Textile Finishing Agents Market 2025–2034: $2.8 Billion to $4.7 Billion at 5.8% CAGR Fueled by PFC-Free Innovation, Circular Chemistry, and Integrated Fiber Processing

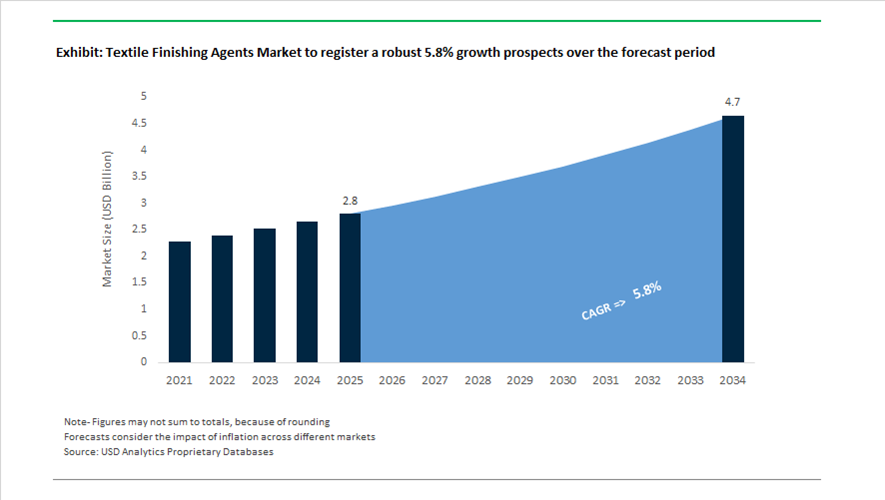

The global textile finishing agents market is valued at $2.8 billion in 2025 and is projected to reach $4.7 billion by 2034, expanding at a CAGR of 5.8%. Finishing agents—including softeners, repellents, antimicrobial treatments, flame retardants, wrinkle-free agents, and performance coatings—are increasingly engineered to meet PFAS restrictions, ZDHC compliance frameworks, and low-carbon manufacturing standards. Market growth is being driven by performance apparel, automotive textiles, aerospace composites, and technical fabrics that require multifunctional properties such as moisture control, durability, odor resistance, and stain repellency. Regulatory pressure on “forever chemicals” and heavy-metal catalysts is accelerating the shift toward bio-based, waterless, and recyclable finishing chemistries.

Portfolio consolidation and distribution realignment intensified across 2024–2026. In 2024, Pulcra Chemicals completed the integration of Tanatex Chemicals, combining two major European finishing portfolios with a focus on bio-based softeners and repellents. In April 2024, Devan Chemicals (a Pulcra subsidiary) introduced a 40% bio-based, PFC-free stain-release technology targeting outdoor apparel brands transitioning away from fluorinated chemistries. In February 2026, RUDOLF GmbH assumed exclusive global distribution rights for Sanitized® hygiene technologies, consolidating antimicrobial finishing under a single international supply platform. In December 2024, Archroma relocated its headquarters to Pratteln, Switzerland, converting its former site into a sustainable technology hub dedicated to next-generation finishing chemistry. In January 2026, Archroma unveiled aniline-free indigo and waterless denim finishing agents at Denimsandjeans Colombia, eliminating traditional heavy-metal catalysts while preserving vintage aesthetics.

Regional capacity expansion and process digitization are reshaping production economics. In March 2025, an AI-driven textile chemical facility launched in Pune, India, integrating solar energy and closed-loop water systems to produce near-zero-carbon finishing agents. In February 2026, Rossari Biotech partnered with Sadara Chemical Company to localize advanced finishing agent production in Saudi Arabia, strengthening Middle Eastern supply resilience. In February 2025, Tonello acquired Flainox, combining finishing machinery with dyeing systems to reduce water and chemical consumption during application cycles. Meanwhile, in February 2026, Rieter Holding AG completed the acquisition of Barmag, integrating fiber extrusion and finishing technologies to streamline in-line application of chemical finishes. Circular feedstock pathways are also emerging: in April 2024, Novoloop and Aether Industries operationalized a recycling pilot in Surat converting polyethylene waste into monomers used in high-performance finishing agents.

