Trimethylgallium Market Overview 2025–2034: $161.2 Million to $239.6 Million at 4.5% CAGR Accelerated by 7N Purity Upgrades, MicroLED Scaling, and Semiconductor Localization

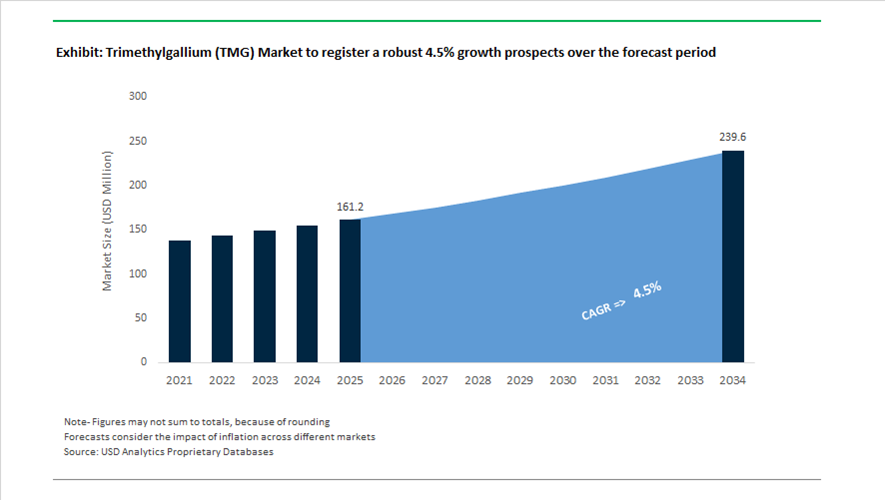

The global Trimethylgallium (TMGa) market is valued at $161.2 million in 2025 and is projected to reach $239.6 million by 2034, registering a CAGR of 4.5%. Trimethylgallium is a critical metalorganic precursor used in MOCVD (Metal-Organic Chemical Vapor Deposition) processes for manufacturing compound semiconductors including GaN (gallium nitride), GaAs (gallium arsenide), power electronics, RF devices, MicroLED displays, and silicon photonics components. Demand is being shaped by 5G and emerging 6G infrastructure, electric vehicle power modules, advanced display technologies, and national semiconductor self-sufficiency programs. The market is increasingly defined by ultra-high purity requirements, supply chain localization, and compliance with stringent environmental controls governing volatile organometallic compounds.

Capacity expansion and purity advancement accelerated throughout 2025. In mid-2025, Jiangsu Nata Opto-electronic Material ramped up its high-purity organometallic production facility in China, targeting 6N and 7N grade TMGa to support domestic semiconductor manufacturing under China’s localization initiatives. In late 2025, Merck announced the successful doubling of its metalorganic source production capacity, including specialized TMGa lines aimed at electric vehicle and high-efficiency power electronics applications. During the third quarter of 2025, leading global manufacturers reported commercial-scale attainment of 7N (99.99999%) purity levels, a critical milestone for fabricating high-frequency 5G and 6G base station components. In late 2025, a laboratory facility in Trombay, Mumbai, achieved indigenous production of 5N (99.999%) TMGa, aligning with India’s semiconductor mission to reduce import dependency for high-purity precursors.

Regulatory and trade dynamics further reshaped supply strategies. The 2024 Global Environmental Accord introduced stricter VOC emission controls, compelling TMGa producers to invest in advanced containment, distillation, and purification systems, increasing operating costs by approximately 18–22% in regulated markets. In late 2025, new U.S. tariff adjustments on select organometallic imports prompted semiconductor manufacturers to accelerate near-shoring and domestic precursor qualification programs to secure resilient supply chains. In 2025, AkzoNobel consolidated its high-purity organometallic operations, maintaining leadership with more than 30% share in the high-purity TMGa segment through centralized semiconductor-focused R&D and distribution. Early 2025 also saw Umicore intensify its strategic emphasis on compound semiconductor precursors under its Specialty Materials pillar, reinforcing its role in next-generation display and wireless communications materials.

