Market Overview: Growth Anchored in Food Cans, Aerosols, and Recyclability

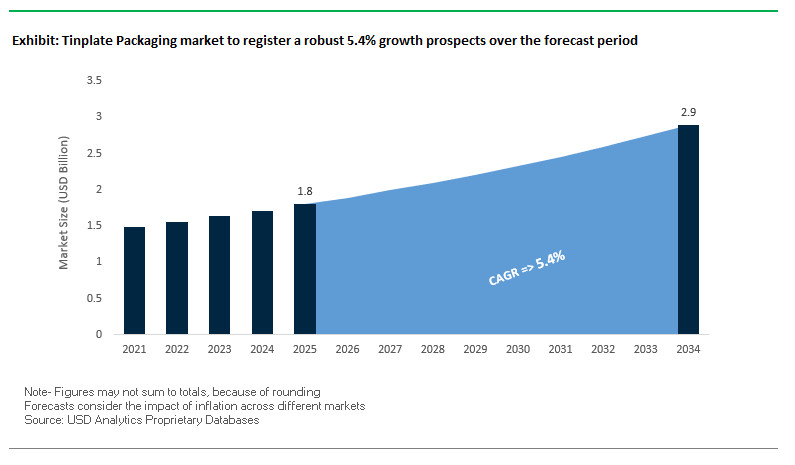

The global tinplate packaging market is projected to grow from USD 1.8 billion in 2025 to USD 2.9 billion by 2034, advancing at a healthy CAGR of 5.4%. This growth trajectory underscores the rising importance of sustainable, recyclable, and durable metal packaging across multiple industries. For buyers and industry professionals, the key question lies in how tinplate packaging can continue to balance cost efficiency, regulatory compliance, and superior product protection while meeting the growing demand for circular economy solutions.

The food and beverage sector dominates tinplate packaging, particularly through food cans, which benefit from tinplate’s excellent barrier properties that ensure product freshness and extended shelf life. Beyond food, aerosol packaging is a fast-growing segment, widely used in personal care, household goods, and paints. Tinplate’s infinite recyclability makes it increasingly attractive in a market shaped by sustainability legislation and consumer pressure for eco-friendly alternatives. Additionally, Asia-Pacific is the production and consumption hub, driven by its growing population, rapid industrialization, and surging packaged food demand.

Key Insights for Industry Professionals:

- Food & beverage leadership: Tinplate food cans remain the backbone of global demand.

- Recyclability advantage: Infinite recyclability positions tinplate as a material of choice for circular economy initiatives.

- Aerosol packaging growth: Expanding use in personal care, paints, and household goods drives adoption.

- Asia-Pacific concentration: Largest production and consumption base, with strong growth from industrial and consumer markets.

Market Analysis: Recent Developments Reshaping Global Tinplate Supply

The tinplate packaging industry is undergoing strategic realignments, partnerships, and expansions that are strengthening its global footprint.

In August 2025, Ball Corporation divested a 41% stake in its Saudi Arabia joint venture to ORG Technology for USD 70 million, streamlining its portfolio to focus on high-margin packaging. A month earlier, in July 2025, Colep Packaging acquired 60% of ALM, reinforcing its leadership in European tinplate and aluminum packaging solutions. Meanwhile, the global steel industry saw a landmark consolidation in June 2025 when Nippon Steel and U.S. Steel finalized their partnership, reshaping the supply chain for steel and tin mill products.

On the innovation front, Eviosys launched a new line of rectangular tinplate cans in Turkey (May 2025) to cater to the meat and packaged food market. Similarly, Sonoco opened its Metal Packaging Technical & Engineering Center in Ohio (May 2025) to drive R&D in steel-based food and aerosol cans. U.S. Steel announced a USD 120 million investment in March 2025 at its Gary Works hot strip mill to enhance tin mill quality.

Earlier, the trend toward consolidation was marked by Amcor’s planned acquisition of Berry Global (November 2024), which echoed similar moves in the packaging sector. Invopak’s September 2024 plant launch in Manchester, UK, to produce tinplate packaging, further highlighted the localization of supply chains to mitigate logistics risks.

