Terpene Resins Market 2025–2034: $2.8 Billion to $6 Billion at 8.8% CAGR Driven by Bio-Based Adhesives, Tire Compounding, and Certified Supply Chains

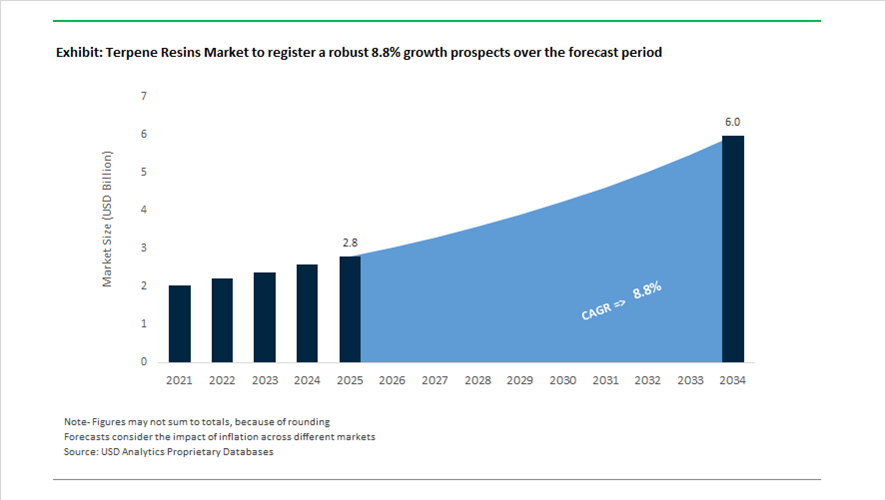

The global terpene resins market is valued at $2.8 billion in 2025 and is projected to reach $6 billion by 2034, expanding at a robust CAGR of 8.8%. Growth is being driven by the accelerating substitution of petroleum-derived tackifiers with pine-based polyterpene and terpene-phenolic resins in hot-melt adhesives, pressure-sensitive adhesives (PSA), tire compounding, inks, and specialty coatings. The market is structurally advantaged by its renewable feedstock base—primarily crude sulfate turpentine (CST), a byproduct of kraft pulping—which aligns terpene chemistry with circular bioeconomy models. As brand owners in packaging, automotive, and construction demand traceable and low-carbon materials, terpene resin producers are increasingly differentiating via ISCC PLUS certification, carbon accounting transparency, and integrated forestry supply agreements.

Sustainability leadership and supply chain control are defining competitive positioning. In January 2026, Kraton Corporation announced that its Panama City, Florida site achieved ISCC PLUS certification, enabling the company to offer mass-balanced bio-attributed grades of its SYLVARES™ and SYLVATRAXX™ terpene resins to adhesive and tire manufacturers. In November 2025, Kraton unveiled new 2032 climate targets focused on reducing Scope 1 and 2 emissions intensity across its pine chemical portfolio. The company further reinforced its ESG standing in September 2025 by securing EcoVadis Platinum status for the fifth consecutive year, placing it within the top 1% of assessed chemical companies globally. In August 2025, Kraton executed a strategic continuity agreement with International Paper, ensuring secure access to CST and related pine-derived intermediates—critical for maintaining terpene resin feedstock stability amid pulp industry cyclicality.

Asian producers are simultaneously strengthening profitability and technical positioning. Yasuhara Chemical Co., Ltd. reported operating income of ¥1.82 billion for fiscal year ending March 2025, nearly tripling year-over-year performance due to strong demand in hot-melt adhesives and electronics-grade applications. Throughout 2025, dsm-firmenich emphasized expansion of its DRT pine chemicals platform, promoting bio-sourced tackifying resins for high-performance tire and specialty adhesive systems. Pricing dynamics tightened in early 2025 when Kraton implemented up to 25% price increases on terpene derivatives, citing raw material volatility and logistics costs. Operational optimization also continued, with Kraton streamlining production at its Berre, France site to enhance global manufacturing efficiency. In marine coatings, a notable downstream innovation is the 2026 launch of CMP NOVA 2000 (Bio), developed by Chugoku Marine Paints and Mitsui Chemicals, utilizing bio-based epoxy systems derived partly from terpene intermediates for liquefied ammonia tankers.