Technology breakthroughs in 2026 reinforced long-term demand fundamentals. In January 2026, imec and Veeco demonstrated successful integration of barium titanate thin films on silicon photonics platforms, enabling hybrid semiconductor architectures that combine gallium-based epitaxy with high-speed optical modulators. In February 2026, LED chip manufacturing reports confirmed rapid scaling of MicroLED technology for smartwatches and premium television displays. MicroLED fabrication requires significantly higher volumes of ultra-high-purity gallium precursors compared to conventional LED production, strengthening structural demand for electronics-grade TMGa.

Technology-Led Demand Inflection and Purity-Critical Opportunities in the Trimethylgallium (TMGa) Market

Industrial-Scale Migration to 200 mm GaN-on-SiC Platforms for 800V and 1,200V EV Powertrains

The Trimethylgallium market is entering a structurally higher demand phase as the automotive industry transitions from 400V electrical architectures toward 800V and 1,200V systems to enable ultra-fast charging, higher power density, and reduced energy losses. This shift is fundamentally anchored in the rapid adoption of Gallium Nitride grown on Silicon Carbide substrates, where TMGa remains the indispensable gallium precursor for Metalorganic Chemical Vapor Deposition reactors. As wafer diameters scale from 150 mm to 200 mm, the gallium consumption per reactor cycle increases materially, amplifying volume demand for ultra-high-purity TMGa.

Large-scale infrastructure investments are accelerating this trend. The completion of Wolfspeed’s John Palmour Manufacturing Center in North Carolina, representing a $5 billion capital commitment to 200 mm SiC wafer production, has redefined substrate availability for GaN epitaxy in power electronics. This facility alone expands addressable epitaxial surface area by more than 75% compared to legacy fabs, directly increasing the intensity and continuity of TMGa supply requirements.

In parallel, Asian and Japanese device manufacturers are moving toward deep vertical integration. Mitsubishi Electric’s completion of its 8-inch SiC manufacturing facility in November 2025 signals a decisive move toward internalized wide-bandgap semiconductor production. For TMGa suppliers, this changes procurement behavior from spot purchasing to long-duration capacity reservation contracts, favoring producers with redundant purification, cylinder management, and logistics capabilities capable of supporting uninterrupted, high-throughput vertical MOCVD operations.

MicroLED Commercialization Drives a Structural Shift Toward 7N and Sub-Particle Purity TMGa

Beyond power electronics, MicroLED technology is emerging as a second major demand pillar reshaping the Trimethylgallium market. As MicroLED transitions from pilot lines into early commercial manufacturing for AR, VR, and large-format displays, precursor consistency has become a yield-determining variable rather than a background input. Each MicroLED panel contains millions of microscopic emitters, where even trace metallic or oxygen contamination in TMGa can translate into dead pixels, wavelength drift, or color non-uniformity across tiled displays.

By late 2025, multiple Asian fabs including ENNOSTAR in Taiwan, HC SemiTek, and Sanan Optoelectronics in China had entered volume ramp-up phases for MicroLED production. These facilities increasingly specify 7N purity TMGa with tightly controlled particle counts, moisture levels, and batch-to-batch reproducibility. This requirement is structurally different from industrial GaN power device demand, creating a distinct premium segment within the TMGa market focused on optical performance rather than electrical robustness alone.

Investment momentum reinforces this trajectory. Despite earlier project recalibrations across the AR sector, MicroLED-focused capital inflows increased by an estimated 10 to 15% in 2025. Mojo Vision’s $75 million funding round to advance a 300 mm GaN-on-silicon MicroLED platform exemplifies this shift. Such platforms depend on TMGa to grow ultra-dense blue and green emitters with nanometer-level thickness control, further elevating the value of precision-engineered gallium precursors.

Opportunity: Photonic-Grade Trimethylgallium for AI-Driven Silicon Photonics and LiDAR

One of the most strategically significant opportunities for the Trimethylgallium market lies in the rapid expansion of silicon photonics driven by artificial intelligence data centers and high-speed optical interconnects. As data rates exceed the limits of copper, Photonic Integrated Circuits are becoming essential for reducing latency, power consumption, and heat generation in hyperscale computing environments. These devices rely on III-V compound layers such as InGaP and AlGaInP, where TMGa purity directly influences optical loss, laser efficiency, and long-term device stability.