Emerging Trends and Opportunities Reshaping the Tinplate Packaging Market

Strategic Investment in Domestic Production Capacity and Supply Chain Resilience

The tinplate packaging market is experiencing a wave of capital investments as governments and corporations alike focus on reducing reliance on imports and enhancing supply chain resilience. Geopolitical uncertainties and raw material disruptions have accelerated this shift, with large-scale expansions and acquisitions reshaping the industry. In India, The Tinplate Company of India Limited (Tata Steel subsidiary) has committed to boosting its production to 679,000 tons per annum, marking a decisive step toward meeting the rising domestic demand where per capita tinplate consumption remains low but is projected to surge.

This trend is reinforced by global collaborations, such as the $669 million joint venture between JSW Steel (India) and JFE Steel (Japan) aimed at electrical steel production. While not tinplate-specific, such cross-border partnerships signal a wider strategy to secure localized steel supply for packaging and industrial applications. Similarly, M&A activity is accelerating, with Mauser Packaging Solutions acquiring a tin-steel aerosol can and steel pail manufacturer in Mexico (May 2024) to strengthen its footprint across Latin America. Together, these investments highlight how tinplate producers are aligning capacity expansion with regional consumption growth and supply chain security.

Accelerated Adoption of Advanced, Sustainable Coatings and Lightweighting

Sustainability is a defining factor in the evolution of tinplate packaging, with manufacturers innovating around lightweighting, alternative coatings, and higher recycled content. Continuous annealing and material engineering techniques have enabled thinner yet stronger tinplate, reducing steel usage while cutting energy consumption in production and logistics by as much as 18%, according to can manufacturing studies. This not only lowers costs but also directly contributes to brands’ climate reduction goals.

Health and safety considerations are also shaping product design. With BPA facing global regulatory restrictions, manufacturers are transitioning to BPA-free coatings that maintain food safety and corrosion resistance while meeting stricter compliance requirements. At the same time, recycled content is gaining prominence. In Europe, steel packaging already averages 67% recycled content, with the industry actively pursuing higher levels to align with corporate ESG targets and EU Packaging and Packaging Waste Regulation (PPWR) mandates. This trend illustrates how innovation in coatings and lightweighting is securing tinplate’s position as a future-ready, sustainable packaging solution.

Capitalizing on the Circular Economy through Superior Recycling Infrastructure

Tinplate holds a unique competitive advantage as the most recycled packaging material globally, presenting an opportunity for both producers and brand owners to leverage its inherent circularity. Unlike plastic or paper, steel can be infinitely recycled without quality degradation, positioning it as a preferred solution in markets tightening Extended Producer Responsibility (EPR) schemes. For example, under new regulations in Europe and parts of North America, producers face higher compliance costs when using materials with low recycling rates, whereas tinplate offers a low-risk, cost-efficient pathway to compliance.

Energy savings further strengthen the case for tinplate. Recycling steel requires 74% less energy than producing virgin steel, reducing greenhouse gas emissions while enabling brands to showcase measurable sustainability performance. With consumer awareness of packaging sustainability at an all-time high, tinplate’s closed-loop recyclability offers an unparalleled opportunity to differentiate in sectors where sustainability credentials drive purchasing decisions.

Expansion into High-Growth Premium and Specialty Food & Beverage Segments

Beyond mass-market canned goods, premium and specialty applications are emerging as a major growth driver for the tinplate packaging market. Its superior barrier properties against oxygen and light make it ideal for sensitive, high-value foods such as gourmet coffee, olive oil, and caviar, where maintaining product integrity is critical. Luxury positioning is reinforced by tinplate’s versatility in branding, offering high-quality surfaces suitable for embossing, lacquering, and intricate printing that enhance shelf appeal and consumer recall.

Tinplate is also gaining ground in non-food premium categories such as cosmetics, candles, and dry fruits, where aesthetics and durability are critical to brand positioning. A tin container’s perceived premium value and reusability resonate with consumers seeking both quality and sustainability, giving brands a way to justify higher price points. With the global shift toward premiumization in consumer goods, tinplate packaging is well-positioned to capture new market share by blending functionality, durability, and luxury appeal.

Competitive Landscape: Leading Companies in the Global Tinplate Packaging Market

The global tinplate packaging market is highly competitive, with leading companies focusing on steel partnerships, sustainability initiatives, decorative innovation, and geographic expansion. Market leaders are building resilience through investments in circular economy models and regional production networks.

