Thin Wall Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Thin Wall Packaging Market Set to Reach $65.7 Billion by 2034 Driven by Sustainability and Lightweight Innovations

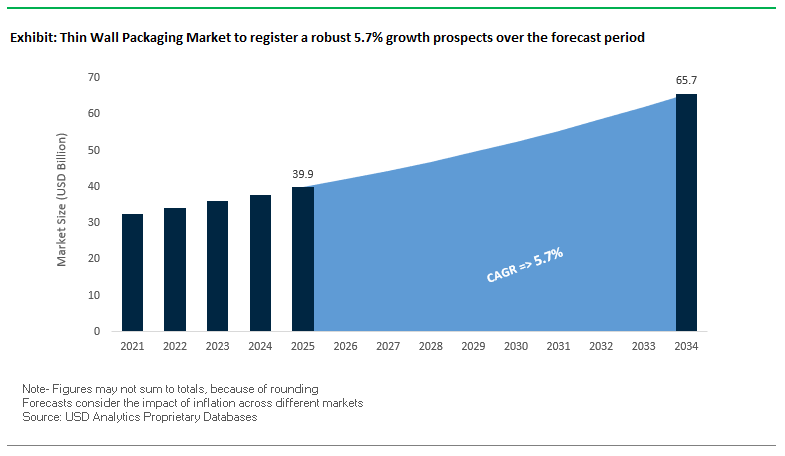

The global thin wall packaging market is projected to grow from $39.9 billion in 2025 to $65.7 billion by 2034, at a CAGR of 5.7%. This market, which encompasses thin-walled cups, trays, and containers, is a cornerstone of the food and beverage industry, emphasizing lightweight, sustainable, and cost-efficient packaging solutions.

Key Insights for packaging and sustainability professionals:

- Material reduction and lightweighting are central trends, with innovations reducing wall thickness up to 15% in PET containers, lowering raw material use and transport emissions.

- Mono-material and recyclable solutions are gaining traction, particularly with polypropylene (PP) and PET technologies, supporting circular economy initiatives.

- Advanced polymer formulations are improving barrier properties, extending shelf life for dairy, ready meals, and fresh produce.

- E-commerce packaging optimization is emerging as a priority, balancing product protection, aesthetics, and shipping efficiency.

- Regulatory and consumer pressure is driving environmentally friendly solutions that reduce carbon footprint and increase recyclability.

The market demonstrates significant opportunities for material innovation, sustainable design, and cost-efficient manufacturing, making it attractive for packaging manufacturers, brand owners, and sustainability-focused investors.

Market Analysis: Technological Advancements and Strategic Collaborations Propel Growth in Thin Wall Packaging

The thin wall packaging market is witnessing dynamic developments, driven by material innovation, circular economy initiatives, and strategic collaborations. In August 2025, Borealis partnered with STABILO and Gehr to explore sustainable materials for consumer products, while also selecting IMCD as its Bormed™ distribution partner for the Americas, expanding its footprint in healthcare and medical device packaging.

Capacity expansion and new product launches are reshaping the industry. In July 2025, Borealis released Borcycle™ M, a flexible packaging grade designed to enhance recyclability and performance in thin wall applications. Similarly, ALPLA Group announced in June 2025 the start of series production of thin-walled rPET yogurt cups, marking a significant step toward a circular economy in dairy packaging.

Sustainability-focused innovations continue to accelerate. In April 2025, Mondi introduced recyclable mono-material pet food bags with Saga Nutrition, replacing multi-material options. SABIC highlighted its mono-PP thin-wall cup with in-mold label in March 2025, facilitating full recyclability. Earlier, in November 2023, ITC Packaging launched TWI-PET, enabling one-step thin-wall PET molding, and Netstal showcased a 100% PP lightweight ICM thin wall cup in October 2023, further emphasizing circularity.

