Market Overview: Camphor Market Expansion Driven by Indian Capacity Consolidation, Pharma-Grade Compliance, and Retail Diversification

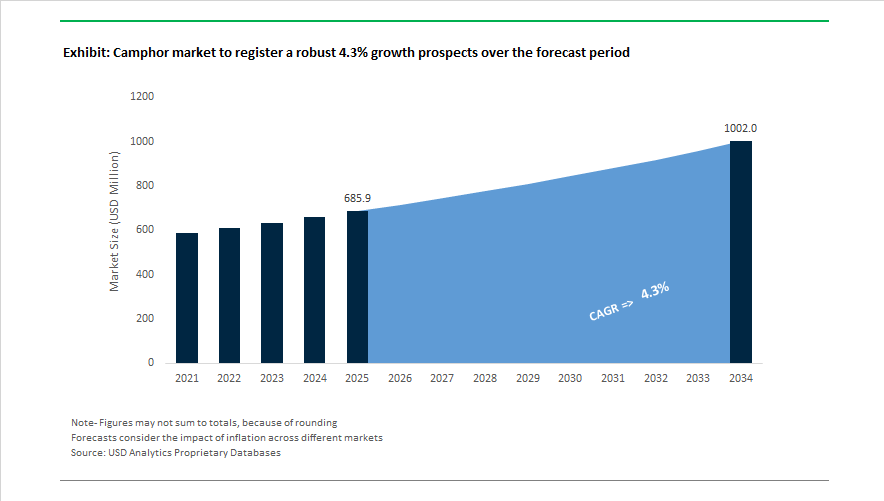

The camphor market is projected to grow from USD 685.9 Million in 2025 to USD 1001.9 Million by 2034, registering a CAGR of 4.3% , supported by expanding demand across pharmaceuticals, spiritual wellness, fragrance chemicals, and topical therapeutics. Production consolidation strengthened in late 2024 and 2025 when Oriental Aromatics Limited completed debottlenecking and expansion of its synthetic camphor unit, pushing segment volumes to record highs to meet export demand from global flavor and fragrance formulators. In September 2025, Kanchi Karpooram Limited finalized the acquisition of Kanchi Allied Peperone Pvt. Ltd., reinforcing upstream integration in terpene chemistry and strengthening supply continuity for resin and derivative manufacturing. Revenue signals in November 2025 showed strong retail traction, with Mangalam Organics Limited reporting a 29.06% year-on-year revenue increase for Q2 FY26 driven by distribution expansion of packaged camphor tablets in domestic and export markets.

Pharmaceutical-grade compliance and regulatory developments reshaped product positioning during 2025 and early 2026. Saptagir Camphor Pvt. Ltd. renewed its WHO-GMP certification in 2025, enabling continued supply of regulated camphor intermediates to more than 50 countries. The United Kingdom confirmed alignment with EU restrictions by banning 4-Methylbenzylidene Camphor effective July 2026, prompting cosmetic and sunscreen manufacturers to reformulate UV-filter systems away from this derivative. In parallel, AI-driven formulation research expanded in late 2024 and 2025 as Kerala Ayurveda and other wellness brands applied data-led tools to optimize camphor-menthol topical efficacy and skin compatibility. Retail healthcare channels broadened in 2025 when Himalaya Wellness partnered with Apollo Pharmacy to secure shelf space for camphor-based therapeutic balms, while multi-action rub launches in late 2025 combined respiratory relief with aromatherapy positioning.

Commercial volatility and channel transformation defined late 2025 to early 2026 dynamics. In September 2025, Kanchi Karpooram received a GST show cause notice concerning tax classification of intermediates, although CRISIL reaffirmed its BBB-/Stable rating in November 2025, citing strong financial fundamentals and low leverage. Mangalam Drugs and Organics reported a 34% sales decline in January 2026 results due to raw material price volatility in terpene intermediates, highlighting feedstock risk in synthetic camphor production. Simultaneously, 2025 saw rapid growth in direct-to-consumer e-commerce for spiritual wellness camphor products from firms such as Mayur Industries and Ajay Camphor Works, shifting the product narrative toward air purification and lifestyle use.