Nippon Steel Corporation: Expanding Global Reach Through U.S. Steel Partnership

Nippon Steel is a leading producer of tinplate products such as electrolytic tinplate (ETP) and tin-free steel (TFS). Its June 2025 partnership with U.S. Steel expands its North American presence and enhances its tinplate capabilities. Known for advanced production techniques and high-quality surface finishes, Nippon Steel supports food, beverage, and industrial packaging markets. Its long-term strategy focuses on carbon-neutral steelmaking, aligning with tightening environmental mandates.

Crown Holdings Inc.: Innovating with Decorative and Aerosol Tinplate Packaging

Crown is a top global supplier of tinplate food cans, decorative tins, and aerosol packaging. Its innovations include HoloCrown holographic tins and Seated Ends, which provide premium aesthetics. With 189 plants in 39 countries, Crown has a robust global footprint and serves growing markets in North America and Asia-Pacific. The company is strategically positioned to deliver sustainable and high-performance tinplate packaging solutions.

Silgan Holdings Inc.: Leading Metal Food Container Supplier in North America

Silgan is the largest manufacturer of metal food containers in North America, producing containers for pet food, vegetables, soups, and proteins. Operating 39 facilities across North America, Europe, and Asia, Silgan ensures proximity to global customers. Its strengths lie in its low-cost production model and multi-year contracts with major food brands, giving it a stable market presence.

Ardagh Group S.A.: Driving Circular Economy Through Metal and Glass Packaging

Ardagh, through its subsidiary Ardagh Metal Packaging (AMP), is a major supplier of tinplate and aluminum cans. Its 42% stake in Trivium Packaging enhances its presence in specialty food and consumer markets. Operating 58 facilities in 16 countries, Ardagh’s strategy centers on circular economy principles, producing infinitely recyclable metal and glass packaging with a focus on Europe, North America, and Brazil.

Ball Corporation: Streamlining Portfolio and Strengthening Core Metal Packaging

Ball Corporation, widely known for aluminum cans, also plays a significant role in tinplate packaging. In August 2025, it sold its stake in a Saudi joint venture to reallocate capital to core businesses. Ball is known for technological innovation in sustainable packaging and continues to expand through acquisitions such as Florida Can Manufacturing (2025) and Alucan Entec (2024). Its disciplined approach to investment ensures a strong presence in metal packaging innovation and sustainability.

Tinplate Packaging Market Share Insights

Cans Drive Tinplate Packaging Market Share by Product Type

Cans represent 65% of the tinplate packaging market in 2025, dominating as the material of choice for global food and beverage preservation. Their superior barrier against oxygen, light, and moisture, combined with long shelf-life performance, makes them indispensable for canned vegetables, seafood, meats, carbonated beverages, and beer. The segment continues to evolve with innovations such as easy-open ends, resealable formats, and shaped cans that enhance convenience and differentiation. Containers, holding 15%, thrive in premium food, confectionery, and gift packaging, leveraging tinplate’s strength and decorative finish to elevate shelf appeal. Lids, closures, drums, and pails maintain essential but smaller shares, each addressing specialized markets such as hermetic sealing for baby food, corrosion resistance in paints, and safe handling of industrial chemicals. The enduring dominance of cans reflects the synergy of mass-volume consumption, consumer trust, and recyclability-driven sustainability narratives.

Food & Beverages Anchor Tinplate Packaging Market Share by Application

Food and beverages account for 70% of tinplate packaging applications in 2025, underscoring their central role in this industry. Tinplate’s ability to withstand retort sterilization processes, extend shelf life for years, and preserve nutritional quality makes it the gold standard for canned food and beverage packaging. The rise of convenience-based consumption, ready-to-drink beverages, and globalized food supply chains keeps this segment unmatched in scale. Paints and coatings maintain a strong position due to tinplate’s solvent resistance and durability, while chemicals and lubricants rely on its barrier strength for purity and safety. Personal care and cosmetics represent a premium niche, leveraging the material’s tactile weight and high-end printing capability to signal luxury and sustainability. This segmentation highlights how food and beverages secure the lion’s share, while paints, chemicals, and cosmetics expand tinplate packaging into diverse, high-value markets.