Structural Decarbonization and Specialty Value Migration in the Terpene Resins Market

Low-VOC Bio-Terpene Tackifiers Displacing Fossil C5/C9 Hydrocarbon Resins in PSAs

The terpene resins market is undergoing a structurally enforced substitution cycle as pressure-sensitive adhesive manufacturers phase out petroleum-derived C5 and C9 hydrocarbon tackifiers. This shift is no longer driven by brand preference alone but by compliance economics tied to LEED v4.1, EU Green Deal chemistry thresholds, and indoor air quality benchmarks in construction, packaging, and logistics applications. Terpene-phenolic and polyterpene resins are emerging as direct functional replacements because they deliver equivalent peel strength, loop tack, and shear resistance while materially lowering volatile organic compound emissions.

A defining inflection point occurred in mid-2025 when Kraton Corporation, Henkel, and Dow formalized decarbonization-aligned supply agreements focused on ISCC PLUS-certified terpene-based tackifiers. These formulations achieved cradle-to-gate carbon footprint reductions of approximately 25% in premium hot-melt adhesives without compromising high-tack performance in carton sealing, labels, and industrial tapes. Importantly, these collaborations moved terpene resins out of niche “green” SKUs and into high-volume PSA platforms, anchoring renewable tackifiers within core procurement frameworks rather than discretionary sustainability lines.

The rapid adoption of ISCC PLUS mass balance certification across terpene resin manufacturing sites in 2024–2025 has further accelerated demand. Mass balance enables downstream CPG and logistics brands to substantiate renewable content claims at the product level, supporting USDA Certified Biobased labeling across a growing portfolio of shipping tapes, hygiene products, and flexible packaging. This certification-driven pull is structurally advantaging terpene resins over fossil hydrocarbon alternatives that face rising Scope 3 emissions penalties and VOC compliance costs.

Vertical Integration and Purification Driving High-Compliance Terpene Resins in Premium CPG

Beyond adhesives, the terpene resins market is experiencing vertical value migration toward high-purity terpene isolates tailored for flavors, fragrances, cosmetics, and medical applications. The Flavors, Fragrances, and Cosmetics sector is increasingly rejecting commodity-grade resins in favor of purified terpene streams that meet ISO 16128 natural origin criteria and deliver consistent sensory performance. This has transformed Crude Sulfate Turpentine from a byproduct into a strategic feedstock for premium isolates such as alpha-pinene, longifolene, and d-limonene.

By late 2025, the global CST market reached an estimated value of $1.21 billion, underpinned by aggressive fractionation investments that convert pulp mill byproducts into fragrance- and detergent-grade terpene inputs. This upcycling model directly aligns with circular economy mandates, allowing manufacturers to monetize forestry residues while meeting “naturally derived” labeling requirements demanded by global CPG brands.

A parallel compliance-driven trend is unfolding in medical and pharmaceutical adhesives. Yasuhara Chemical has set a new benchmark with its YS Resin PX1150N, a terpene resin qualified under FDA Drug Master File standards. This level of purity enables hypoallergenic transdermal patches and medical tapes, signaling a decisive shift in terpene resins from industrial tackifiers to regulated, high-margin specialty excipients. For producers, this trend materially raises switching costs and embeds terpene resins deeper into regulated supply chains with long product lifecycles.

Bio-Compatible Terpene Compatibilizers for Compostable and Biopolymer Packaging

One of the most structurally attractive growth avenues lies in the use of terpene resins as compatibilizers and plasticizers in compostable polymer systems. As bioplastics such as PLA, PHA, and PBS scale across food service, agriculture, and medical packaging, processors face inherent brittleness and slow melt processing that limit throughput. Terpene-derived modifiers address these constraints without compromising compostability certifications.