Sustainability-Conscious Sourcing Shifts, Regulatory Precision, and Downstream Pharmaceutical Demand Shape Trends and Opportunities in the Camphor Market

Expansion of Synthetic Turpentine-Based Camphor and Diversified Botanical Sourcing

Camphor production is expanding beyond traditional reliance on Cinnamomum camphora due to conservation policies and tighter harvesting controls in East Asia. Industrial buyers are prioritizing synthetic alpha-pinene routes that deliver stable availability and controllable purity profiles. In 2024, global demand for alpha-pinene reached approximately 196 thousand tonnes, reflecting rising industrial adoption of synthetic camphor with 96 to 98% purity suitable for pharmaceuticals and regulated consumer products.

At the same time, strategic diversification into new botanical inputs is advancing in India and East Africa. Ocimum kilimandscharicum (Kapur Tulsi) produces essential oil containing up to 70% camphor, reducing ecological pressure on endangered tree sources. These pilot projects support ESG-certified sourcing and create a premium channel for fragrance and ayurvedic wellness brands that require traceability and alignment with biodiversity compliance. As sustainability reporting becomes integral to procurement, hybrid sourcing models that balance synthetic reliability with natural origin claims are gaining traction.

Enantiopure Camphor Gains Momentum in Wellness, Aromatherapy, and High-Purity OTC Topicals

Consumer expectations in wellness markets are shifting from commodity-grade racemic camphor to enantiomer-specific (+)-camphor associated with higher perceived therapeutic efficacy. Across Europe and North America, therapeutic-grade camphor has achieved a 15 to 20% demand premium due to brand requirements for ISO-backed purity, documented provenance, and low impurity thresholds.

Concurrently, regulators are raising safety benchmarks. ECHA’s 2025 guidance for CAS 76-22-2 mandates greater toxicology transparency for consumer rinse-off and leave-on formulations. This drives formulators to eliminate low-cost industrial grades that carry residual terpene impurities. The result is a market where differentiation is no longer based on cost alone but on evidence-backed safety and performance positioning to meet retailer audits and regulatory review cycles.

Critical Role in Tenofovir Prodrug Manufacturing Supports Healthcare Access and Supply Chain Integration

Camphor’s value in pharmaceuticals extends beyond its direct topical applications to its function as a chiral intermediate in Tenofovir Disoproxil Fumarate (TDF), a primary antiviral medication for HIV/AIDS and Hepatitis B. With more than 250 million individuals affected by chronic Hepatitis B globally, TDF remains pivotal in global disease eradication strategies targeting 2030.

To sustain supply affordability, manufacturers in India and China are strengthening backward integration to control camphor-derived intermediates amid historical tariff and price disruptions in 2024–2025. Ensuring uninterrupted supply of pharmaceutical-grade camphor is increasingly viewed as a national healthcare priority in major exporting countries. This reinforces the market’s evolution from commodity chemical supply into a strategically protected ingredient category tied to public health outcomes.

Performance-Enhancing Plasticizer for Cellulose-Based Biopolymers in Sustainable Packaging and Electronics

Camphor is emerging as a key enabler in the transition toward petroleum-free polymers. Cellulose esters such as CAB and plasticized cellulose nitrate rely on camphor to improve flexibility, UV stability, and surface quality. These materials are gaining adoption in automotive interior trims and insulation films that require scratch resistance and optical clarity.

The renewed focus on eco-packaging is accelerating camphor use in cellulose-based transparent films that can reach more than 90% light transmission, making them viable replacements for PET in luxury packaging and specialty optics. As brands pursue sustainability-linked packaging mandates, camphor-enabled cellulose films are positioned to scale rapidly through 2025 and beyond, particularly in regions with single-use plastic restrictions.

Camphor Market Share and Segmentation Insights

Market Share by Form: Tablets Lead Tradition-Driven Demand While Oils Capture Wellness Growth

Camphor tablets hold 48% of global consumption in 2025, anchored by their widespread use in religious ceremonies, household rituals, and pest control, with India representing the largest single market. Low-cost synthetic camphor dominates this segment, supported by culturally ingrained demand patterns that remain resilient across economic cycles. Camphor powder ranks second, favored for faster dissolution and blending in pharmaceutical balms, ointments, and industrial formulations, with fine particle grades enabling uniform dispersion. Camphor oil is the smallest but fastest-growing form, expanding through aromatherapy, massage oils, vapor rubs, and hair tonics, benefiting from the global wellness movement and higher unit value compared to solid formats.

