging Industry

Corrugated packaging leads the battery packaging market with a 40% share in 2025, reflecting its position as the industry standard for balancing protection, cost, and sustainability. Integrated with molded pulp, foam, or ESD-safe inserts, corrugated formats dominate consumer electronics shipments, from AA and AAA cells to laptop and smartphone batteries, where lightweight, recyclable, and customizable packaging is essential for both performance and global compliance. Hard case packaging accounts for 25% of the market, serving as the go-to solution for high-value and large-format applications. Engineered plastics and metal enclosures provide unmatched crush resistance, impact durability, and environmental sealing, making them indispensable for automotive EV battery modules, large industrial packs, and sensitive medical devices. Thermal packaging represents a smaller but strategically critical niche, designed to mitigate the risks of overheating and thermal runaway. From insulated foams to advanced temperature-controlled shipping containers, this category is expanding rapidly in line with rising demand for high-capacity lithium-ion cells in EVs and grid-scale ESS. Flexible packaging, including ESD pouches and barrier films, plays a vital role in safeguarding smaller battery cells against static and moisture damage during inter-facility transport, while wooden crates are reserved for the heaviest-duty applications, including the shipment of entire EV battery packs and large industrial systems where unmatched structural integrity is required. Collectively, these segments highlight how packaging formats align directly with the growing complexity, size, and risk profile of battery technologies.

Market Share by End-Use Industry in the Battery Packaging Industry

The automotive sector, primarily electric vehicles (EVs), represents the largest share of the battery packaging market at 35% in 2025, underscoring its position as the high-growth, high-stakes driver of innovation. Packaging for EVs must withstand extreme weight and stress, comply with UN 38.3 and IATA/DOT transport regulations, and incorporate advanced thermal and structural protections to ensure safety throughout global supply chains. Consumer electronics follows with a 25% share, representing the highest-volume segment. Billions of small-format batteries for smartphones, laptops, wearables, and power tools require standardized yet reliable packaging, reinforcing the dominance of corrugated and flexible solutions designed for lightweight and high-throughput logistics. Energy storage systems (ESS) form a rapidly expanding application, driven by the scaling of residential, commercial, and grid-level renewable energy infrastructure. Packaging here must accommodate bulky modules and provide robust protection through wooden crates, hard cases, and advanced thermal insulation during transit and installation. Industrial applications, including motive power systems for forklifts, telecom backup batteries, and off-grid power units, add to the diversity of demand, requiring high-strength, compliant solutions similar to those used in automotive and ESS. Meanwhile, medical device batteries form a smaller but critically important niche, where packaging performance must be flawless due to the life-saving nature of applications, reinforcing reliance on high-value hard cases and precision thermal solutions. Together, these segments illustrate how the battery packaging industry is evolving in tandem with the electrification of mobility, the expansion of renewable energy systems, and the continuing ubiquity of portable consumer devices.

China: Government-Backed R&D and Standardization Propel the World’s Largest Battery Packaging Market

China dominates the global battery packaging market as both the largest producer and consumer of batteries, fueled by its leadership in electric vehicles (EVs) and consumer electronics. The demand for advanced packaging solutions is surging as manufacturers focus on safety, durability, and efficiency. With government-backed initiatives, China is aggressively investing in research and development for next-generation battery packaging. These efforts target improvements in thermal management, fire resistance, and energy efficiency, ensuring that battery packs remain reliable for EVs, grid storage, and portable devices.

The country is also prioritizing circularity in battery packaging design. New regulations are pushing manufacturers toward recyclable and easily disassemblable formats to manage the rising volume of end-of-life EV batteries. Advancements in thermal management systems, such as liquid cooling plates and phase change materials, are being integrated directly into packaging for enhanced performance. At the same time, the industry is moving toward standardized battery modules, which reduce costs and speed up production, further cementing China’s position as the global hub for battery packaging innovation.

United States: Safety Standards and Fire-Resistant Packaging Drive Market Innovation

The United States battery packaging market is defined by strict federal regulations and innovation in advanced safety technologies. Regulations such as Reese’s Law mandate secure packaging for button and coin cell batteries, highlighting the country’s emphasis on child safety and compliance. At the industrial level, the U.S. is at the forefront of developing fire-resistant and flame-retardant materials designed to mitigate thermal runaway risks in lithium-ion batteries. These innovations are essential for EVs, consumer electronics, and large-scale energy storage systems.