United States: Sustainability, M&A Activity, and Technological Advances Reshape the Tinplate Packaging Market

The U.S. tinplate packaging market is evolving rapidly, shaped by changing consumer preferences, sustainability mandates, and advanced manufacturing technologies. One of the biggest drivers is the rising demand for shelf-stable and ready-to-eat foods, where tinplate packaging is preferred due to its superior barrier properties that preserve food quality and extend shelf life. A notable development is the industry’s focus on recyclable materials, as tinplate is 100% recyclable without loss of quality, which aligns with both corporate sustainability goals and stringent state-level regulations.

Technological innovation is another defining factor, with companies like Sonoco Products Co. investing in cutting-edge research and development. Its 11,000-square-foot Metal Packaging Technical & Engineering Center in Ohio demonstrates the sector’s emphasis on automation, digitalization, and collaboration with brand owners to advance sustainable packaging. Additionally, mergers and acquisitions (M&A) are shaping market dynamics, with Colep Packaging’s acquisition of a 60% stake in ALM highlighting the growing importance of tinplate in the aerosol and global metal packaging industry. Together, these trends are pushing the U.S. market toward innovation-driven and sustainability-focused growth.

Germany: Eco-Design Leadership and Regulatory Pressure Drive Tinplate Packaging Innovation

The German tinplate packaging market operates under one of the strictest regulatory environments in Europe, heavily influenced by the EU Packaging and Packaging Waste Regulation (PPWR). These policies are accelerating the demand for eco-friendly, recyclable tinplate solutions and driving companies to redesign packaging with sustainability at its core. Germany has also emerged as a leader in the circular economy, fostering collaborations between manufacturers, recyclers, and end-users to increase recycled content and improve recyclability rates in tinplate products.

A key development shaping the German market is the adoption of eco-design strategies, particularly the removal of Bisphenol A (BPA) from food can linings and the introduction of alternative coatings to improve both safety and environmental performance. Furthermore, the upcoming ban on Cr(VI)-based chemicals for tinplate passivation from 2028 represents a significant challenge and opportunity for innovation in surface coating technologies. These combined factors are pushing German manufacturers to set new global benchmarks for safe, recyclable, and regulation-compliant tinplate packaging solutions.

China: Industrial Expansion and Green Transformation Propel Tinplate Packaging Market Growth

The China tinplate packaging market is experiencing strong momentum, supported by the country’s vast industrial base and rapid growth in food, beverage, and chemical production. As a global hub for mass manufacturing, China’s demand for durable and reliable packaging solutions continues to rise. At the same time, government-led initiatives are reshaping the sector, particularly under China’s “dual carbon” goals to achieve carbon peak and neutrality. These policies are driving the green transformation of logistics and express delivery industries, pushing tinplate packaging producers to adopt eco-friendly, reduced, and reusable designs.

Strategic acquisitions are also reshaping China’s market structure. A landmark example is China Baowu Steel Group’s acquisition of CPMC Holdings, one of the country’s largest metal packaging companies. This move strengthens Baowu’s customer base and enhances profitability, while consolidating the industry to meet domestic and international demand more efficiently. Combined with regulatory pressure for sustainability, China’s manufacturing scale, government backing, and corporate consolidation are positioning it as a powerhouse in the global tinplate packaging industry.

India: Domestic Production, Circular Economy, and E-commerce Expansion Fuel Tinplate Packaging Demand

India’s tinplate packaging market is undergoing significant expansion, strongly supported by government initiatives such as “Make in India” and “Zero Effect Zero Defect”, which promote quality manufacturing and encourage foreign and domestic investments. A major development is the expansion in local production, highlighted by the Tinplate Company of India (TCIL), a Tata Steel subsidiary, signing an MoU with the Jharkhand government to establish a US$ 204.2 million tinplate manufacturing facility in Jamshedpur, set for commissioning in 2026. This move is expected to enhance India’s self-reliance in high-quality packaging.

At the demand side, the e-commerce boom in India, particularly in the food and beverage sector, has significantly increased the need for safe, hygienic, and durable tinplate packaging. Simultaneously, the industry is embracing the circular economy model with pioneering initiatives like Tata Steel and TCIL’s tin can recycling program, which has created a complete supply chain for collection, shredding, and recycling used cans. These advancements not only reduce environmental risks from reused cans but also establish India as a market progressing toward sustainable and future-ready tinplate packaging solutions.