Empirical studies published in 2025 on PBS blends demonstrated that incorporating up to 30 wt% bio-based terpene derivatives, including limonene oxide, yields films with tensile moduli around 330 MPa while preserving full biodegradability. These performance gains are unlocking applications in agricultural mulching films and bioresorbable medical scaffolds where mechanical integrity and controlled degradation must coexist.

Commercial validation is already underway. In September 2024, Power Adhesives launched tecbond 214B, the world’s first fully certified biodegradable hot-melt adhesive. Formulated with 44% bio-based content and terpene chemistry at its core, the product meets ASTM D6400 and EN13432 standards, proving that terpene resins can replace fossil tackifiers in zero-microplastic, compost-safe adhesive systems.

Terpene Phenolic Resins for EV Sealing, Damping, and Thermal Cycling Resistance

Electrification is creating a specialized demand profile for terpene phenolic resins in automotive elastomer systems. Electric vehicles impose higher torque loads, broader thermal cycling, and stricter vibration control requirements than internal combustion platforms, particularly in battery seals, gaskets, and cooling hoses. Terpene phenolic resins are increasingly specified to enhance rubber-to-metal adhesion and green strength in hydrogenated nitrile and EPDM compounds.

Late-2025 technical evaluations indicate that terpene phenol-based reinforcement resins are now instrumental in tuning glass transition temperatures in EV tire compounds and sealing systems. By elevating Tg and improving interfacial bonding, these resins support the durability requirements of heavy battery packs and high-frequency vibration environments.

In automotive sealing applications, product families such as the YS Polystar series are being engineered with controlled phenol modification levels to balance heat resistance, damping efficiency, and long-term elasticity. This positions terpene resins not merely as sustainable substitutes but as performance enablers in next-generation EV platforms, where failure tolerance is low and material qualification cycles are long.

Terpene Resins Market Share and Segmentation Insights

Polyterpene Resins Lead Terpene Resins Market with Bio-Based Tackifier Performance

Polyterpene resins accounted for 48.60% of the terpene resins market in 2025, driven by their strong performance as bio-based tackifiers derived from alpha-pinene and beta-pinene. These resins offer excellent adhesion, cohesion, thermal stability, and compatibility with natural and synthetic rubbers, making them ideal for high-performance adhesive systems. Their renewable origin supports increasing demand for sustainable and low-carbon adhesive formulations across packaging and hygiene sectors. The 2025 market trend focuses on bio-based adhesive adoption, where polyterpene resins replace petroleum-derived hydrocarbon resins, enabling renewable content claims while maintaining performance in pressure-sensitive and hot-melt adhesive applications.

Adhesives and Sealants Segment Drives Terpene Resin Consumption with Packaging and Hygiene Demand

Adhesives and sealants accounted for 42.80% of terpene resins market demand in 2025, reflecting their essential role in pressure-sensitive adhesives, hot-melt adhesives, and construction bonding systems. Terpene resins provide the tack and bonding strength required for labels, tapes, packaging adhesives, and hygiene products. Their compatibility with food-contact applications further supports adoption. The 2025 industry trend highlights hygiene adhesive market expansion, where growing demand for baby diapers, feminine hygiene products, and adult incontinence solutions in emerging markets is driving increased consumption of high-purity terpene resin tackifiers designed for safety-critical applications.

Terpene Resins Market Competitive Landscape

The terpene resins market in 2026 is shaped by feedstock security strategies, ISCC PLUS-certified mass balance systems, and rising demand for bio-based tackifiers. Growth is driven by EV tire additives, medical-grade adhesives, and sustainable hydrocarbon resin alternatives with high thermal stability and biocompatibility.