Industry insights from late 2025 indicate that photonic devices exhibit extreme sensitivity to metallic contamination, with even parts-per-billion impurities capable of increasing scattering losses in waveguides and degrading laser coherence. This is driving demand for photonic-grade TMGa featuring near-zero particle counts, advanced filtration down to parts-per-trillion thresholds, and validated impurity analytics. Suppliers capable of meeting these specifications are positioning themselves as strategic partners rather than commodity vendors within the semiconductor value chain.

Automotive sensing further strengthens this opportunity. As Advanced Driver Assistance Systems move toward Level 3 and Level 4 autonomy, GaN-based LiDAR systems are gaining traction for their high-frequency switching and thermal resilience. These applications require defect-free epitaxial layers, reinforcing demand for ultra-clean TMGa in safety-critical optical sensing platforms.

Opportunity: Specialized Gallium Precursors for Gallium Oxide and ALD-Driven 3D Architectures

A second high-growth opportunity is emerging beyond conventional MOCVD applications as the semiconductor industry adopts Atomic Layer Deposition for increasingly complex three-dimensional device architectures. While TMGa remains effective for thick GaN layers, its thermal characteristics limit its suitability for low-temperature ALD processes required in advanced logic and memory nodes. This creates a market gap for next-generation gallium precursors optimized for conformal deposition and enhanced thermal stability.

Gallium Oxide is gaining attention as an ultra-wide-bandgap material capable of operating at electric fields far beyond GaN or SiC, making it attractive for extreme-voltage power electronics. Government-backed research programs in the United States and Japan in 2025 are actively exploring plasma-enhanced ALD routes for Ga₂O₃ deposition, where traditional TMGa chemistry faces volatility and decomposition constraints. This opens a pathway for alternative organometallic gallium compounds with higher vapor pressure, lower decomposition temperature, and improved safety profiles.

At the same time, logic nodes below 3 nm are driving demand for gallium-containing barrier layers and gate materials in three-dimensional transistor stacks. With the global ALD and CVD precursor market projected to reach $6.56 billion in 2025, precursor manufacturers that can deliver oxygen-free, safer-to-handle gallium chemistries stand to capture high-margin positions in advanced logic, memory, and heterogeneous integration segments currently dominated by silicon and titanium-based processes.

Trimethylgallium Market Share and Segmentation Insights

Purity Grade Market Share: Ultra-High Purity Grade Leads with Semiconductor and Epitaxy Requirements

Ultra-high purity trimethylgallium dominates the market with a 68.40% share in 2025, driven by stringent quality requirements in semiconductor manufacturing, LED epitaxy, and advanced optoelectronics. Applications such as MOCVD processes demand impurity levels at parts-per-billion to ensure high device performance, yield, and reliability. High-purity grade serves less critical applications with moderate specifications. A key market trend is the tightening of purity standards linked to advanced semiconductor packaging and 3D integration, where even trace contaminants such as oxygen and metallic impurities can significantly impact device efficiency, accelerating demand for ultra-high purity precursors in high-performance electronics manufacturing.

Application Market Share: LED Production Dominates with GaN-Based Device Manufacturing

LED production accounts for 48.60% of the trimethylgallium market in 2025, supported by the widespread use of gallium nitride materials in lighting, display technologies, and automotive lighting systems. Trimethylgallium is a key precursor in MOCVD processes used to grow high-quality GaN epitaxial layers. Semiconductor manufacturing, optoelectronics, solar cell production, and nanotechnology represent additional application segments with growing demand. A major growth driver is the emergence of MicroLED technology, which requires precise control over material composition and thickness, increasing demand for high-purity trimethylgallium and expanding its role in next-generation display and optoelectronic applications.

Trimethylgallium Market Competitive Landscape

The Trimethylgallium market in 2026 is defined by epitaxial integration, ultra-high-purity precursor delivery systems, and geographically diversified megasites that reduce logistics risk for pyrophoric materials while meeting zero-defect semiconductor yield requirements across advanced logic, MicroLED, and power electronics applications.