The rapid expansion of renewable energy projects, especially solar and wind, is accelerating demand for durable packaging solutions in energy storage applications. Companies are forming strategic partnerships and scaling production capacity to meet these needs, with players like UFP Technologies investing heavily in protective foam-based enclosures. Furthermore, automotive battery packaging is evolving to include crash-resistant materials and advanced structural designs that can withstand vehicle collisions. This emphasis on performance and safety ensures that the U.S. remains a critical market for high-value battery packaging solutions.

Germany: Automotive Leadership and EU Battery Regulation Shape Packaging Innovation

Germany stands as a European powerhouse in the battery packaging market, driven by its globally competitive automotive industry and alignment with the EU Battery Regulation. As German automakers transition toward electric mobility, demand for lightweight, high-strength enclosures that integrate seamlessly into vehicle chassis is surging. The EU’s recycling and circular economy mandates further push the industry to adopt sustainable packaging designs that facilitate disassembly and reuse, reinforcing the market’s eco-conscious orientation.

The German market is also characterized by heavy investments in infrastructure and advanced manufacturing. Companies such as MAN are building large-scale battery production facilities equipped with state-of-the-art packaging systems. Digitalization and automation are reshaping production workflows, with robotics and AI ensuring precision in assembly and quality control. This combination of regulatory alignment, technological expertise, and automotive leadership cements Germany’s role as a leading hub for battery packaging innovation in Europe.

Japan: High-Density Batteries and Wearable Technology Reshape Packaging Needs

Japan’s role in the battery packaging market is rooted in its technological leadership in high-density battery development. The demand for packaging solutions that can safely contain and manage these powerful cells is growing rapidly. Advanced material innovations such as electrolytes designed to perform under extreme conditions are influencing the evolution of protective enclosures that ensure stability, longevity, and safety.

The Japanese market is also distinguished by its strict focus on quality control, with manufacturers investing in precision engineering and rigorous testing to maintain world-class reliability. In addition to EV and consumer electronics applications, Japan is pioneering packaging for flexible and wearable batteries. These emerging technologies require entirely new approaches to design, as packaging must be lightweight, flexible, and safe without compromising energy performance. This positions Japan as a trailblazer in both traditional and next-generation battery packaging applications.

South Korea: Global EV Supply Chains and Energy Storage Expansion Fuel Growth

South Korea plays a vital role in the global EV battery supply chain, with its packaging industry deeply integrated into partnerships with leading automakers worldwide. Known for rapid innovation, South Korean manufacturers are developing cutting-edge packaging that enhances thermal performance, structural strength, and safety in advanced lithium-ion batteries. These solutions are tailored to meet the demands of both EV and consumer electronics markets.

The country is also expanding aggressively into the energy storage system (ESS) sector. Large-scale stationary batteries require highly durable packaging solutions capable of handling thermal stress and extended lifespans. This diversification strengthens South Korea’s battery ecosystem and increases its influence in the global market. By combining technological leadership with strategic expansion, South Korea continues to solidify its position as a top-tier player in battery packaging.

India: Government Policies and Localized Supply Chains Boost Battery Packaging Ecosystem

India is emerging as a high-growth market for battery packaging, primarily driven by government policies that promote electric vehicle adoption and domestic manufacturing. The National Mission on Transformative Mobility and Battery Storage and the Make in India initiative are catalyzing investments from both domestic and international companies. For example, TDK Corporation has established a new lithium-ion battery plant in Haryana, supporting the development of a robust local ecosystem for battery production and packaging.

The country is also emphasizing localized supply chains to reduce reliance on imports, creating opportunities for domestic manufacturers of protective enclosures and advanced packaging materials. At the same time, the Indian market is adopting smart packaging solutions, integrating sensors that monitor temperature, humidity, and impact in real time. These intelligent systems are particularly relevant for EV and industrial battery applications, where safety and performance monitoring are critical. With strong government support and rising consumer demand, India is rapidly positioning itself as a significant market for battery packaging innovation.