Yasuhara Chemical Leads Medical-Grade Terpene Resin Innovation with DMF-Registered High-Purity Grades

Yasuhara Chemical Co., Ltd. remains the technological benchmark in terpene resins, driven by advanced molecular weight control and hydrogenation expertise. Its YS Resin PX and YS Polystar series, particularly PX1150N, are FDA DMF-registered for medical-grade adhesive applications. A long-term terpene feedstock agreement through 2027 ensures stable crude sulfate turpentine supply. CLEARON hydrogenated resins are optimized for UV-cured systems, offering low inhibition and high optical clarity for electronics and display films. The company is expanding into food packaging, enhancing oxygen and moisture barrier properties in polypropylene films. Strong positioning in high-purity, bio-based resin applications supports premium segment leadership.

Kraton Accelerates ISCC PLUS Certified Bio-Based Resin Portfolio for EV Tire and Adhesive Markets

Kraton Corporation is strengthening its leadership in bio-based terpene resins through ISCC PLUS certification across its pine chemical operations. Its SYLVARES™ and SYLVATRAXX™ product lines now offer traceable, mass balance-certified sustainable resin solutions. Strategic leadership transition in 2026 is aligned with circular bioeconomy expansion and polymer optimization. The company is investing heavily in Scope 3 emission reductions across certified facilities. SYLVATRAXX™ resins are gaining traction as EV tire performance additives, improving wet grip and reducing rolling resistance. Kraton’s focus on sustainable tackifiers positions it strongly in advanced adhesive and elastomer markets.

DRT Expands Global Terpene Resin Footprint Through Pinova Acquisition and Firmenich Integration

DRT (Dérivés Résiniques et Terpéniques), part of DSM-Firmenich, is leveraging plant-based chemistry leadership to expand terpene resin applications globally. The $150 million acquisition of Pinova strengthened North American manufacturing capabilities, particularly at the Brunswick site. DRT’s Dertal® resin portfolio supports long-term partnerships across adhesives, fragrance, and healthcare industries. With revenues exceeding €440 million, the company maintains a strong global presence across Europe, North America, and Asia. Integration with Firmenich enables cross-functional innovation combining terpene chemistry with aroma and food-grade solutions. Focus remains on sustainable elastomers and specialty bio-based intermediates.

Ingevity Strengthens CST-Based Terpene Resin Supply with Vertical Integration and Industrial Performance Applications

Ingevity Corporation is capitalizing on its vertical integration in crude tall oil and CST refining to ensure terpene feedstock security. Its pine-based EnvaWet and EnvaDry product lines are expanding into oilfield chemicals and industrial additives. The company’s terpene-modified resins are widely used in pavement markings, delivering enhanced durability and visibility. Strong alignment with green chemistry mandates supports adoption in automotive and construction sectors. Vertical integration from black liquor soap to refined derivatives provides cost advantages and supply stability. Ingevity continues to scale sustainable alternatives to petroleum-based resins across industrial applications.

Arakawa Chemical Advances Hydrogenated Resin Technologies with Life Science and Adhesive Market Focus

Arakawa Chemical Industries, Ltd. is leveraging its "V-ACTION for sustainability" roadmap to expand its terpene and rosin-based resin portfolio. The company is prioritizing hydrogenation technologies and water-based polymers for high-performance adhesive systems. Strategic consolidation of its Vietnam facility strengthens its Southeast Asian production hub. Arakawa is increasingly targeting life science and pharmaceutical applications, transitioning terpene derivatives into high-value functional materials. With over 1,600 employees and stable financial performance, the company maintains operational resilience. Its integration of digital and material innovation supports next-generation sustainable resin development.

Mangalam Organics Scales Cost-Efficient Terpene Resin Production for High-Volume Asia-Pacific Markets

Mangalam Organics Limited is a key Asian manufacturer, leveraging integrated turpentine processing to produce camphor and terpene resins at scale. The company supplies high-volume industrial grades to adhesives, sealants, inks, and coatings sectors across Asia-Pacific. Its cost-efficient manufacturing and scale advantage position it competitively in the solid terpene resin segment. Growing demand from construction and packaging industries in India supports volume expansion. Mangalam is exploring downstream diversification into consumer-facing terpene products. Strong domestic manufacturing integration ensures resilience against feedstock price volatility.