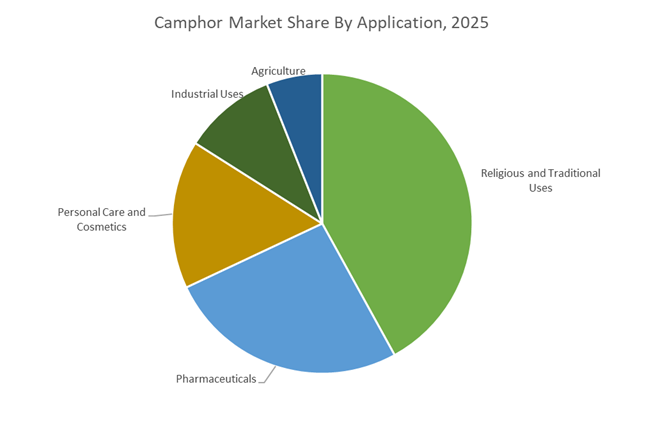

Market Share by Application: Ritual Use Leads While Personal Care Accelerates Adoption

Religious and traditional uses account for 42% of camphor demand in 2025, driven by daily worship and festival practices across South and Southeast Asia, with strong seasonality around Diwali and Navratri. Pharmaceuticals represent the second-largest segment, utilizing camphor for topical analgesics, anti-itch lotions, chest rubs, and mild expectorant formulations, with consumption tied to respiratory illness cycles and aging populations. Personal care and cosmetics form the fastest-growing application, integrating camphor into skincare, haircare, and fragrance products for its cooling and antiseptic properties, supported by clean beauty and Ayurveda-inspired branding. Industrial uses persist in celluloid plasticizers, specialty coatings, and pyrotechnics, while agriculture remains a niche outlet for natural insect repellents and veterinary balms, expanding gradually alongside organic farming practices.

Competitive Landscape of the Camphor Market

The global camphor market in 2026 is characterized by vertical integration across the pine chemicals value chain, rising demand for pharmaceutical-grade camphor, synthetic camphor crystals, terpene derivatives, and bio-based aroma chemicals, and increasing alignment with regulatory compliance and sustainability standards. Growth is being driven by expanding applications in topical analgesics, muscle rubs, vaporizing tablets, spiritual homecare products, plasticizers, nitrocellulose lacquers, and biodegradable polymers. Market leaders are differentiating through WHO GMP certification, USFDA compliance, CST-to-camphor integration, low-carbon alpha-pinene conversion technologies, and downstream retail branding strategies, positioning themselves to capture high-margin pharma, FMCG, and specialty chemical segments globally.

Integrated CST-to-Camphor Manufacturing Leadership by Mangalam Organics Limited

Mangalam Organics has established itself as a vertically integrated pine chemicals powerhouse, bridging industrial-scale synthetic camphor production with branded retail leadership. Its advanced Kumbhivali manufacturing hub integrates crude sulfate turpentine processing into finished camphor tablets and pharma-grade camphor powder, delivering cost efficiency and feedstock security. In 2026, Mangalam and CamPure dominate India’s homecare and spiritual camphor segment with innovative air fresheners and sublimating cones. The incorporation of Mangalam Vanasya Organic Private Limited strengthens its footprint in organic and natural pine derivatives. Supported by ESOP 2026 initiatives, the company aligns technical talent with long-term R&D growth in high-purity camphor and terpene derivatives.

Pharma-Grade Aroma-Camphor Synergy from Oriental Aromatics Limited

Oriental Aromatics Limited stands at the intersection of pharmaceutical camphor and global fragrance chemistry, leveraging full integration of Camphor & Allied Products Ltd operations into its aroma platform. Its USFDA and WHO GMP accredited camphor grades are preferred by global pharmaceutical manufacturers producing muscle rubs, nasal decongestants, and topical balms. Beyond pharma, OAL’s sublimating camphor enhances top-note clarity in fine fragrances and aromatherapy formulations, strengthening its position in FMCG and perfumery markets. Modernized plants in Bareilly and Mahad support scalable production of terpineols and specialty aroma chemicals, enabling cross-segment synergy and reinforcing OAL’s leadership in high-purity synthetic camphor exports.