Battery Packaging Market Report Scope

Battery Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$119 Billion

|

|

Market Size (2034)

|

$374.9 Billion

|

|

Market Growth Rate

|

13.6%

|

|

Segments

|

By Packaging Type (Hard Case Packaging, Flexible Packaging, Thermal Packaging, Corrugated Packaging, Wooden Crates), By Level of Packaging (Cell Packaging, Module Packaging, Pack Packaging, Transport Packaging), By End-Use Industry (Automotive, Industrial, Consumer Electronics, Medical Devices, Energy Storage Systems, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nefab Group, DS Smith, Zarges GmbH, Rogers Corporation, UFP Technologies, Inc., SVOLT Energy Technology Co., Ltd., Mondi plc, SABIC, Amcor plc, Crown Holdings, Inc., Sonoco Products Company, Gentex Corporation, Sealed Air Corporation, The Dow Chemical Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Battery Packaging Market Segmentation

By Packaging Type

- Hard Case Packaging

- Flexible Packaging

- Thermal Packaging

- Corrugated Packaging

- Wooden Crates

By Level of Packaging

- Cell Packaging

- Module Packaging

- Pack Packaging

- Transport Packaging

By End-Use Industry

- Automotive

- Industrial

- Consumer Electronics

- Medical Devices

- Energy Storage Systems

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Battery Packaging Market

- Nefab Group

- DS Smith

- Zarges GmbH

- Rogers Corporation

- UFP Technologies, Inc.

- SVOLT Energy Technology Co., Ltd.

- Mondi plc

- SABIC

- Amcor plc

- Crown Holdings, Inc.

- Sonoco Products Company

- Gentex Corporation

- Sealed Air Corporation

- The Dow Chemical Company

* List Not Exhaustive

Research Coverage

This comprehensive report by USDAnalytics investigates the global battery packaging market, providing a detailed examination of technological breakthroughs, regulatory developments, and strategic industry initiatives that are shaping the sector. It highlights innovations in flame-retardant materials, smart connected packaging, and circular economy-focused designs, making it an essential resource for professionals seeking actionable insights into the rapidly expanding EV and energy storage ecosystem. The analysis reviews market dynamics across key regions, covering historical data from 2021 to 2024 and forecasts extending through 2034, and it delves into the strategies and competitive positioning of 15+ leading companies. The report further emphasizes opportunities in design-for-disassembly, reusable logistics systems, and digital lifecycle management, underlining how packaging is evolving from a protective necessity into a value-adding, smart, and sustainable component of the battery supply chain. For industry experts, this report highlights trends, innovations, and operational best practices that can inform decision-making across product development, supply chain management, and regulatory compliance.

Scope Highlights

- Segmentation: By Packaging Type (Hard Case, Flexible, Thermal, Corrugated, Wooden Crates), Level of Packaging (Cell, Module, Pack, Transport), End-Use Industry (Automotive, Industrial, Consumer Electronics, Medical Devices, Energy Storage Systems, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024; Forecast data from 2025 to 2034

- Company Coverage: Profiles and strategic analysis of 15+ major players, including Nefab Group, DS Smith, Zarges GmbH, Rogers Corporation, UFP Technologies, SVOLT Energy Technology, Mondi plc, SABIC, Amcor plc, Crown Holdings, Sonoco Products, Gentex Corporation, Sealed Air Corporation, The Dow Chemical Company

Methodology

The methodology underpinning this USDAnalytics report combines quantitative and qualitative research approaches to deliver a rigorous and comprehensive market assessment. Primary research involved direct engagement with industry executives, packaging engineers, and regulatory specialists to validate data on emerging technologies, compliance requirements, and adoption trends across key sectors such as EVs, consumer electronics, and energy storage systems. Secondary research encompassed peer-reviewed publications, industry whitepapers, company reports, and regulatory filings to triangulate historical market data from 2021 to 2024. Advanced statistical techniques and market modeling tools were used to forecast market growth from 2025 to 2034, considering factors such as regional demand, material innovations, and shifts in supply chain logistics. Competitive analysis was performed using SWOT and benchmarking frameworks to evaluate 15+ leading players, identifying key differentiators in sustainability, smart packaging adoption, and thermal safety solutions. This multi-layered approach ensures robust insights for decision-makers seeking to optimize product development, regulatory compliance, and operational efficiency within the battery packaging market.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.