United States Terpene Resins Market Anchored in Feedstock Volatility Management and Supply Chain Rebalancing

The United States terpene resins market in 2025 has been defined by feedstock price realignment and infrastructure-driven capacity redistribution. In February 2025, Kraton Corporation announced a general price increase of up to 25% on turpentine-refined products and terpene derivatives, effective April 2025. This adjustment directly reflected structural changes in pine wood pulping economics, where crude tall oil and turpentine availability has become increasingly sensitive to forestry operations, pulp mill rationalization, and competing biofuel demand. Pricing actions at this scale indicate a market that is prioritizing margin preservation over volume-led growth, particularly in high-performance tackifier and adhesive applications.

Supply-side consolidation further reshaped the U.S. market. The permanent closure of the Pinova terpene resin facility in Brunswick, Georgia, in late 2024 triggered a strategic reallocation of capital toward Texas and Mississippi, where producers expanded hydrogenation and polymerization assets to stabilize domestic supply. These investments coincided with growing downstream pull from sustainable construction. By mid-2025, terpene resins were increasingly specified as bio-based binders in roofing membranes and paving formulations, enabling developers to lower Scope 3 emissions. Feedstock continuity has become a strategic priority. In August 2025, Kraton entered a long-term continuity agreement with International Paper to secure stable supplies of crude tall oil and turpentine. This was reinforced by new 2032 climate and resource-efficiency targets announced in November 2025, committing major U.S. producers to a 30% reduction in water use and waste intensity across terpene resin synthesis operations.

India Terpene Resins Market Driven by Capacity Scaling and Import Substitution Economics

India’s terpene resins market is undergoing a phase of accelerated capacity expansion supported by strong domestic adhesive demand and policy-led localization. In 2025, Mangalam Organics Limited completed major expansion projects, scaling Bhimseni and Isoborneol flakes production to 2,500 metric tons per annum. These intermediates are critical for terpene-derived aroma chemicals and terpene phenolic resins, which are increasingly consumed by India’s fast-growing packaging, woodworking, and footwear adhesive sectors.

Financial performance in late 2025 underscored this momentum. Mangalam Organics reported 29.1% year-over-year revenue growth in its Q2 FY2025–26 disclosures, reflecting robust offtake for terpene phenolic resins. Policy alignment has amplified this trend. Under the Make in India initiative, terpene chemistry has been prioritized as a strategic bio-resin platform to reduce dependence on imported petroleum-based tackifiers, particularly for tire, rubber, and construction adhesives. Indian manufacturers have also improved profitability through input optimization. By late 2025, EBITDA margins expanded by approximately 151 basis points as producers diversified turpentine sourcing toward Brazil, Argentina, and Indonesia, mitigating feedstock concentration risks while maintaining cost competitiveness.

Japan Terpene Resins Market Defined by Hydrogenation Leadership and High-Specification Grades

Japan occupies a high-technology niche in the global terpene resins market, anchored in hydrogenated resin innovation and premium-grade development. Yasuhara Chemical Co., Ltd. remains the exclusive producer of hydrogenated terpene phenolic resins. In 2025, the company introduced new water-white, low-VOC grades tailored for transparent acrylic adhesives used in electronics assembly and film surface modification, where color stability and odor neutrality are critical performance parameters.

Supply chain resilience has been a parallel focus. Yasuhara continues to execute a multi-year raw material supply agreement with Leaf Resources, ensuring operational stability through at least 2026. Beyond hydrogenation, Japanese producers pushed performance boundaries in 2025 by launching terpene resin grades with softening points up to 160°C. These materials enhance heat resistance in hot-melt adhesives and engineering plastics used in automotive interiors and under-the-hood components. Strategic repositioning is also underway. Arakawa Chemical Industries, approaching its 150th anniversary in 2026, initiated its “V-ACTION for Sustainability” plan, reallocating R&D and capital toward rosin and terpene hydrogenation technologies for life science and digital electronics applications.