Trends and Opportunities in the Thin Wall Packaging Market

Accelerated Lightweighting through Advanced Material Engineering

The thin wall packaging market is being transformed by lightweighting strategies driven by polymer innovation and process optimization. Companies like Borealis are advancing the use of Borstar® Nucleation Technology, enabling up to 30% wall thickness reduction while maintaining stiffness, impact resistance, and durability. This shift is not only reducing material usage but also directly lowering transportation emissions, making it a cornerstone of sustainability and cost efficiency.

Resin producers such as SABIC are also reshaping manufacturing economics with PP FLOWPACT impact copolymers, which deliver faster crystallization speeds and high-flow properties. A 15-gram container with a 0.38 mm wall thickness, for example, can achieve 11% faster cycle times, enhancing throughput and lowering unit costs. Furthermore, advanced polypropylene (PP) grades are achieving superior top-load performance, boosting stackability for logistics and reducing freight expenses. These innovations demonstrate how lightweighting and efficiency improvements are converging to redefine profitability and sustainability in thin wall food and beverage packaging.

High-Performance PCR Integration for a Circular Economy

The demand for post-consumer recycled (PCR) content is reshaping the thin wall packaging market. Breakthroughs in chemical recycling are enabling food-grade polypropylene (rPP) from difficult-to-recycle plastic waste. A pioneering case from Borealis and Greiner Packaging demonstrated chemically recycled rPP iced coffee cups, proving the feasibility of virgin-quality PCR in sensitive food applications.

Meanwhile, ALPLA’s RePETec thin-wall containers made with up to 100% rPET are pushing the boundaries of recycled content integration. These ultra-thin (0.32 mm) walls outperform conventional PP with 20x higher oxygen barrier protection and 1.5x lower water vapor transmission, ensuring safety and product longevity. In parallel, the industry is eliminating problematic packaging components. In-mold labeling (IML) removes adhesives that contaminate recycling streams, aligning with new EU regulations that ban paper-sleeved cups. This trend underscores how design-for-recycling and mono-material strategies are becoming critical to achieving a circular economy.

Development of Enhanced Barrier Properties for Extended Shelf Life

One of the most promising opportunities in the thin wall packaging market lies in creating high-barrier, recyclable structures. ExxonMobil’s development of a 95% polyethylene (PE)-based thermoformed food barrier container with a thin EVOH layer exemplifies this shift. Such designs deliver extended shelf life comparable to multi-material laminates while ensuring compatibility with recycling streams.

The push toward bio-based barrier coatings is also gaining traction. Research highlights materials like polyvinyl alcohol (PVA) and lignin-based coatings as viable alternatives to petrochemical barriers. These innovations can drastically reduce oxygen and moisture permeability, enabling sustainable packaging for sensitive food categories such as juices, dairy, and fresh produce. By replacing complex laminates with mono-material or bio-enhanced solutions, brands can expand shelf-stable product portfolios while meeting recyclability and compostability mandates.

Design for Advanced Recycling Compatibility

Thin wall packaging often suffers from downcycling in mechanical recycling systems, where food-contaminated or multi-layer materials are turned into lower-value products. However, advanced chemical recycling technologies such as pyrolysis are unlocking new value streams by converting polypropylene (PP) and polyethylene (PE) waste into virgin-quality feedstocks.

Designing packaging for compatibility with these technologies offers dual benefits: it ensures higher-value recovery while securing a stable supply of recycled raw materials for new food-grade packaging. Industry investments, particularly in Europe and Asia, are scaling facilities capable of processing difficult-to-recycle thin-wall waste streams, reducing reliance on fossil-based resins. This compatibility-driven approach not only advances the circular economy for plastics but also ensures that thin wall packaging remains a viable, sustainable solution for high-volume food and beverage applications.

Competitive Landscape: Key Players in Thin Wall Packaging Are Leveraging Sustainability and Technology to Drive Market Leadership

The thin wall packaging industry is dominated by companies focused on material innovation, recycling, lightweighting, and global scalability, supporting the growth of food, beverage, and consumer product sectors.