Compliance-Led Reformulation and Value-Added Functionalization in the Textile Finishing Agents Market

PFAS-Free DWR Becomes a Regulatory Requirement Rather Than a Brand Choice

The textile finishing agents market has crossed a structural inflection point as fluorinated chemistries move from being discouraged to being legally prohibited across major apparel consumption markets. The ban on intentionally added PFAS under California AB 1817 and parallel legislation in New York, effective January 1, 2025, has eliminated optionality for apparel brands and their chemical suppliers. Finishing agents based on long-chain and short-chain fluorocarbons are now commercially nonviable for consumer textiles, forcing mills to adopt silicone, paraffin, and dendrimer-based water repellents at industrial scale.

A defining signal of this shift was the February 2025 announcement by W.L. Gore & Associates confirming the full commercialization of its expanded polyethylene (ePE) membrane platform. By integrating PFAS-free laminates with fluorine-free DWR chemistries, Gore-Tex Pro garments supplied to Arc’teryx, Patagonia, and Mammut achieved parity with legacy waterproof performance benchmarks. This effectively reset technical expectations for high-performance outerwear, accelerating the obsolescence of fluorinated repellents across premium and mass-market segments alike.

Regulatory tightening in Europe is reinforcing this trajectory. The EU’s updated POPs Regulation in May 2025 reduced allowable PFOS trace contamination to 0.025 mg/kg, while the August 2025 European Chemicals Agency REACH proposal introduced a ban-with-derogations framework. While limited exemptions remain for PPE and certain industrial textiles, consumer apparel finishing is now firmly locked into fluorine-free chemistries. This bifurcation is reshaping supplier portfolios, with R&D investment shifting toward high-durability non-fluorinated repellents capable of meeting outdoor performance and wash-fastness requirements.

Bio-Based Softeners Scale Rapidly in Skin-Contact and Export-Oriented Apparel

Parallel to the PFAS exit, the market is experiencing a pronounced shift toward bio-based softeners in categories where skin contact, odor neutrality, and carbon footprint disclosures directly influence brand equity. Babywear, intimate apparel, and premium cotton garments are increasingly specified with softeners derived from vegetable oils and amino-acid surfactants rather than petrochemical quaternaries.

In September 2025, Archroma launched Siligen® D2W LIQ C, a bio-based silicone softener engineered to meet ZDHC Level 3 and Bluesign requirements. Beyond compliance, the formulation delivers a documented carbon footprint reduction of up to 30% compared to fossil-based alternatives, a metric that is now actively tracked by EU and UK apparel importers under ESG disclosure frameworks.

This transition is also driving regional capacity realignment. Late-2025 industry data shows over $180 million in new investment flowing into Bangladesh’s textile chemical sector as multinational suppliers localize the production of eco-based finishing agents. These investments are directly linked to the EU’s Ecodesign for Sustainable Products Regulation, which places responsibility for chemical safety and environmental impact on both brands and their upstream processing partners. For export-oriented garment hubs, access to certified bio-based softeners is becoming a prerequisite for order retention rather than a differentiator.

Microencapsulated Phase Change Materials Enable Active Thermoregulation Finishes

A high-margin opportunity is emerging at the intersection of activewear, occupational safety, and wellness through microencapsulated Phase Change Materials. These finishing agents introduce dynamic thermal regulation by absorbing and releasing heat within a defined temperature window, shifting textile finishes from passive comfort enhancement to active performance management.

Insights presented at the October 2025 Tech Tour Bio-based Industries forum highlighted the commercialization of bio-derived PCMs integrated into finishing formulations as replacements for petroleum wax systems. These materials stabilize microclimate temperatures by operating within a 28°C to 32°C buffer zone, a range critical for reducing heat stress without compromising garment breathability.

Adoption accelerated in 2025 within protective workwear for first responders and industrial operators, where PCM-based finishes capable of surviving more than 50 industrial wash cycles demonstrated measurable reductions in thermal fatigue. As the technical textiles segment exceeds $2.5 billion in value, durable thermoregulating finishes represent a scalable pathway for chemical suppliers to move beyond commoditized softeners and repellents into performance-priced functional systems.