China Terpene Resins Market Shaped by Tariff Pressure and Bio-Based Materials Policy

China’s terpene resins market has entered a phase of structural adjustment driven by trade dynamics and regulatory support for green materials. By early 2026, tariff pressures on imported rosin and terpene derivatives prompted producers in Guangdong and Guangxi to deepen vertical integration. This strategy has helped partially insulate margins from import duty volatility while strengthening control over upstream pine chemical feedstocks.

Policy direction has reinforced demand-side growth. Under the Ministry of Industry and Information Technology’s 2025 roadmap for green chemicals, terpene resins have gained traction as bio-based alternatives to petroleum tackifiers in inks, paints, and coatings used in urban infrastructure. Municipal projects increasingly specify terpene-based binders to meet low-VOC and sustainability criteria, positioning domestic producers to benefit from regulatory-driven substitution across construction and maintenance coatings.

Comparative Snapshot: Terpene Resins Market by Country

Terpene Resins Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Driver

|

Market Implication

|

|

United States

|

Feedstock security and consolidation

|

CTO and turpentine volatility

|

Stable high-performance tackifier supply

|

|

India

|

Capacity expansion and localization

|

Adhesive demand and Make in India

|

Rapid substitution of imported resins

|

|

Japan

|

Hydrogenated and high-softening-point grades

|

Electronics and automotive specifications

|

Premium, high-margin resin segments

|

|

China

|

Vertical integration and green substitution

|

Tariff pressure and MIIT policy

|

Bio-based tackifier adoption in coatings

|

Terpene Resins Market Report Scope

Terpene Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$6 Billion

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Product Type (Polyterpene Resins, Terpene-Phenol Resins, Styrenated Terpene Resins, Liquid Terpene Resins), By Form (Solid, Liquid), By Application (Adhesives and Sealants, Inks and Coatings, Rubber and Tires, Food and Beverage, Cosmetics and Pharmaceuticals, Paper and Pulp), By End-Use Industry (Packaging, Automotive, Construction, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kraton Corporation, Yasuhara Chemical Co., Ltd., DRT, Arakawa Chemical Industries, Ltd., Mangalam Organics Limited, Ingevity Corporation, Sumitomo Bakelite Co., Ltd., Guangdong Nuochi Chemical Co., Ltd., Ganzhou Taipu Chemical Co., Ltd., Xiamen Well-Sunshine Co., Ltd., Star Pine Chemical Co., Ltd., Lawter B.V., Pinova Inc., Guangxi Dinghong Resin Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Terpene Resins Market Segmentation

By Product Type

- Polyterpene Resins

- Terpene-Phenol Resins

- Styrenated Terpene Resins

- Liquid Terpene Resins

By Form

By Application

- Adhesives and Sealants

- Inks and Coatings

- Rubber and Tires

- Food and Beverage

- Cosmetics and Pharmaceuticals

- Paper and Pulp

By End-Use Industry

- Packaging

- Automotive

- Construction

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Terpene Resins Industry

- Kraton Corporation

- Yasuhara Chemical Co., Ltd.

- DRT

- Arakawa Chemical Industries, Ltd.

- Mangalam Organics Limited

- Ingevity Corporation

- Sumitomo Bakelite Co., Ltd.

- Guangdong Nuochi Chemical Co., Ltd.

- Ganzhou Taipu Chemical Co., Ltd.

- Xiamen Well-Sunshine Co., Ltd.

- Star Pine Chemical Co., Ltd.

- Lawter B.V.

- Pinova Inc.

- Guangxi Dinghong Resin Co., Ltd.

*- List not Exhaustive