Ultra-Pure Synthetic Camphor Export Hub by Saptagir Camphor Limited

Saptagir Camphor Limited is one of the world’s largest dedicated synthetic camphor manufacturers, operating WHO GMP-certified facilities in Hyderabad and Anantapur with exports to more than 50 countries. In 2026, the company leads in ultra-pure pharma-grade camphor, using advanced distillation to exceed pharmacopeia impurity standards required by European and North American CDMOs. Its portfolio includes camphor powder, crystalline flakes, and isoborneol intermediates essential for specialty plasticizers and high-performance chemical synthesis. With a strategic focus on zero-defect manufacturing and global regulatory compliance, Saptagir has emerged as a reliable Western supply chain alternative amid tightening quality benchmarks in the global camphor market.

Pine-to-Camphor Scale and Low-Carbon Synthesis by Fujian Green Pine Co., Ltd.

Fujian Green Pine dominates China’s camphor market through unmatched access to southern pine resources and large-scale alpha-pinene conversion facilities. Its vertically integrated pine-to-camphor operations provide feedstock stability, positioning the company as a price maker in the technical-grade camphor segment. In 2026, the company intensified investments in automated reactor systems to reduce energy intensity and carbon emissions during camphor synthesis. Its products are widely used in plasticizers, nitrocellulose lacquers, solvents, and celluloid-based plastics. Concurrently, Fujian Green Pine is advancing R&D into camphor-derived bio-based polymers, aligning with the global shift toward green plastics and sustainable specialty materials.

Terpene Derivatives Diversification Strategy by Kanchi Karpooram Limited

Kanchi Karpooram Limited specializes in terpene-based aroma chemicals, with camphor serving as its flagship revenue driver. Its portfolio spans camphene, dipentene, pine oils, and downstream isobornyl esters, enabling diversification beyond commodity camphor cycles. In 2026, the company is expanding tableting and branded packaging capacity to meet surging demand for high-purity retail camphor across Southeast Asia’s spiritual and homecare markets. Strategic focus on value-added derivatives reduces exposure to raw camphor price volatility while enhancing margins. By strengthening its downstream resin and ester production capabilities, Kanchi Karpooram positions itself as a specialty terpene innovator within the global camphor ecosystem.

High-Traceability USP/BP Camphor Supply in North America by Camphor Technologies, Inc.

Camphor Technologies represents the regulatory gold standard for USP and BP grade camphor distribution in North America. Serving pharmaceutical, cosmetics, and hospital-grade formulation markets, the company emphasizes high-traceability documentation aligned with FDA and EPA requirements. Its Florida-based quality control and repackaging facility enables customized particle size control, including micro-milled camphor powder preferred for rapid-absorption topical analgesics. In 2026, the company continues to bridge Asian manufacturing with Western compliance standards, offering customized packaging formats for laboratory and research applications. Its regulatory expertise and precision processing capabilities solidify its role as a strategic supply partner in the premium pharmaceutical camphor segment.

India’s Integrated Camphor Value Chain and Continuous Distillation Technology Strengthen Pharmaceutical and Spiritual Demand

India remains a structurally significant hub in the global camphor industry, supported by pharmaceutical integration, large-scale synthetic camphor production, and diversified end-use applications across religious, industrial, and wellness sectors. In late 2025, Oriental Aromatics Ltd reported a strategic pivot in its distribution model by internalizing legacy camphor brands such as Saraswati and 3 Pine, enabling end-to-end control of the camphor value chain—from alpha-pinene-based synthesis to direct pharmaceutical and spiritual retail channels. This backward and forward integration strengthens margin control in high-purity camphor crystals, camphor tablets, and terpene derivatives.