Conductive and Anti-Static Finishes Expand with Medical and Electronic Textiles

The final major opportunity vector lies in conductive and anti-static finishing agents as smart textiles transition from experimental applications to regulated healthcare and electronics environments. Demand is being driven by e-wearables, medical monitoring garments, and cleanroom apparel where static control and signal reliability are mission-critical.

Peer-reviewed research published in April 2025 demonstrated successful Direct Ink Writing of conductive finishes onto textiles using bio-based solvents, enabling flexible circuits that retain conductivity under repeated mechanical stress. These developments are accelerating the industrialization of textile-based sensors for heart rate, glucose, and motion monitoring.

In parallel, October 2025 product launches from leading technical chemical suppliers introduced graphene-based anti-static and EMI-shielding finishes designed for semiconductor cleanrooms and hospital environments. These coatings achieve surface resistivity levels between 10⁵ and 10⁹ ohms, aligning with stringent safety standards while maintaining fabric flexibility and wash durability. For finishing agent producers, this segment offers a defensible growth opportunity where regulatory compliance, electrical performance, and application know-how create high barriers to entry.

Textile Finishing Agents Market Share and Segmentation Insights

Chemistry Type Market Share: Silicone-Based Agents Lead with Advanced Softness and Functional Performance

Silicone-based agents hold the largest share at 32.80% in the textile finishing agents market in 2025, driven by their superior ability to impart softness, smoothness, and enhanced hand feel across diverse textile applications. These agents are widely used in apparel, home textiles, and technical fabrics due to their multifunctional properties, including water repellency, wrinkle resistance, and durability. Other chemistry types such as fluorine-free repellents, flame retardants, polymeric and bio-based agents, cross-linking agents, and enzyme-based auxiliaries contribute to performance-specific applications. A notable trend is the development of hydrophilic silicone softeners, which combine softness with improved moisture absorption and wicking, supporting next-generation comfort textiles.

End-Use Industry Market Share: Apparel Segment Drives Finishing Agent Demand Through Performance Textiles

Apparel accounts for 42.80% of the textile finishing agents market in 2025, supported by the extensive use of finishing chemicals to enhance comfort, durability, and functionality in clothing. The segment requires a broad range of finishes, including softeners, antimicrobial agents, water repellents, and wrinkle-resistant treatments. Home textiles, technical textiles, and industrial textiles contribute to additional demand with application-specific requirements. A key growth driver is the expansion of performance apparel and athleisure segments, where demand for advanced finishes such as moisture management, UV protection, odor control, and durable water repellency continues to rise, with formulations designed to maintain performance across multiple wash cycles.

Textile Finishing Agents Market Competitive Landscape

The textile finishing agents market in 2026 is defined by formula transparency, PFAS-free innovation, and Right-First-Time (RFT) processing. Industry leaders are deploying nanotechnology, low-VOC chemistries, and biocircular feedstocks to achieve performance parity with fluorinated finishes while optimizing energy efficiency and minimizing chemical waste in textile finishing operations.

Archroma Advances Silicone-Based Softeners and Low-Temperature Finishing Systems for Sustainable Textiles

Archroma leads the textile finishing agents market through its Planet Conscious strategy, replacing legacy chemistries with high-performance sustainable systems. The launch of SILIGEN® D2W LIQ C in November 2025 addresses softness and elasticity challenges in cotton-lycra blends using advanced silicone chemistry. Its 2026 partnership with HeiQ strengthens antimicrobial and odor-control finishing capabilities for athleisure and hygiene textiles. Archroma’s exclusive global distribution of Fibre52® technology enables low-temperature, neutral-pH bleach and dye systems, reducing energy consumption. Ten major product groups achieving Cradle to Cradle Certified® Material Health Gold highlights its leadership in circular textile chemistry. The company continues to integrate digital traceability and eco-compliant finishing solutions for global textile mills.