Merck KGaA Expands Kaohsiung Megasite to Lead High-Purity TMGa Innovation

Merck KGaA is reinforcing its dominance in the Trimethylgallium market through its “Level Up” strategy and large-scale semiconductor megasite investments. The €500 million Kaohsiung facility, spanning 150,000 m², is set to reach full-scale production in 2026, supplying thin-film materials and specialty gases for AI-driven semiconductor manufacturing. The company reported €21.1 billion in FY2025 sales with a strong 28.9% EBITDA margin, reflecting high profitability in advanced precursor segments. Merck is intensifying R&D on proprietary MOCVD precursors to enable uniform GaN epitaxial layers critical for MicroLED displays and 5G/6G infrastructure. Its 2026 outlook projects stable revenues despite forex pressures, supported by sustained semiconductor demand. The integrated precursor-and-delivery model enhances contamination control and strengthens its position in zero-defect fabrication environments.

Nouryon Strengthens Organometallic Leadership with Green Synthesis and Supply Chain Resilience

Nouryon is maintaining a strong position in the Trimethylgallium market through its leadership in metal alkyls and advanced organometallic chemistry. The company supplies high-purity TMGa and trimethylaluminum using its expertise in handling pyrophoric materials, ensuring safe and reliable delivery to semiconductor fabs. Its transition toward green synthesis pathways is reducing carbon intensity in energy-intensive alkylation processes, aligning with sustainability mandates. Recognition for supply chain excellence in 2026 highlights its robust logistics network, a critical differentiator in the transport of hazardous semiconductor precursors. Nouryon is also expanding into life sciences and sensor technologies, where TMGa-enabled components support advanced diagnostics and smart medical devices. This diversified application focus enhances long-term demand visibility and strengthens its specialty materials positioning.

Entegris Drives Ultra-Clean TMGa Delivery Systems for Advanced Semiconductor Nodes

Entegris is positioning itself as a critical enabler in the Trimethylgallium market by integrating high-purity chemistry with advanced fluid management systems. The company reported Q4 2025 sales of $824 million, supported by strong demand for selective etch and CMP consumables in complex semiconductor architectures. Its newly introduced electrostatic charge mitigation system ensures safe and contamination-free delivery of TMGa, preserving precursor integrity during canister-to-chamber transfer. A $700 million R&D investment in the U.S., including a new Illinois technology center, is accelerating innovation aligned with CHIPS Act-driven localization. Entegris’ 2026 EBITDA guidance of 26.5%–27.5% reflects strong margin performance in specialty semiconductor materials. Its solutions are critical for foundries deploying 3D transistor architectures and gallium-based epitaxial layers.

Sumitomo Chemical Accelerates Green TMGa Strategy and Semiconductor Expansion

Sumitomo Chemical is advancing its role in the Trimethylgallium market through strategic investment in ICT and mobility-driven semiconductor materials. The company is allocating 80% of its capital toward high-growth sectors, targeting an 11% ROIC in ICT & Mobility by 2027. Its acquisition of a Taiwanese semiconductor chemicals firm strengthens its footprint in the global semiconductor hub and enhances localized precursor production capabilities. Sumitomo is leveraging its GX (Green Transformation) platform to develop low-carbon TMGa solutions, including CO2 recovery integration for sustainable manufacturing. The company is capitalizing on its 2024 recovery momentum to generate 200 billion yen in cash between 2025 and 2027, funding expansion in high-purity organometallics. This strategy aligns with increasing demand for GaN-based power electronics and advanced display technologies.

UBE Corporation Refocuses on Electronic-Grade Chemicals and Semiconductor Supply Chains

UBE Corporation is reshaping its competitive position in the Trimethylgallium market by transitioning fully toward specialty electronic materials. The company is exiting commodity chemicals, including cyclohexanone and caprolactam production, to prioritize high-margin semiconductor and battery material segments. Capacity expansion in high-purity nitric acid and related chemicals supports a broader electronic-grade portfolio integrated with organometallic precursor lines. Collaboration with Tohoku University through its Co-creation Research Institute is accelerating innovation in MicroLED and power semiconductor materials. UBE’s planned U.S. manufacturing facility in 2026 strengthens its localized supply chain strategy, supporting semiconductor and EV ecosystem growth. This structural transformation enhances its competitiveness in high-purity precursor markets requiring stringent quality and regional supply reliability.