Saptagir Camphor Pvt Ltd continues to operate as India’s largest synthetic camphor manufacturer, maintaining a WHO-GMP certified facility and exporting terpene intermediates to over 50 countries. Industrial demand remains resilient: Kanchi Karpooram Ltd reported operational revenue of ₹39.95 crore for the quarter ending September 2025, reflecting steady demand for camphor used in paper chemicals and devotional applications. Indian manufacturers are increasingly deploying continuous distillation systems capable of producing isoborneol flakes and camphor crystals exceeding 99.5% purity, targeting aromatherapy oils and topical analgesic formulations. To mitigate alpha-pinene volatility, Mangalam Organics has expanded backward integration into crude turpentine oil sourcing. Automated camphor tablet compression lines at facilities such as Ajay Camphor Works now produce 4–5 metric tonnes per day, responding to rising demand for convenience-driven spiritual and home-care products.

China’s Green Manufacturing Mandates and Pinene Feedstock Dominance Enhance Synthetic Camphor Exports

China commands a competitive advantage in the global synthetic camphor market due to integrated gum rosin and turpentine production, regulatory digitization, and green manufacturing mandates. As a dominant global supplier of pinene derivatives, China benefits from abundant domestic feedstock, allowing companies such as Hunan Deli Essential Oil to maintain a lower cost basis for camphor powder and terpene-based intermediates.

On November 4, 2025, the Ministry of Agriculture and Rural Affairs (MARA) introduced draft rules to streamline registration of “export-only” chemical agents, including terpene derivatives, reducing approval friction for global camphor exports. Implementation of the National Pesticide Registration System (NPRS) has digitized certifications for camphor-based insect repellents and fumigants, leveraging AI-driven document review to accelerate cross-border trade. Under the 2025 Green Agriculture Plan, camphor plants must reduce VOC emissions, prompting adoption of closed-loop synthesis systems and advanced wastewater recovery technologies. Coastal refineries have integrated blockchain traceability to verify natural versus synthetic camphor crystal origin, strengthening compliance with European transparency standards. Concurrently, academic collaborations are exploring camphor as a carbon precursor in carbon nanotube synthesis, positioning it as a sustainable input for next-generation electronics manufacturing.

Japan’s Ultra-High-Purity Camphor and Oncology-Focused R&D Elevate Pharmaceutical-Grade Applications

Japan’s camphor industry is distinguished by high-purity pharmaceutical grades and advanced biomedical research. Companies such as Nippon Fine Chemical Co and Mitsubishi Gas Chemical prioritize JP/EP-grade camphor for topical medications, antiseptic formulations, and neurological research applications. Production processes emphasize ultra-low impurity thresholds to meet stringent pharmacopeial standards for medical-grade camphor crystals.

Peer-reviewed studies published in early 2025 by Japanese researchers highlight camphor’s potential in oncology, particularly its capacity to differentiate between malignant and healthy cells in targeted therapeutic research. Japan also leads in aromatherapy innovation, utilizing cold-press extraction to preserve delicate terpenoids in premium essential oil blends serving the luxury wellness market. In alignment with national circular economy objectives, producers are piloting bio-based camphor synthesis derived from forest waste streams, reducing reliance on petroleum-based intermediates. Advanced research investments in 4D microscopy and molecular modeling are analyzing camphor’s behavior as a skin penetration enhancer, expanding its utility in transdermal drug delivery systems and controlled-release pharmaceutical formulations.

Brazil’s Petrochemical Expansion and Green Medicine Movement Boost Domestic Camphor Manufacturing

Brazil’s camphor industry is benefiting from upstream petrochemical expansion and growing pharmaceutical demand. In 2025, Petrobras reported oil and gas production exceeding targets by 11% , securing stable availability of petrochemical intermediates required for synthetic camphor powder manufacturing. This feedstock security strengthens Brazil’s positioning as a regional synthetic camphor production hub for South America.

International chemical distributors are targeting Brazil for new camphor plant investments to supply the domestic pharmaceutical sector with locally manufactured alternatives. Generic drug manufacturers such as Cipla have expanded camphor inclusion in multi-ingredient respiratory capsules (camphor + chlorothymol + eucalyptol), responding to seasonal influenza spikes across Latin America. Government-backed “Forestry to Pharma” initiatives incentivize cultivation of Cinnamomum camphora for natural camphor oil extraction, diversifying export portfolios. Urban consumer trends in São Paulo and other metropolitan centers show rising demand for camphor-based topical rubs free from synthetic fragrances and dyes, aligning with the broader Green Medicine movement and supporting natural camphor crystal applications.