Berry Global Group, Inc.: Accelerating Circular Economy Transition Through Vertically Integrated Sustainable Packaging

Berry Global offers rigid and flexible thin wall packaging solutions, closures, and films across food, beverage, and personal care applications. In March 2025, the company reported that 93% of its FMCG packaging is recyclable or has a validated alternative and increased bioplastics purchases by 130% YoY. Its vertically integrated model enables efficient scaling of sustainable solutions in line with its Impact 2025 roadmap.

Amcor plc: Driving Circular Economy Through Post-Consumer Recycled Packaging Innovations

Amcor provides flexible and rigid packaging solutions, including AmPrima™ recycle-ready pouches and PCR bottles/jars. In August 2025, the company upgraded its UK recycling facility to support increased use of post-consumer recycled content, and launched a 50% recycled paint container with Flügger. Its global manufacturing network and circular economy strategy reinforce its market leadership.

Huhtamaki Oyj: Advancing Sustainable Food Packaging with Mono-Material Solutions and EcoCertifications

Huhtamaki specializes in paper- and fiber-based food packaging. In July 2025, it received an EcoVadis gold medal for the fifth consecutive year, highlighting sustainability excellence. The company is developing Push Tab® blister lids, a mono-PET solution designed for full recyclability, while leveraging its global footprint for broad market impact.

ALPLA Group: Pioneering Ultra-Thin-Walled rPET Solutions to Enable Circular Economy in Packaging

ALPLA offers bottles, containers, and preforms with a focus on lightweighting and recycled materials. Its RePETec technology produces ultra-thin rPET containers in a one-step injection molding process, enabling bottle-to-cup and cup-to-bottle recycling, representing a major breakthrough in circular packaging solutions.

Greiner Packaging International GmbH: Expanding Circular Packaging Solutions Across Food, Non-Food, and Pharma Sectors

Greiner Packaging provides plastic packaging solutions for multiple industries, emphasizing sustainability through K3 cardboard-plastic combinations and reusable containers. Its Greiner strategic plan focuses on reducing environmental footprint and creating packaging with recycled content, supported by a vertically integrated model that ensures quality and compliance globally.

Thin Wall Packaging Market Share Insights, 2025-2034

Food & Beverages Secure Majority Share by Application in Thin Wall Packaging Industry

Food and beverages dominate thin wall packaging applications, accounting for nearly 70% of the market, fueled by high-volume demand across dairy, ready-to-eat meals, bakery, spreads, and frozen desserts. Thin-wall injection-molded and thermoformed containers have become the packaging standard in this sector due to their combination of material efficiency, durability, and excellent shelf presence. Lightweight designs reduce plastic usage by up to 30% compared to conventional rigid formats, aligning with both brand sustainability commitments and regulatory mandates to cut single-use plastic consumption. Their versatility allows for barrier customization, stackability, and high-quality graphics, making them attractive to major food brands and private label players. The surge in convenience-driven consumption—snack cups, portioned spreads, and meal kits—further accelerates growth. As retailers and manufacturers emphasize recyclability and PCR integration, food and beverage brands are prioritizing thin wall packaging as a cost-effective yet eco-aligned packaging solution, cementing its undisputed leadership in this industry.

Containers Retain Market Leadership by Packaging Type in Thin Wall Packaging Industry

Containers hold the largest share of the thin wall packaging industry, representing 35% of demand, due to their broad applicability across food, industrial, and personal care sectors. Their dominance is attributed to their adaptability in size (from small yogurt tubs to industrial-scale pails), rigidity for stacking and transport, and cost-efficiency for high-volume production runs. Injection-molded thin-wall containers provide superior dimensional accuracy, enabling secure closures and tamper-evident features, which are critical for both food safety and industrial durability. In the food industry, containers are the default format for dairy, spreads, ice cream, and sauces, while in industrial settings they are increasingly replacing heavier formats for lubricants, adhesives, and paints. Their strong recyclability, integration of PCR resins, and lightweight designs further enhance their sustainability profile, making them a preferred format under extended producer responsibility (EPR) regulations. The balance of functionality, cost-effectiveness, and environmental compliance ensures containers maintain a commanding position within the thin wall packaging ecosystem.