DyStar Optimizes Global Supply Chain with Cadira® Modules and Integrated Manufacturing Backbone

DyStar has strengthened its competitive position following full integration under Zhejiang Longsheng Group in 2026, enhancing upstream-downstream synergies. The restructuring resolved legacy ownership disputes while improving supply chain stability and cost efficiency. Its Cadira® finishing modules remain a cornerstone offering, enabling textile mills to reduce water, energy, and chemical usage through pre-validated process recipes. Operational consolidation in North America has significantly lowered fixed costs and improved profitability. DyStar’s regional sales restructuring supports growth in automotive textiles and high-performance workwear segments. The company is leveraging its integrated manufacturing base to deliver scalable, resource-efficient finishing solutions.

RUDOLF Scales PFAS-Free Finishing with Carbon Footprint Transparency and Advanced Hygiene Technologies

RUDOLF is at the forefront of PFAS-free textile finishing, expanding its global footprint through exclusive rights to Sanitized® technologies in 2026. Its portfolio now integrates advanced odor-neutralization and antimicrobial solutions such as Silvertec™, Puretec™, and Odorex™. The OX20 non-biocidal odor control technology delivers durable performance via physical adsorption while maintaining GOTS compliance. RUDOLF’s PCF-certified BIONIC-FINISH® ECO platform enables transparent carbon accounting for fluorine-free water repellents. The company is targeting high-performance medical and workwear textiles requiring durability under industrial washing conditions. Its innovation pipeline focuses on sustainable, high-temperature-resistant finishing agents aligned with evolving global regulations.

Evonik Expands Silicone Polymer Innovation for High-Performance Textile and Technical Applications

Evonik is advancing its position in textile finishing agents through its Beyond Chemistry strategy, focusing on high-margin specialty additives. Achieving €1.87 billion EBITDA in 2025, the company is reinvesting in advanced silicone-based polymers for textile and polyurethane applications. Its Tailor Made program enhances agility in developing finishing agents for technical textiles, including 3D-printed materials and breathable membranes. Evonik’s Custom Solutions segment targets elastane and microfiber treatments requiring superior durability and water resistance. The company is aligning its portfolio toward ROCE-driven growth, emphasizing advanced technologies over commodity chemicals. Its finishing agents play a critical role in performance apparel and industrial textile innovation.

Pulcra Delivers Bio-Based Finishing Solutions with Advanced Fixation and Thermoregulation Technologies

Pulcra Chemicals is positioning itself as a process-driven innovator, offering tailored finishing auxiliaries for complex textile applications. The launch of STABIFIX® NBF in 2026 enhances wet fastness and durability in polyamide-based technical fabrics. Its Naturalis® portfolio supports bio-based finishing aligned with ESG and bluesign® standards. Integration of Devan Chemicals has expanded Pulcra’s capabilities into thermoregulation and flame retardant finishes for home textiles. The PULCRA TEC® NFS platform addresses performance gaps in PFAS-free water repellents, eliminating yellowing issues while maintaining high efficiency. Its EcoVadis Silver rating reinforces its commitment to sustainable textile chemical innovation and transparent manufacturing practices.

Huntsman Strengthens Textile Coatings Portfolio with MDI-Based Solutions and Cost-Optimized Operations

Huntsman has repositioned its textile finishing presence following the divestiture of its Textile Effects division, focusing on high-performance intermediates and coatings. The company achieved $100 million in cost savings in 2025, improving margin resilience in specialty intermediates. Its MDI-based polyurethane and TPU solutions are critical for technical textiles used in automotive, construction, and cold chain applications. Huntsman is optimizing production at its Ghent and Florida facilities to meet global demand for amine-based finishing components. Additional $45 million productivity targets in 2026 support operational efficiency and supply chain optimization. Its advanced materials portfolio enables durable, high-performance coatings for industrial and functional textiles.

India Textile Finishing Agents Market Anchored in Mega Parks and Compliance-Driven Modernization

India’s textile finishing agents market is being structurally reshaped by large-scale infrastructure integration and tightening regulatory frameworks. The rollout of seven PM MITRA mega textile parks during 2025–2026, backed by an estimated $10 billion in cumulative investment, is a decisive inflection point for finishing auxiliaries. These parks are designed with centralized Zero Liquid Discharge and Common Effluent Treatment Plants capable of handling the high Chemical Oxygen Demand associated with modern resins, softeners, and functional coatings. As a result, finishing agents with lower liquor ratios, improved exhaustion, and faster biodegradability are increasingly preferred by mills operating within these integrated ecosystems.