Germany’s REACH 2025 Compliance and Neurotherapeutic Research Advance Premium Camphor Grades

Germany is at the forefront of EU-compliant camphor manufacturing, aligning with REACH 2025 purity standards by minimizing trace impurities in camphor used for disinfectants, preservatives, and pharmaceutical excipients. Advanced sublimation technology investments have reduced the carbon intensity of camphor crystal formation, enabling CO₂-footprint labeling for eco-conscious buyers.

German pharmaceutical clusters are expanding research into camphor-derived compounds for neurodegenerative disorder therapies, reinforcing demand for ultra-refined, medical-grade camphor. Supply chain resilience has improved through diversification of alpha-pinene sourcing, incorporating recycled turpentine and sustainably harvested Asian gum to reduce geopolitical concentration risk. Beyond healthcare, Germany’s high-performance coatings industry uses camphor as a plasticizer in specialty lacquers and paints requiring controlled evaporation rates and high-gloss finishes, supporting industrial-grade camphor consumption in advanced manufacturing sectors.

Vietnam’s Refinery Integration and ASEAN Export Strategy Accelerate Camphor-Based Consumer Products

Vietnam is emerging as a competitive camphor manufacturing base in Southeast Asia, supported by infrastructure development and petrochemical integration. A $966 million investment by Vinhomes JSC in smart city projects has stimulated demand for camphor-based disinfectants, air-care products, and household repellents.

Expansion of the Nghi Son Refinery has enhanced access to chemical precursors, reducing reliance on imported feedstocks and lowering production costs for domestic camphor processors. Vietnam is positioning itself as a low-cost export hub for camphor-based insect repellents and mothballs targeting ASEAN and North American retail markets. Favorable FDI policies, including tax holidays for downstream petrochemical projects, have attracted foreign manufacturers to establish terpene processing plants in central industrial zones, strengthening Vietnam’s role in the global synthetic camphor and terpene derivatives supply chain.

Camphor Market Report Scope

Camphor market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$685.9 Million

|

|

Market Size (2034)

|

$1001.9 Million

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product Type (Natural Camphor, Synthetic Camphor), By Form (Camphor Powder, Camphor Tablets, Camphor Oil), By Grade (Pharmaceutical Grade, Industrial Grade, Specialty Grade), By Application (Pharmaceuticals, Personal Care and Cosmetics, Agriculture, Industrial Uses, Religious and Traditional Uses), By End Use Industry (Healthcare and Pharmaceuticals, Consumer Goods and Wellness, Agriculture and Horticulture, Chemicals and Materials)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mangalam Organics, Kanchi Karpooram, Oriental Aromatics, Saptagir Camphor, Taiwan Tekho Camphor, Indukem International, Spectrum Chemical, Vigon International, Hunan Nutramax, Ningbo Inno Pharmchem, Aldon Corporation, Arora Aromatics, SD Fine Chem, Mysore Camphor

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Camphor Market Segmentation

By Product Type

- Natural Camphor

- Synthetic Camphor

By Form

- Camphor Powder

- Camphor Tablets

- Camphor Oil

By Grade

- Pharmaceutical Grade

- Industrial Grade

- Specialty Grade

By Application

- Pharmaceuticals

- Personal Care and Cosmetics

- Agriculture

- Industrial Uses

- Religious and Traditional Uses

By End Use Industry

- Healthcare and Pharmaceuticals

- Consumer Goods and Wellness

- Agriculture and Horticulture

- Chemicals and Materials

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Camphor Industry

- Mangalam Organics

- Kanchi Karpooram

- Oriental Aromatics

- Saptagir Camphor

- Taiwan Tekho Camphor

- Indukem International

- Spectrum Chemical

- Vigon International

- Hunan Nutramax

- Ningbo Inno Pharmchem

- Aldon Corporation

- Arora Aromatics

- SD Fine Chem

- Mysore Camphor

*- List not Exhaustive