United States: Regulatory Push and Thin Wall Injection Molding Innovation

The United States thin wall packaging market is undergoing a transformation driven by stringent regulatory measures and sustainability mandates. California’s SB 54 Extended Producer Responsibility (EPR) law, which requires producers to take financial and physical responsibility for post-consumer packaging waste, is setting the tone for other states like Washington and Maryland in 2025. At the federal level, the EPA’s national recycling initiatives are spurring investments in advanced recycling infrastructure and lightweight packaging solutions. Companies such as Berry Global are leading the market shift by developing thin wall containers that integrate recycled and bio-based content to meet rising demand for eco-friendly packaging.

Technological innovation is also at the forefront. Thin wall injection molding (TWIM) allows manufacturers to produce containers with wall thicknesses below 1 mm while maintaining durability, reducing material use, and lowering costs. Meanwhile, in-mold labeling (IML) is gaining traction as a sustainable branding solution by eliminating adhesives that disrupt recycling streams. Coupled with the rise of e-commerce, which requires durable, lightweight, and space-efficient solutions, the U.S. market is expected to see rapid adoption of thin wall packaging across food, beverage, and consumer goods.

European Union: Circular Economy Regulations Driving Compostable and Refillable Solutions

The European Union thin wall packaging market is evolving under the Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. The regulation mandates minimum recycled content levels by 2030 and requires all packaging to meet at least Grade C recyclability standards. In parallel, the Ecodesign for Sustainable Products Regulation (ESPR) is pushing companies to design packaging that is durable, reusable, and repairable, directly impacting thin wall plastic containers.

The introduction of the Digital Product Passport (DPP) adds another layer of compliance, requiring transparency on material composition and recyclability. Companies such as Mondi are leveraging EU funding under Horizon Europe to pioneer bio-based and compostable thin wall packaging, including starch blends and cellulose films. With strong regulatory backing, the EU is shaping the market toward recyclable mono-material solutions, refillable systems, and advanced compostable films, making the region one of the leaders in thin wall packaging sustainability.

China: Advanced Barrier Technologies and E-commerce-Driven Demand

The China thin wall packaging market is heavily influenced by government-led sustainability reforms. Under the 14th Five-Year Plan, new rules effective June 1, 2025, require express delivery companies to adopt eco-friendly, reusable, and reduced packaging, a critical driver for the e-commerce sector. At the same time, the State Administration for Market Regulation (SAMR) has introduced updated standards like GB 4806.1 for food contact materials, emphasizing barrier safety through “complete barrier” requirements.

China is also experiencing a strong shift toward premium, high-tech packaging designs with enhanced barrier properties, anti-counterfeiting measures, and smart features. Local manufacturers, supported by government tax incentives for green technology, are scaling up production of aluminum-plastic composites and mono-material thin wall structures. Reports such as the Ellen MacArthur Foundation’s collaboration with Tsinghua University have further highlighted the urgent need to strengthen recycling systems, positioning China as both a consumer-driven and policy-driven growth hub for thin wall packaging.

India: EPR Regulations and Retail Growth Boosting Adoption

The India thin wall packaging market is being reshaped by the Plastic Waste Management (Amendment) Rules, 2024, effective April 1, 2025, which emphasize Extended Producer Responsibility (EPR) for manufacturers, importers, and brand owners. From July 1, 2025, all plastic packaging in India must be traceable through QR codes or barcodes, ensuring accountability for environmental impact. This creates strong compliance-driven momentum for recyclable and trackable thin wall packaging solutions.

India’s fast-growing e-commerce and retail sectors are further fueling demand for lightweight, durable, and space-saving packaging, particularly in food, beverages, and consumer goods. The government’s investment in reverse logistics systems also ensures that producers are responsible for post-consumer recycling and disposal, aligning thin wall packaging with India’s broader sustainability objectives. With both regulatory pressure and retail expansion, India is positioned as a fast-emerging growth market for thin wall packaging.