Tinplate Packaging Market Report Scope

Tinplate Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$2.9 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Cans, Containers, Lids & Closures, Drums & Pails, Other Products), By Thickness (Less than 0.15 mm, 0.15 mm to 0.30 mm, More than 0.30 mm), By Application (Food & Beverages, Paints & Coatings, Chemicals & Lubricants, Personal Care & Cosmetics, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ArcelorMittal, Tata Steel, Nippon Steel Corporation, JFE Steel Corporation, Ball Corporation, CPMC Holdings Limited, Eviosys, Crown Holdings Inc., Sonoco Products Company, Silgan Holdings Inc., Colep Packaging, Hindustan Tin Works Ltd., BWAY Corp., Kaira Can Company Limited, Toyo Kohan Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tinplate Packaging Market Segmentation

By Product Type

- Cans

- Containers

- Lids & Closures

- Drums & Pails

- Other Products

By Thickness

- Less than 0.15 mm

- 0.15 mm to 0.30 mm

- More than 0.30 mm

By Application

- Food & Beverages

- Paints & Coatings

- Chemicals & Lubricants

- Personal Care & Cosmetics

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Tinplate Packaging Market

- ArcelorMittal

- Tata Steel

- Nippon Steel Corporation

- JFE Steel Corporation

- Ball Corporation

- CPMC Holdings Limited

- Eviosys

- Crown Holdings Inc.

- Sonoco Products Company

- Silgan Holdings Inc.

- Colep Packaging

- Hindustan Tin Works Ltd.

- BWAY Corp.

- Kaira Can Company Limited

- Toyo Kohan Co., Ltd.

*List not Exhaustive

Research Coverage

This in-depth report by USDAnalytics investigates the global tinplate packaging market, highlighting breakthroughs in sustainable coatings, lightweighting, and high-performance metal packaging solutions. The analysis reviews market dynamics, including the dominance of food cans, growing adoption in aerosol packaging, and the strategic expansion of production capacity across key regions. The report highlights innovations in circular economy models, recycling infrastructure, and regulatory-compliant BPA-free coatings, demonstrating how tinplate packaging continues to balance durability, cost-efficiency, and eco-friendliness. It also examines the competitive landscape, showcasing mergers, acquisitions, and strategic partnerships that are reshaping global supply chains and regional manufacturing capabilities. This report is an essential resource for manufacturers, brand owners, and supply chain professionals seeking insights into evolving consumer preferences, regulatory mandates, and premiumization trends, while also providing actionable guidance on leveraging tinplate’s recyclability and barrier properties for both mass-market and specialty applications. By combining historical performance from 2021 to 2024 with forecasts to 2034, USDAnalytics equips decision-makers with data-driven insights to optimize production, supply chain, and product development strategies in this rapidly evolving market.

Scope Highlights:

- Segmentation: By Product Type (Cans, Containers, Lids & Closures, Drums & Pails, Other Products); By Thickness (Less than 0.15 mm, 0.15 mm to 0.30 mm, More than 0.30 mm); By Application (Food & Beverages, Paints & Coatings, Chemicals & Lubricants, Personal Care & Cosmetics, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024; forecast data from 2025 to 2034.

- Companies Covered: Analysis/profiles of 15+ companies including ArcelorMittal, Tata Steel, Nippon Steel Corporation, JFE Steel Corporation, Ball Corporation, CPMC Holdings Limited, Eviosys, Crown Holdings Inc., Sonoco Products Company, Silgan Holdings Inc., Colep Packaging, Hindustan Tin Works Ltd., BWAY Corp., Kaira Can Company Limited, Toyo Kohan Co., Ltd.

Methodology

The research methodology for this report integrates a combination of primary and secondary approaches to deliver a comprehensive understanding of the tinplate packaging market. Primary insights were gathered from interviews with industry executives, R&D managers, and supply chain specialists, while secondary data was sourced from corporate reports, regulatory filings, trade publications, and sustainability disclosures. Market sizing and forecasting were conducted using a top-down approach, triangulating historical production, consumption trends, and regional demand patterns across product types and applications. Competitive benchmarking focused on mergers, acquisitions, partnerships, and technological innovation among leading producers. Emerging trends such as lightweighting, advanced coatings, BPA-free formulations, and circular economy adoption were assessed using scenario analysis and adoption modeling. This methodology ensures that the report captures both macroeconomic drivers and granular operational insights, providing industry professionals with actionable intelligence for investment, strategic planning, and sustainability-driven product development.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.