Policy instruments are reinforcing this shift. Under the National Technical Textiles Mission, start-ups supported through the GREAT scheme in 2025 are accelerating innovation in medical and industrial finishes, including antimicrobial, flame-retardant, and barrier coatings. The revised Production Linked Incentive 2.0 scheme lowered investment thresholds for MSMEs, incentivizing domestic production of man-made fiber and technical textile finishes where moisture management and hygiene performance are critical. Commercial launches such as Zydex Group’s siZaltex LVn illustrate the market’s pivot toward bio-eliminable alternatives that reduce polymeric residue in effluents. Concurrently, BIS Quality Control Orders effective in early 2026 are forcing formulators to standardize finishing chemistries to international safety benchmarks, accelerating consolidation toward compliant, export-ready products.

China Textile Finishing Agents Market Driven by Digital Dosing and PFAS Substitution

China’s textile finishing agents market is transitioning from volume-led growth to precision-driven efficiency under the Ministry of Industry and Information Technology’s 2026 Blueprint. Finishing plants across Zhejiang and Guangdong have integrated AI-driven dosing and monitoring systems, with early 2025 data indicating an average 15% reduction in chemical waste. This digitalization is materially altering demand patterns, favoring highly concentrated finishing agents with predictable performance profiles that can be optimized through automated application.

Upstream integration further strengthens domestic supply chains. The Sinopec Yizheng Chemical Fiber complex reached full operational scale in 2025, providing integrated polyester feedstocks that support the localized production of polyester-affinity finishing agents and specialty resins. Regulatory and trade measures are also shaping the market. Import duty relaxations introduced in January 2026 for select high-end auxiliaries and raw wool are enabling Chinese garment manufacturers to target European premium segments. At the same time, major suppliers such as Skychem Group completed the phase-out of long-chain fluorinated repellents in 2025, replacing them with bio-based and silicone-based Durable Water Repellent systems to align with global PFAS restrictions.

Germany Textile Finishing Agents Market Defined by Low-Temperature Performance and EU Compliance Leadership

Germany represents the technology and compliance frontier of the textile finishing agents market. In mid-2025, BASF SE expanded its Lavergy C Care and A Star ranges at Ludwigshafen, focusing on soil release, whiteness maintenance, and finishing performance at ultra-low wash temperatures of 30°C to 40°C. These formulations directly address energy reduction mandates while maintaining premium fabric aesthetics required by European brands.

Innovation is complemented by strong regulatory leadership. CHT Group received the German Sustainability Award in late 2025 for its PIGMENTURA solution, a solvent-free pigment printing and finishing process that cuts energy use by up to 20%. German firms are also investing upstream to decarbonize finishing chemistry. BASF’s methane pyrolysis pilots initiated in late 2025 aim to supply low-carbon hydrogen for the synthesis of amines, softeners, and functional finishes. By 2025–2026, Germany-led suppliers had largely completed the transition to ZDHC MRSL V3.1 Level 3 standards, reinforcing their role as preferred partners for compliance-sensitive global apparel supply chains.

United States Textile Finishing Agents Market Reshaped by PFAS and Flame-Retardant Regulation

The United States textile finishing agents market is undergoing a regulatory-driven substitution cycle. The Environmental Protection Agency’s prohibition on articles containing PIP (3:1), effective October 31, 2026, is forcing apparel and upholstery manufacturers to reformulate flame-retardant finishes that historically relied on phenolic phosphate chemistries. This has accelerated demand for alternative binders and coatings with improved toxicological profiles.

State-level actions have amplified the impact. Bans on intentionally added PFAS implemented in California and New York from January 2025 are redefining water-repellency standards across the U.S. market. Finishing agents based on alkylated polymers, silicones, and hybrid bio-based systems are rapidly replacing legacy fluorinated chemistries. Feedstock innovation is supporting this transition. The Qore facility in Iowa, a joint venture between Cargill and HELM, scaled production of QIRA bio-based BDO in 2025, providing renewable building blocks for polyurethane textile coatings and functional finishes aligned with emerging ESG procurement criteria.