China Trimethylgallium Market Driven by Localization Mandates and Display–RF Convergence

China has positioned Trimethylgallium as a strategically sensitive metalorganic precursor under its semiconductor self-reliance agenda. In 2025, the Integrated Circuit Industry Investment Fund Phase III, widely referred to as “Big Fund III,” prioritized localization of high-purity MO sources, explicitly targeting a 20% increase in domestic TMG output to reduce dependence on Western suppliers. This policy push coincides with China hosting the world’s largest installed base of MOCVD systems by late 2025, with new expansion phases announced in Zhejiang and Guangdong that together require more than 300 tons of electronic-grade TMG annually for LED, GaN-on-Si, and RF device fabrication.

Downstream demand is broadening rapidly. Pilot Micro-LED production lines launched in 2025 by BOE and TCL are using tailored TMG grades for high-uniformity epitaxial growth on 8-inch wafers. At the regulatory level, the Ministry of Industry and Information Technology enforced new 2025 green manufacturing standards for organometallic synthesis, compelling legacy plants to implement closed-loop gallium recovery. Simultaneously, tighter export licensing for gallium-related materials has effectively prioritized domestic suppliers such as Nata Opto-electronic, while the nationwide rollout of 5G-Advanced (5.5G) infrastructure in 2025 has lifted demand for TMG-based RF front-end modules and high-frequency power amplifiers.

South Korea Trimethylgallium Market Anchored in Purity Standards and AR/VR Displays

South Korea’s Trimethylgallium market is shaped by a national focus on compound semiconductors and extreme purity control. In late 2025, the government unveiled a ₩260.1 billion strategy extending through 2031 to strengthen GaN and SiC ecosystems, formally designating TMG as a core strategic material. This policy alignment has reinforced captive demand from display and wafer manufacturers transitioning to next-generation architectures.

In 2025, Samsung Display and LG Display shifted OLED-on-Silicon (OLEDoS) development toward TMG-enhanced epitaxy for AR and VR devices. Parallel investments by SK Siltron to expand SiC and GaN wafer capacity have further tightened requirements for ultra-pure TMG. Academic and regulatory reinforcement is notable. A 2025 government-funded program at Yonsei University demonstrated a 7.5N purity TMG purification process using low-temperature distillation, targeting commercialization by 2027. Meanwhile, the Korean Agency for Technology and Standards updated impurity thresholds in 2025, mandating sub-5 ppb silicon and magnesium levels for TMG used in high-performance RF chips.

United States Trimethylgallium Market Focused on Supply Chain Security and Power Electronics

The United States TMG market is increasingly defined by resilience, defense priorities, and power semiconductor adoption. Under Phase II of the CHIPS and Science Act, the U.S. Department of Commerce allocated new 2025 grants to strengthen specialty chemical supply chains, directly supporting domestic TMG producers such as Albemarle and Indium Corporation. These initiatives aim to de-risk reliance on imported metalorganic sources amid tightening global trade controls.

Demand growth is increasingly tied to GaN-on-silicon power devices. In mid-2025, U.S. semiconductor firms launched high-volume pilot lines for GaN power transistors used in EV fast-charging infrastructure, materially increasing consumption of power-grade TMG. From a strategic standpoint, the Defense Logistics Agency highlighted in a 2025 report the need for national stockpiles of gallium precursors, including TMG, to safeguard aerospace radar and defense electronics supply chains. Regulatory oversight is also tightening, with new 2026 reporting obligations under the Environmental Protection Agency TSCA Section 8(a) framework requiring detailed life-cycle tracking of organometallic gallium compounds.