Japan: High-Barrier Material Innovation and Circular Economy Strategies

The Japan thin wall packaging market is transitioning rapidly under the Plastic Resource Circulation Strategy (2025), which mandates that all packaging must be reusable or recyclable. The Plastic Resource Circulation Promotion Law, also effective in 2025, enforces the reduction and redesign of single-use plastic products, accelerating the adoption of compostable and reusable thin wall formats.

Japanese companies are also pioneering advanced materials. Kuraray’s EVAL™ EVOH high-performance barrier technology enables the production of ultra-thin, lightweight multilayer structures that maintain strength and extend shelf life, while meeting sustainability targets. In addition, the MHLW’s positive list system, effective June 1, 2025, standardizes which synthetic materials are safe for food contact, ensuring compliance in food and beverage thin wall packaging. Japan’s focus on sustainable innovation and material efficiency makes it a regional leader in thin wall packaging development.

Brazil: Reverse Logistics and Domestic Waste Management Driving Growth

The Brazil thin wall packaging market is supported by the National Solid Waste Policy (PNRS), which provides a framework for responsible waste management, recycling, and reduction. The enactment of Law No. 15,088 in January 2025, banning the import of plastic waste, has accelerated reliance on domestic recycling and bio-based alternatives.

The Brazilian government is investing heavily in reverse logistics systems, requiring producers to manage the post-consumer recycling and disposal of packaging. This is fostering demand for thin wall packaging solutions that integrate recyclable or compostable materials, especially in the foodservice and retail sectors. As one of the largest producers of bio-based feedstocks, Brazil is well-positioned to expand the role of renewable resins and lightweight thin wall plastics in its domestic market.

Thin Wall Packaging Market Report Scope

Thin Wall Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$39.9 Billion

|

|

Market Size (2034)

|

$65.7 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Material (PP, PE, PS, PET, Bio-based Polymers), By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Industrial), By Packaging Type (Containers, Trays, Lids, Cups, Clamshells), By Technology (Injection Molding, Thermoforming, Extrusion)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Berry Global, Inc., Amcor plc, Huhtamaki Oyj, Greiner Packaging International, Faerch Group, Silgan Holdings Inc., Sonoco Products Company, DS Smith plc, Constantia Flexibles Group GmbH, WestRock Company, Alpla, PlastiPak Holdings, Inc., Sabic, Mondi Group, Kuraray Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Thin Wall Packaging Market Segmentation

By Material

- PP

- PE

- PS

- PET

- Bio-based Polymers

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Industrial

By Packaging Type

- Containers

- Trays

- Lids

- Cups

- Clamshells

By Technology

- Injection Molding

- Thermoforming

- Extrusion

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Thin Wall Packaging Market

- Berry Global, Inc.

- Amcor plc

- Huhtamaki Oyj

- Greiner Packaging International

- Faerch Group

- Silgan Holdings Inc.

- Sonoco Products Company

- DS Smith plc

- Constantia Flexibles Group GmbH

- WestRock Company

- Alpla

- PlastiPak Holdings, Inc.

- Sabic

- Mondi Group

- Kuraray Co., Ltd.

* List Not Exhaustive

Methodology

USDAnalytics applies a structured, data-driven methodology to analyze the global thin wall packaging market, integrating both qualitative and quantitative insights. Our research combines primary interviews with packaging manufacturers, brand owners, sustainability experts, and supply chain professionals with secondary sources including company reports, regulatory documents, trade publications, and industry news. USDAnalytics assesses technological innovations such as thin wall injection molding, thermoforming, and advanced polymer formulations, alongside sustainability initiatives including post-consumer recycled (PCR) integration, mono-material packaging, and lightweighting strategies. Regional analyses encompass market dynamics in the United States, European Union, China, India, Japan, and Brazil, considering regulatory frameworks like EPR laws, Plastic Waste Management rules, and circular economy mandates. Market sizing, CAGR forecasting, and trend evaluations are performed using historical data, material adoption rates, and emerging application opportunities across food & beverages, healthcare, personal care, and industrial sectors. This methodology ensures actionable, accurate, and strategic insights for packaging professionals, investors, and brand owners seeking competitive advantage through innovation, sustainability, and cost-effective thin wall packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.