Bangladesh Textile Finishing Agents Market Strengthened by Green Factory Investment

Bangladesh’s textile finishing agents market is increasingly aligned with sustainability-led export competitiveness. In 2025, multinational chemical suppliers invested more than Tk 2,000 crore to support the country’s transition toward certified green factories within the Ready-Made Garment sector. These investments are concentrated in low-formaldehyde resins, energy-efficient softeners, and high-exhaustion finishing systems that reduce both water and energy intensity.

Decarbonization metrics are becoming a differentiator. DBL Group reported a reduction of 3,095 tons of CO2 emissions in 2025 through the adoption of heat recovery modules and sustainable finishing chemistries. This progress is positioning Bangladesh as a transparent, compliance-ready sourcing destination for European and North American brands, structurally increasing demand for certified, low-impact textile finishing agents.

Comparative Snapshot: Textile Finishing Agents Market by Country

Textile Finishing Agents Market County Level Snapshot

|

Country

|

Primary Growth Lever

|

Regulatory or Infrastructure Driver

|

Strategic Impact on Finishing Agents

|

|

India

|

PM MITRA parks and PLI 2.0

|

ZLD and BIS QCO enforcement

|

Shift toward bio-eliminable, low-COD finishes

|

|

China

|

Digital dosing and integration

|

MIIT 2026 and PFAS phase-out

|

Precision, high-concentration formulations

|

|

Germany

|

Low-temperature performance

|

ZDHC MRSL Level 3, EU eco-regulation

|

Premium, compliance-led innovation

|

|

United States

|

Chemical substitution

|

EPA PIP and state PFAS bans

|

Rapid reformulation of DWR and FR finishes

|

|

Bangladesh

|

Green factory investments

|

Brand-driven decarbonization

|

Rising demand for certified sustainable finishes

|

Textile Finishing Agents Market Report Scope

Textile Finishing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Chemistry Type (Fluorine-Free Repellents, Silicone-Based Agents, Polymeric and Bio-Based Agents, Cross-Linking Agents, Enzyme-Based Auxiliaries, Flame Retardants), By Functionality (Softening and Hand-Feel, Durable Water Repellency, Antimicrobial Finishes, Wrinkle-Free Finishes, Flame Retardancy, UV Protection and Moisture Management), By Application Method (Pad-Dry-Cure, Exhaust Processing, Coating and Lamination, Digital Finishing, Plasma and Nano-Finishing), By End-Use Industry (Apparel, Home Textiles, Technical Textiles, Industrial Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, BASF SE, Huntsman Corporation, CHT Group, Rudolf GmbH, DyStar Group, Evonik Industries AG, Tanatex Chemicals, Pulcra Chemicals, Wacker Chemie AG, Dow Chemical Company, Solvay S.A., Zydex Group, HeiQ Materials AG, Skychem Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Textile Finishing Agents Market Segmentation

By Chemistry Type

- Fluorine-Free Repellents

- Silicone-Based Agents

- Polymeric and Bio-Based Agents

- Cross-Linking Agents

- Enzyme-Based Auxiliaries

- Flame Retardants

By Functionality

- Softening and Hand-Feel

- Durable Water Repellency

- Antimicrobial Finishes

- Wrinkle-Free Finishes

- Flame Retardancy

- UV Protection and Moisture Management

By Application Method

- Pad-Dry-Cure

- Exhaust Processing

- Coating and Lamination

- Digital Finishing

- Plasma and Nano-Finishing

By End-Use Industry

- Apparel

- Home Textiles

- Technical Textiles

- Industrial Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Textile Finishing Agents Market

- Archroma

- BASF SE

- Huntsman Corporation

- CHT Group

- Rudolf GmbH

- DyStar Group

- Evonik Industries AG

- Tanatex Chemicals

- Pulcra Chemicals

- Wacker Chemie AG

- Dow Chemical Company

- Solvay S.A.

- Zydex Group

- HeiQ Materials AG

- Skychem Group

*- List not Exhaustive