Japan Trimethylgallium Market Oriented Toward Next-Generation Communications and ESG Compliance

Japan’s Trimethylgallium market is characterized by high-value specialization and strategic M&A. In 2025, Sumitomo Chemical reorganized its specialty chemicals division to prioritize next-generation electronic materials, raising TMG production efficiency at domestic sites to remain competitive against expanding Chinese output. This strategic pivot was reinforced in November 2025 through an agreement to acquire a Taiwanese semiconductor process chemical firm, expanding Sumitomo’s purification and distribution footprint within the Hsinchu Science Park ecosystem.

Technology pull is intensifying. The Ministry of Internal Affairs and Communications funded a 2026 pre-standardization lab focused on 6G, where TMG-based terahertz emitters and sensors are core materials. On the sustainability front, Mitsubishi Gas Chemical finalized late-2025 agreements for low-carbon methanol feedstocks to support the production of ESG-compliant “Green TMG,” aligning with the procurement requirements of global semiconductor foundries.

India Trimethylgallium Market at an Early Inflection Point in Semiconductor Localization

India’s Trimethylgallium market remains nascent but strategically significant as the country builds a domestic semiconductor base. In September 2025, the unveiling of India’s first fully indigenous 32 nm chip marked a symbolic milestone, signaling future demand for localized TMG supply chains as fabrication scales between 2026 and 2027. While current consumption volumes are limited, policy direction is clear.

The India Semiconductor Mission expanded its Chips to Startup initiative in 2025 to include training modules in organometallic synthesis, addressing a projected shortfall of 1.2 million skilled engineers by 2026. At the ecosystem level, commitments announced during Semicon India 2025 led major global MO source suppliers to sign MOUs for feasibility studies on TMG purification and filling facilities in the Dholera Special Investment Region. These moves position India as a future secondary hub for Trimethylgallium once wafer fabrication capacity matures.

Comparative Snapshot: Trimethylgallium Market by Country

Trimethylgallium (TMG) Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Emphasis

|

Market Character

|

|

China

|

LED, Micro-LED, 5.5G RF

|

Localization and scale

|

Volume-led, policy-driven

|

|

South Korea

|

AR/VR displays, RF chips

|

Ultra-high purity

|

Precision-focused

|

|

United States

|

GaN power, defense

|

Supply chain security

|

Resilience-oriented

|

|

Japan

|

6G, advanced electronics

|

ESG and M&A-led

|

High-value specialization

|

|

India

|

Emerging fabs

|

Capability building

|

Early-stage, strategic

|

Trimethylgallium (TMG) Market Report Scope

Trimethylgallium (TMG) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$161.2 Million

|

|

Market Size (2034)

|

$239.6 Million

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Purity Grade (High-Purity Grade, Ultra-High Purity Grade), By Application (LED Production, Semiconductor Manufacturing, Solar Cell Production, Optoelectronics, Nanotechnology), By End-Use Industry (Consumer Electronics, Telecommunications, Automotive, Aerospace and Defense, Renewable Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nouryon, Merck KGaA, Sumitomo Chemical Company Limited, Albemarle Corporation, Jiangsu Nata Opto Electronic Material Co. Ltd., Umicore SA, Indium Corporation, Dow Inc., Air Liquide SA, Mitsubishi Gas Chemical Company Inc., Taiyo Nippon Sanso Corporation, American Elements, Jiujiang Tanbre Co. Ltd., Tosoh Corporation, Gelest Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Trimethylgallium Market Segmentation

By Purity Grade

- High-Purity Grade

- Ultra-High Purity Grade

By Application

- LED Production

- Semiconductor Manufacturing

- Solar Cell Production

- Optoelectronics

- Nanotechnology

By End-Use Industry

- Consumer Electronics

- Telecommunications

- Automotive

- Aerospace and Defense

- Renewable Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Trimethylgallium Market

- Nouryon

- Merck KGaA

- Sumitomo Chemical Company Limited

- Albemarle Corporation

- Jiangsu Nata Opto Electronic Material Co. Ltd.

- Umicore SA

- Indium Corporation

- Dow Inc.

- Air Liquide SA

- Mitsubishi Gas Chemical Company Inc.

- Taiyo Nippon Sanso Corporation

- American Elements

- Jiujiang Tanbre Co. Ltd.

- Tosoh Corporation

- Gelest Inc.

*- List not Exhaustive